10-Year Winners, 5-Year Losers: Are These S-REITs Ready for a Comeback?

Three Singapore REITs show 86%+ decade gains but red five-year returns—is this the mean reversion setup savvy investors have been waiting for?

Editor’s Note: This post has been updated on October 19, 2025, to ensure it is fresh and accurate, and now includes the latest analysis on S-REIT performance and their mean reversion potential.

Here’s the investor puzzle keeping many of us up at night: How do you spot quality that’s been beaten down versus a genuine decline? Right now, three Singapore REITs are flashing exactly this signal. DrWealth just uncovered something fascinating—Frasers Logistics & Commercial Trust, Mapletree Industrial Trust, and Mapletree Logistics Trust all delivered at least 86% gains over ten years, yet all three posted negative returns over the past five years. If you’ve been watching these names sink while knowing their long-term track record, you’re probably torn between FOMO and caution. Are these trusts just casualties of a brutal rate cycle, or are we looking at one of the best “quality on sale” moments in years? For investors who rely on S-REIT dividends to fund their retirement—perhaps in their CPF-IA or SRS accounts—this question is critical.

I’m breaking down exactly why these REITs made this unusual list, what their portfolio pivots really mean for future performance, how the interest rate reversal changes everything, and most importantly—whether this is the mean reversion trade Singapore investors should be paying attention to right now. Let’s get into it.

In This Article:

• The Mean Reversion Setup: Quality Beaten Down by Rates

• Strategic Sector Pivots: Betting on Asia’s Growth Engines

• Interest Rate Reversal: The Tailwind Finally Arrives

• Conservative Financial Management: How They Survived the Storm

• The Green Advantage: ESG as Competitive Edge

• My Take: The Patience Play (But Don’t Chase the Party)

• Action Steps for Singapore InvestorsThe Mean Reversion Setup: Quality Beaten Down by Rates

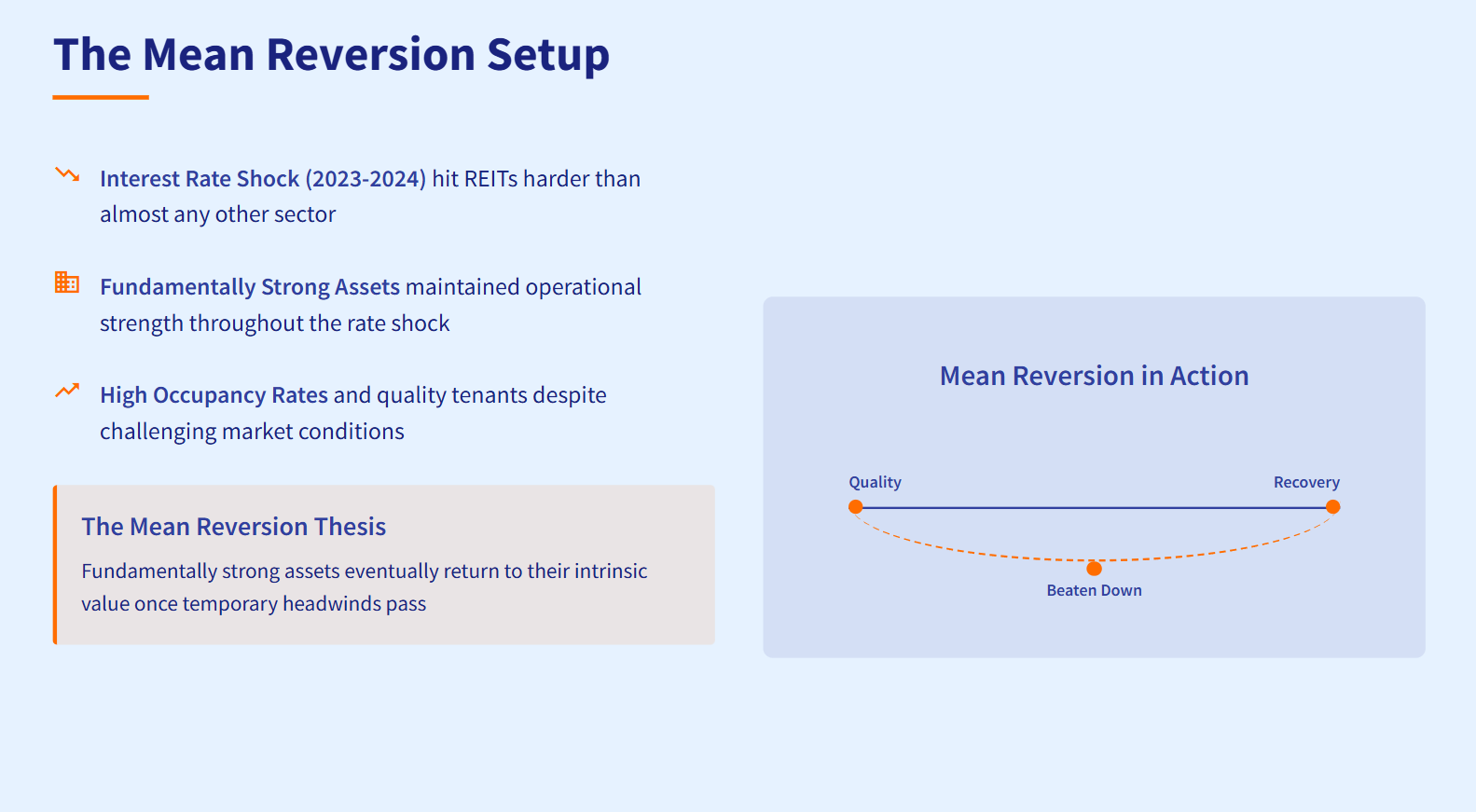

Picture this: You open your brokerage app and see these three names still underwater after years of losses. The five-year charts look brutal. But zoom out to ten years and suddenly you’re looking at winners that delivered 86% or more in gains. What happened? The answer is simple but painful—the interest rate shock of 2023 and 2024 hit REITs harder than almost any other sector. When borrowing costs spike, property trusts with leverage get hammered. Share prices fall. Dividend yields look less attractive compared to risk-free T-bills. Investors bail.

But here’s the thing about mean reversion—it’s based on the idea that fundamentally strong assets eventually return to their intrinsic value once temporary headwinds pass. Think of it like a champion swimmer getting dunked by a wave. The wave was real, the dunking was real, but the swimmer’s ability didn’t disappear. These three REITs maintained their operational strength throughout the rate shock. High occupancy rates. Quality tenants. Conservative leverage. Strategic portfolio upgrades. They didn’t panic or overextend. They played defense and prepared for better times.

That’s the setup we’re looking at now. The question isn’t whether these REITs are broken—they’re clearly not. The question is whether the market will reward their resilience as conditions improve.

Strategic Sector Pivots: Betting on Asia’s Growth Engines

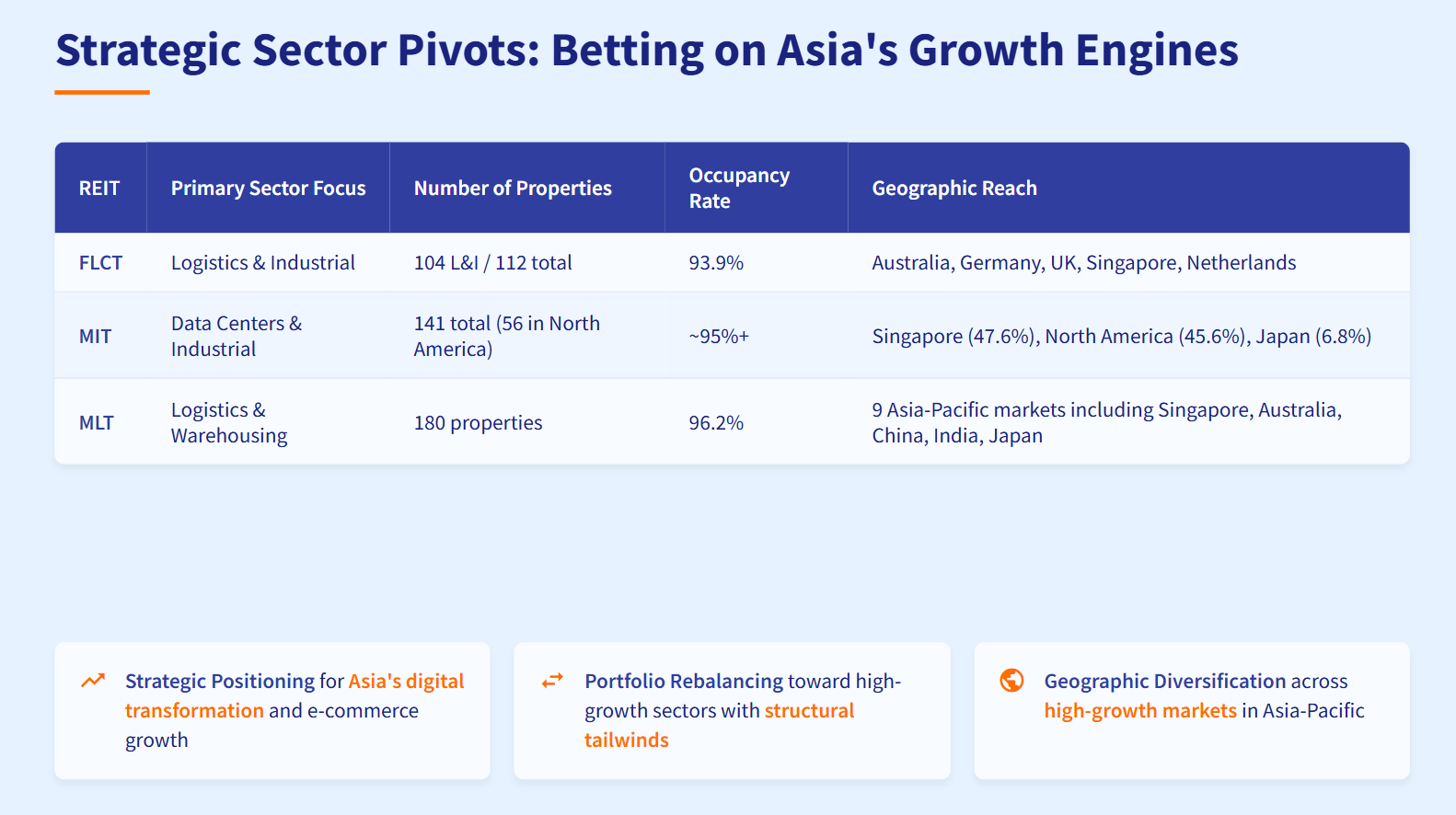

All three REITs are making deliberate, high-conviction moves into sectors with structural tailwinds. This isn’t random portfolio shuffling—it’s strategic positioning for the next decade of Asian growth. Let’s break down what each trust is doing.

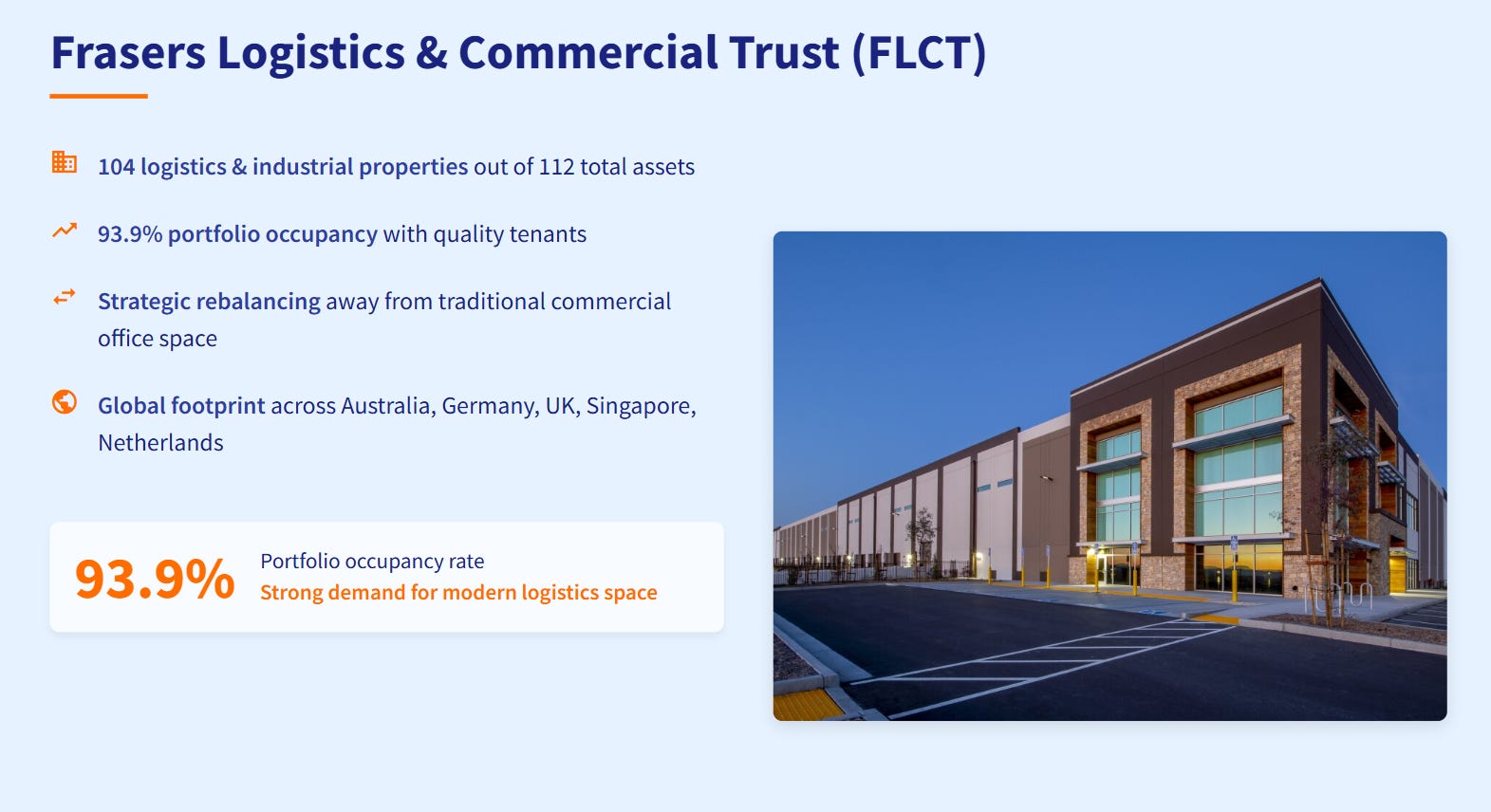

Frasers Logistics & Commercial Trust (FLCT) now owns 104 logistics and industrial properties out of 112 total assets. Portfolio occupancy sits at 93.9%. The trust is actively rebalancing away from traditional commercial office space and doubling down on warehousing, distribution centers, and industrial facilities. Why? E-commerce growth, supply chain diversification, and manufacturing reshoring across Southeast Asia all drive demand for modern logistics space. FLCT is positioning directly in this trend’s path.

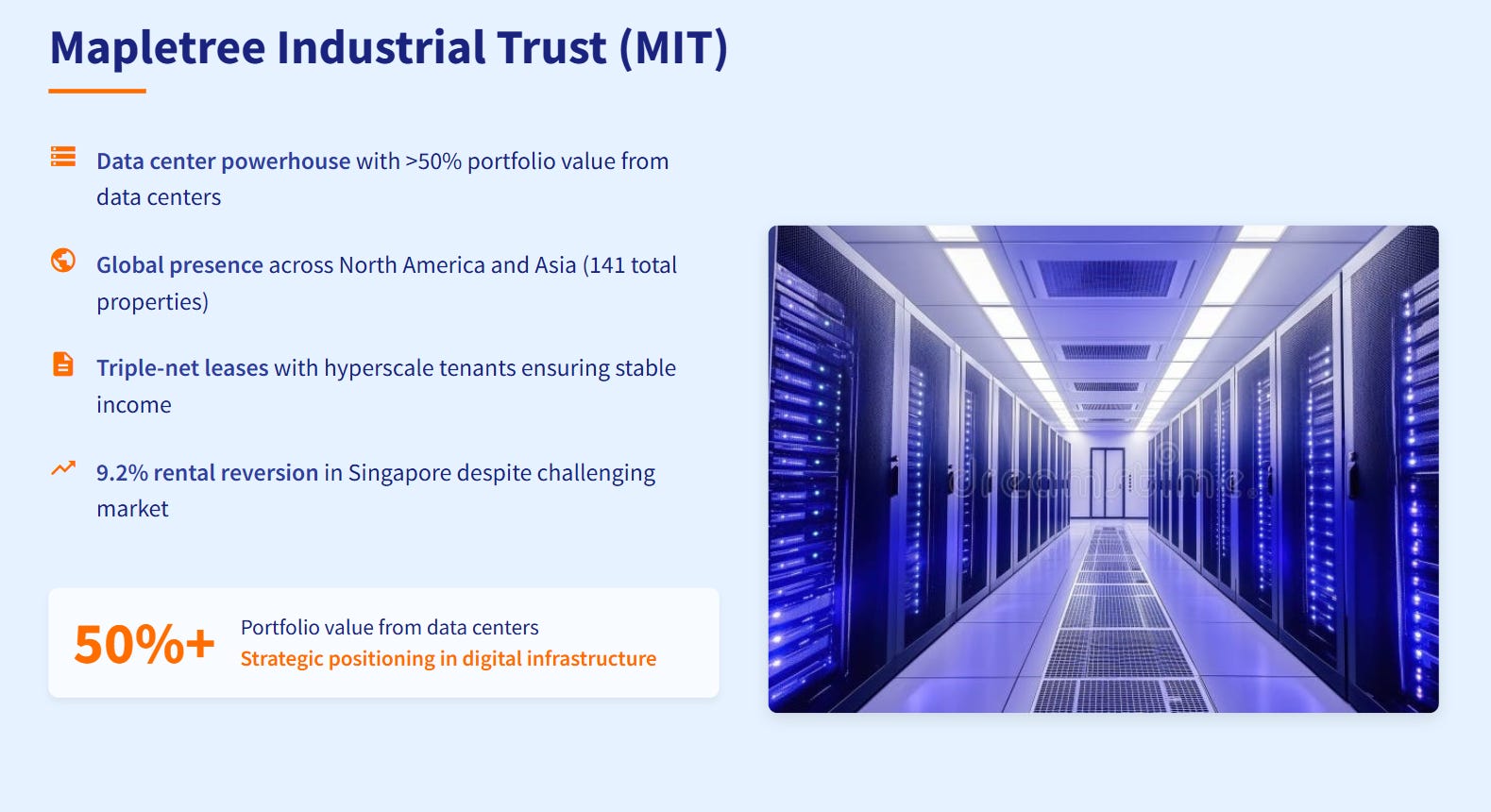

Mapletree Industrial Trust (MIT) has transformed itself into a data center powerhouse. More than half its portfolio value now comes from data centers across North America and Asia. This is a radical shift from its industrial Singapore roots, but it’s brilliant timing. Cloud computing, AI infrastructure, and digital services all need massive data center capacity. MIT locked in long-term triple-net leases with hyperscale tenants—exactly the stable, high-quality income streams investors want.

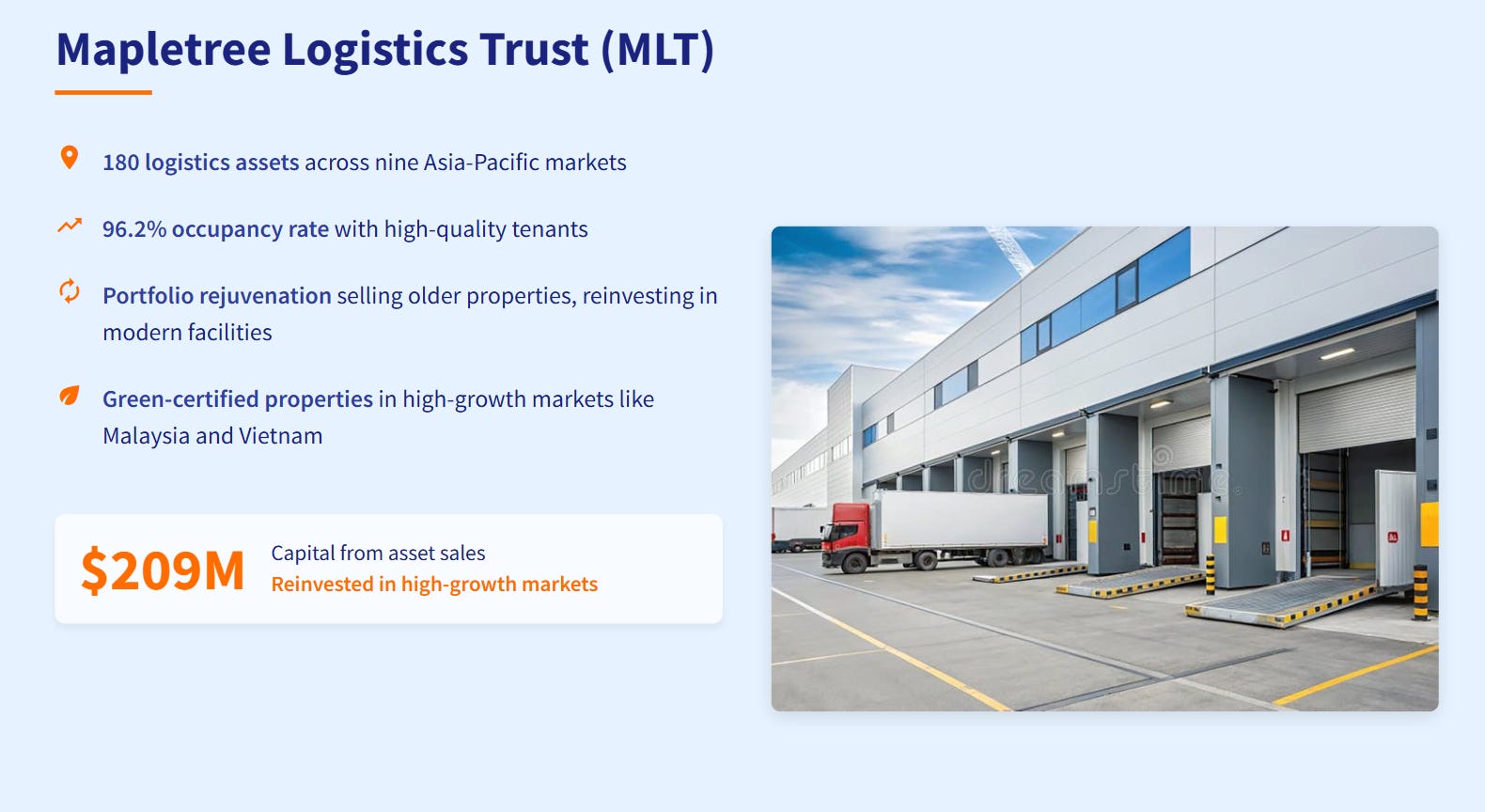

Mapletree Logistics Trust (MLT) manages 180 logistics assets across nine Asia-Pacific markets with 96.2% occupancy. The trust has been actively recycling capital—selling older, lower-yield properties and reinvesting in modern, green-certified facilities in high-growth markets like Malaysia and Vietnam. This “portfolio rejuvenation” strategy keeps the asset base fresh and competitive while capturing rising demand in emerging Southeast Asian economies.

Table: Portfolio positioning shows all three REITs concentrated in high-growth sectors with strong occupancy fundamentals.

These aren’t defensive moves to preserve dying business models. These are offensive plays to capture Asia’s digital transformation, e-commerce explosion, and supply chain evolution. The trusts are betting billions that logistics, data infrastructure, and industrial modernization will drive the next wave of property returns. Given the fundamentals, that’s a bet with strong odds.

Interest Rate Reversal: The Tailwind Finally Arrives

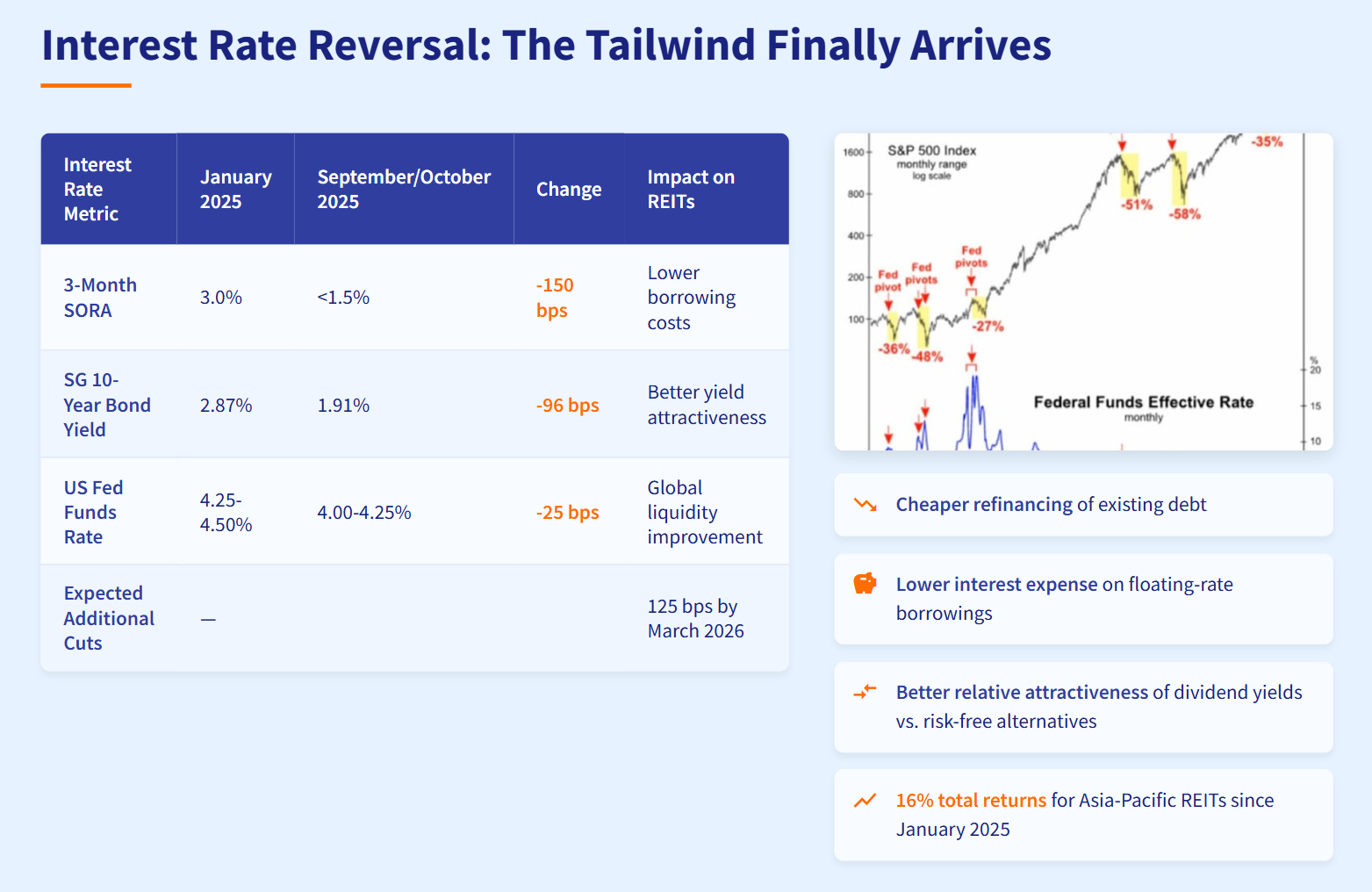

Here’s where the comeback thesis gets real support. After years of rate hikes crushing REIT valuations, the tide has finally turned. The US Federal Reserve cut rates by 25 basis points in September 2025—the first cut in this cycle. Analysts at Citi expect another 125 basis points in cuts from September 2025 through March 2026. That’s a massive shift in the cost of capital.

Singapore’s rates have already responded. The 10-year government bond yield dropped from 2.87% at the start of 2025 to just 1.91% by September 30. The three-month SORA—Singapore’s key reference rate—fell from 3% in January to under 1.5% by October. For REITs, lower rates mean three critical improvements: cheaper refinancing of existing debt, lower interest expense on floating-rate borrowings, and better relative attractiveness of dividend yields compared to bonds and fixed deposits.

Let’s put numbers to this. When SORA was at 3%, a 1-year Singapore T-bill offered nearly 3% risk-free. If a REIT yielded 5%, you were only getting 2% premium for taking property market risk and leverage risk. Not compelling. But with SORA now under 1.5% and T-bills yielding similar, that same 5% REIT yield suddenly offers 3.5% premium over risk-free rates. That’s a dramatic improvement in risk-adjusted attractiveness. Capital will flow where it’s rewarded.

Table: Interest rate decline creates multiple tailwinds for REIT performance and investor appetite.

This is the catalyst that mean reversion trades need. The fundamental quality was always there—these REITs never stopped being well-managed, high-occupancy, strategically positioned trusts. But sentiment and valuation couldn’t turn until the rate headwind stopped. Now it has. Asia-Pacific REITs as a group have already delivered 16% total returns since January 2025, largely driven by this rate reversal thesis playing out.

Conservative Financial Management: How They Survived the Storm

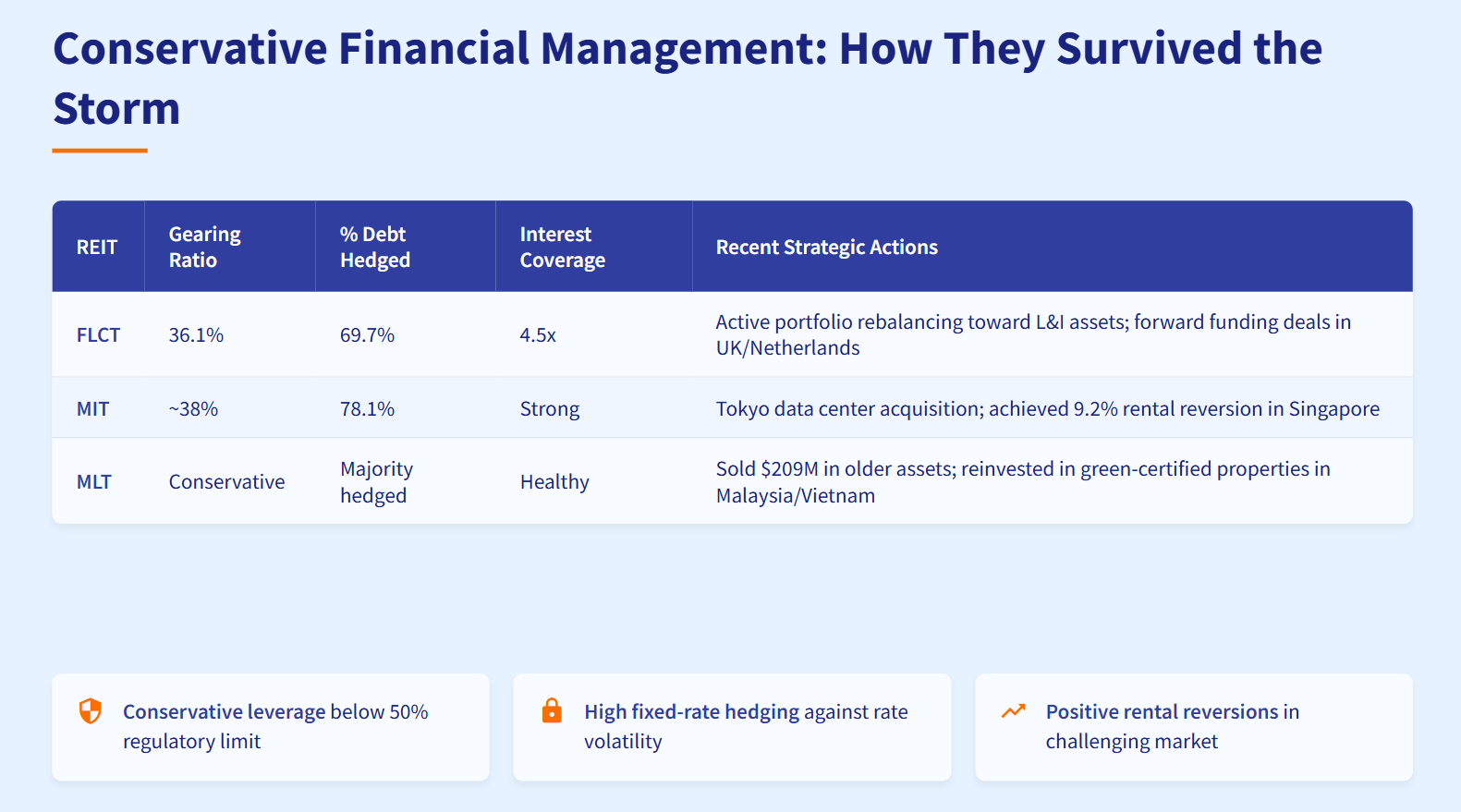

One reason these three REITs are comeback candidates rather than casualties is their disciplined approach to capital structure. When rates were rising and weaker trusts got squeezed, FLCT, MIT, and MLT maintained conservative balance sheets that kept them out of trouble.

FLCT maintains a gearing ratio of just 36.1%—well below the 50% regulatory limit for Singapore REITs. Nearly 70% of its debt is hedged at fixed rates, protecting against further rate volatility. Interest coverage stands at 4.5 times, meaning the trust generates 4.5 dollars of operating income for every dollar of interest expense. That’s a comfortable cushion.

MIT keeps gearing around 38% with 78.1% of debt hedged at fixed rates. Even during the tough rate environment, MIT delivered positive rental reversions of 9.2% in Singapore—meaning new leases were signed at prices 9.2% higher than expiring leases. That’s pricing power. When you can raise rents in a difficult market, you have quality assets and quality tenants.

MLT took a proactive approach: selling older, lower-yielding properties for over $200 million and reinvesting that capital into modern, green-certified logistics facilities in Malaysia and Vietnam. This capital recycling strategy accomplishes two goals—it locks in gains from mature assets before they decline, and it redeploys capital into higher-growth markets with better long-term potential. It’s textbook portfolio optimization.

Table: Financial prudence across all three REITs kept them resilient during the rate shock and positioned for recovery.

The takeaway here is simple: these REITs didn’t get lucky—they were well-prepared. Conservative leverage meant they could weather high rates without forced asset sales or dividend cuts. High fixed-rate hedging meant their interest costs stayed predictable. Positive rental reversions and active portfolio management meant they weren’t just surviving—they were improving their asset quality throughout the downturn.

When the next credit crunch or recession hits, these are the names that will outperform weaker competitors. Quality of management matters, and these three trusts have proven it.

The Green Advantage: ESG as Competitive Edge

Sustainability is moving from nice-to-have to must-have in institutional real estate. All three REITs are ahead of the curve, and it’s translating into real business advantages.

FLCT leads with 72% of its borrowings structured as green or sustainable financing. That’s not just optics—green loans typically carry lower interest rates and better terms. Banks want to deploy capital into ESG-compliant projects, and they reward borrowers who meet those criteria. FLCT is actively capitalizing on this trend.

MIT completed the third phase of its solar panel installation program, beating long-term sustainability targets ahead of schedule. Lower energy costs improve net operating income. Clean energy credentials attract quality tenants who face their own ESG mandates. It’s a virtuous cycle.

MLT has 51% of its net lettable area now under green leases—agreements where tenants commit to sustainability standards in exchange for modern, efficient facilities. Major multinational tenants increasingly demand green-certified space because their own investors and stakeholders expect it. REITs that can’t deliver green space will lose out on premium tenants willing to pay premium rents.

Table: ESG positioning creates tangible financial advantages beyond compliance—lower costs, better tenants, premium rents.

This isn’t greenwashing. These are real investments in asset quality that improve operating margins, tenant retention, and long-term competitiveness. As ESG mandates tighten globally, REITs with strong green credentials will have first-mover advantages in tenant acquisition and lower cost of capital. That competitive edge compounds over time.

My Take: The Patience Play (But Don’t Chase the Party)