45% Rent Hikes vs. 0.57% CPF Spread: The Keppel DC REIT Consultant Debate

Because a 0.57% risk premium won't even buy you the extra egg at the economy rice stall.

The Keppel DC REIT Dilemma: Two Hypotheses, One Decision — A Forensic Case Study

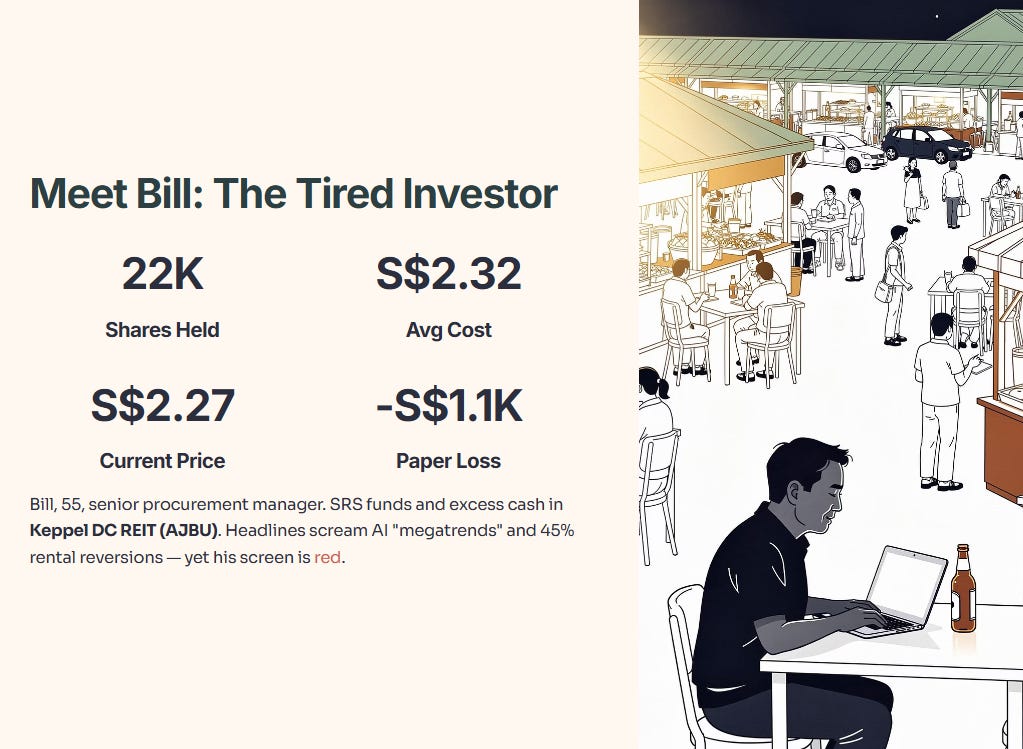

Bill is 55, and he is tired. Not tired of his job as a senior procurement manager—tired of the noise. For three years, he has dutifully funnelled his SRS funds and excess cash into what the “experts” called the gold standard of Singapore REITs: Keppel DC REIT (AJBU).

Last night, Bill sat at his dining table with a cold Tiger beer and a spreadsheet that didn’t look as pretty as it used to. He owns 22,000 shares at an average cost of S$2.32. With the price currently hovering at S$2.27, he is looking at a paper loss of about S$1,100. It’s not a catastrophe, but it’s a pebble in his shoe. He sees the headlines about AI “megatrends” and record-breaking rental reversions of 45%, yet his screen is red.

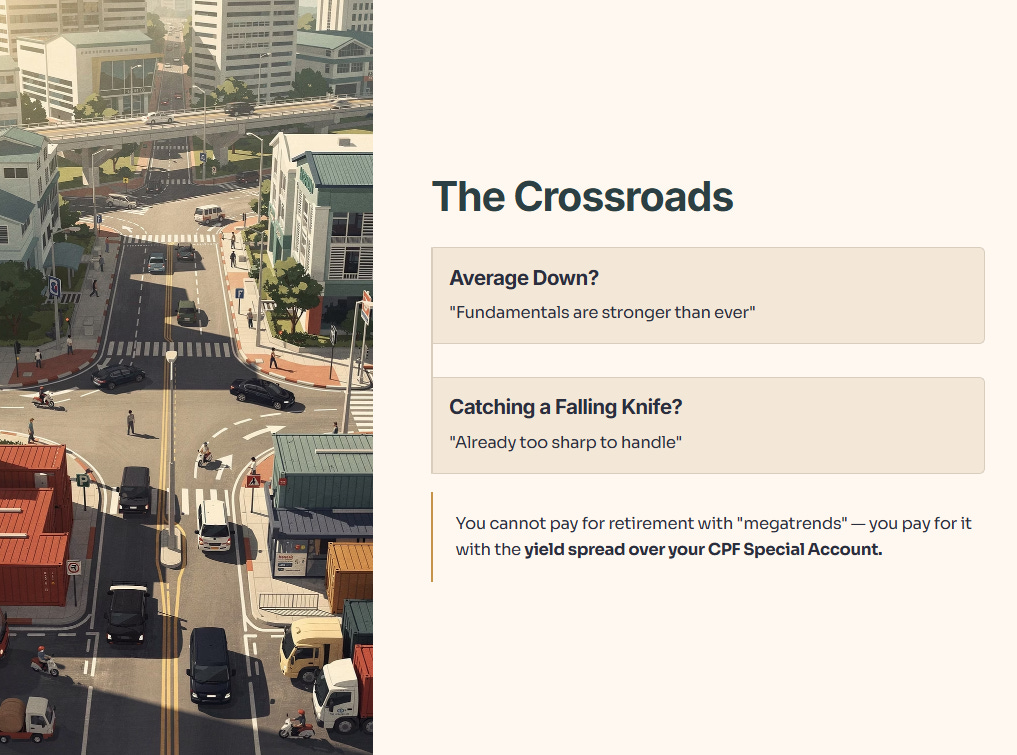

He is facing the classic Singaporean crossroads: Do I “average down” because the fundamentals are “stronger than ever,” or am I catching a falling knife that’s already too sharp to handle?

And look, the bulls are not wrong about the growth. But here is the uncomfortable truth: You cannot pay for your retirement with “megatrends”; you pay for it with the yield spread over your CPF Special Account.

In This Article:

The Masterclass: The “Kopitiam Stall” Scarcity

Step 1: The Health Check (Balance Sheet and Solvency)

The Forensic Audit: Debt and Coverage

Financial Health Checklist (AJBU)

Step 2: The Wealth Check (Cash Flow and Yield)

The Dividend Spread Audit

Dividend and Payout Trajectory (5-Year View)

Step 3: The Price Check (Valuation and Peers)

Peer Comparison Table

Step 4: The Future Check (Scenarios and Fair Value)

Sensitivity Matrix: AJBU 2026/2027

The Bottom Line

InvestingPro Reality Check

Iggy's VerdictAbout Iggy & the Elite 190

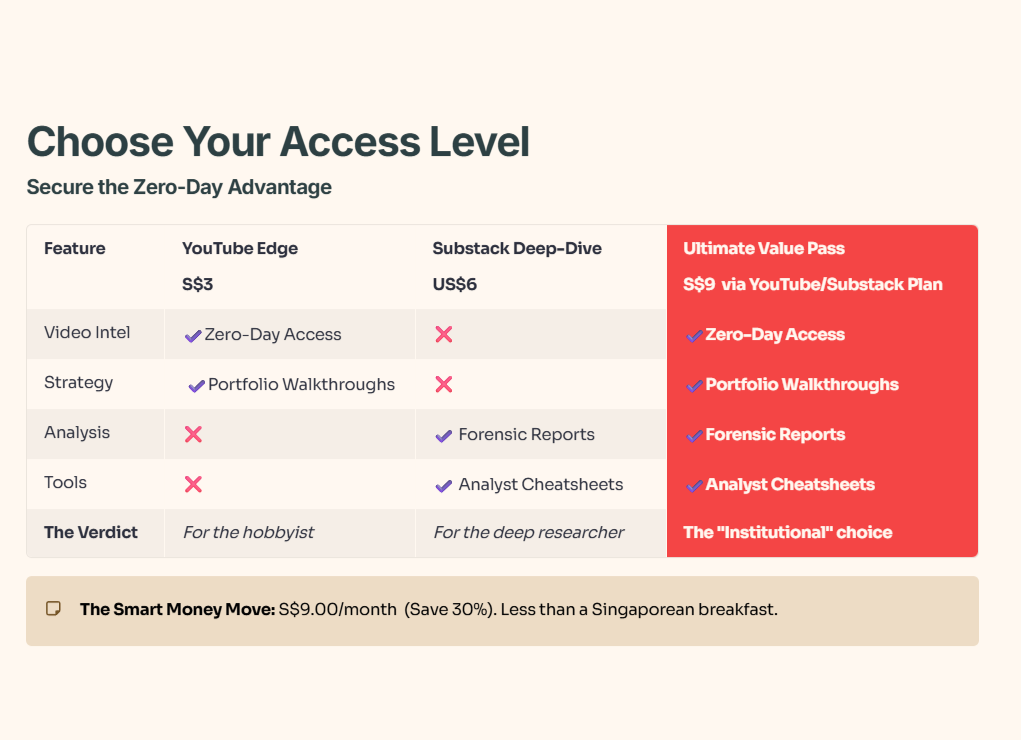

Stop Guessing. Start Auditing. Why do most retail investors fail? Because they read the “Marketing Brochure” while the Elite 190 read the “Forensic Footnotes.” For the cost of one casual lunch, you get the full Equity Evaluation & Growth Income Strategy (EEGIS) toolkit:

Zero-Day Intel: Get my audits before the market reacts.

The Vault: Full access to every forensic scorecard and risk-free spread audit.

Institutional Edge: Cheatsheets designed for the “Bedok-to-Boardroom” investor.

Join 190 high-conviction investors who value math over narratives.

👉 [Upgrade to the Elite 190 Vault]

The Masterclass: The “Kopitiam Stall” Scarcity

To understand Keppel DC REIT, you have to stop thinking about “data centres” as complex server farms and start thinking about them as the prime corner stall at a popular Maxwell Hawker Centre.

In Singapore, you cannot simply open a new hawker stall whenever you want. The government controls the licenses, the NEA regulates the space, and if you want the “good” spot near the entrance with the most foot traffic, you have to pay a massive premium. Data centres are exactly the same.

Singapore’s moratorium on new builds (now replaced by strict green criteria) means that “power” is the new “flour.” If you don’t have the power quota, you can’t bake the bread.

Keppel DC REIT owns the ovens. They have the legacy power quotas and the Tier-3 connectivity that hyperscalers like Google and Meta crave. This scarcity is why they can demand a 45% rental increase when a contract expires—because where else is the tenant going to go? To a void deck with a portable fan? No. They need the industrial-grade cooling and the “iron bastion” reliability that Keppel provides.

So what does this mean for you? It means Keppel DC REIT isn’t just a property play; it is a toll-booth play on the entire digital economy of Southeast Asia. But even the best toll booth is a bad investment if you pay ten times what the toll is worth.

Step 1: The Health Check (Balance Sheet and Solvency)

If Keppel DC REIT were a person, would they be fit enough to run a marathon in a high-interest-rate environment, or are they one cramp away from a collapse? We apply the Safety First pillar here. We aren’t interested in the “potential” for growth; we are interested in the fortress of the balance sheet.

The Forensic Audit: Debt and Coverage

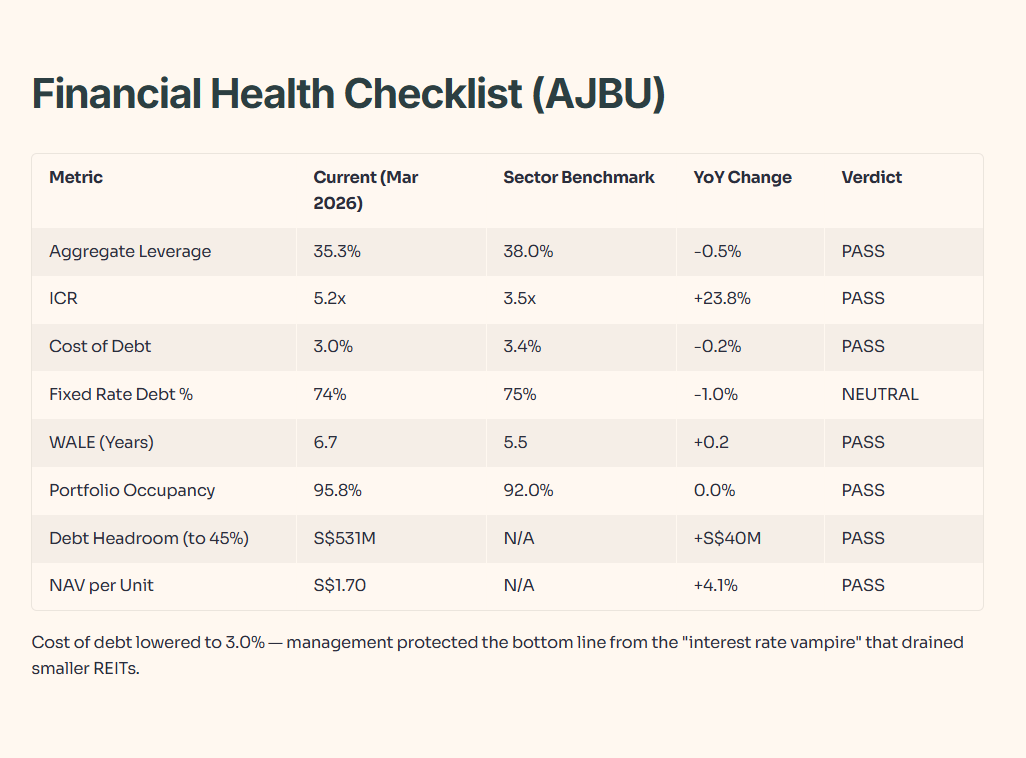

As of March 3, 2026, Keppel DC REIT reports an Aggregate Leverage (Gearing) of 35.3%.

Layer 1 — Raw Fact: The gearing stands at 35.3% with an Interest Coverage Ratio (ICR) of 5.2x.

Layer 2 — Historical Benchmark: This is a significant improvement from the 2023-2024 “danger zone” where ICR dipped to 4.0x. However, it remains far below the 2020 peak of 11.3x.

Layer 3 — Peer Context: Compared to Digital Core REIT (DCRU), which carries a gearing closer to 38.5%, Keppel is “leaner.” But compared to Mapletree Industrial Trust (ME8U)—which has a more diversified industrial base—Keppel’s singular focus on data centres makes this 35% feel “heavier” in a sector downturn.

Layer 4 — Forward Scenario: If interest rates rise another 50 basis points (a 10% deterioration in financing conditions), the ICR would likely contract to 4.8x. This remains comfortably above the MAS regulatory floor of 2.5x but reduces the “buffer” for future acquisitions.

Layer 5 — Wallet Impact: For a 55-year-old like Bill, this 35.3% gearing represents a Yellow Light. It is safe, but it limits the REIT’s ability to “buy the dip” in new assets without asking unitholders for more money via a rights issue.

Financial Health Checklist (AJBU)

Double-Entry Data Check: The 35.3% gearing and 5.2x interest coverage show a REIT that has successfully navigated the “rate spike” of 2024-2025. By lowering their average cost of debt to 3.0%, management has protected the bottom line from the “interest rate vampire” that sucked the blood out of smaller REITs.

🎓 Educational Note: Interest Coverage Ratio (ICR)

Think of ICR like your ability to pay your monthly HDB mortgage using only your take-home salary, before you spend a cent on cai fan or transport. An ICR of 5.2x means Keppel earns $5.20 for every $1.00 they owe the bank in interest. It’s a huge safety net.

So what does this mean for you? It means the dividend isn’t at risk of being cancelled just to keep the bank happy. The “HDB mortgage” is well-covered.

🦎 Iggy’s Insight: The Fortress of Solitude

Keppel DC REIT has spent the last 24 months building an Iron Bastion around its balance sheet. While other REITs were panicking about refinancing, Keppel was raising capital and lowering its cost of debt to 3.0%. They aren’t just surviving; they are hoarding dry powder.

However, don’t mistake “safety” for “cheapness.” A fortress is expensive to maintain, and you are paying a premium to stand behind these walls. The debt is managed, but the “growth engine” now requires massive fuel (acquisitions) to move the needle on a multi-billion dollar portfolio.

Punchline: The foundation is made of granite, but the rent is already sky-high.

“Now that you’ve seen why the 0.57% spread is the trap, the only question that matters is this: what specific price (and yield) flips AJBU from ‘CPF-lookalike’ to ‘worth-the-risk’—and how do we verify the DPU isn’t a one-off illusion?”