5 "Safety" Stocks I Am Buying Now (The January 2026 Playbook)

With the STI hitting record highs of 4,647, the easy money has been made. Here is my rigorous analysis on where the safe yield, recovery growth, and structural insurance still hide.

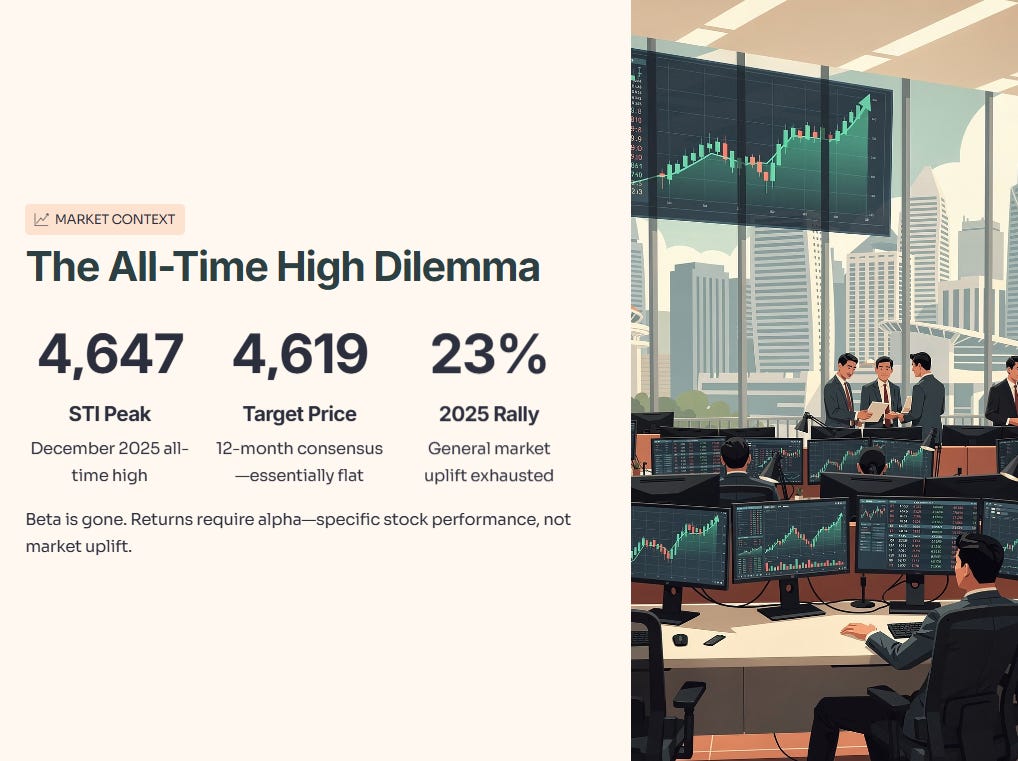

The Straits Times Index (STI) just hit an all-time high of 4,647 points in December 2025.

That number looks great on a headline, but for those of us managing retirement portfolios or growing our CPF/SRS accounts, it triggers a very specific fear: Is it too expensive to buy now?

The 12-month consensus target is sitting at 4,619—which is essentially flat from here. This tells us that the “beta” (general market uplift) is gone. If you want returns in 2026, you have to find “alpha” (specific stock performance).

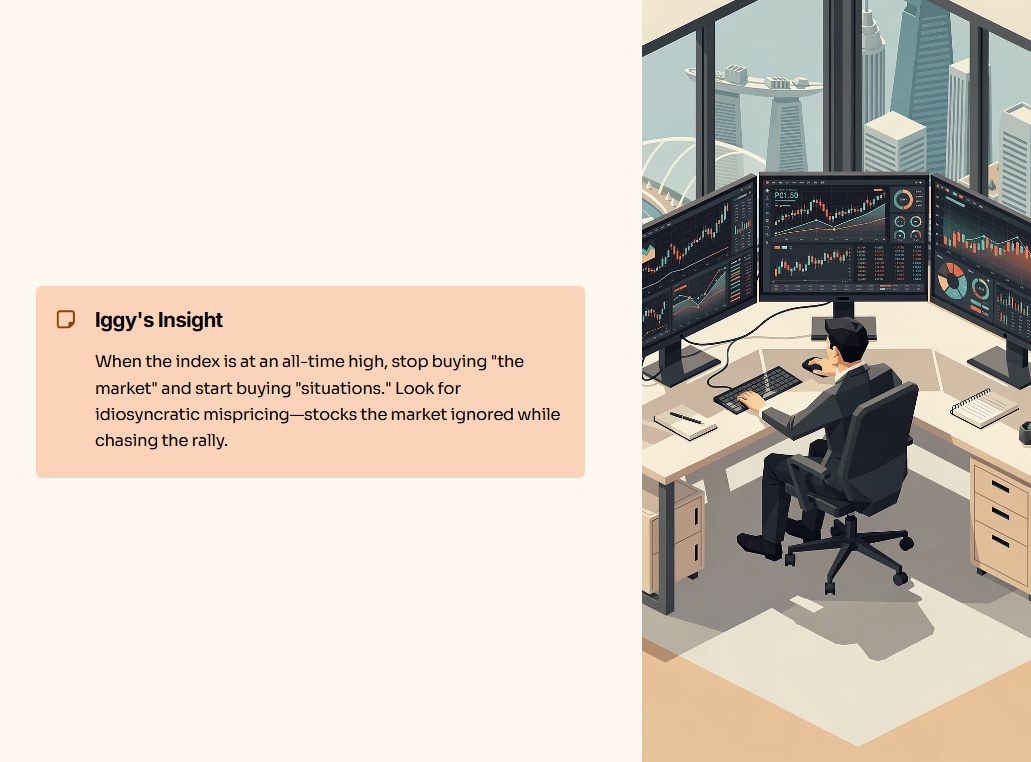

Iggy’s Insight:

When the index is at an all-time high, you stop buying “the market” and start buying “situations.” We are looking for idiosyncratic mispricing—stocks that the market has ignored or misunderstood while chasing the rally.

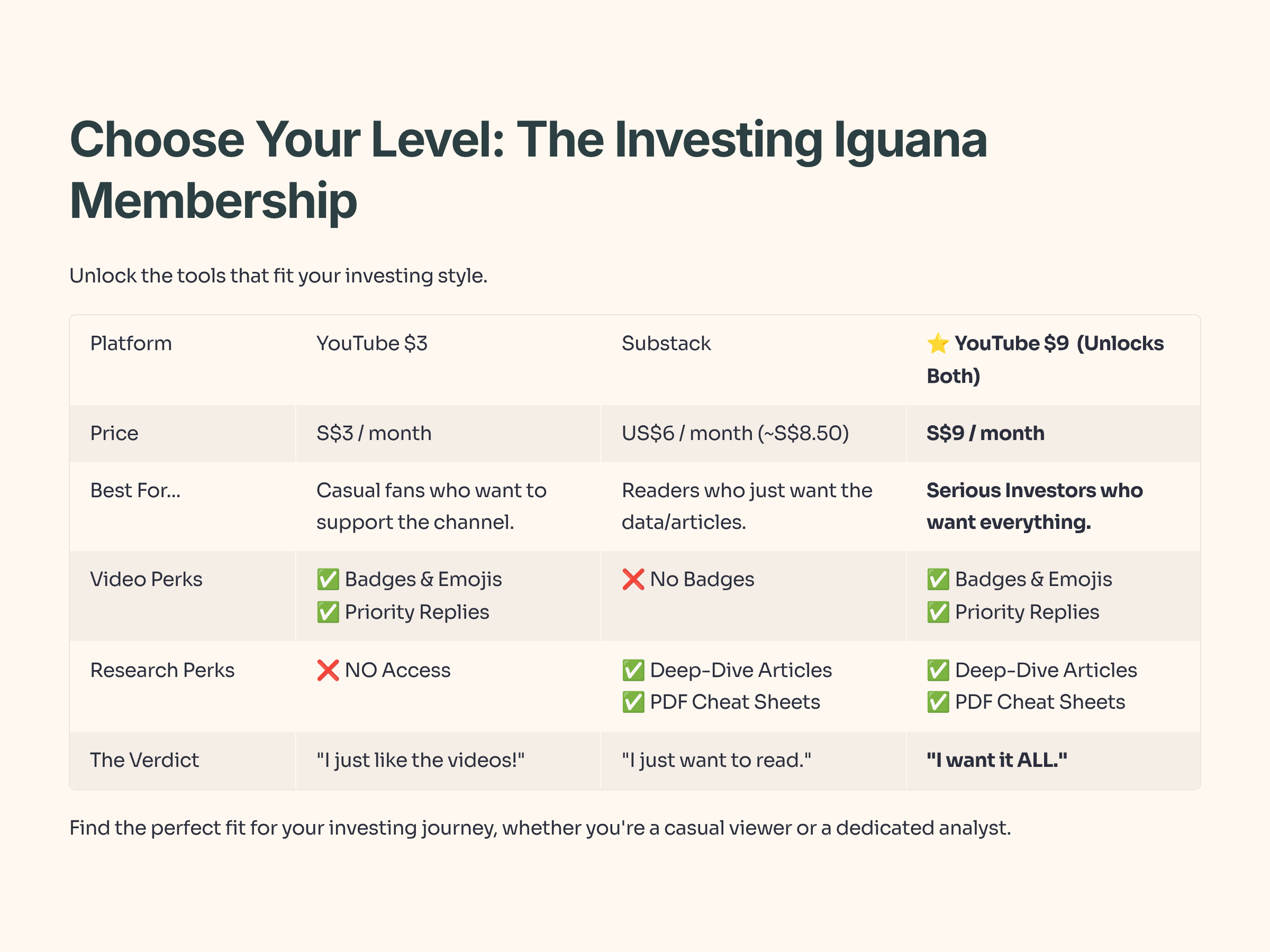

If you’re new here, welcome. I’m Iggy, your Singapore-based market analyst. Since October 2025, we’ve produced over 1,300 videos and 400 articles with 1.1 million watch hours. We are also home to a growing community of over 60 YouTube Premium subscribers and 30 paid Substack members.

Quick Housekeeping: If you want the best value, the YouTube Premium Membership (S$9/mth) bundles these deep-dive articles with the podcast videos. Substack alone is US$6, so the bundle is the “smart money” move.

Now, let’s get to the numbers.

In This Article:

• The “Fortress” Industrial: ST Engineering

• The “Fallen Angel”: Keppel DC REIT

• InvestingPro Reality Check

• The “Reasonable Growth”: Broadcom

• The “Cash Cow”: NetLink NBN Trust

• The “Hedge”: SPDR Gold Shares

• Iggy’s Verdict: Rotation, Not Retreat

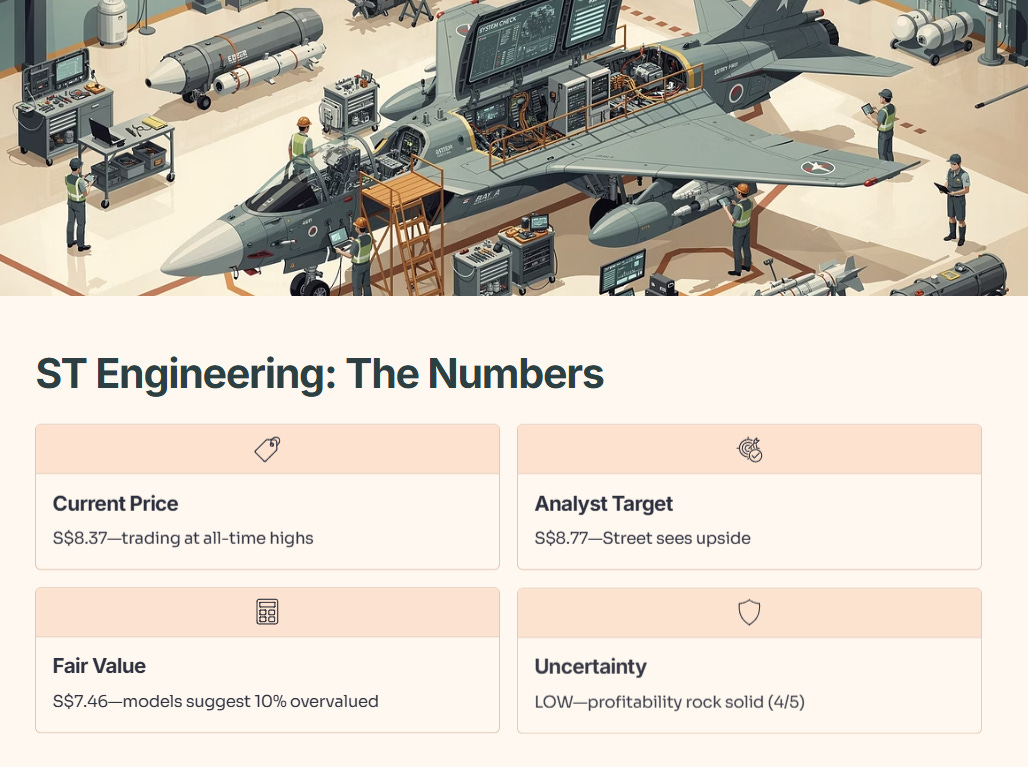

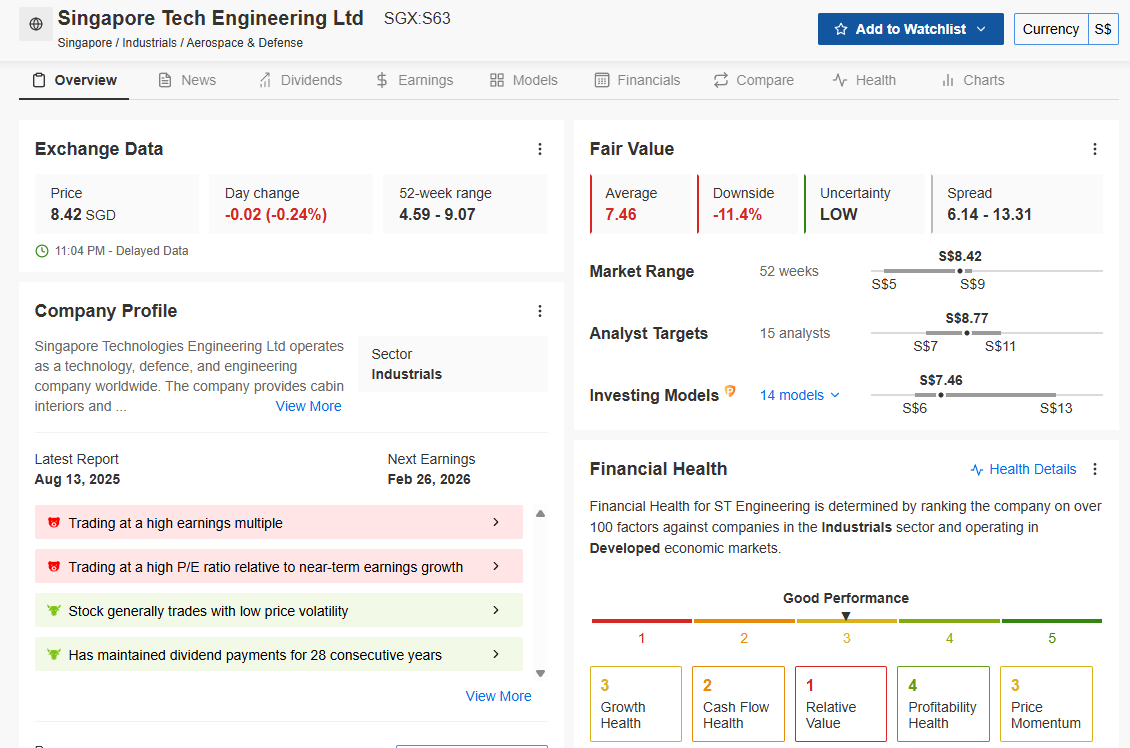

1. The “Fortress” Industrial: ST Engineering (SGX: S63)

Most Singaporean portfolios are overweight banks. If you already own DBS/OCBC, buying more at record highs isn’t diversification—it’s doubling down.

The smarter move for 2026 is ST Engineering. But let’s be clear: Quality is not cheap.

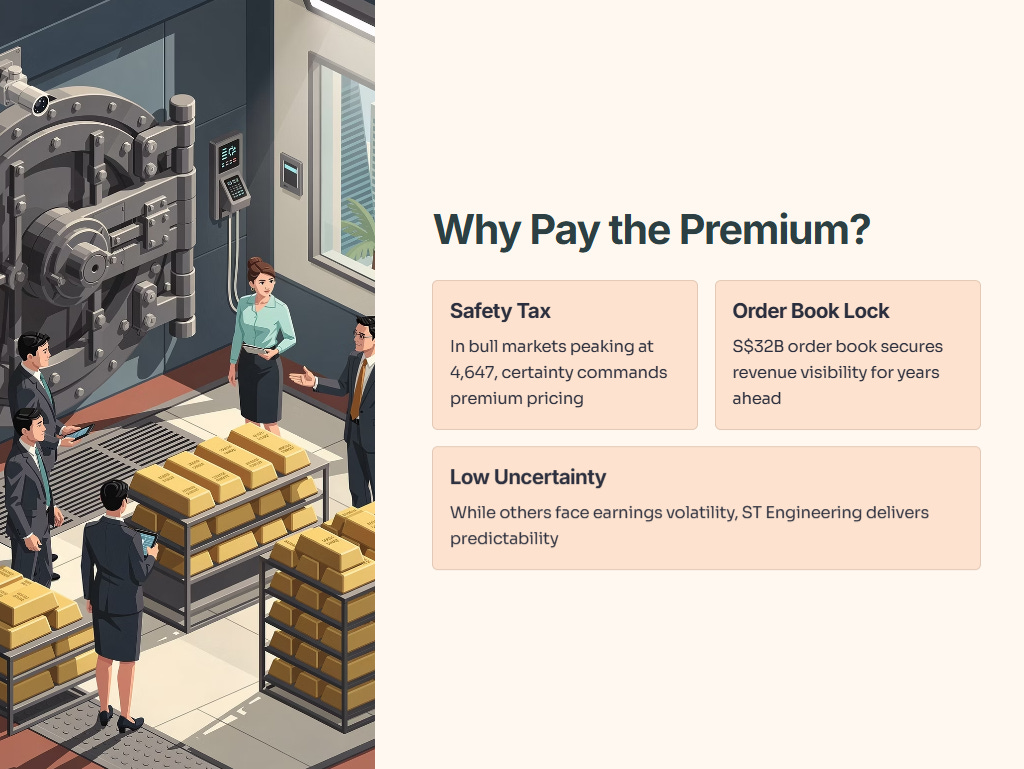

The “Alpha”: Why Pay the Premium?

You might ask: “Iggy, the model says it’s overvalued by 10%. Why buy?”

Because in a bull market peaking at 4,647 points, safety commands a premium. Look at the “Uncertainty” score in the data—it is LOW.

While other stocks have “High Uncertainty” (meaning their earnings could crash), ST Engineering’s S$32B order book locks in revenue for years.

Iggy’s Take:

I am willing to overpay slightly for a “Fortress.” The Analysts (Target S$8.77) are bullish because of the order book. The Models (Fair Value S$7.46) are bearish because of the P/E ratio.

My move: I am not chasing it at S$8.37 with a lump sum. I am nibbling. I’m buying for the 18+5 cent dividend visibility, accepting that I’m paying a “safety tax” for a stock that lets me sleep at night.

InvestingPro Data Check: Fair Value

I don’t just guess at valuations. I check the institutional models.

Source: InvestingPro data. Unlock these institutional tools for yourself: Use code INVESTINGIGUANA for an exclusive 55% discount to kickstart 2026.

The Model Says: InvestingPro often flags ST Engineering as having “Low Price Volatility” and a “Healthy” score. The Fair Value models likely suggest upside toward the S$5.50 - S$6.00 range, validating the analyst consensus (UOB Kay Hian recently raised targets to S$6.80).

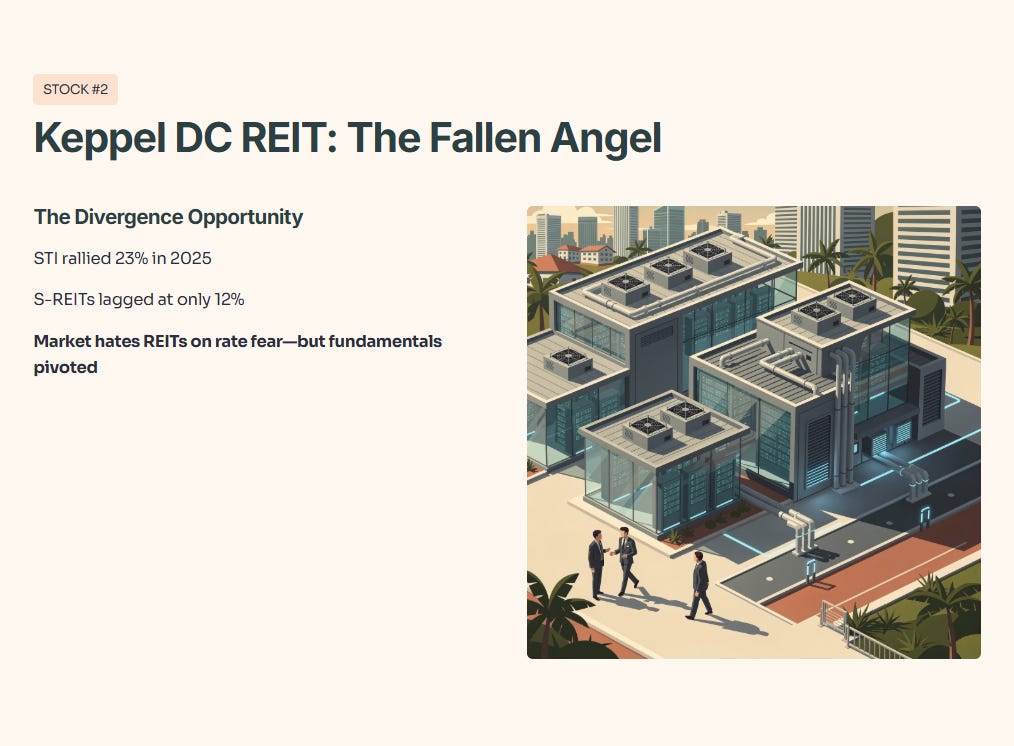

2. The “Fallen Angel”: Keppel DC REIT (SGX: KDREIT)

While the STI rallied nearly 23% in 2025, S-REITs lagged, managing only ~12%. This divergence is where the opportunity lies.

The market hates REITs right now because of “rate fear.” But for Keppel DC REIT, the fundamentals have quietly pivoted.

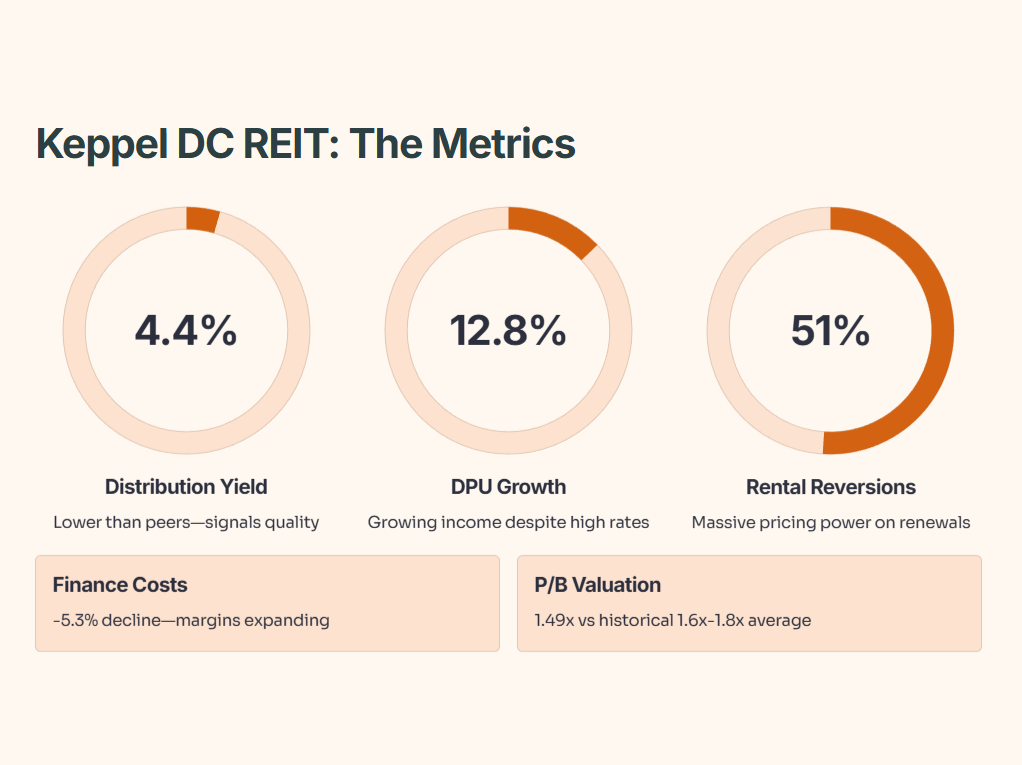

The “Why”: AI is a Physical Asset

We talk about AI as software, but it lives in hardware. Keppel DC REIT owns the physical shells (SGP 7 & 8, Tokyo assets) where the hyperscalers (Microsoft, Google, AWS) live. The 51% rental uplift on contract renewals is the smoking gun—it proves that demand for data center space is inelastic. Tenants must pay up because there is no vacancy.

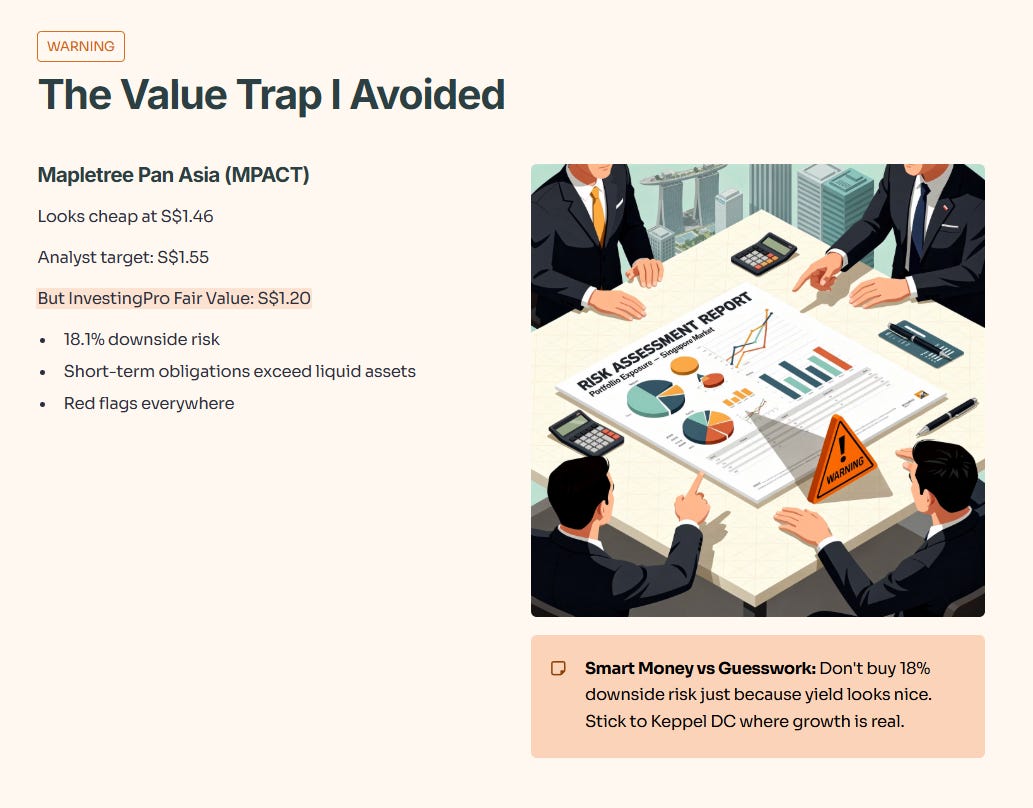

Iggy’s Insight: The “Value Trap” I Avoided (Mapletree Pan Asia)

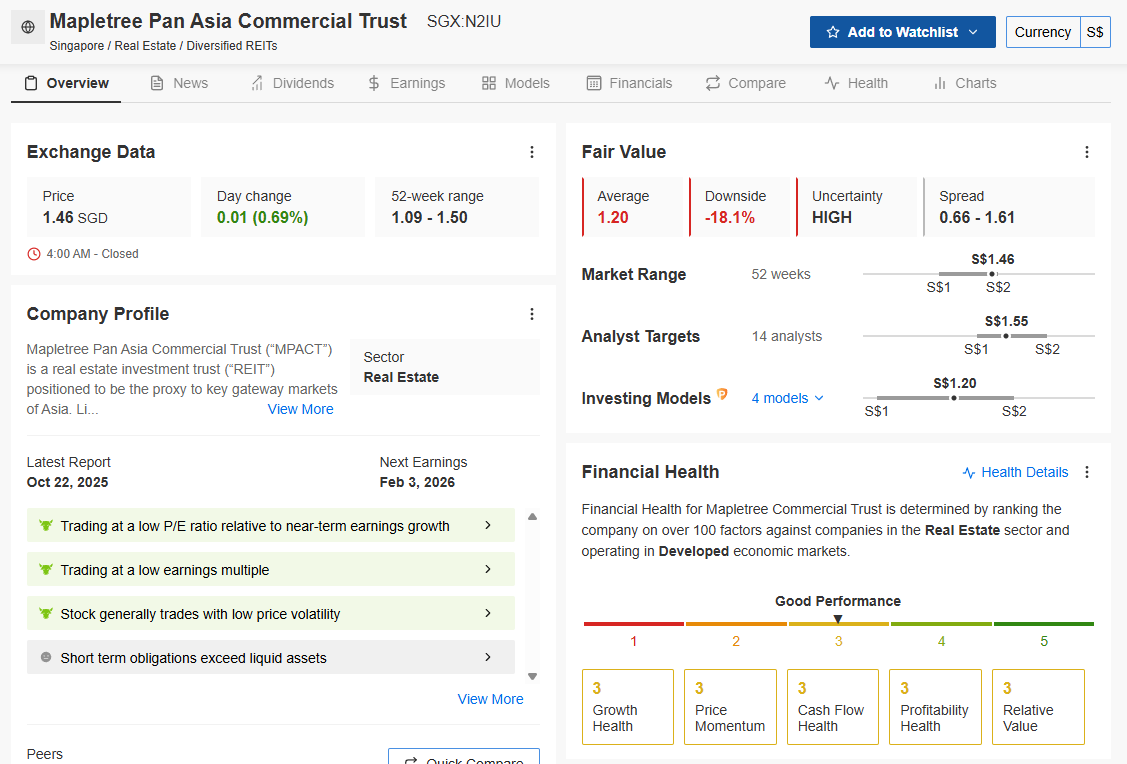

I know many of you are looking at Mapletree Pan Asia Commercial Trust (MPACT). It looks cheap at S$1.46, and analysts have a target of S$1.55.

But look at the Data Check below.

InvestingPro data flags a Fair Value of just S$1.20—that is an 18.1% downside risk.

Even worse? Look at the red flag: “Short term obligations exceed liquid assets.”

This is the difference between “Smart Money” and “Guesswork.” I don’t buy stocks with 18% downside risk and liquidity issues just because the yield looks nice. We stick to Keppel DC, where the growth is real.

InvestingPro Data Check: The “Trap” vs. The “Treasure”

I don’t just guess at valuations. I check the institutional models to spot the difference between a bargain and a trap.

Source: InvestingPro data. Unlock these institutional tools for yourself: Use code INVESTINGIGUANA for an exclusive 55% discount to kickstart 2026.

The Model Says: Notice the red flag? “Downside -18.1%.” When the Fair Value line ($1.20) is that far below the Price line ($1.46), you stay away. The model also flags that “Short term obligations exceed liquid assets.” That is a stress point we don’t want in our portfolio.

3. The “Reasonable Growth”: Broadcom (NASDAQ: AVGO)

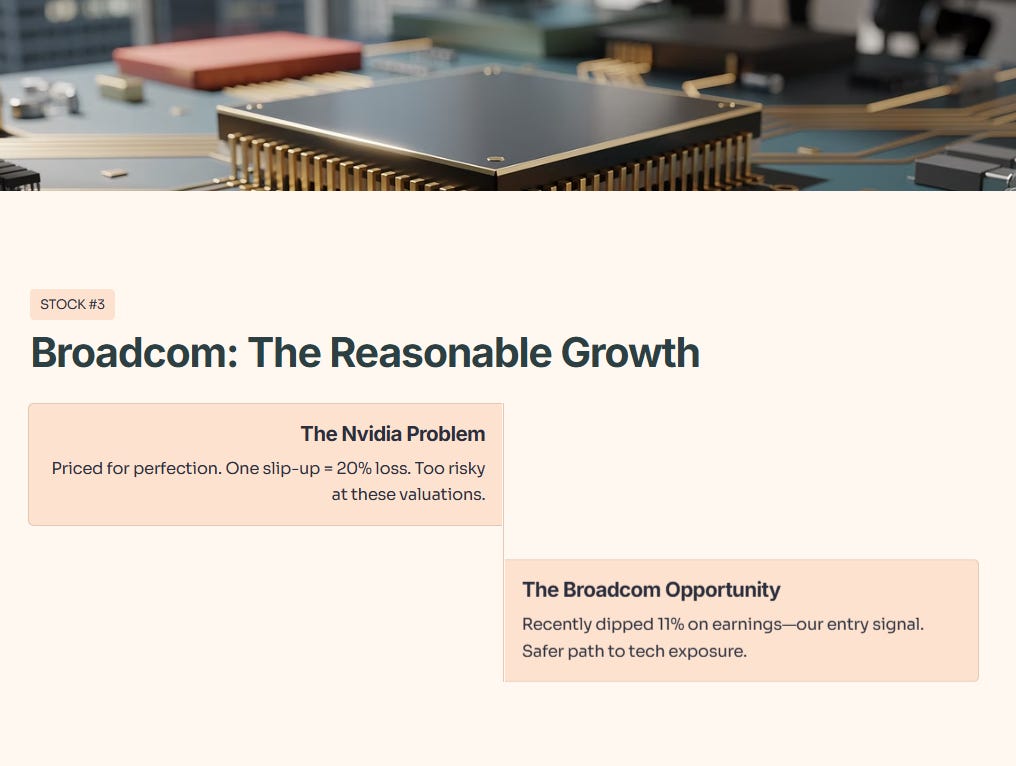

I know many of you are tempted by Nvidia. But at these valuations, Nvidia is priced for perfection. One slip-up, and you lose 20%.

Broadcom (AVGO) offers a safer path to tech exposure. The stock recently dipped 11% on earnings, and that is our entry signal.

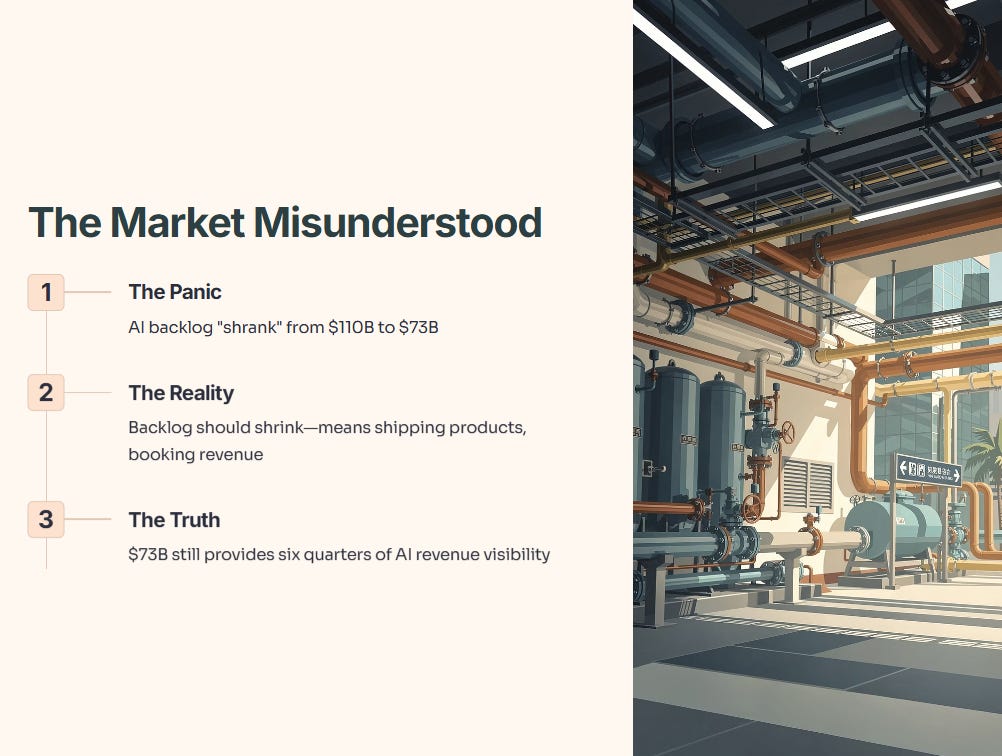

The Misunderstanding: The Backlog “Collapse”

The market panicked because Broadcom’s AI backlog “shrank” from $110B to $73B.

This is the wrong interpretation.

A backlog should shrink—that means you are shipping products and booking revenue! Even at $73B, Broadcom has clear visibility for the next six quarters of AI revenue.

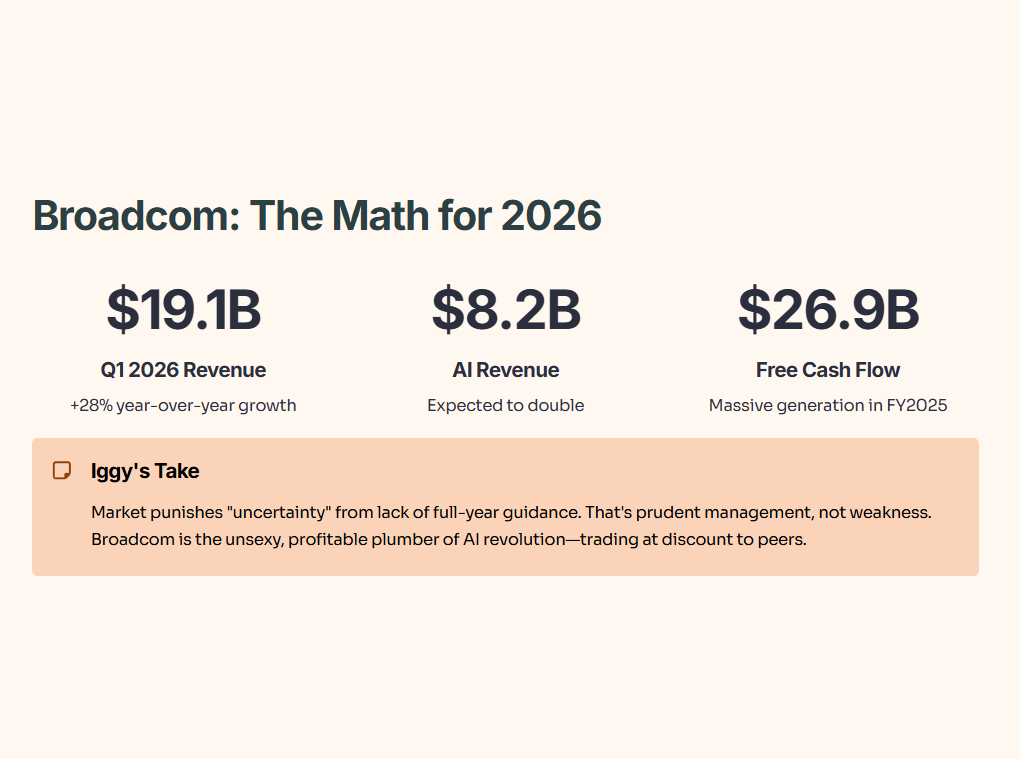

The Math for 2026:

Q1 2026 Guidance: $19.1B Revenue (+28% YoY)

AI Revenue: Expected to double to $8.2B.

Free Cash Flow: A massive $26.9B generated in FY2025.

Iggy’s Take:

The market is punishing Broadcom for “uncertainty” because they didn’t provide full-year guidance. That is prudent management, not weakness. While Google (P/E 31x) faces regulatory breakup risks and Nvidia faces hype fatigue, Broadcom is the “plumber” of the AI revolution. It’s unsexy, profitable, and trading at a discount to its peers.

4. The “Cash Cow”: NetLink NBN Trust (SGX: CJLU)

When markets are at all-time highs, you need a portion of your portfolio that acts like a bond but pays better.

NetLink is the monopoly utility that underpins Singapore’s internet. Whether the economy booms or busts, people pay their broadband bills.

Yield: 5.3% (approx 380 bps spread over T-Bills).

Risk Profile: Extremely Low.

Moat: Regulatory Monopoly.

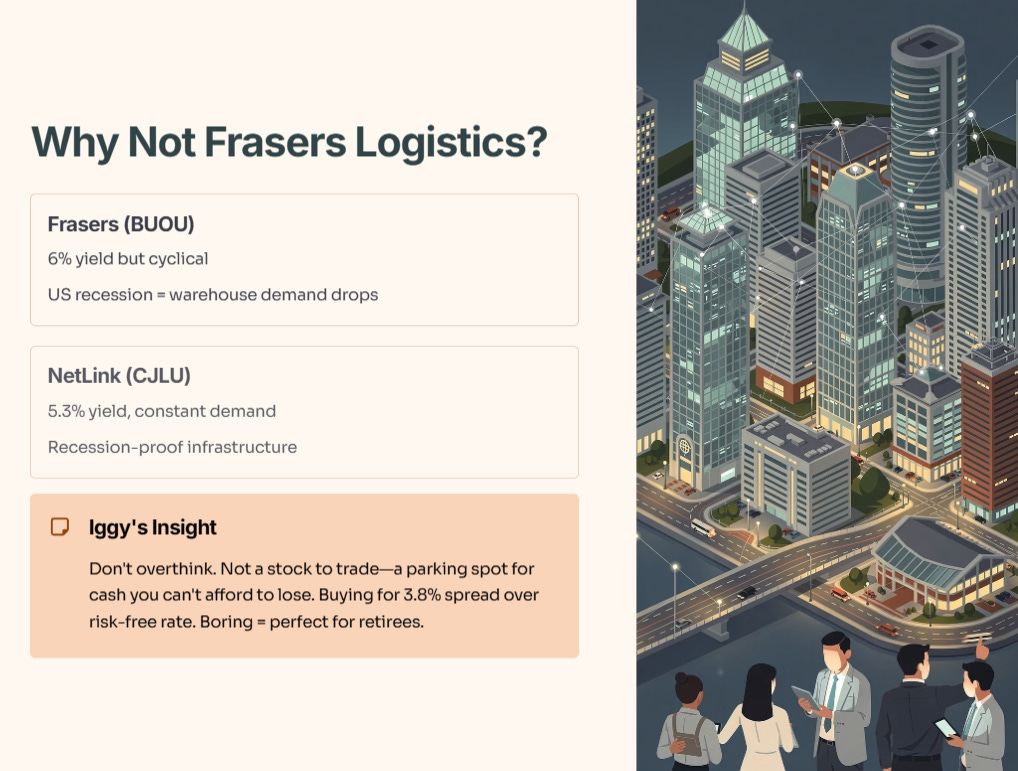

Why not Frasers Logistics (BUOU)?

Frasers yields 6%, but it is cyclical. If the US enters a recession in late 2026, warehouse demand drops. NetLink’s demand is constant.

Iggy’s Insight:

Don’t overthink this one. This isn’t a stock to trade. It is a parking spot for cash that you can’t afford to lose. We are buying this for the 3.8% spread over the risk-free rate. It’s boring, and that is exactly why it belongs in a retiree’s portfolio.

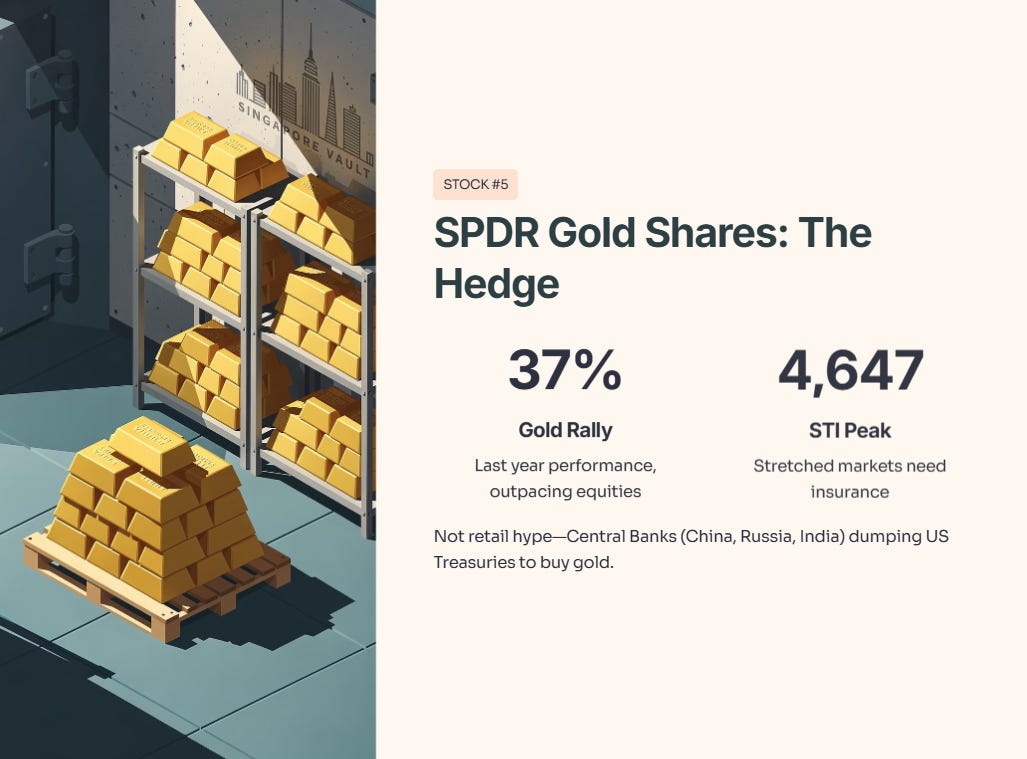

5. The “Hedge”: SPDR Gold Shares (NYSE: GLD)

I rarely recommend commodities, but with the STI at 4,647 and the S&P 500 stretched, we need insurance.

Gold rallied 37% in the last year, outpacing equities. This wasn’t driven by retail hype—it was driven by Central Banks (China, Russia, India) dumping US Treasuries to buy gold.

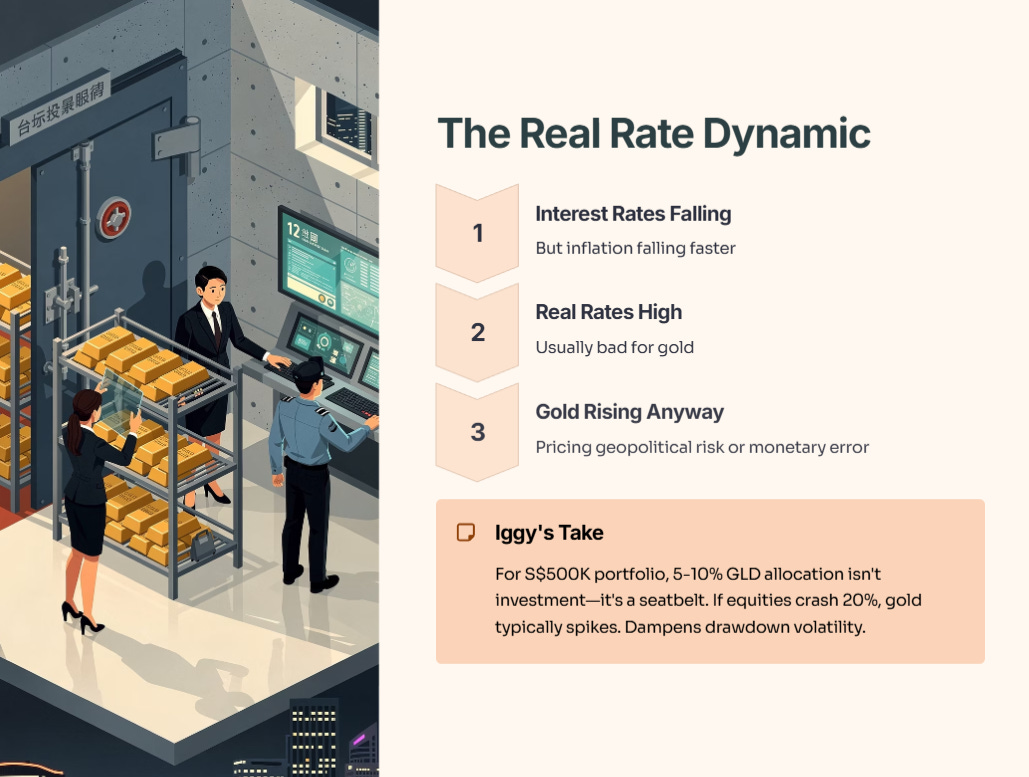

The “Real Rate” Dynamic:

Even though interest rates are falling, inflation is falling faster. This keeps “Real Rates” high. Usually, this is bad for gold. But gold is rising anyway. This signals that the market is pricing in a geopolitical event or a monetary error (inflation resurgence).

Iggy’s Take:

If you have a S$500,000 portfolio, a 5-10% allocation to GLD is not an “investment”—it is a seatbelt. If equities crash 20%, gold typically spikes. It dampens the volatility of your drawdown.

The Investor’s Action Plan: How to Execute