5 Temasek-Linked Dividends: Which One Actually Holds Up?

Same parent, same reputation — but not the same dividend safety

5 Temasek-Linked Dividends: Which One Actually Holds Up?

My phone buzzed with five different dividend headlines this week. One doubled, one got trimmed despite record revenue, one is quietly propped up by asset sales. If you are living off these payouts, that inconsistency is the whole story, not a footnote.

Every one of these five companies has Temasek sitting on the register, which tells you nothing about whether the dividend itself is something you can actually count on. A rising payout can mean a business firing on all cylinders, or it can mean a company handing back money it made from selling something. A falling payout can mean trouble, or it can mean a perfectly healthy business being compared against a one-off gain from the year before. The only way to tell the difference is to look past the headline number at what is actually generating it.

Singapore Airlines: the dividend fell, but the business didn’t

Angela’s Observation

Seatrium: the dividend doubled, the cash didn’t

Angela’s Observation

ST Engineering: the profit fell 34 percent. The cash didn’t move at all.

Angela’s Observation

DBS: the total number and the durable number are not the same number

Angela’s Observation

Singtel: nearly a third of this year’s payout came from selling assets, not from the phone bill

Angela’s Observation

So which one actually holds up?

Singapore Airlines: the dividend fell, but the business didn’t

SIA’s total dividend for the year came to 37 cents a share, down from 40 cents the year before. On its own, that reads like a company pulling back. But revenue hit a record S$20.5 billion, passenger numbers hit a record 42.4 million, and operating profit actually jumped 39 percent.

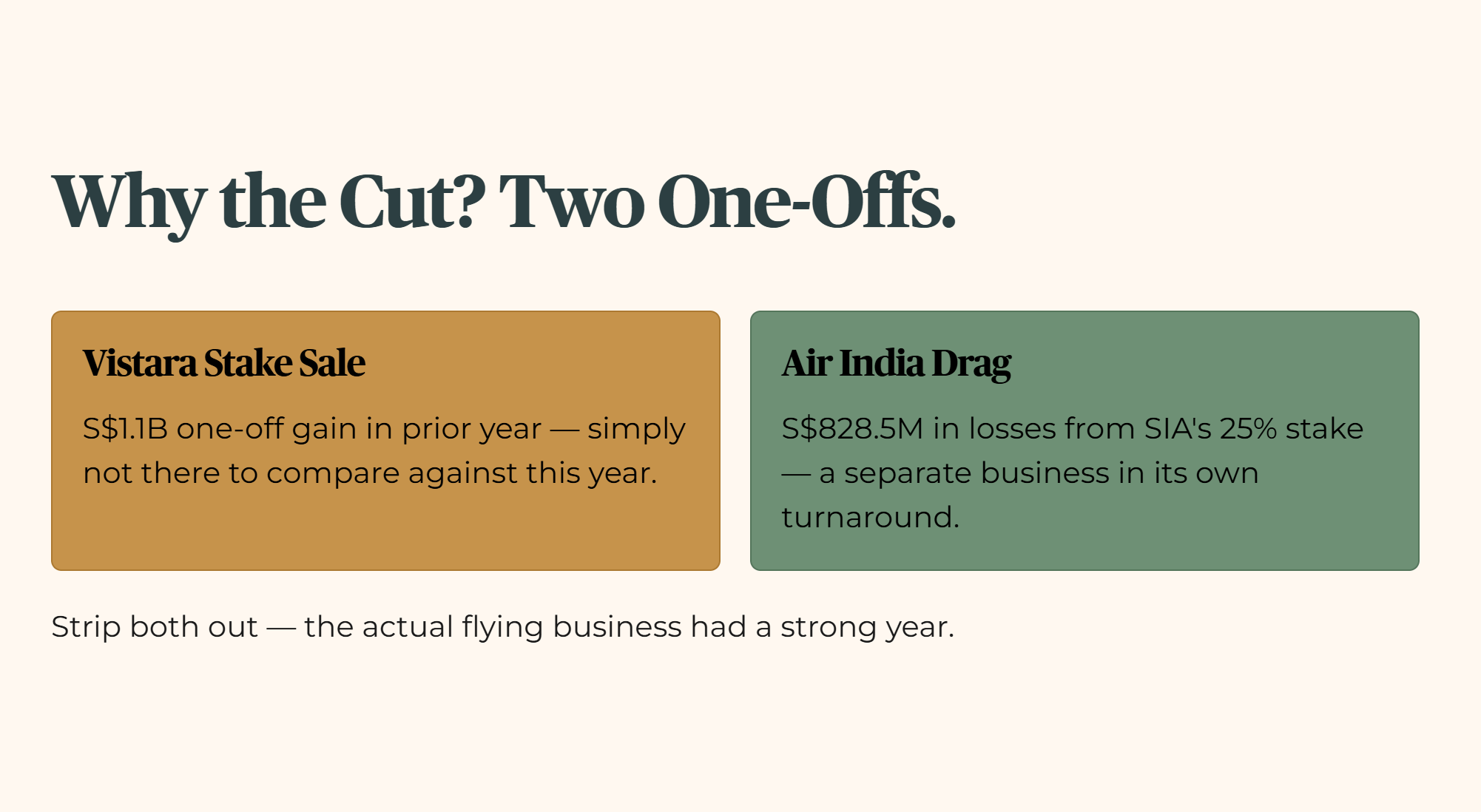

So why the cut? Two reasons, and neither one is about the airline losing altitude. The prior year’s profit included a S$1.1 billion one-off gain from selling down its Vistara stake, a gain that simply is not there to compare against this year. And SIA booked S$828.5 million in losses from its 25 percent stake in Air India, a separate business entirely, going through its own turnaround. Strip those two items out and the actual flying business had a strong year.

The dividend cut here looks less like caution about the core airline and more like SIA choosing not to pay out against profit that came from somewhere else entirely. Worth watching next year: management has flagged jet fuel costs as the real pressure point, with prices more than doubling since the Middle East conflict began and the airline’s pricing lagging the increase. If fares don’t catch up, that is the number that could genuinely test next year’s dividend, not this year’s Air India accounting.

🟠 Angela’s Observation

This is the pattern I keep seeing across the Temasek names this earnings season: a headline number moving because of something that happened somewhere else entirely, not because the core business changed direction. SIA’s flying business had a genuinely strong year. The question worth sitting with is whether Air India becomes a recurring drag on this dividend story or a one-time adjustment year, because that answer shapes whether next year’s headline number means anything at all.

Seatrium: the dividend doubled, the cash didn’t

Seatrium’s final dividend doubled to 3 cents a share from 1.5 cents, on the back of net profit more than doubling to S$323.6 million. That is a real, reported improvement, revenue grew 24.3 percent, the order book sits at S$17.8 billion, and management is chasing over S$32 billion in new opportunities over the next two years.

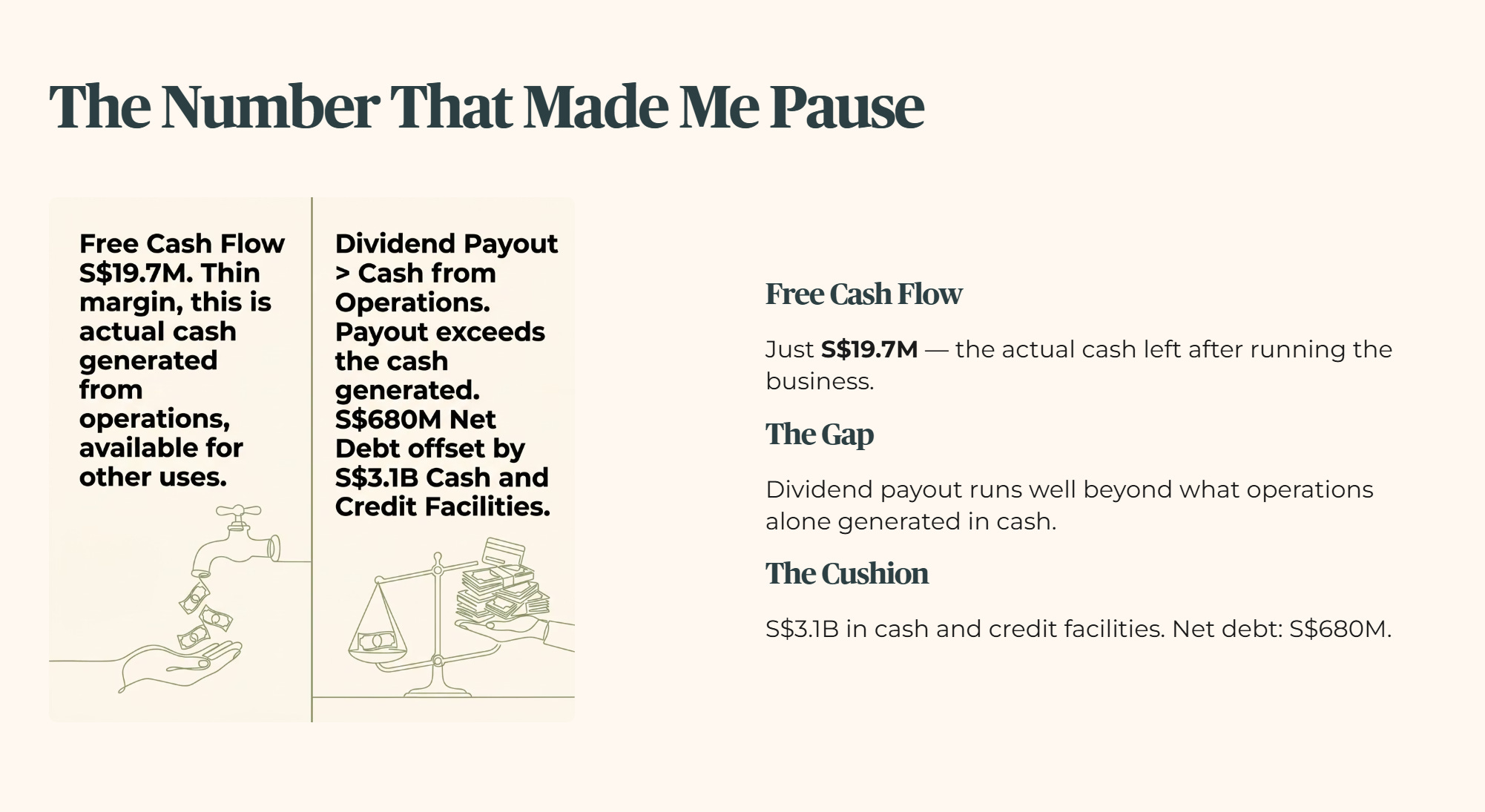

Here is the number that made me pause. Free cash flow, the actual cash left over after running the business and paying for equipment, came in at just S$19.7 million for the year. A dividend payout of this size runs well beyond what operations alone generated in cash, and the company still carries net debt of S$680 million even with S$3.1 billion in cash and credit facilities on hand as a cushion.

None of this means Seatrium is in trouble, the order book and cash facilities give it real runway. But a dividend that doubled on an improving income statement, while the cash generation behind it stayed thin, is not the same story as a company whose core operations are now throwing off more cash. If you are holding this one for income, the order book executing into actual cash over the next couple of years is the thing to watch, not this year’s profit number.

🟠 Angela’s Observation

My neighbour mentioned Seatrium to me last month, excited that the dividend had doubled. I didn’t have the heart to walk her through the free cash flow number over kopi. A doubling dividend and a doubling order book both sound like good news, but only one of them is cash in hand today. The real test here isn’t this year’s announcement, it’s whether that S$17.8 billion order book actually converts into the kind of cash flow that makes next year’s payout feel as comfortable as this year’s felt exciting.

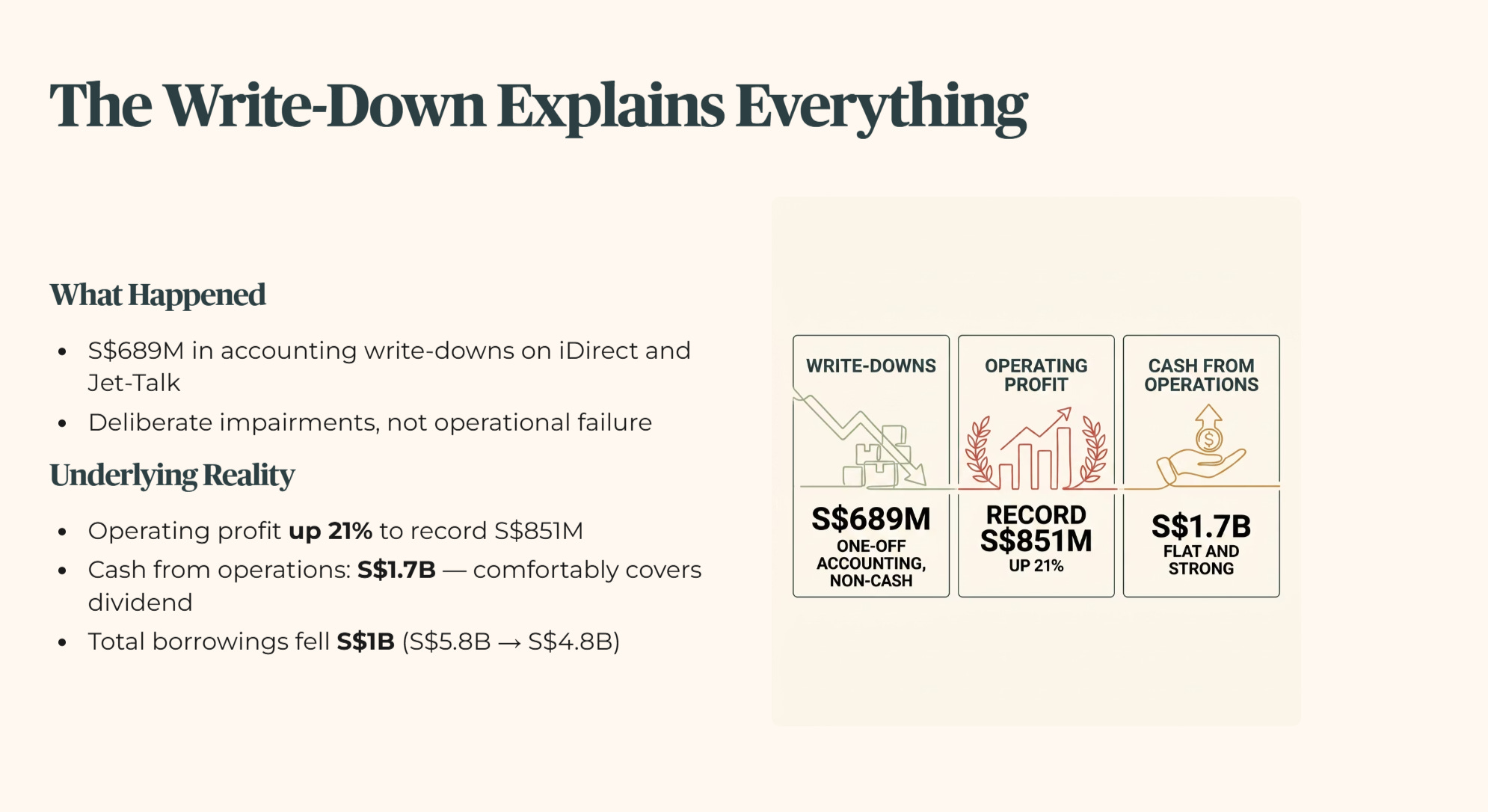

ST Engineering: the profit fell 34 percent. The cash didn’t move at all.

This is the one that looks the most alarming on the surface and turns out to be the least concerning underneath. ST Engineering’s reported net profit fell to S$462.8 million from S$702.3 million, a 34 percent drop. Meanwhile the total dividend went up, from 17 cents to 23 cents a share, an increase that on paper looks completely disconnected from the earnings line right above it.

The gap is almost entirely one-off impairments, S$689 million in accounting write-downs on two underperforming units, iDirect and Jet-Talk, that management chose to take this year. Strip those out, along with some divestment gains that cut the other way, and underlying operating profit was actually up 21 percent to a record S$851 million. Cash from operations came in at S$1.7 billion, essentially flat from the year before and comfortably larger than the entire dividend payout. Total borrowings fell by a billion dollars over the year, from S$5.8 billion to S$4.8 billion.

So the headline profit number here is arguably the least useful figure in the entire release. The business that actually generates cash and pays the dividend was steady to improving, and the balance sheet got stronger, not weaker, in the same year the reported bottom line took its biggest hit. The 5-cent special dividend tucked into that 23 cents came alongside roughly S$700 million in proceeds from selling several smaller units, a genuine one-off, but one funded from strength rather than from stretching the balance sheet.

🟠 Angela’s Observation

This is the one that would have scared me off if I’d only read the headline. A 34 percent profit drop sounds like a company in trouble, not one raising its dividend. But this is exactly the kind of year where the reported number and the real story pull in opposite directions, and it’s a useful reminder that a big write-down taken deliberately, on a business the company was ready to walk away from, is a very different thing from a business that’s actually struggling to make money.

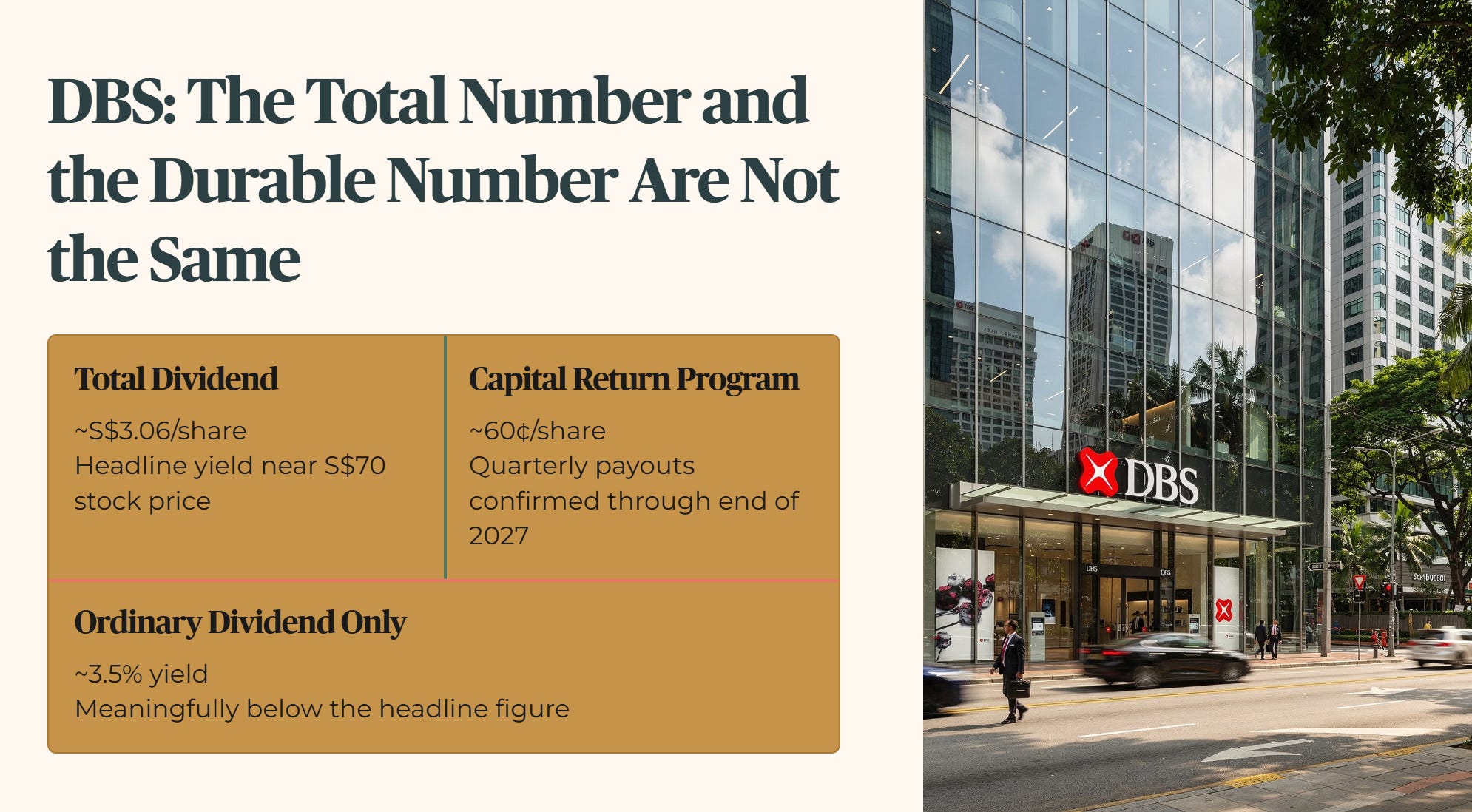

DBS: the total number and the durable number are not the same number

DBS’s total dividend works out to about S$3.06 a share at current levels, which sounds like a healthy yield on a stock trading near S$70. But roughly 60 cents a share of that is a separate capital return program, quarterly payouts confirmed through the end of 2027, layered on top of the regular ordinary dividend.

Strip that program out and the ordinary dividend alone works out closer to 3.5 percent, meaningfully below the total headline figure. That is not a criticism, the bank’s capital position remains very strong and the program is a deliberate, disclosed choice to return excess capital rather than a sign of anything shaky. But it does mean the yield you see quoted today has an expiry date built into part of it. Worth asking yourself, when 2027 arrives and that program runs its course, whether you were counting on the full number continuing or whether you always understood part of it as temporary.

🟠 Angela’s Observation

Banks doing capital return programmes are becoming something of a pattern across this list, not just DBS. It’s a reasonable way for a well-capitalised bank to hand back money it doesn’t need for growth, but it does mean part of today’s yield has an expiry date attached, whether that’s obvious from the headline number or not. Worth asking yourself, the next time a bank’s total yield looks unusually generous, how much of it is ordinary and how much is a program with a calendar on it.

Singtel: nearly a third of this year’s payout came from selling assets, not from the phone bill

Singtel’s full-year ordinary dividend came to 18.5 cents a share, but roughly 5.1 cents of that, close to 28 percent of the total, is a value realisation dividend funded directly from S$3.9 billion in capital recycling proceeds, not from telecom earnings. The core dividend, the part actually tied to running the business, works out closer to 13.4 cents.

That split matters because it tells you which part of this payout repeats. Selling down stakes in assets to return cash to shareholders is a real and legitimate strategy, and management has flagged an expanded S$9 billion recycling program going forward, but a program has a finite pool of assets to sell. The interest cover and debt profile here are genuinely strong, so there is no near-term worry about the dividend itself. The real question is simpler: when you see next year’s Singtel dividend number, check how much of it is still coming from the phone and broadband business versus how much is still riding on asset sales.

🟠 Angela’s Observation

Asset recycling has become the quiet engine behind a lot of dividend growth stories on this exchange, and Singtel is a clean example of it. It’s not a red flag on its own, the company is being transparent about where the money is coming from, but it does shift the real question from “is the dividend growing” to “how many more assets are left to sell, and what happens to the payout once that pool runs dry.”

The yield profile across these five names changes completely once you translate each headline payout into “core business” cash coverage, and that conversion step is exactly where the real sanctuary-versus-yield-trap line appears.