Why I Don't Buy What Billionaires Buy (My Strategy)

When smart money floods Singapore, blue-chip valuations rise—and your dividend checks shrink. Here’s how to find the plays they can’t.

If you’re new here, welcome—The Investing Iguana just hit 1.3 million reads and 65,000 likes. We’re thrilled to welcome over 30 YouTube Premium subscribers and 15 paid Substack members. We landed 8th in Tiger Brokers’ 2024 Influential Tigers ranking. Since October 2025, I’ve produced over 1,200 videos and more than 600,000 watch hours, spanning local and global market trends. If you want deeper context and a sharper edge in Singapore’s markets, you’re right where you need to be.

The Headline That Should Worry You (But Mostly Shouldn’t)

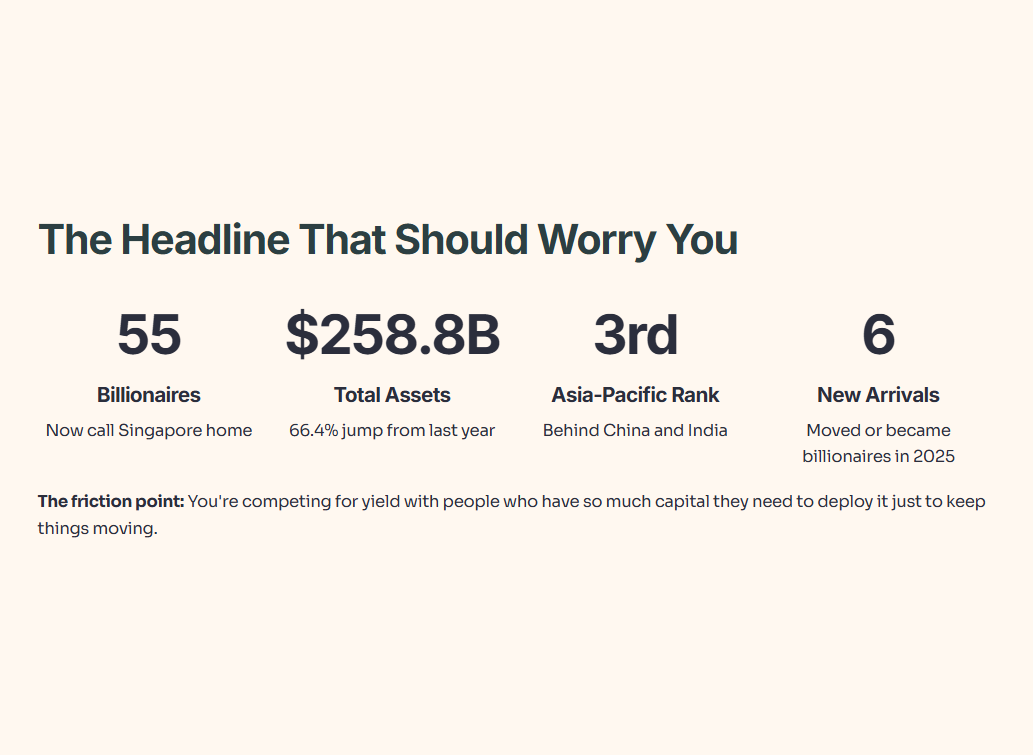

Singapore just hit a wealth milestone. Fifty-five billionaires now hold US$258.8 billion in assets, a 66.4% jump from last year. For context, we’ve just become the third-largest billionaire hub in Asia-Pacific, sitting behind China and India. Six new billionaires moved to or became billionaires in Singapore during 2025 alone.

On the surface, this sounds great. A wealthier nation, stronger stock markets, more investment firepower. Tax revenue flows, infrastructure improves, economy hums along.

But here’s the friction point: you, the retail dividend hunter, are competing for yield with people who have so much capital they need to deploy it just to keep things moving. And their arrival changes the game.

In This Article:

• Iggy’s Data Check: Are The Banks Too Expensive?

• The Wealth Transfer Tsunami: A Bigger Problem Coming

• Your Edge: Go Where the Billionaires Can’t (Or Won’t)

• The Actionable Framework: Your Billionaire-Proof Dividend Strategy

• Iggy’s Verdict

The Capital Inflow Problem: Safety Over Growth

When billionaires and family offices look for homes for their wealth, they’re not hunting for moonshot growth stocks. They’re hunting for safety with returns.

Think about it. If you have US$500 million sitting in cash, you can’t throw it all into speculative biotech plays. You need assets that:

Trade on liquid, regulated exchanges (so you can exit without moving the price)

Generate steady, predictable income

Survive market downturns

Hold purchasing power over decades

In Singapore’s context, that means blue-chip REITs, bank stocks, and utility plays. The big, boring, liquid stuff.

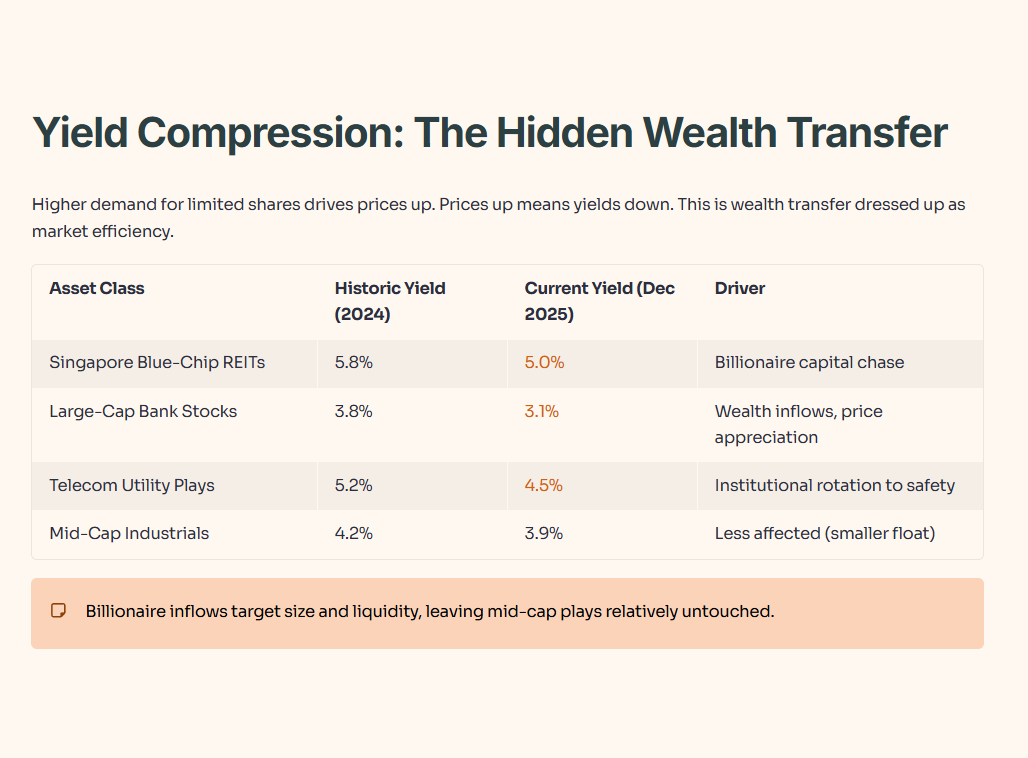

What happens next is textbook market mechanics. Higher demand for a limited supply of shares drives prices up. Prices up means yields down. A REIT yielding 6.5% last year? Today it’s 5.8%. A bank dividend that looked attractive at 4%? Now it’s 3.2%.

This is wealth transfer dressed up as market efficiency.

This table reflects observable yield compression across Singapore’s most popular dividend sectors. Billionaire inflows target size and liquidity, leaving mid-cap plays relatively untouched. The data shows why your traditional hunting grounds are getting crowded.

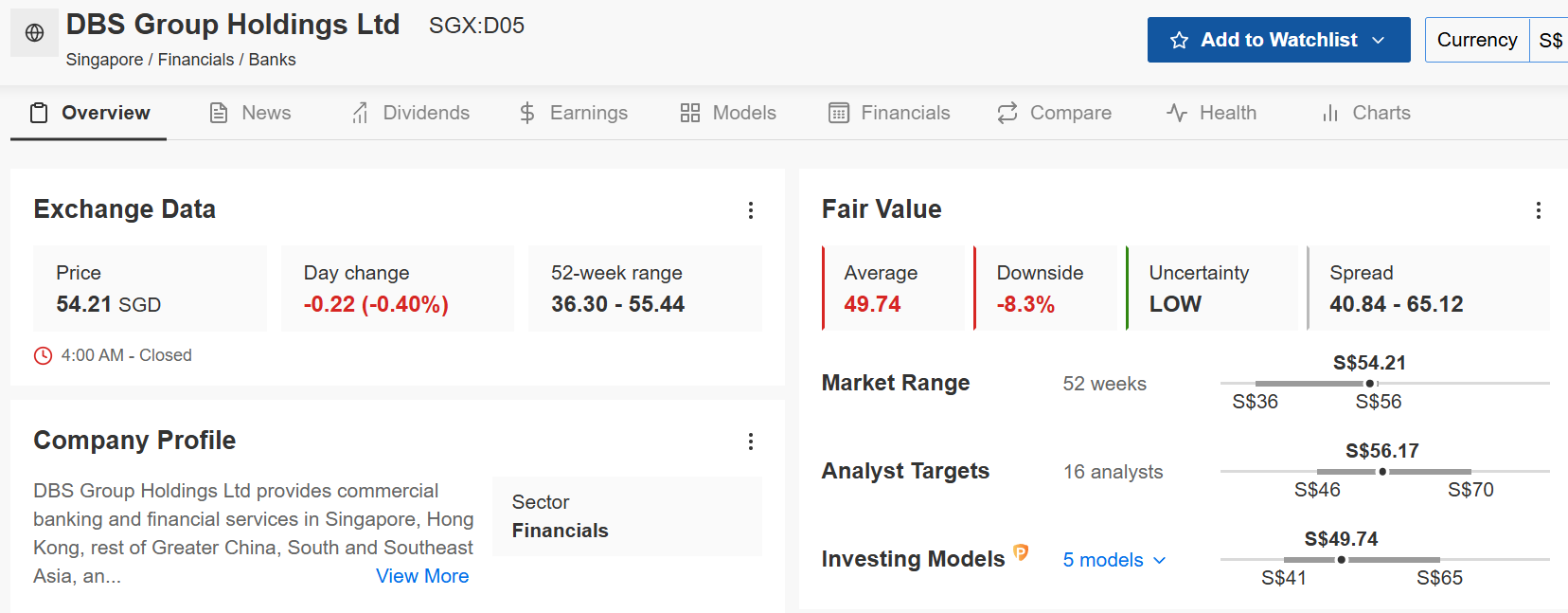

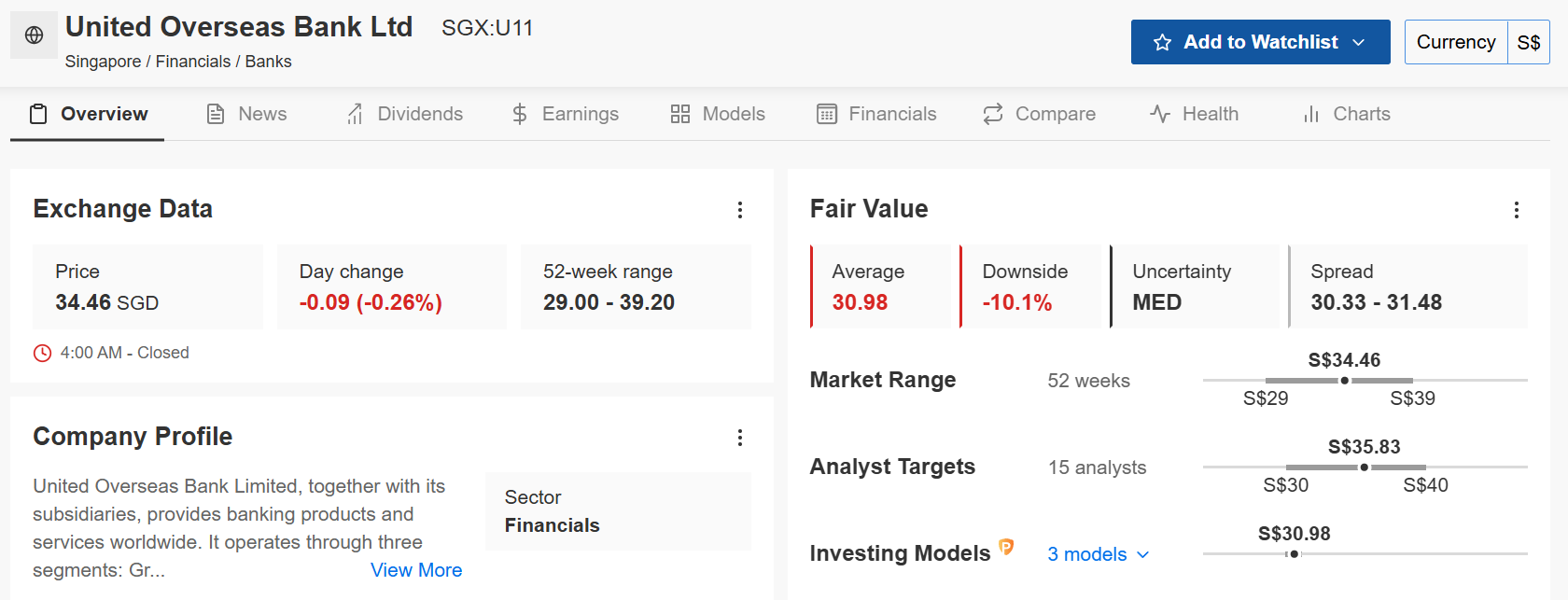

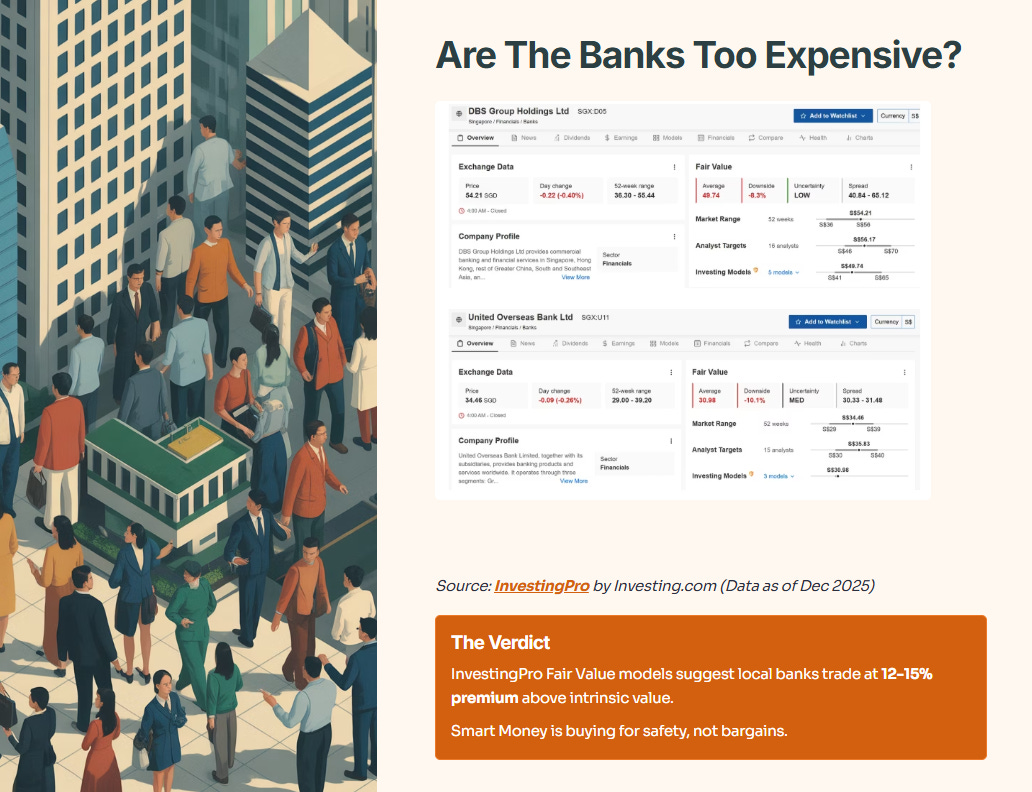

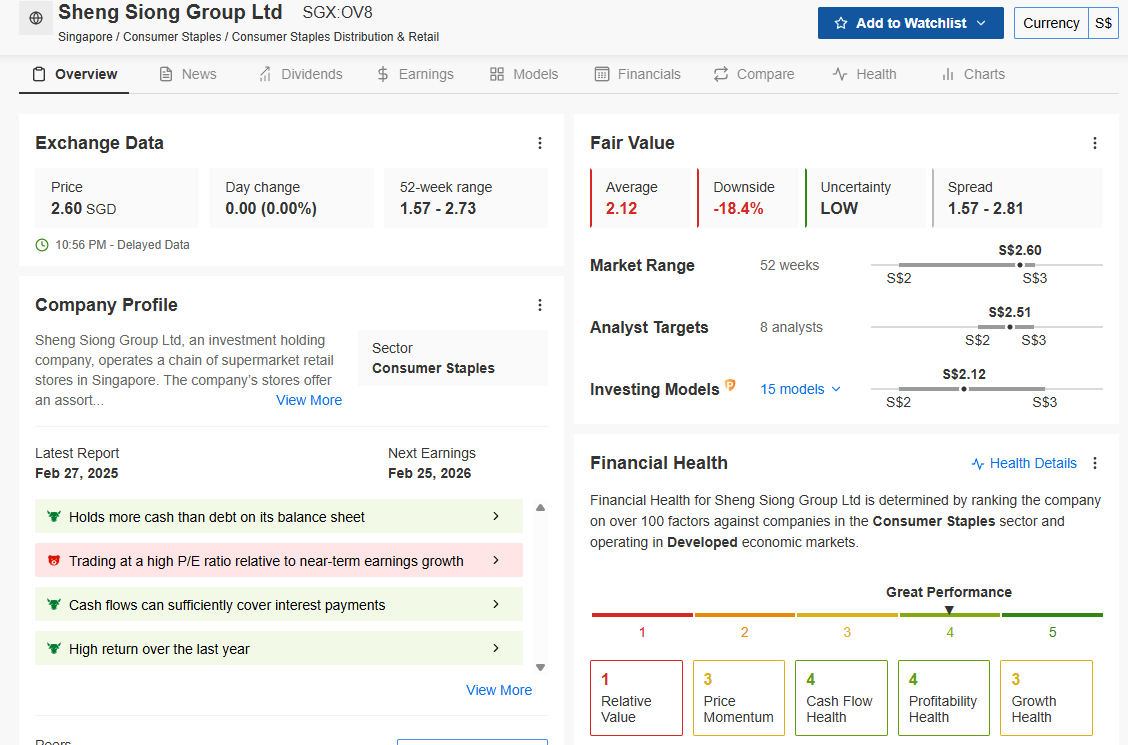

I don’t just guess at these valuations. I check the institutional models to see if the “Big Three” banks are actually overvalued, or if the billionaires are onto something.

Iggy’s Data Check: Are The Banks Too Expensive?

Source: InvestingPro by Investing.com (Data as of Dec 2025). Premium members can use code INVESTINGIGUANA for up to 50% off.

The Analysis: The InvestingPro Fair Value models—which average out 10+ financial metrics—suggest the local banks are currently trading at a premium of roughly 12-15% above their intrinsic value. The “Smart Money” is buying for safety, not for a bargain.

The UBS Billionaire Ambitions Report confirms this pattern. Singapore’s new billionaires include tech entrepreneurs (Justin Sun from Tron, the Zhang brothers from Mixue Ice Cream & Tea), and many have connections to China’s booming tech ecosystem. They’re not here to gamble. They’re here to park wealth.

Iggy’s Insight: They’re going to win the valuation game because they can afford to wait 20 years for a 3% yield. You probably can’t.

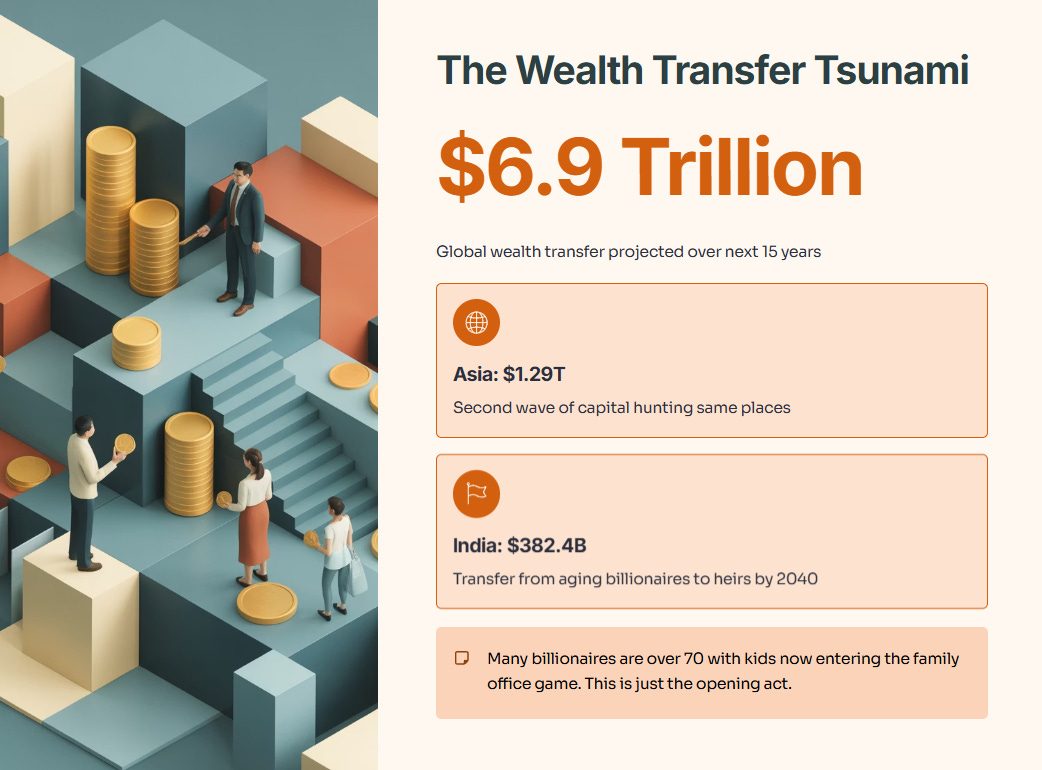

The Wealth Transfer Tsunami: A Bigger Problem Coming

But here’s what keeps me up at night: the billionaires today are just the opening act.

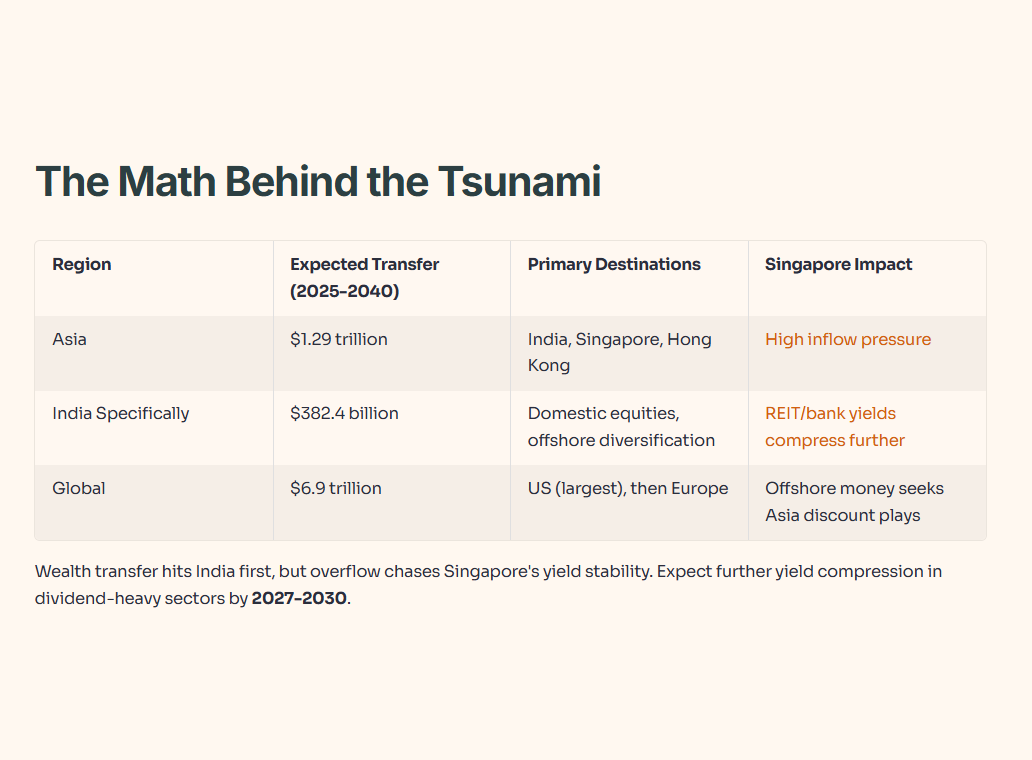

UBS projects US6.9trillioninwealthwilltransfergloballyoverthenext15years.InAsiaalone,that′sUS1.29 trillion. India alone will see US$382.4 billion transfer from ageing billionaires to their heirs by 2040. Many of these folks are over 70 with kids who are now entering the family office game.

What does that mean? A second wave of capital hunting for exactly the same places: Singapore’s regulated, liquid, income-generating assets.

Consider the math:

Wealth transfer will hit India first and hardest, but overflow will chase Singapore’s yield stability. Expect further yield compression in dividend-heavy sectors by 2027-2030. The pattern is clear: safe, liquid, income-generating assets in well-regulated financial hubs will remain pressure-cooker valuation zones.

So what’s the retail investor’s move?

Your Edge: Go Where the Billionaires Can’t (Or Won’t)

Here’s the thing about billionaire capital: it’s elephantine. A family office with US$2 billion can’t profitably deploy it into a small-cap industrial play trading 200,000 shares a day. They’d move the price, face liquidity risk, and spend more on analysis than the position is worth.

That’s your edge.

The retail investor—armed with CPF/SRS tax advantages and zero institutional overhead—can hunt in the overlooked corners where billionaires can’t economically compete.

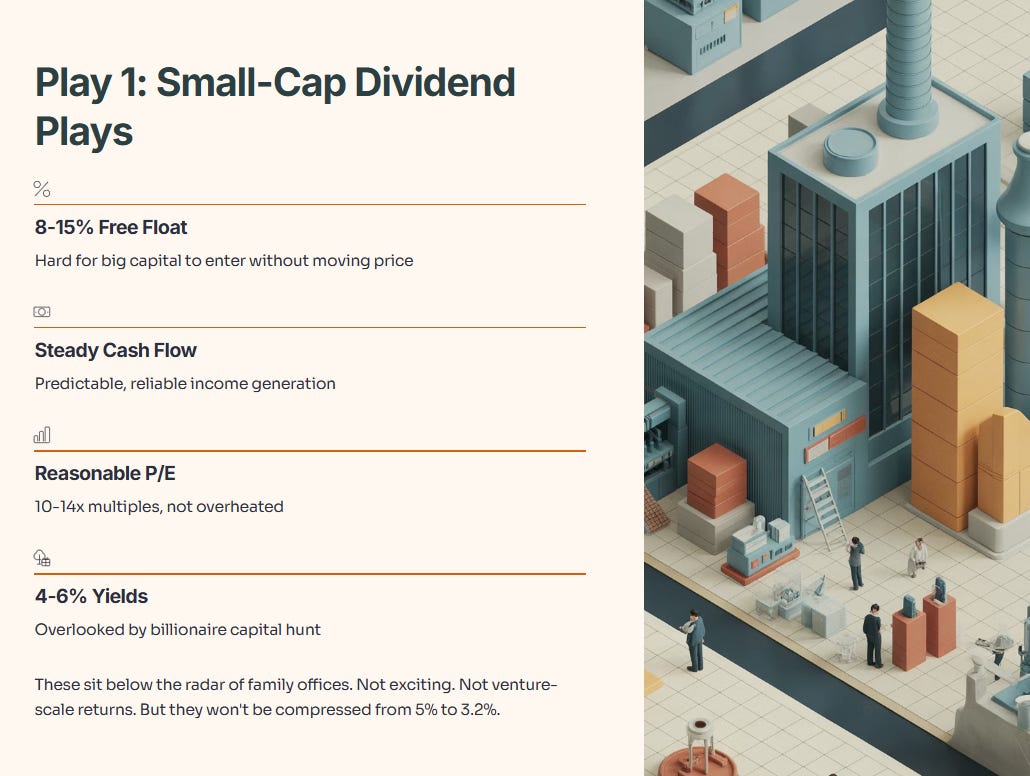

Play 1: Small-Cap Dividend Plays with Genuine Pricing Power

Look for mid-cap industrials or healthcare plays trading on SGX that:

Have 8-15% free float (hard for big capital to enter without moving price)

Generate steady, predictable cash flow

Trade at reasonable P/E multiples (10-14x)

Pay 4-6% yields overlooked by the billionaire capital hunt

These sit below the radar of family offices. Not exciting. Not venture-scale returns. But they won’t be compressed from 5% to 3.2% because nobody big is chasing them.

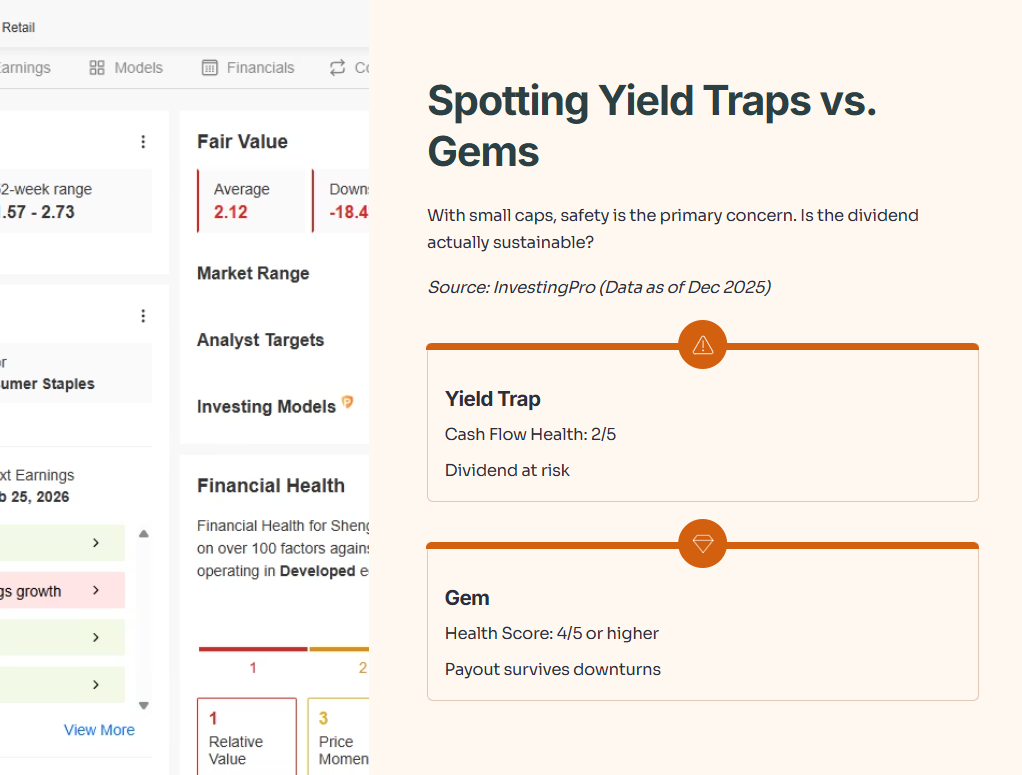

But with small caps, safety is the primary concern. Is the dividend actually sustainable, or is it a yield trap? This is where I look at Financial Health scores.

Iggy’s Data Check: Spotting a “Yield Trap” vs. a “Gem”

Source: InvestingPro (Data as of Dec 2025). Premium members can use code INVESTINGIGUANA for up to 50% off.

The Analysis: When hunting small caps, ignore the yield percent for a second and look at the “Cash Flow Health” bar. If it’s a 2/5, that dividend is at risk. We want to see a Health Score of at least 4/5 (Great Performance) to ensure the payout survives a downturn.

Play 2: REITs in Niche Segments (Industrial, Cold Storage, Healthcare)

While mega-cap REITs face yield compression, smaller-segment REITs focused on industrial warehousing or cold-chain logistics still trade at healthier yields. Why? Billionaires want marquee assets: office towers, malls in Orchard Road. They don’t want to explain a cold-storage REIT to their limited partners. Yields can still hover 5.5-6.5% if the operator has clean management and real cash flow.

Play 3: Use Tax-Advantaged Accounts Strategically

This is not rocket science, but it’s often overlooked: SRS contributions let you access the same blue-chip plays (lower yield) while reducing your tax burden. So the “squeeze” on yield is less painful because you’re keeping more of what you earn.

The Actionable Framework: Your Billionaire-Proof Dividend Strategy