The 3.2% Forensic Floor: Why Most 6% Yield REITs are Now a Bad Trade

The S$2.4 billion S-REIT debt wall is hitting; check if your retirement income is backing First REIT’s May cliff.

The 2026 S-REIT Forensic Audit: Why the STI Peak is a Retirement Mirage

The Straits Times Index (STI) just hit 4,812.75, having teased the 5,000 psychological summit. If you’re reading the mainstream headlines, the champagne is flowing. But if you’re a Singaporean retiree sitting in your HDB flat looking at your CDP statement, specifically your REIT holdings, the celebration feels a little hollow. It’s like being invited to a wedding banquet at a five-star hotel only to find out you’re sitting at the table nearest the kitchen door—you can smell the food, but you aren’t eating.

While the “Big Three” banks are lifting the index, the S-REIT sector is fighting a quiet, surgical war against a S$2.4 billion debt wall maturing throughout 2026. The paradox is simple: the headline is green, but the distributions are under siege. The Elite 190 Inner Circle members have already started asking the right question: why is the index at a high-water mark while my DPU is trending toward a three-year low?

In This Article:

The Forensic Floor: The Moat is Drying Up

The “Fortress” Plays: Three Anomalies in the Storm

Digital Core REIT (SGX: DCRU) — The Refinancing Anomaly

Elite UK REIT (SGX: MXNU) — The Sovereign Backstop

The SORA Arbitrage — Treasury Discipline

The Red Flags: Three Forensic Traps

First REIT (SGX: AW9U) — The May 2026 Cliff

The “Index Drag” of Large-Caps

The Currency Erosion (SGD vs. JPY/IDR)

The Final Audit: The Yield Spread Formula

InvestingPro Reality Check

Iggy's Verdict

About Iggy & the Elite 190

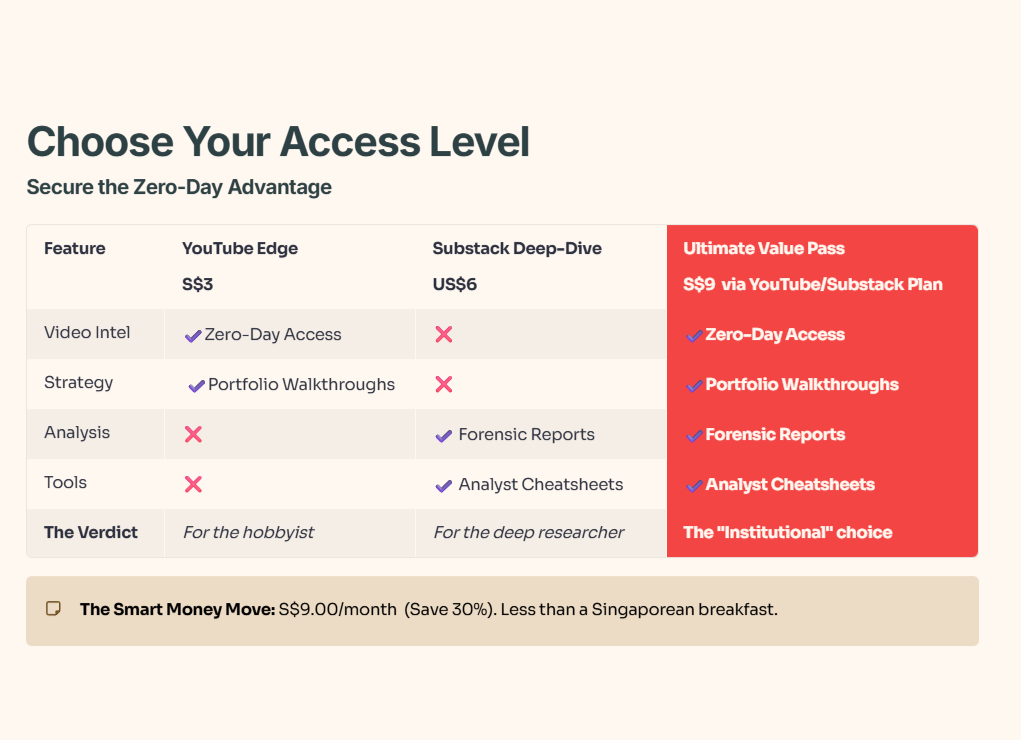

The 48-Hour Gap is Closing. In this market, the difference between a “Sanctuary” and a “Yield Trap” is often decided in a single trading session. If you’re reading this as a free subscriber, you’re looking at 14-day-old data—and in the time it took you to open this email, the “Smart Money” has already moved.

The Elite 190 don’t wait for the lag. They get zero-day forensic reports, the full “Red Zone” watchlist, and institutional-grade cheatsheets the second they are finalized.

For S$9/month—less than a kopi and kaya toast set at Raffles Place—you stop being the “Exit Liquidity” and start being the Analyst.

👉 [Secure Your Seat in the Elite 190 Here]

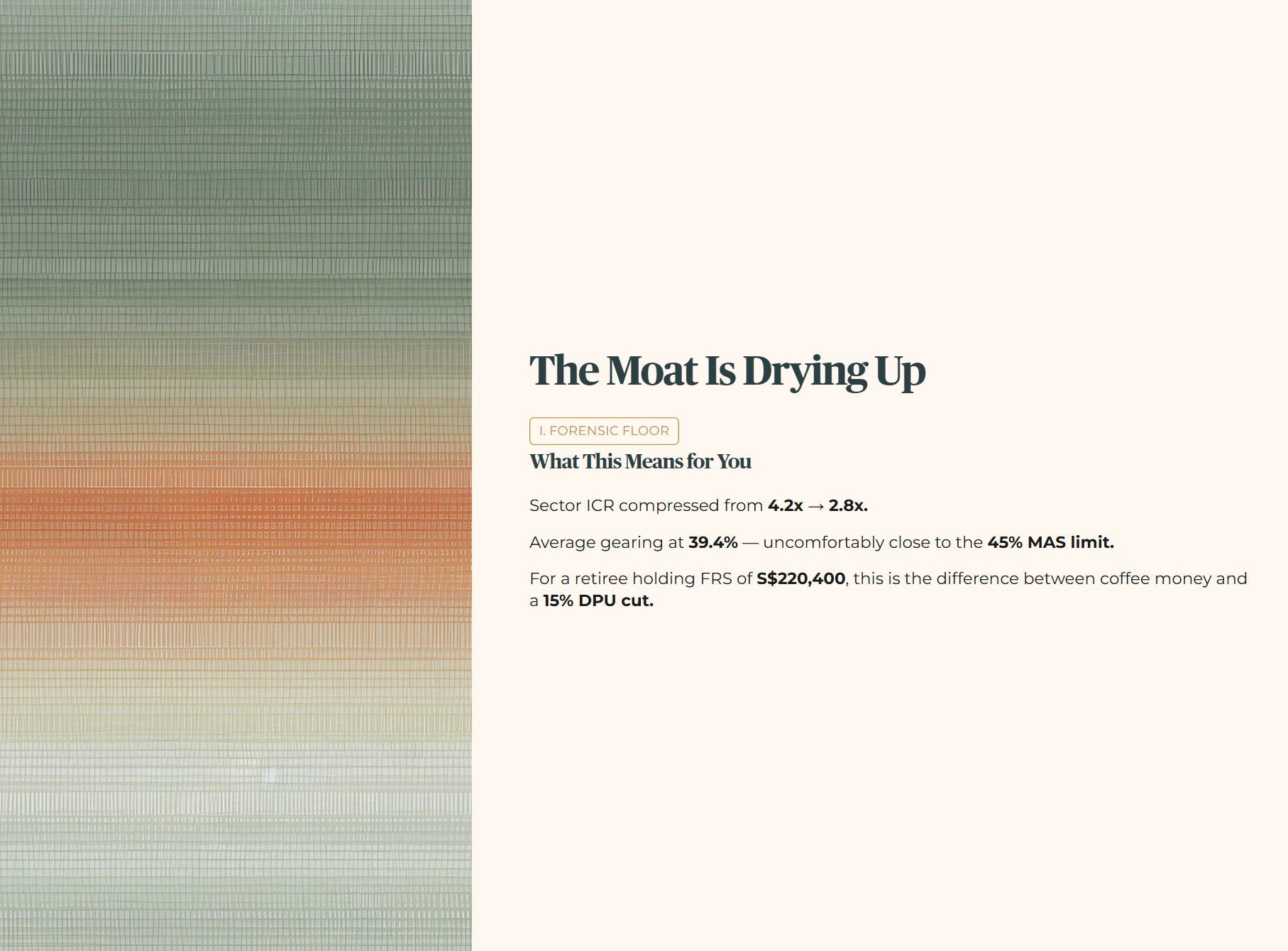

I. The Forensic Floor: The Moat is Drying Up

Before we pick winners, we need to talk about the Interest Coverage Ratio (ICR). In 2023, the sector average was a healthy 4.2x. Today, as we sit in March 2026, that average has compressed to 2.8x.

For a Singaporean investor managing a Full Retirement Sum (FRS) of S$220,400, this isn’t just a spreadsheet error. This is the difference between a stable “coffee money” stream and a 15% DPU cut to satisfy a bank’s covenant. When the average sector gearing hits 39.4%, you are uncomfortably close to the 45% MAS regulatory limit for those with weak ICRs.

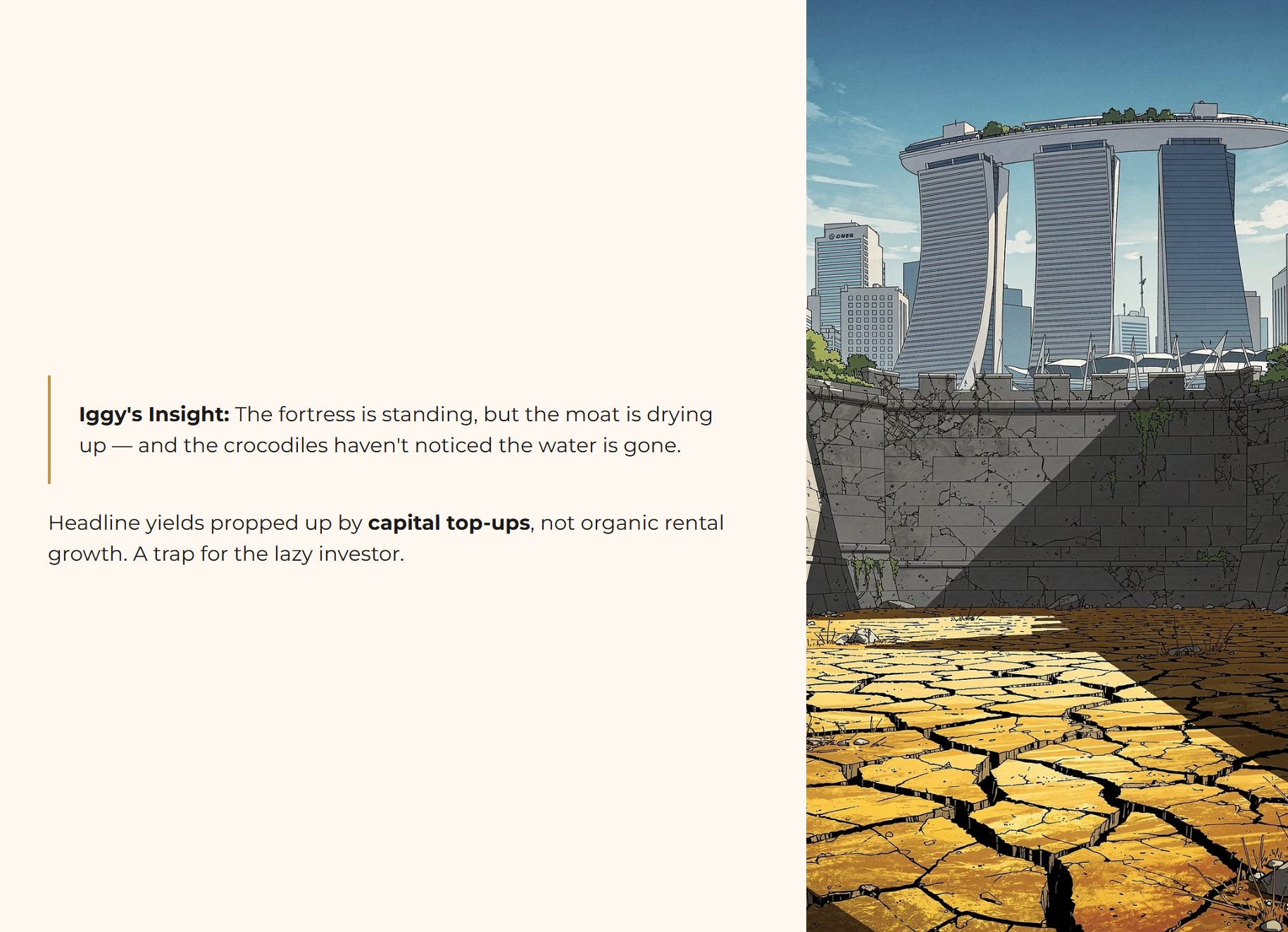

🦎 Iggy’s Insight: The current S-REIT sector is a trap for the lazy investor. We see a landscape where headline yields are being propped up by capital top-ups rather than organic rental growth. The fortress is standing, but the moat is drying up—and the crocodiles haven’t noticed the water is gone.

The Financial Health Baseline Table

The metric that concerns me most is the Fixed Rate Debt percentage dropping to 76%. This tells us that as old, low-interest hedges expire, REIT managers are struggling to find affordable replacements. They are leaving your portfolio exposed to the volatility of the SORA because they have no other choice.

II. The “Fortress” Plays: Three Anomalies in the Storm

1. Digital Core REIT (SGX: DCRU) — The Refinancing Anomaly

DCRU is the rare bird in this environment. While others sell crown jewels to keep their gearing below 45%, DCRU has maintained a 37.1% gearing ratio.

The Receipts: 100% of their debt is unsecured. No major maturities until late 2027. This is significantly lower than their 2024 peak gearing of 40.5%.

The Peer Context: Compare this to Keppel DC REIT, which, while high-quality, carries more complex geographic tax risks across Europe and North America.

The Wallet Impact: For a 55-year-old using SRS funds, this low leverage reduces the “Rights Issue” nightmare. You know the story—the REIT announces a rights issue at a deep discount, and you either fork out more cash or watch your stake get diluted. DCRU minimizes that threat.

2. Elite UK REIT (SGX: MXNU) — The Sovereign Backstop

Elite UK is undergoing a fundamental shift from a “risky micro-cap” to a “social infrastructure” play. The catalyst is the FTSE Global Micro-Cap Index re-entry on March 20th.

The Receipts: They secured £24.3 million in new lease commitments from the UK Government’s Department for Work and Pensions. This isn’t a speculative startup; this is the British taxpayer.

The Wallet Impact: Unlike UK retail REITs that are dying, government-backed leases are the “UK version of CPF.” At a 9% yield, you’re being paid a massive premium to wait for the institutional money to rotate in.

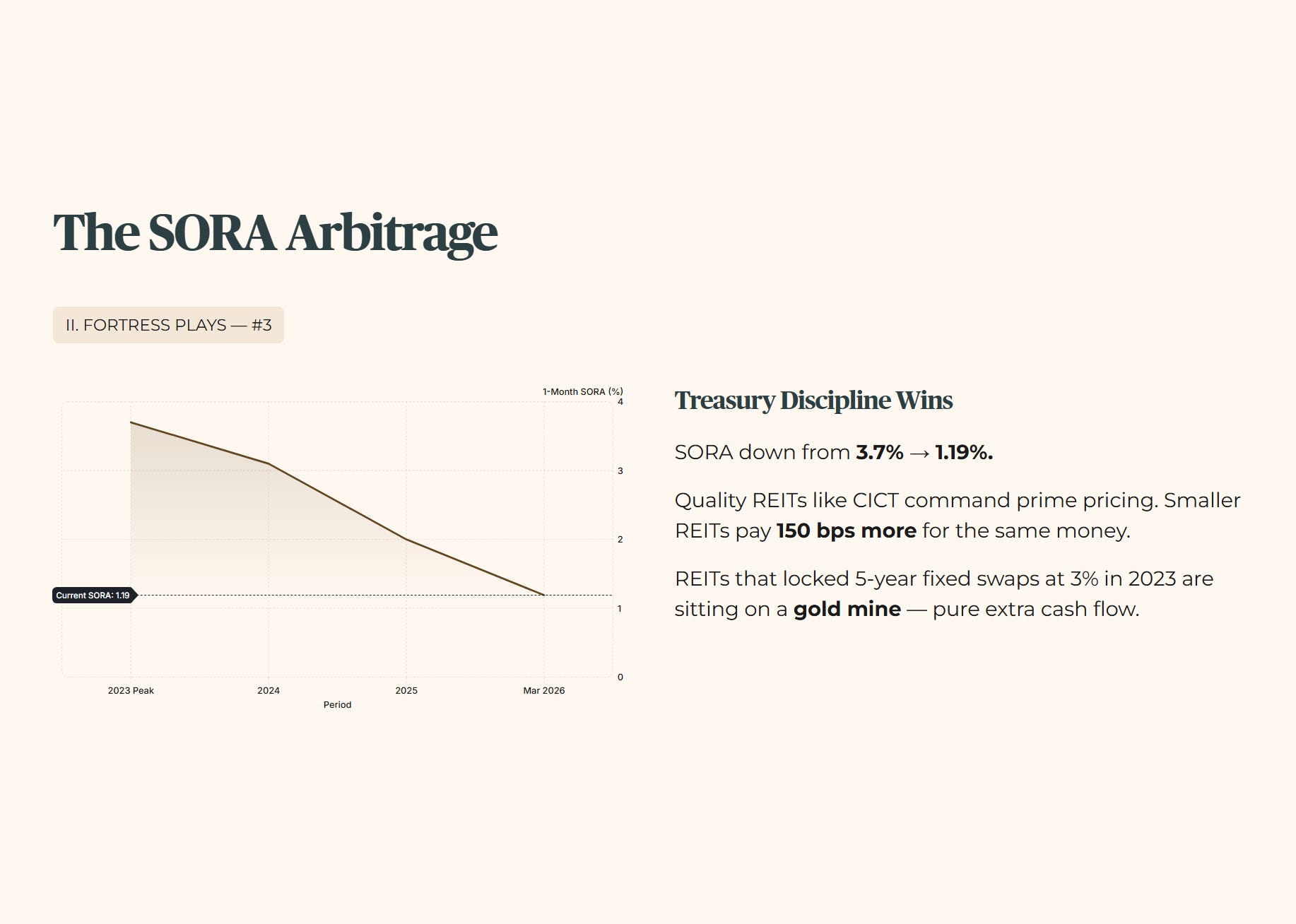

3. The SORA Arbitrage — Treasury Discipline

The 1-month SORA has stabilized at ~1.19%, way down from the 3.7% peak of 2024.

The Logic: High-quality REITs like CapitaLand Integrated Commercial Trust (CICT) can walk into any bank in Singapore and demand prime pricing. Smaller REITs are paying 150 basis points more for the same money.

The Wallet Impact: A REIT that locked in 5-year fixed swaps at 3% in 2023 is now sitting on a gold mine. This is like finding out your HDB mortgage rate just dropped while your salary stayed the same—it’s pure “extra” cash flow in your pocket.

“But the real danger begins in the next section — the forensic traps that could silently erase two years of your dividends before you even notice.”