America is Broke ($38T): Why It’s Time to Sell 'US Hope' and Buy 'Singapore Reality

Forget the AI Hype: Why Singapore Banks and Construction Orders are the 'Fortress' you need against the tariff storm.

In This Article:

The Global Headline: The $38 Trillion Time Bomb and the Tariff Wall

Iggy’s Insight: The “Contagion” Effect

The Local Impact: The “Invisible” Squeeze on Your Wallet

Iggy’s Insight: The “3% Hurdle” Rule

The Data Proof: The “Boring” Fortresses vs. The Gamblers

Iggy’s Insight: The “Double-Loss” Trap

The Action Plan: The 2026 “Bunker” Strategy

InvestingPro Reality Check

Iggy's Verdict

1. The Global Headline: The $38 Trillion Time Bomb and the Tariff Wall

It is January 24, 2026. While you were busy planning your Chinese New Year reunion dinner, the United States just walked to the edge of a fiscal cliff and looked down. The latest data from the CRFB is terrifying: the US National Debt has hit $38 Trillion, effectively reaching 100% GDP parity. This isn’t just a number on a screen; it is a structural fracture in the global financial system. When the world’s reserve currency is levered to the hilt, the “risk-free rate” becomes a misnomer.

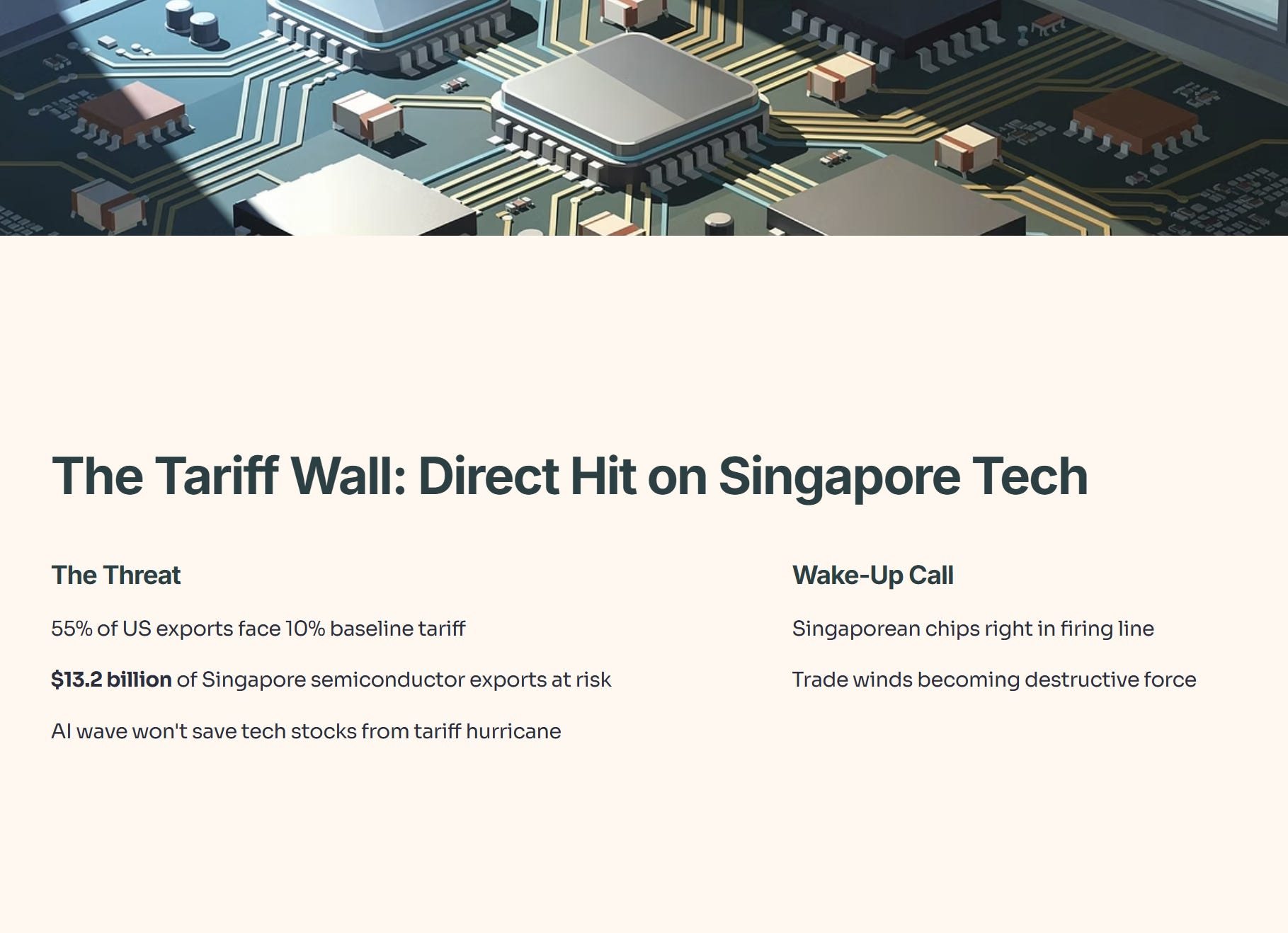

To make matters worse, the trade winds are turning into a hurricane. We are looking at a scenario where 55% of US exports are now facing a baseline tariff of 10%. For an open economy like Singapore, this is a direct hit. Specifically, S$13.2 billion worth of our semiconductor exports are at risk. If you are holding tech stocks thinking the AI wave will carry you forever, you need to wake up. The “Tariff Wall” is being built, and Singaporean chips are right in the firing line.

🦎 About Iggy the Investing Iguana

Welcome to the Iguana Pit! If you’re new here, I’m Iggy: your guide through the dense jungle of the Singapore markets. My mission is simple: to spot the predators before they spot your portfolio.

We are now 5,800+ subscribers strong across YouTube and Substack, focusing purely on the data-driven alpha that mainstream media misses.

🚀 Join the “Elite 150” Inner Circle

Real alpha is found behind the velvet rope. Stop following the herd and start following the data with our 150+ paid members.

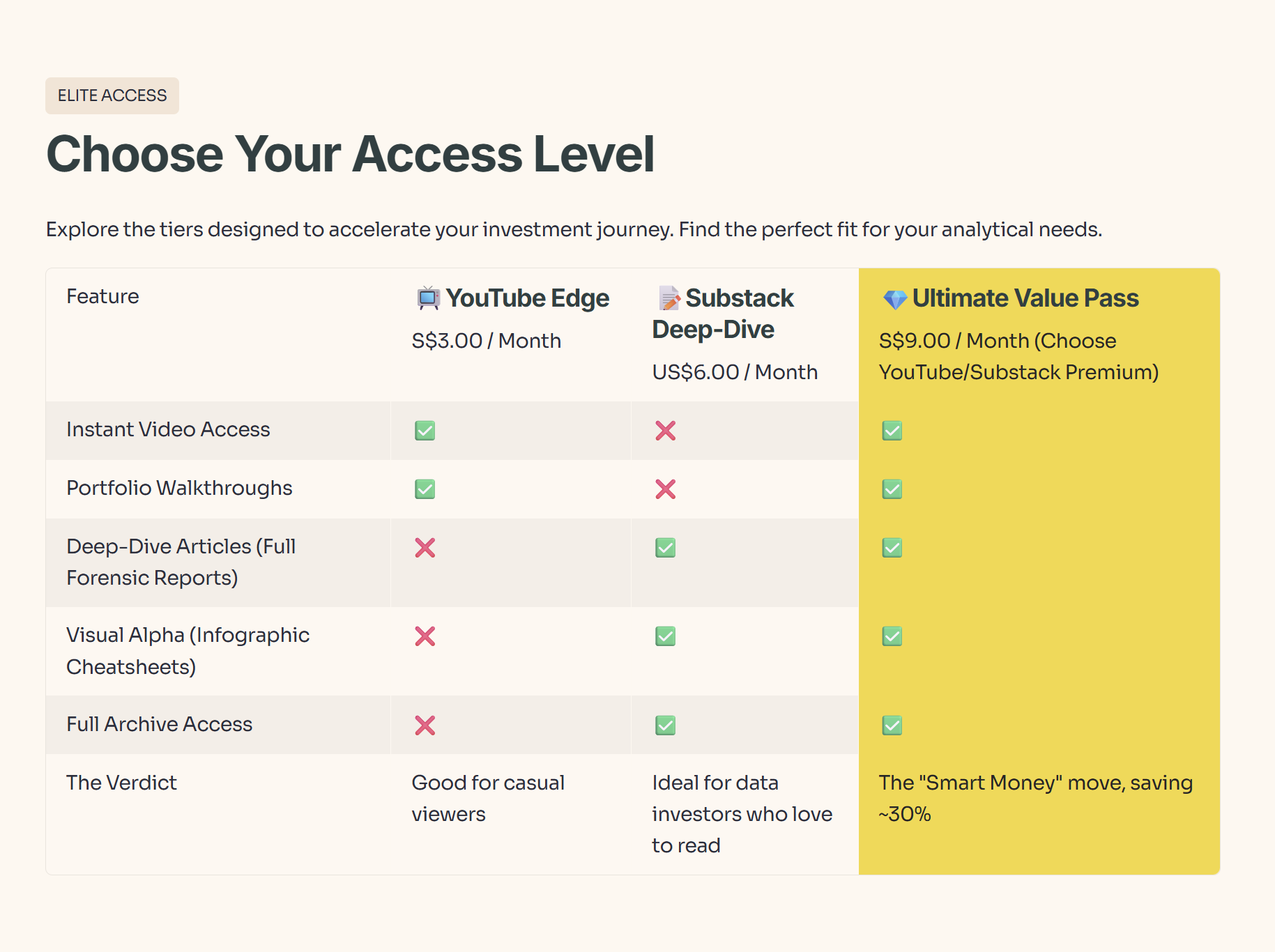

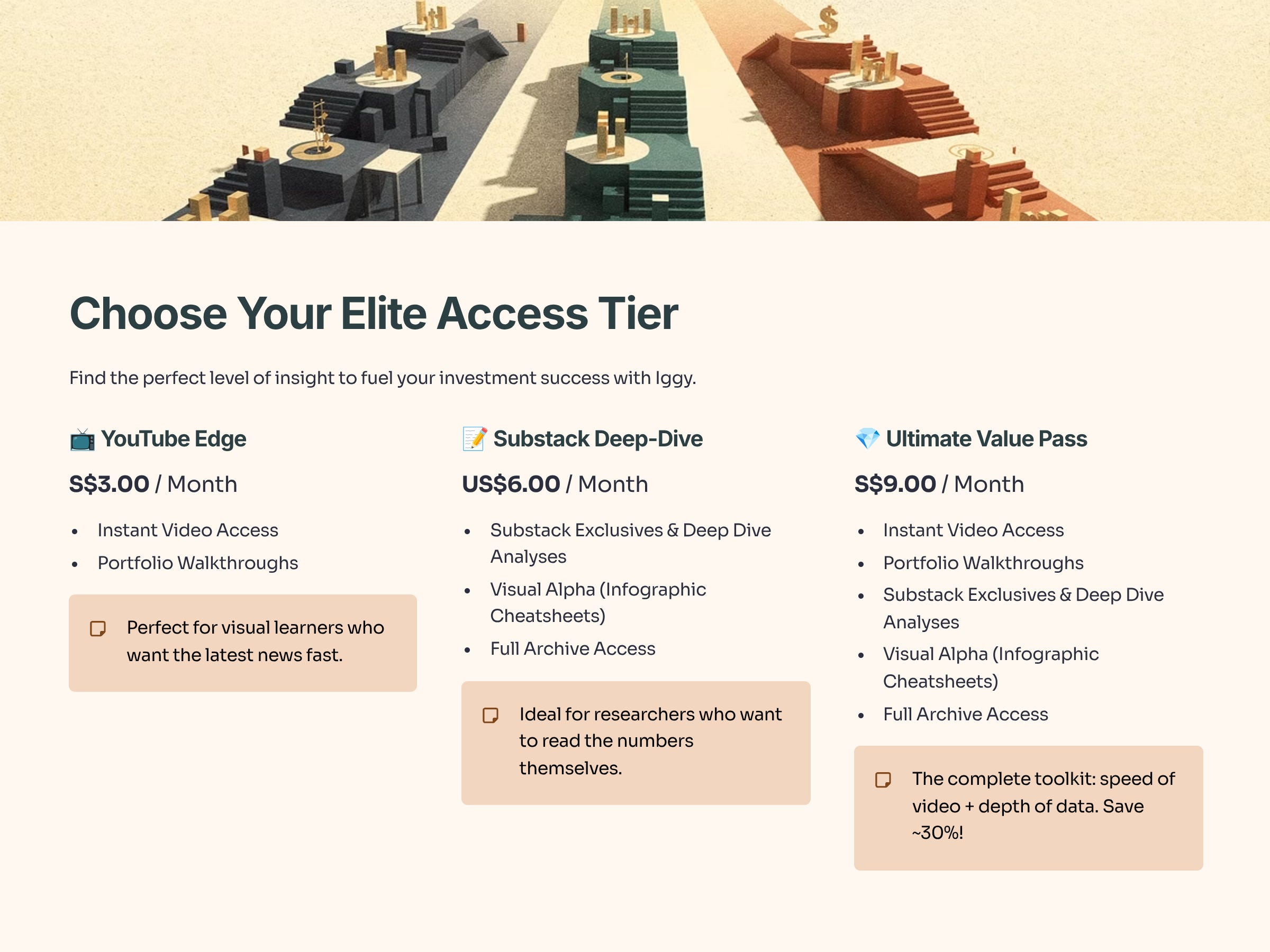

📺 The YouTube Edge (S$3/mo): Beat the Delay.

Instant Access: Watch new videos the moment they drop.

The Free Tier Trap: Free subscribers wait up to 14 days to see the same video. (By then, the news is old and the trade is gone).

📝 The Substack Deep-Dive (US$6/mo): Unlock the Vault.

Zero Paywalls: Read the full “Deep Dive” articles and “Substack Exclusive” articles found only on Substack.

Visual Alpha: Download exclusive Infographic Cheatsheets not available to free readers.

💎 The Ultimate Value Pass (S$9/mo): (BEST VALUE)

Get It All: Paid via YouTube, this bundle grants you Instant Video Access AND Full Substack Access.

The Math: You save ~30% compared to buying them separately. It’s the “Smart Money” move.

Why wait 2 weeks for old news? Get the data while it’s fresh. 👉 Join Here: https://www.youtube.com/@InvestingIguana/membership

💡 Iggy’s Insight: The “Contagion” Effect

Most investors think, “I live in Bedok, why do I care about US debt?” Here is the mechanism: When the US government has to issue massive amounts of debt to cover that $38T hole, they suck global liquidity out of the room like a vacuum. Capital flees emerging markets and safe havens alike to chase US Treasury yields. This spikes borrowing costs globally. Your mortgage rate in Singapore is ultimately tethered to this dysfunction. You are paying for their excess.

2. The Local Impact: The “Invisible” Squeeze on Your Wallet

Closer to home, the narrative is shifting from “Growth” to “Survival.” The Ministry of Trade and Industry (MTI) is forecasting 2026 core inflation at a manageable 1.3%. But let me be clear: Do not trust the headline number to plan your retirement.

While official core inflation is low, the items that actually hurt your daily cash flow are surging. We are seeing sticky inflation anchors in food (oils +3.6%, sugar +3.8%) and utilities driven by the carbon tax. When you go to the hawker centre or pay your SP Services bill, it doesn’t feel like 1.3%.

And here is the kicker: The “Johor Escape Valve” is closing. For years, Singaporeans have mitigated local inflation by crossing the causeway for cheap groceries and petrol. That trade is dying. The Malaysian Ringgit has strengthened to RM3.13 per SGD as of yesterday—its strongest level since March 2022. Johor tourism is already down 25% YoY because the math doesn’t work anymore. You are being squeezed by rising costs at home and a stronger currency next door.

💡 Iggy’s Insight: The “3% Hurdle” Rule

I never use the government’s 1.3% inflation forecast for financial planning. It breeds complacency. I strictly apply a 3% Stress Test to all my portfolio projections. Why? Because your personal inflation rate—dominated by healthcare, food, and energy—is always higher than the “average” basket. If your portfolio can’t beat a 3% hurdle, you aren’t investing; you are slowly bleeding purchasing power.

🛑 A Critical Note on My “3% Inflation” Rule (Read This Before You Comment)

“Iggy, stop saying inflation is 3%. The official Core Inflation for 2025 was only 0.7%!”

I’ve seen this comment from sharp-eyed readers like Styler in our community, and you are absolutely correct. The official MAS data shows Core Inflation cooling to 0.7% in 2025, with a forecast of just 0.5%–1.5% for 2026. Historically, Singapore’s CPI has indeed averaged below 2%.

So, why do I insist on using 3% in my models?

It is not a prediction; it is a Stress Test.

When engineers build a bridge, they don’t design it to hold exactly the weight of the cars they expect. They build it to hold three times that weight. That is called a “Margin of Safety.”

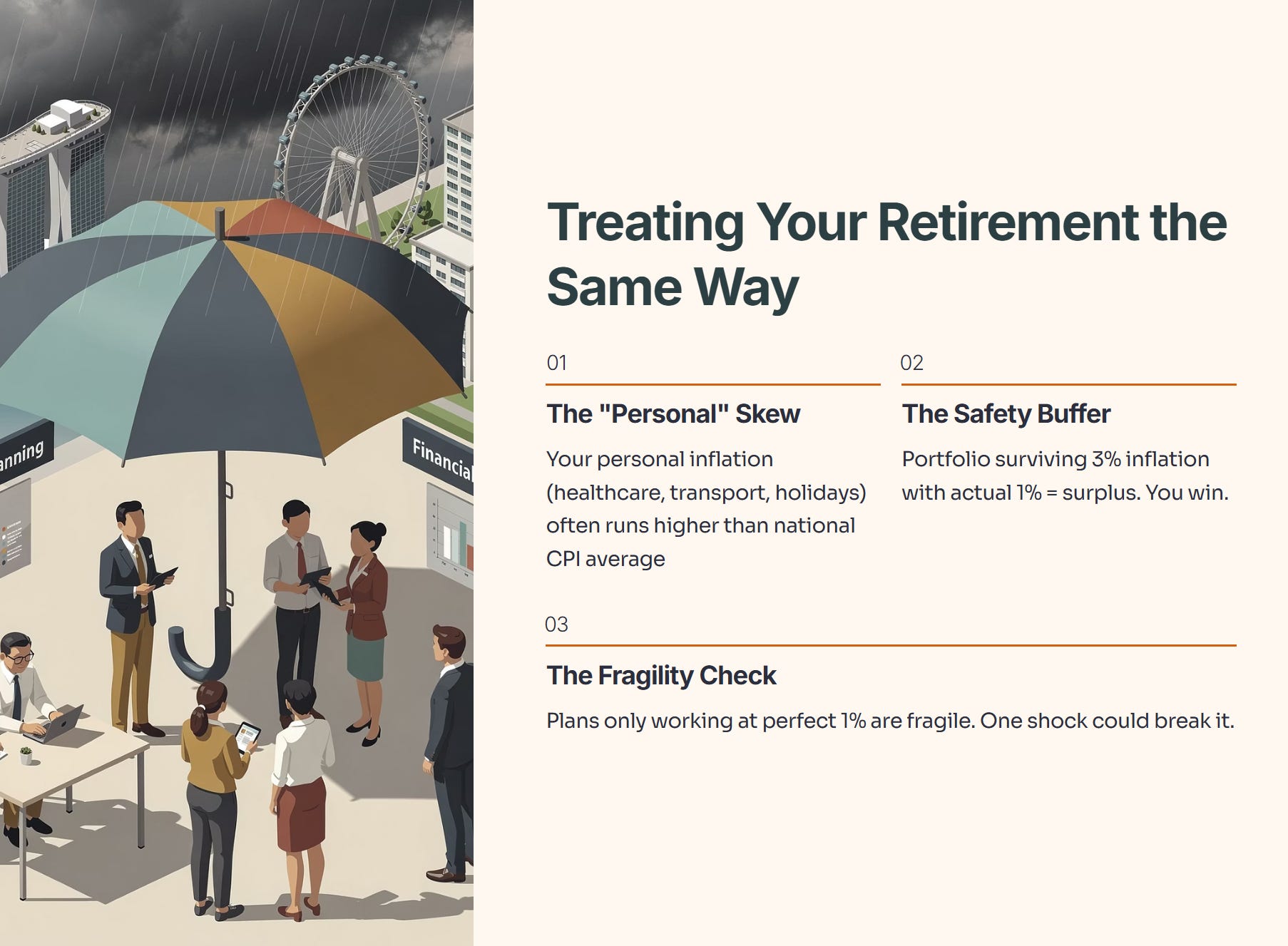

I treat your retirement the same way.

The “Personal” Skew: Official CPI is an average. But your personal inflation (healthcare, private transport, that extra holiday) often runs higher than the national basket.

The Safety Buffer: If I build a portfolio that survives a 3% inflation hurdle, but actual inflation comes in at 1%, you win. You have a surplus.

The Fragility Check: If your retirement plan only works because inflation stays at a perfect 1%, your plan is fragile. One supply chain shock or oil spike could break it.

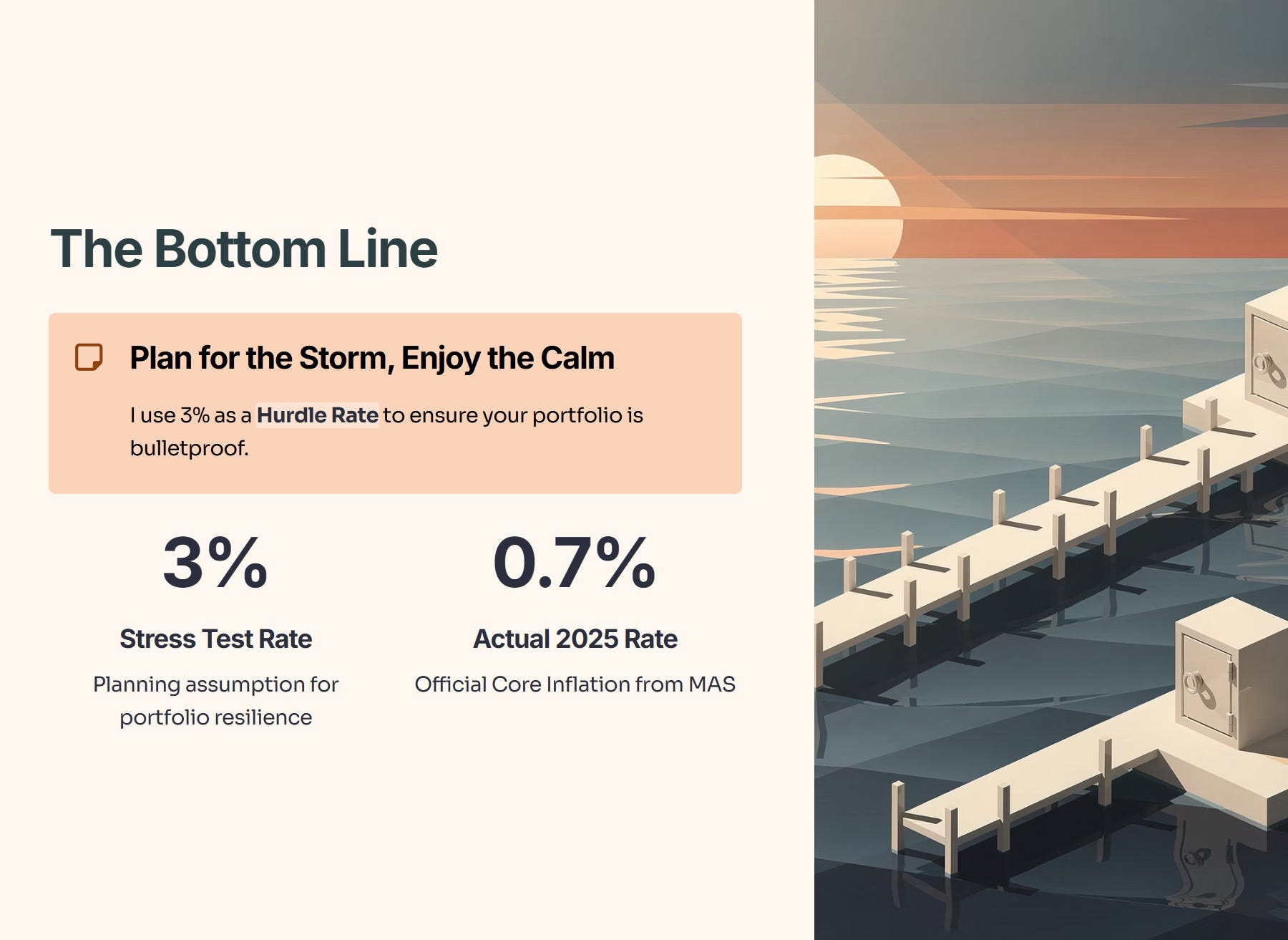

The Bottom Line: I use 3% as a “Hurdle Rate” to ensure your portfolio is bulletproof. We plan for the storm (3%) so we can enjoy the calm (0.7%).

3. The Data Proof: The “Boring” Fortresses vs. The Gamblers

Let’s look at the hard evidence. While the global tech sector shakes under tariff threats, the “boring” domestic economy is quietly booming.

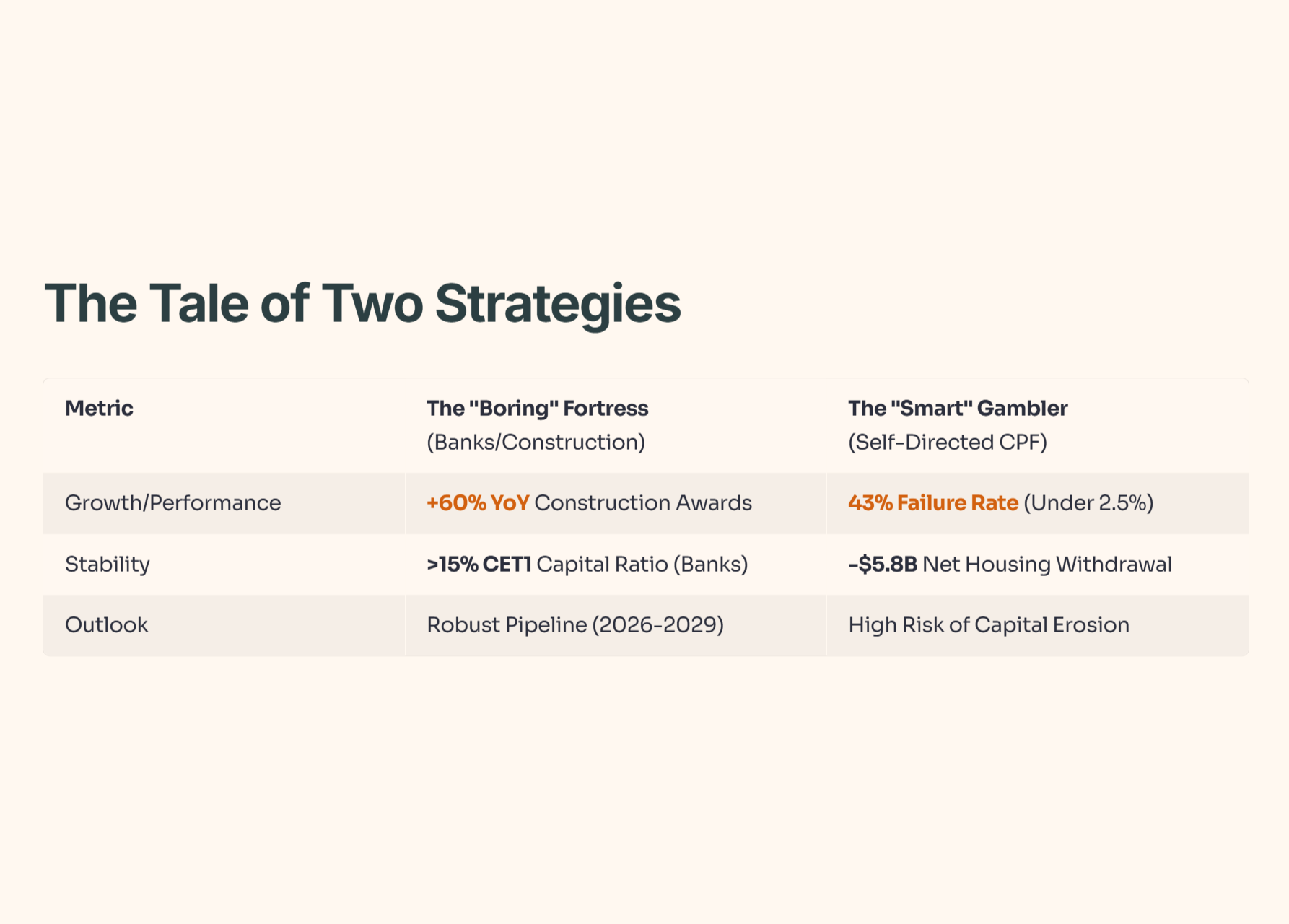

The construction sector is on fire. Contract awards have surged by a massive 60% Year-on-Year in early 2025, and the pipeline through 2029 looks robust. This is real economic activity—steel, concrete, and labor—not paper gains.

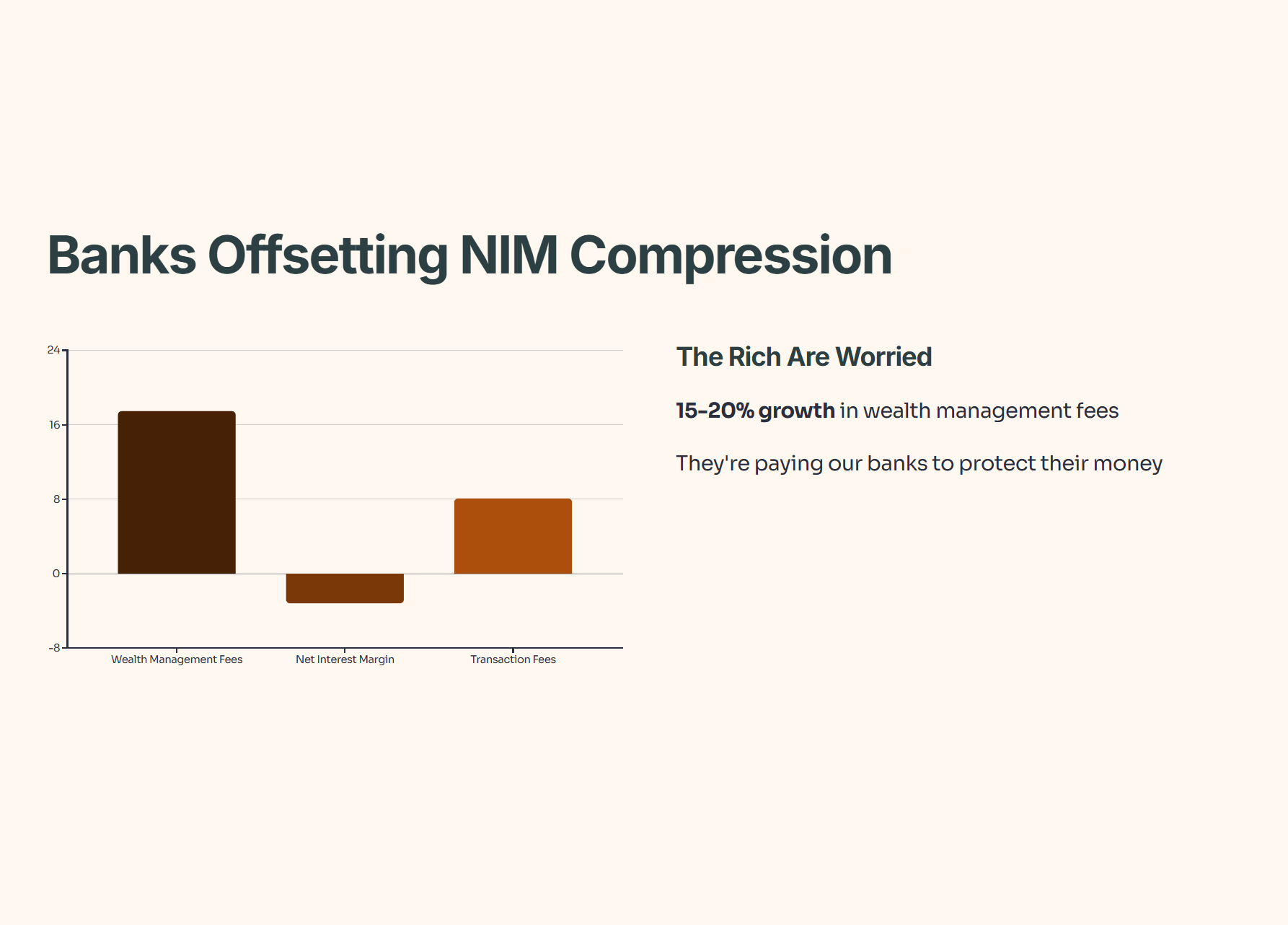

Contrast this with the banking sector. Our local trio (DBS, OCBC, UOB) are sitting on CET1 ratios above 15%. This is a fortress balance sheet. Even facing Net Interest Margin (NIM) compression, they are offsetting it with a 15–20% growth in wealth management fees. The rich are getting worried, and they are paying our banks to protect their money.

However, the most shocking statistic comes from the CPF Board. In a desperate bid to beat inflation, many Singaporeans took their money out of the guaranteed Ordinary Account (OA) to invest it themselves. The result? 43% of self-invested CPF accounts underperformed the risk-free 2.5% floor between 2020 and 2024. Let that sink in. Nearly half of the people who tried to be “smart” ended up poorer than if they had done absolutely nothing.

The Tale of Two Strategies:

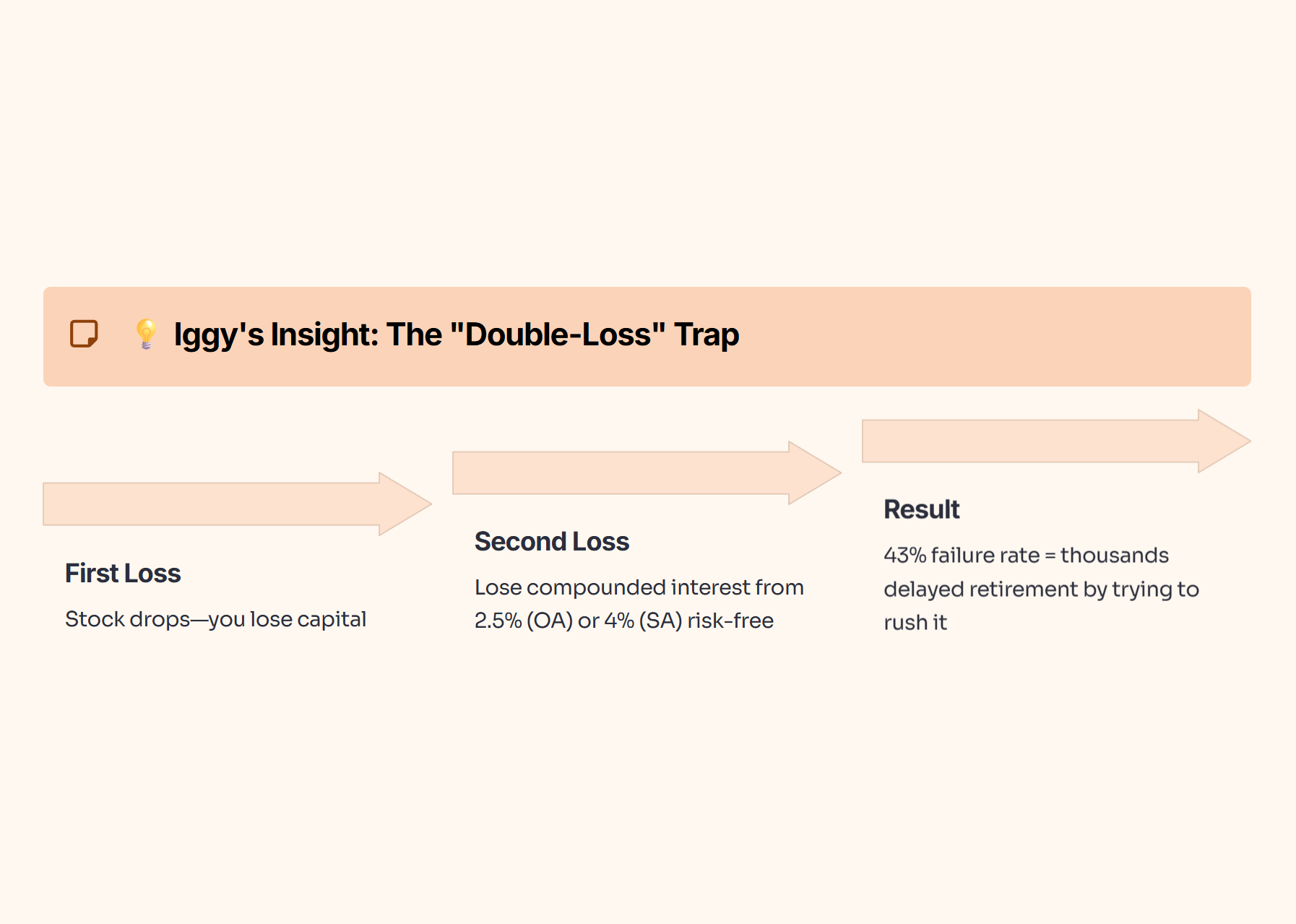

💡 Iggy’s Insight: The “Double-Loss” Trap

When you take money out of your CPF OA to buy a stock that drops, you suffer a double loss. First, you lose the capital. Second, you lose the compounded interest that the 2.5% (or 4% in SA) would have generated risk-free. That 43% failure rate isn’t just a statistic; it represents thousands of Singaporeans who delayed their retirement by trying to rush it.

4. The Action Plan: The 2026 “Bunker” Strategy

The data is screaming one message: Defense is the new Offense. With US debt threatening liquidity, tariffs threatening tech, and the Ringgit cutting off our cheap supply line, you need to hunker down.