April 14 MAS Policy Statement Today SGX Daily Pulse (April 14, 2026) |🦖EP1546

MAS speaking today so don't blur-blur. Your REIT dividends are at the mercy of the S$NEER path now.

Today’s MAS Monetary Policy Statement is live. Every yield play on the board is being repriced in real time.

The market is not waiting for the MAS to finish speaking. With Brent crude at US$111.43 on Hormuz supply disruption and the S$NEER path under active review today, the forensic question is not whether rates move — it is whether your portfolio was built to survive the answer either way.

In This Article:

Market Snapshot

The Audit Acrophyte Hospitality Trust

The Audit Koh Brothers Eco Engineering

The Audit Capital World

Analyst Chatter

Watchlist and Yield Spread

Iggys Take The Bottom Line

Iggys Forensic Compliance Standards Standard Disclaimer

MARKET SNAPSHOT

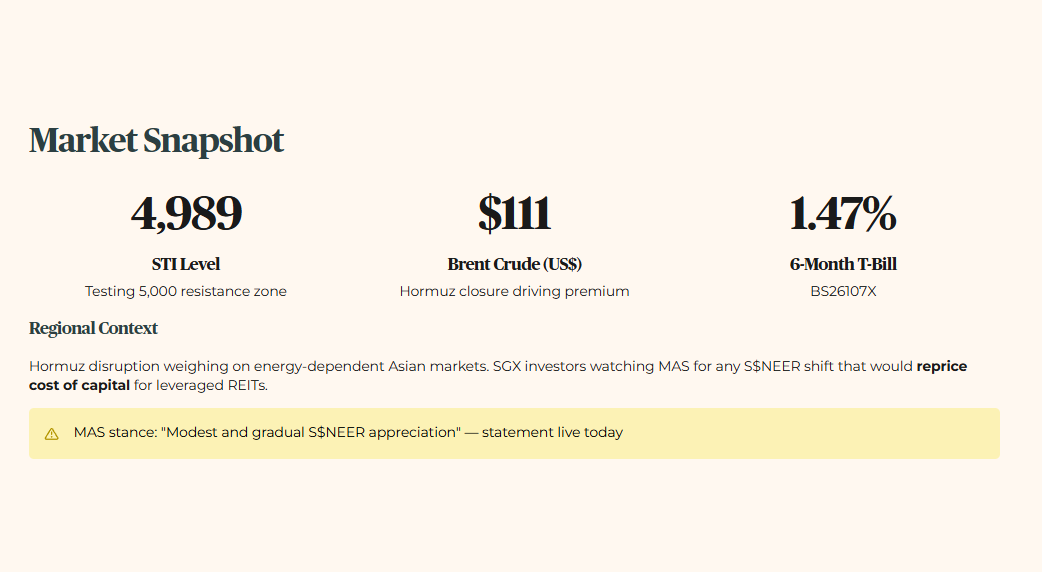

STI Level: 4,989.41 (Closed 10 April 2026 — testing 5,000 resistance zone ahead of today’s MAS statement)

Brent Crude: US$111.43 (Hormuz closure driving supply disruption premium)

6-Month T-Bill (BS26107X): 1.47%

MAS Stance: “Modest and gradual S$NEER appreciation” — policy statement releasing today, April 14

Regional Context: Hormuz supply disruption is weighing on energy-dependent markets across Asia. SGX investors are watching the MAS statement for any shift in the S$NEER appreciation path that would reprice the cost of capital for leveraged REITs.

THE AUDIT

1. Acrophyte Hospitality Trust (SGX: XZL)

The Debt Wall has not approached — it has arrived. Auditors are already waving the red flag.

Layer 1 — Raw Fact: Auditors have flagged a “material uncertainty” regarding Acrophyte’s ability to refinance a US$198.5 million loan due September 2026. The trust is not approaching a debt wall — it is standing at one.

Layer 2 — Benchmark: Gearing at 42.7% sits significantly above the 35% Iggy Forensic Ceiling. ICR at 1.62x against a 4x floor means the trust is generating S$1.62 of operating income for every S$1 of interest owed — a margin so thin that any revenue softness triggers a coverage failure. This is not a yellow flag. It is a red one.

Layer 3 — Peer Context: CDL Hospitality Trusts maintains a materially stronger ICR and higher absolute EBITDA. The gap between a hospitality REIT with institutional balance sheet discipline and one carrying a US$198.5 million refinancing cliff in five months is not a peer comparison — it is a forensic case study in what happens when gearing is allowed to drift above the ceiling.

Layer 4 — Forward Scenario: A 10% increase in financing costs at September refinancing would push ICR from an already fragile 1.62x toward technical default territory. There is no buffer. The Debt Wall refinancing shock is not a scenario — it is a scheduled event.

Layer 5 — Wallet Impact: A 65-year-old drawing CPF LIFE payouts holding these stapled securities faces potential total loss of distribution if the September refinancing fails. This is not a yield trap in the making — the trap has already closed. Forensic Verdict: Exit Watchlist.

🦎 Iggy’s Insight

Acrophyte is not a complicated forensic call — it is a textbook one. Three thresholds breached simultaneously: gearing above the ceiling, ICR below the floor, Net Debt/EBITDA deep in red flag territory. Any one of these would trigger a watchlist review.

All three together, with a US$198.5 million refinancing due in five months and auditors already using the phrase “material uncertainty,” means the forensic work is done. The yield may look attractive from the outside. That is precisely how yield traps work — they advertise the return and bury the refinancing risk in the footnotes. Your CPF LIFE payout does not have a recovery mechanism if the distribution is cut. The gearing ratio does.

2. Koh Brothers Eco Engineering (SGX: KBE)

The rejection of the Oiltek distribution signals a board prioritising group liquidity over immediate shareholder returns.

Layer 1 — Raw Fact: Koh Brothers rejected a shareholder resolution to distribute its 54.8% stake in Oiltek International. The board is holding the asset, not recycling it.

Layer 2 — Benchmark: The balance sheet is genuinely clean — net cash position of S$19.06M with total debt of S$52.71M covered by cash of S$71.77M. That is fortress territory on gearing. But a 0.26% dividend yield against a 4.7% minimum hurdle is not a near-miss. It is a structural failure on income by 4.44 percentage points. A clean balance sheet does not compensate for a yield that cannot fund a single kopitiam breakfast per thousand dollars invested.

Layer 3 — Peer Context: Asset-light operators like LHN are actively recycling capital to close the yield gap. KBE’s decision to retain the Oiltek stake suggests a different priority — group liquidity preservation over shareholder income. In a 2026 oil shock environment that is defensible as corporate strategy. It does not make KBE an income play.

Layer 4 — Forward Scenario: A 10% downturn in construction margins in a rising raw material cost environment would further compress group liquidity, making a special distribution even less likely. The Oiltek stake remains locked.

Layer 5 — Wallet Impact: For a 45-year-old HDB owner in Jurong looking for a special dividend windfall, this rejection confirms KBE as a Watchlist Trigger only — not a payout play. The balance sheet is worth monitoring. The yield is not worth waiting for. Forensic Verdict: Watchlist — Balance Sheet Only.

🦎 Iggy’s Insight

KBE presents a split forensic verdict that income investors need to read carefully. The balance sheet is one of the cleanest on the SGX mid-cap board — net cash, low leverage, no refinancing cliff. In a market where Acrophyte is sitting on a US$198.5 million debt wall, that kind of balance sheet discipline deserves acknowledgment. But acknowledgment is not a yield.

At 0.26%, KBE is missing the 4.7% minimum hurdle by 4.44 percentage points — a gap so wide that even a special Oiltek distribution would need to be substantial and immediate to shift the forensic verdict. The board has signalled it is not in a hurry. For a 45-year-old in Jurong building a retirement income portfolio, a clean balance sheet with no visible path to yield is a watchlist position, not a portfolio position.