Are Singapore's Banks Still the Dividend Kings? The Rise of Tech as the Next Dividend Powerhouse

Banks still pay 5%, but this guide shows how to rebalance into REITs, SGX-linked tech, and data-centre plays to lock in higher income today and faster dividend growth for the next decade.

Most Singapore investors still think banks are the only reliable dividend play in town. But while many chase 5% yields from DBS and OCBC, a quiet shift is underway. Tech-linked cash flows and digital infrastructure are maturing into steady, rising dividends that could outpace banks over the next decade.

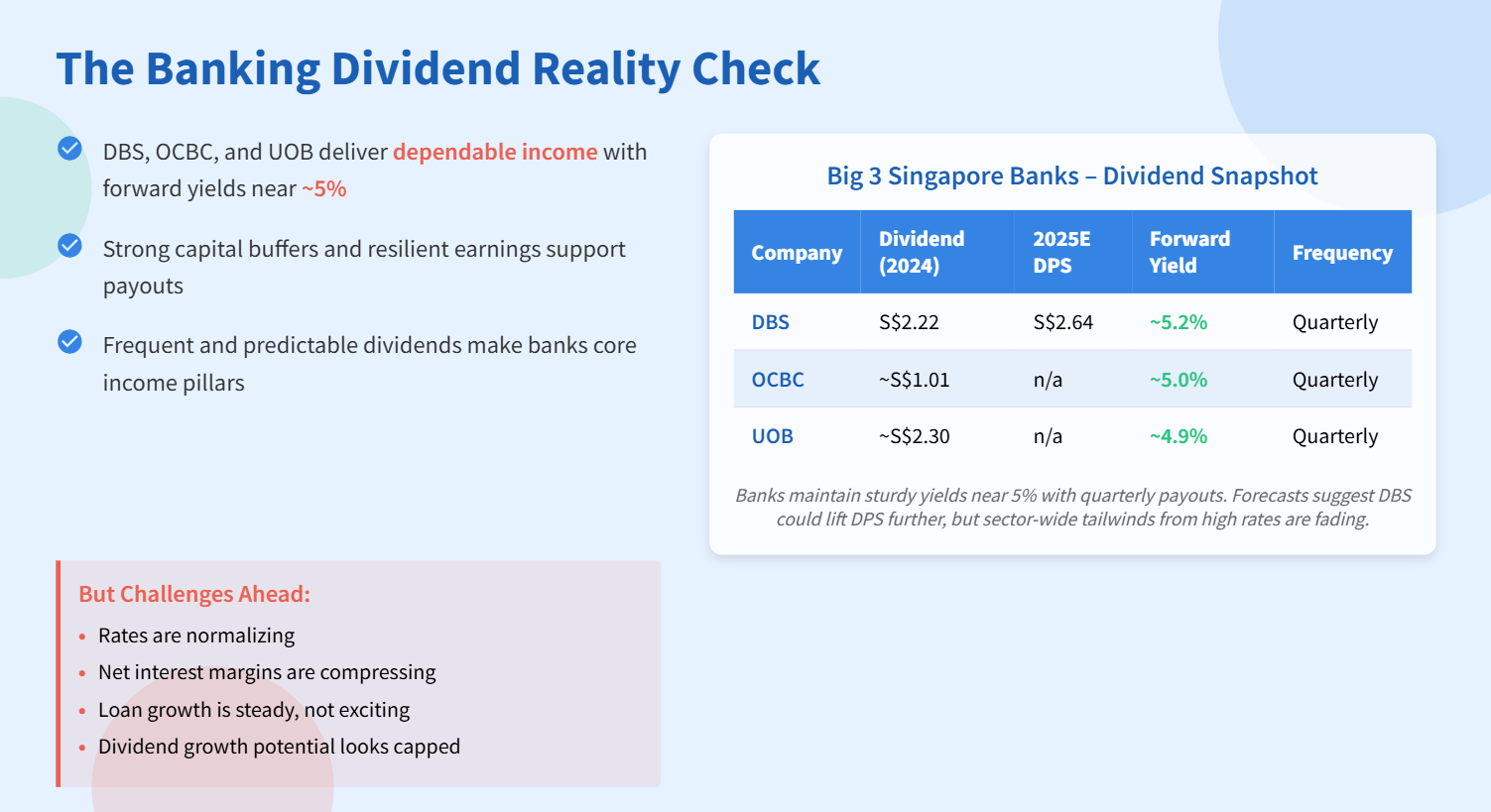

The Banking Dividend Reality Check

Let’s start with the anchors. DBS, OCBC, and UOB still deliver dependable income. Forward yields sit near 5%, backed by strong capital buffers and resilient earnings. Payouts are frequent and predictable, which is why banks remain a core income pillar for many CPF and SRS portfolios.

But we must weigh the next phase. Rates are normalising. Net interest margins are compressing. Loan growth is steady, not exciting. The dividend engine still runs, but the throttle is no longer wide open. For investors who want both income today and growth in the stream tomorrow, we need to broaden the frame.

Caption: DBS, OCBC, and UOB maintain sturdy yields near 5% with quarterly payouts. Forecasts suggest DBS could lift DPS further, but sector-wide tailwinds from high rates are fading. The case for banks remains solid, yet the upside in dividend growth looks capped near term.

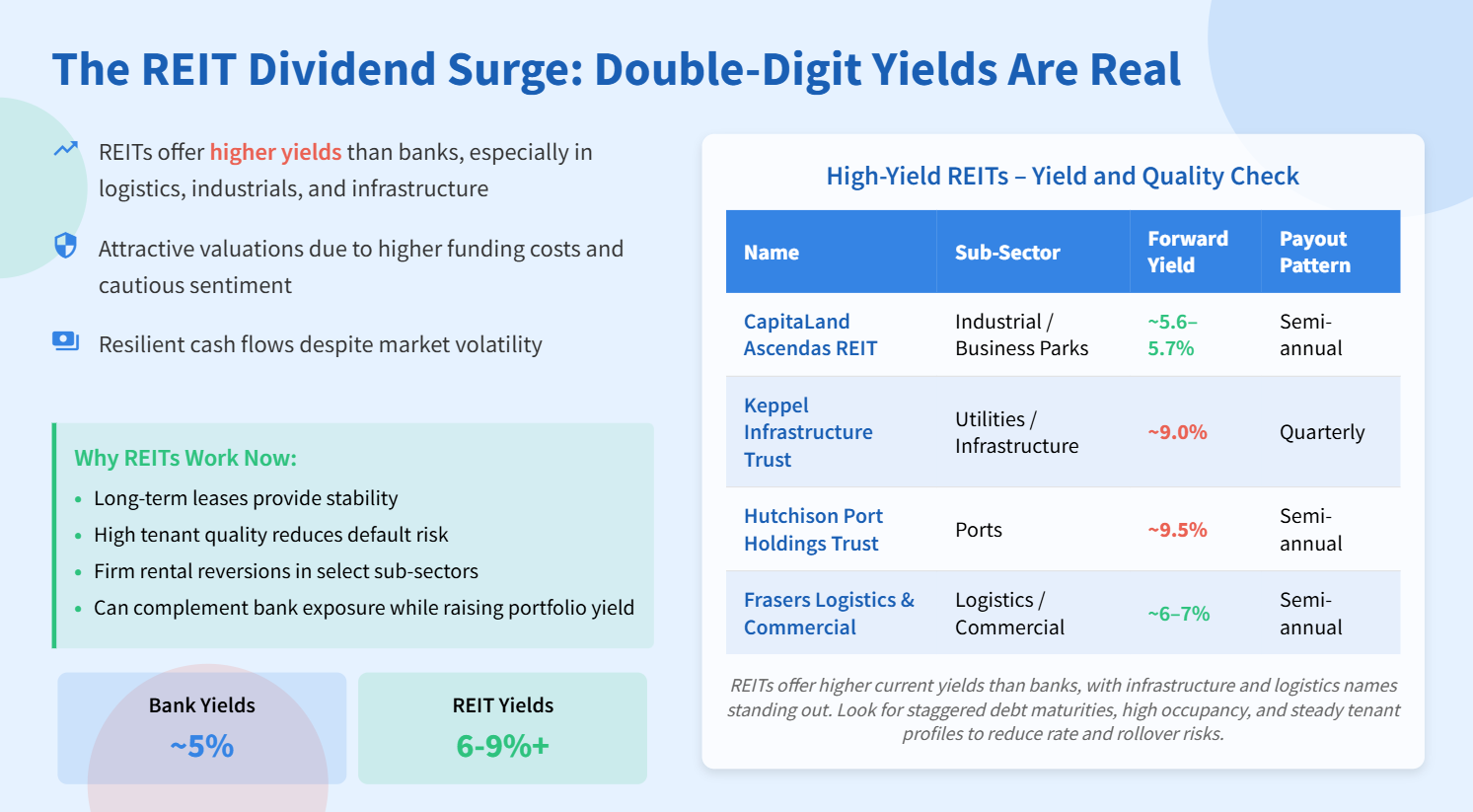

The REIT Dividend Surge: Double-Digit Yields Are Real

Income hunters now find higher yields in REITs, especially those tied to logistics, industrials, and infrastructure. Several names still trade at attractive yields due to higher funding costs and cautious sentiment. Yet cash flows remain resilient. Leases are long. Tenant quality is high. And rental reversions in select sub-sectors are firm.

Caption: REITs offer higher current yields than banks, with infrastructure and logistics names standing out. Look for staggered debt maturities, high occupancy, and steady tenant profiles to reduce rate and rollover risks. This basket can complement bank exposure while raising portfolio yield.

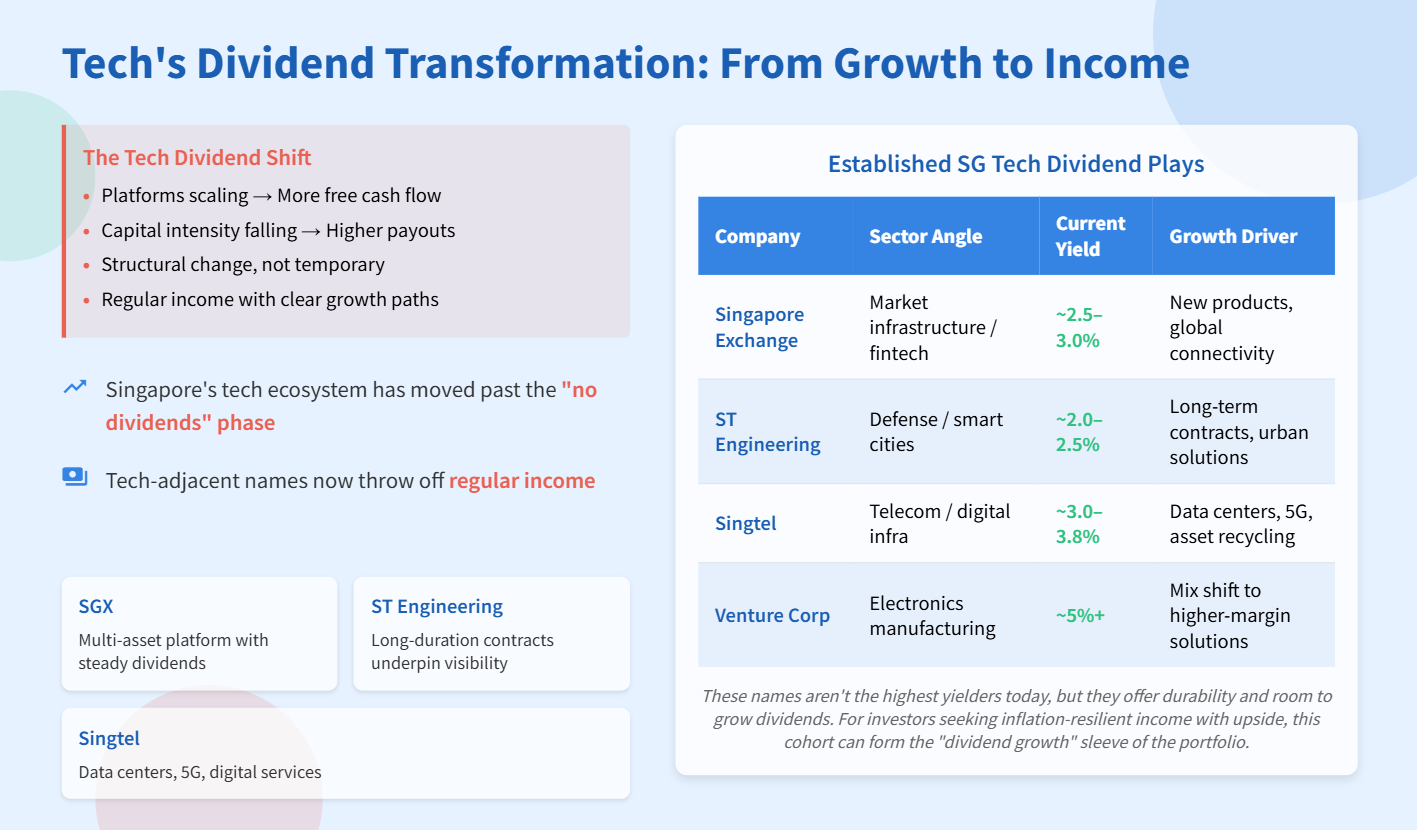

Tech’s Dividend Transformation: From Growth to Income

Singapore’s tech ecosystem has moved past the “no dividends” phase. Several tech-adjacent names now throw off regular income and have clear paths to grow payouts. The shift is structural, not temporary. As platforms scale and capital intensity falls, more free cash flow can reach shareholders.

SGX is evolving from local exchange to multi-asset platform. Fee growth and product breadth support steady dividends.

ST Engineering blends defense, aerospace, and smart-city solutions with long-duration contracts. That underpins visibility.

Singtel is leaning into data centers, 5G, and digital services, while recycling capital through asset monetisation and buybacks.

Caption: These names aren’t the highest yielders today, but they offer durability and room to grow dividends. For investors seeking inflation-resilient income with upside, this cohort can form the “dividend growth” sleeve of the portfolio.