Are Your SGX Dividends Still Safe This October? The Income Reality Check Every Singapore Investor Needs

What OCTOBER'S Rising Rates, Geopolitics, and Property Trends Mean for Your Payouts—SGX Dividend Dangers (and Safe Havens) Explained

Editor’s Note: This post has been updated on October 19, 2025, to provide deeper, more comprehensive analysis. The article now includes a full framework for our Malaysian audience, including the EPF retirement benchmark, M-REITs, and key KLCI dividend stocks, to parallel our original Singaporean analysis.

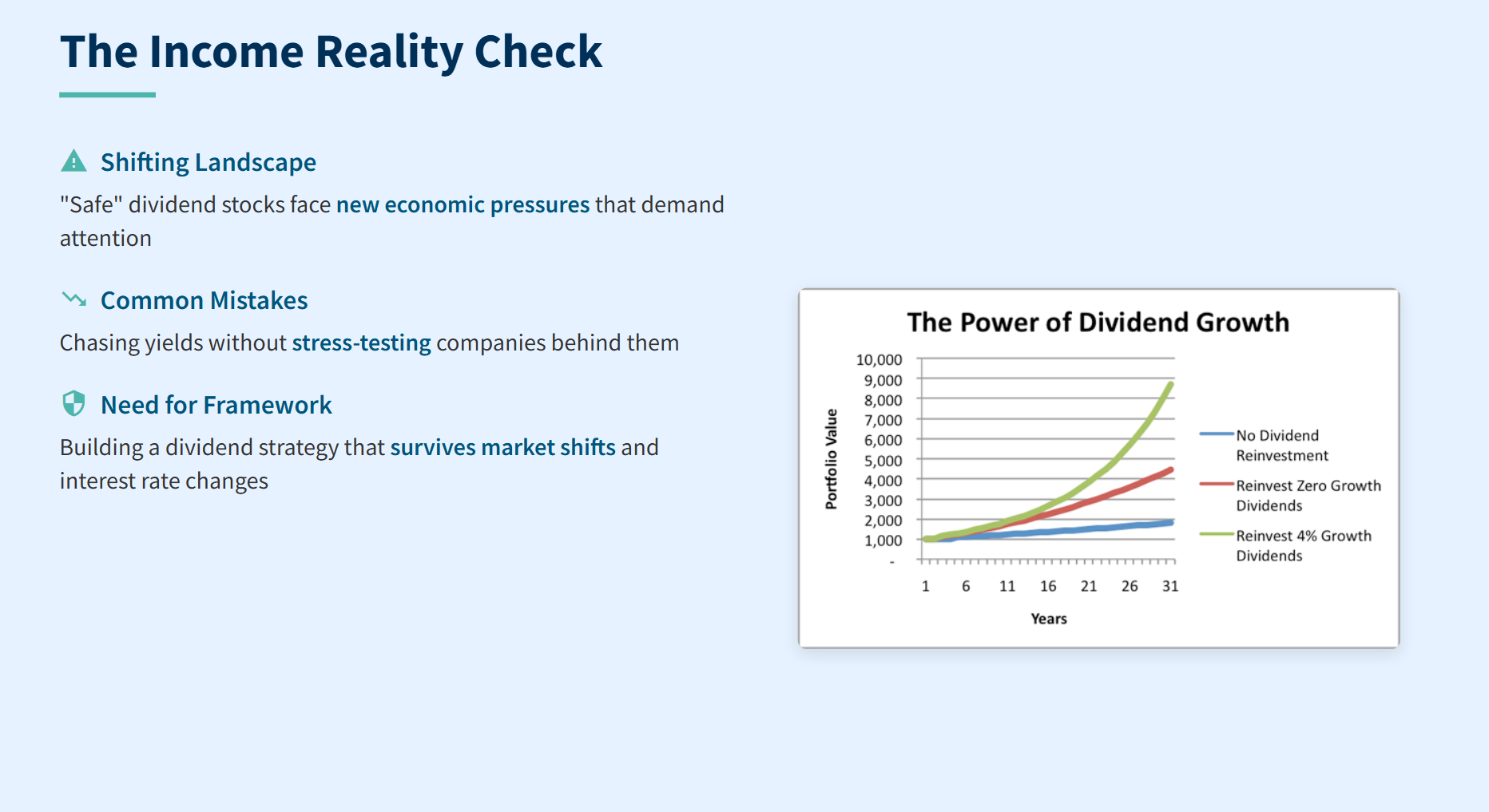

October’s dividend season brings a harsh truth: some of your “safe” income stocks aren’t as secure as they seem, and the new economic shifts demand a smarter safety framework.

Walking through Singapore’s financial district this month, you see the same confident faces rushing to work, portfolios loaded with dividend stocks that seemed bulletproof just months ago. But behind those steady payouts lies a shifting landscape that demands your attention.

The uncomfortable reality? Many Singapore investors are flying blind with their dividend strategies. They chase yields without stress-testing the companies behind them. They treat all CPF and SRS eligible stocks as equally safe. They assume past payouts guarantee future income.

This isn’t just about picking winners and losers. It’s about building a dividend strategy that survives market shifts, interest rate changes, and company-specific challenges. By the time you finish reading this, you’ll have a clear framework to separate the truly safe dividend plays from the yield traps lurking in your portfolio.

The Trade-off That’s Fooling SG & MY Investors

High yields look tempting on paper, but October’s fresh data reveals a crucial split in both the Singapore and Malaysian dividend landscapes. Companies offering the fattest yields often carry the biggest risks—and the market is starting to price this in.

In Singapore, take Uni-Asia Group, flashing a 3.7% yield that caught many income-focused investors. Dig deeper and you find a company bleeding cash with a negative operating margin of over 200%. This is a classic yield trap.

In Malaysia, you see a similar story with stocks like British American Tobacco (BAT). Its 8.7% yield looks incredible, but it’s supported by a dangerously high payout ratio (often over 80%) in a declining market. That dividend is not sustainable.

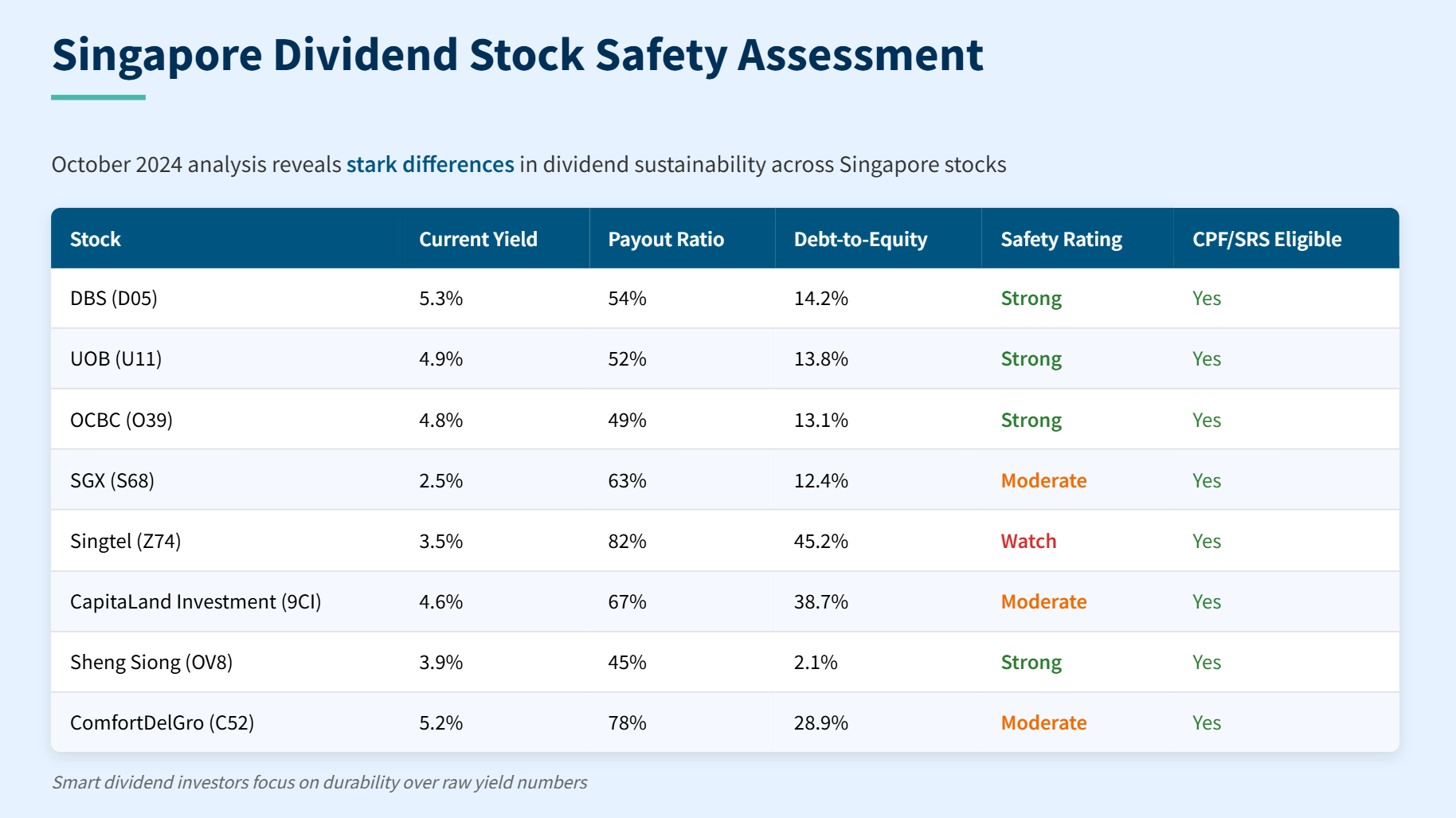

Singapore Dividend Stock Safety Assessment (October 2024)

The table shows the stark reality. Singapore’s big three banks deliver solid yields with sustainable payout ratios below 55%. Meanwhile, Singtel’s 82% payout ratio signals potential pressure if earnings dip. ComfortDelGro’s high payout ratio combined with moderate debt levels puts it in the “watch carefully” category.

Smart dividend investors focus on durability over raw yield numbers. The 5.3% from DBS backed by strong fundamentals beats a 7% yield from a struggling company that might slash payouts next quarter.

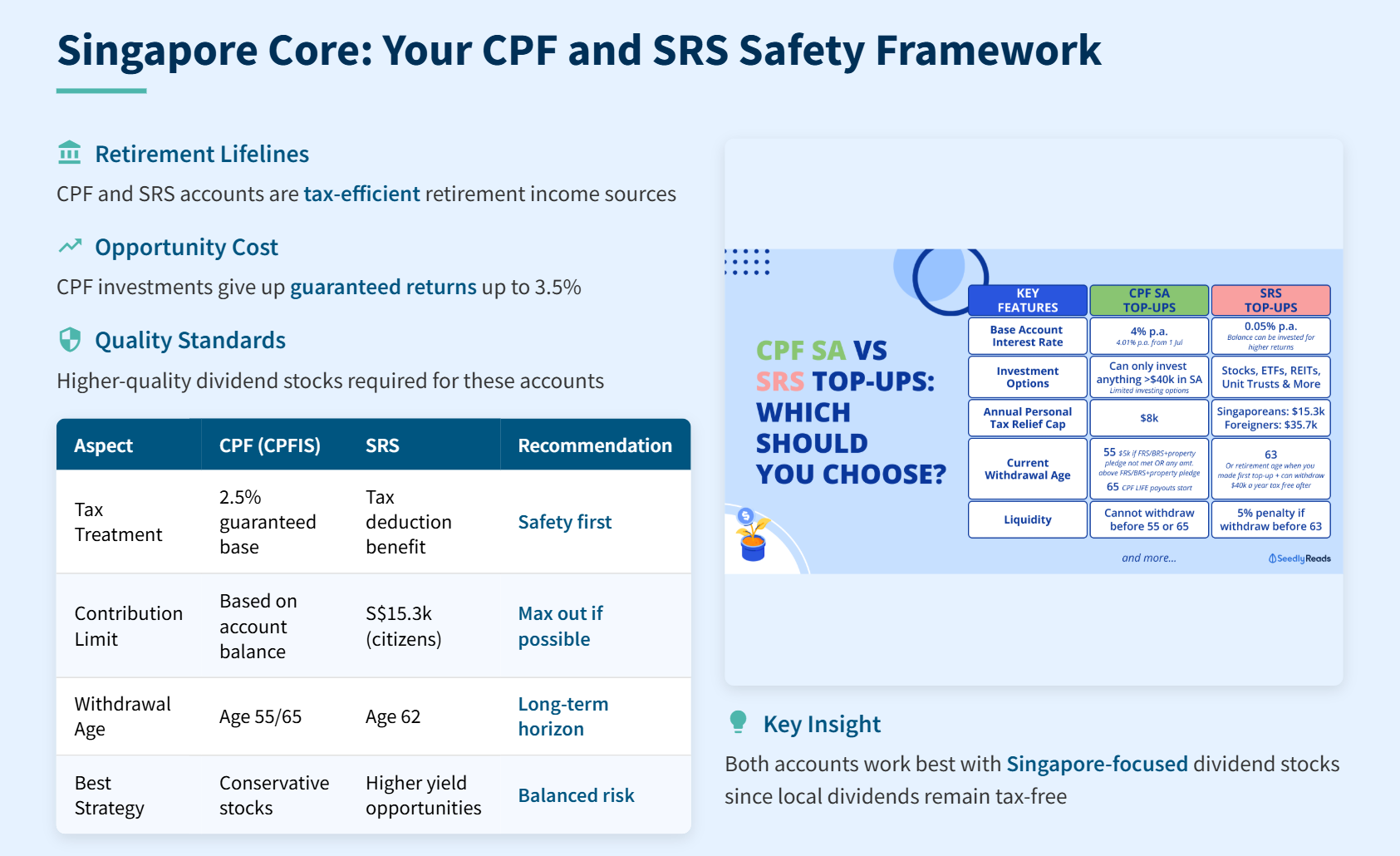

Your Retirement Core: A CPF, SRS & EPF Safety Framework

Your CPF and SRS accounts aren’t just tax-efficient—they’re your retirement income lifelines. This makes the safety assessment even more critical. Every stock in these accounts should pass stricter tests than your regular portfolio holdings.

The CPF Investment Scheme requires you to maintain at least S$20,000 in your Ordinary Account, and your first S$60,000 earns an extra 1% interest. This means you’re giving up guaranteed returns of up to 3.5% when you invest your CPF funds. The opportunity cost demands higher-quality dividend stocks.

SRS offers different advantages with tax deduction benefits and broader investment flexibility. Singapore citizens can contribute up to S$15,300 annually while foreigners can contribute S$35,700. The key insight: both accounts work best with Singapore-focused dividend stocks since local dividends remain tax-free.

CPF vs SRS Dividend Strategy Comparison

For CPF accounts, stick with the highest-quality dividend stocks: the big three banks, SGX, and maybe one or two defensive plays like Sheng Siong. For SRS, you can afford slightly more risk and higher yields, but maintain the same quality standards.

The framework here isn’t about maximizing yield—it’s about ensuring your retirement income streams remain intact when you need them most.

For our Malaysian readers, the benchmark is even higher. You’re not just giving up the 3.5% from CPF OA; you’re giving up the ~5.5% - 6.3% (based on recent 2023/2024 dividends) guaranteed annual dividend from your EPF (Employees Provident Fund).

This means any dividend stock you buy using EPF’s Members Investment Scheme (MIS) must clear a much higher hurdle. The opportunity cost is massive. You are risking guaranteed, high, compound returns for a variable one. Therefore, your EPF dividend stock-picking criteria must be even stricter.

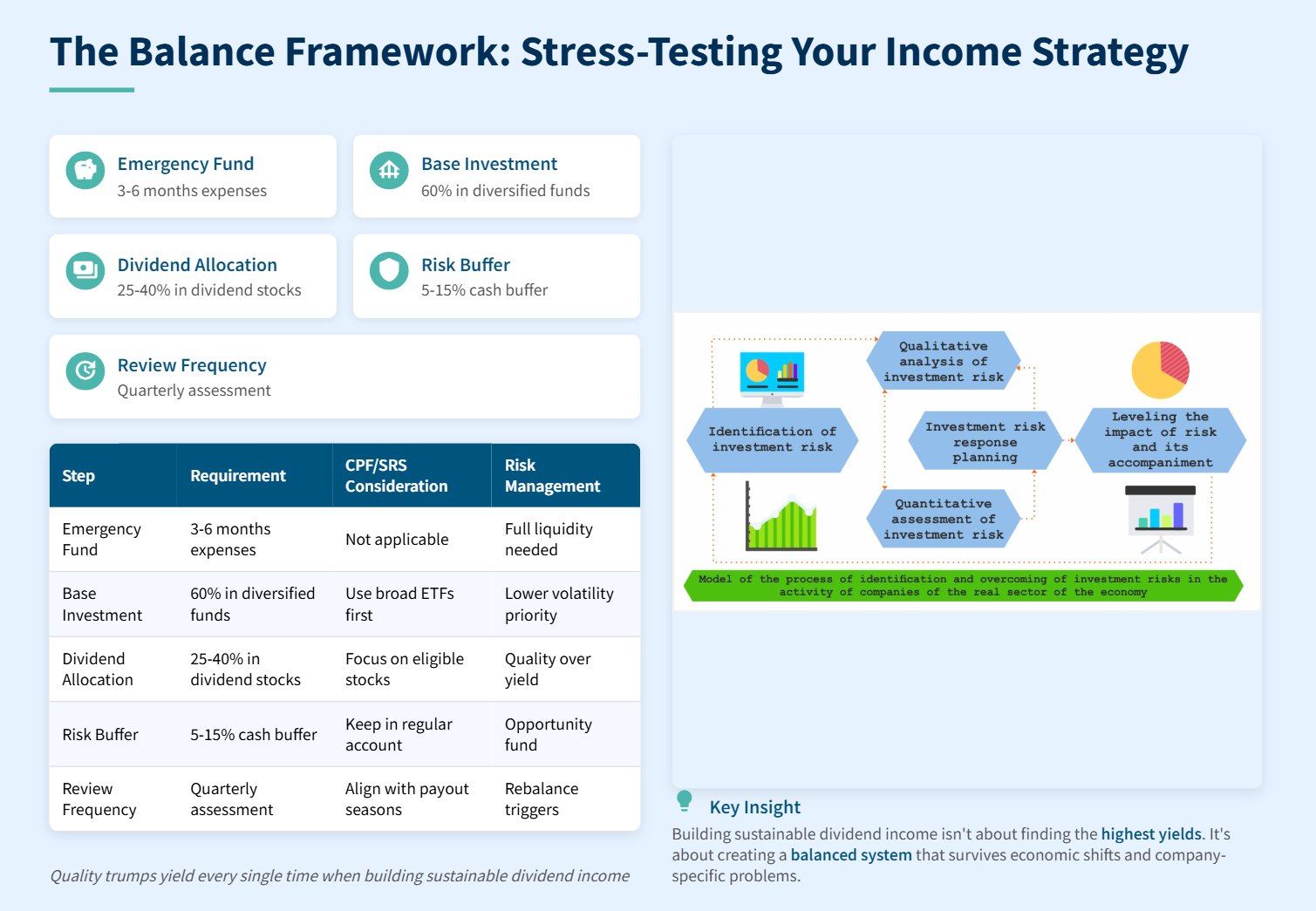

The Balance Framework: Stress-Testing Your Income Strategy

Building sustainable dividend income isn’t about finding the highest yields. It’s about creating a balanced system that survives economic shifts, company-specific problems, and your own psychological biases.

The framework starts with five essential steps that every Singapore dividend investor should implement:

Balance Framework Implementation Guide

Step one locks in your non-negotiables. Before chasing any dividend, ensure you have emergency funds and basic expenses covered. This removes the pressure to rely on dividend income for immediate needs.

Step two establishes your foundation with diversified, lower-volatility investments. Use broad market ETFs like the STI ETF for this base layer. Only after this foundation exists should you layer on dividend-focused investments.

Step three is where dividend stocks fit—as a focused allocation, not your entire strategy. Keep this between 25-40% of your total portfolio. Within this allocation, quality trumps yield every single time.

Step four maintains flexibility. Keep some cash ready for opportunities or unexpected needs. This prevents you from selling dividend stocks at bad times.

Step five keeps you disciplined. Review your dividend holdings every quarter, ideally aligning with Singapore’s dividend seasons. This catches problems early and prevents emotional decision-making.

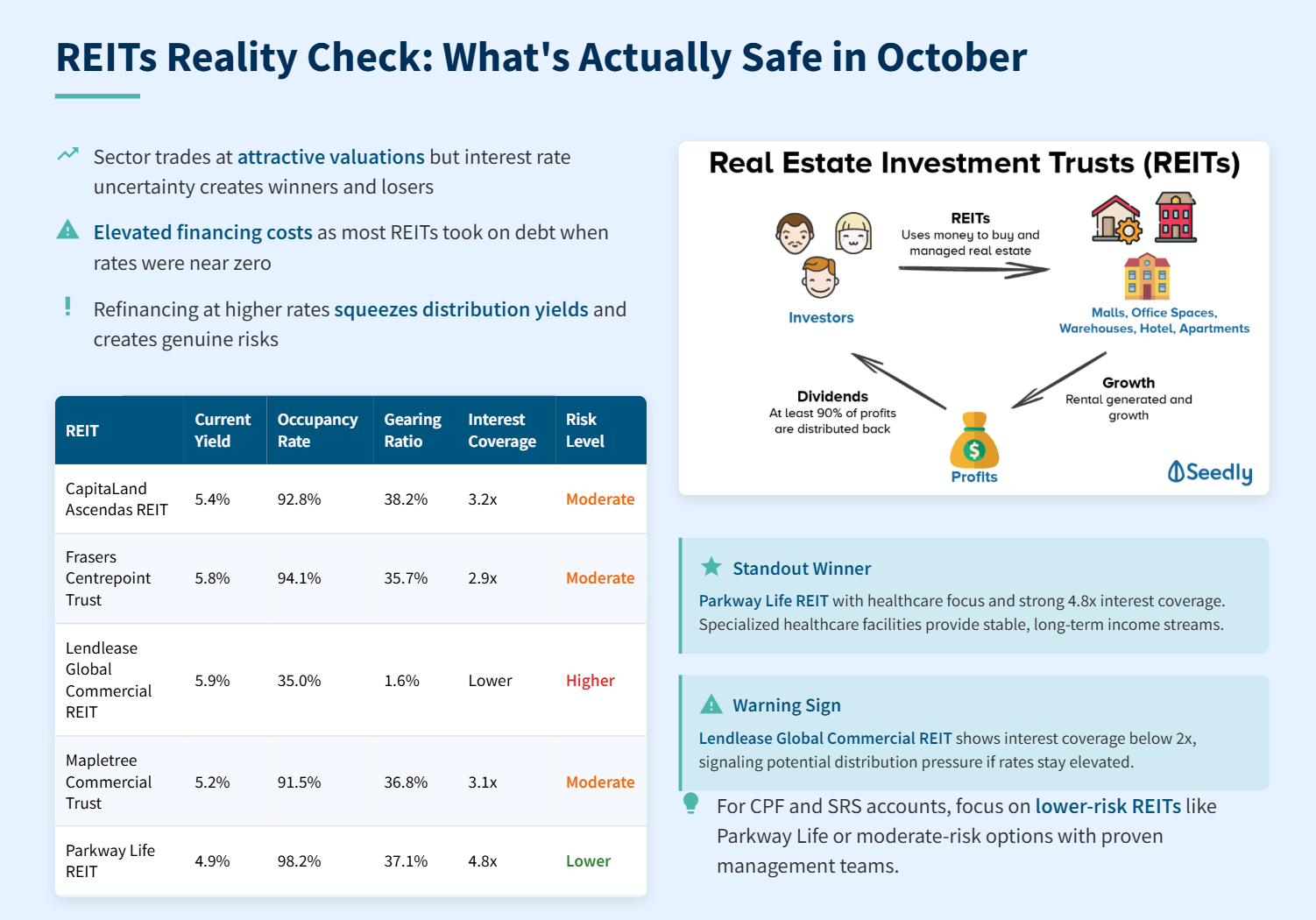

REITs Reality Check: What’s Actually Safe in October

Singapore REITs deserve special attention this dividend season. The sector trades at attractive valuations, but interest rate uncertainty creates winners and losers within the REIT universe.

The sector-wide challenge remains elevated financing costs. Most REITs took on debt when rates were near zero. Now they’re refinancing at much higher rates, squeezing distribution yields and creating genuine risks for some players.

Singapore REITs Dividend Outlook (October 2024)

The standout winner remains Parkway Life REIT with its healthcare focus and strong 4.8x interest coverage. The specialized healthcare facilities provide stable, long-term income streams that justify the lower 4.9% yield.

Lendlease Global Commercial REIT shows warning signs with interest coverage below 2x. Despite the attractive 5.9% yield, the weak coverage ratio signals potential distribution pressure if rates stay elevated.

The moderate-risk REITs like CapitaLand Ascendas and Frasers Centrepoint offer reasonable yields with manageable fundamentals. Their 5.4-5.8% yields come with occupancy rates above 92% and interest coverage around 3x—adequate but requiring monitoring.

For CPF and SRS accounts, focus on the lower-risk REITs like Parkway Life or stick with the moderate-risk options that have proven management teams and Singapore-focused assets.

For our Malaysian readers on Bursa, the challenge is different. While S-REITs are primarily battling high financing costs, M-REITs face a structural headwind: a persistent oversupply of office and retail space, especially in the Klang Valley.

This creates a sharp “flight to quality.” Prime, high-footfall assets like IGB REIT’s Mid Valley & The Gardens Malls or Sunway REIT’s Sunway Pyramid remain highly resilient with occupancies near 100%. However, smaller REITs with older, non-green-certified “B-grade” office towers are facing high vacancy and serious rental pressure. For M-REITs, the key risk isn’t just interest rates—it’s asset obsolescence.

🦎 Iggy’s Take: Stop Fixating on Rates, Start Auditing Management

Everyone is obsessed with what the Fed will do next. That’s a rookie mistake. In this environment, I’m watching management quality like a hawk.

Rising rates are a headwind for all REITs, but it’s bad management that will sink the ship. I want to see managers who are proactively divesting weaker assets before they’re forced to, who have already hedged their debt, and who have a track record of growing DPU through smart acquisitions, not just financial engineering. The gap between A-grade and C-grade management is about to become painfully obvious. Make sure you’re not holding a C-grade portfolio.

Practical Dividend Tactics: Your October Action Plan

Building a safe dividend portfolio requires specific tactics, not just theory. Here’s your step-by-step approach to implementing the safety framework this dividend season.