No Forensic Floor = No Safety in SGX Tech Momentum | 🦖EP1594

Your retirement drawdown depends on yield floors, not 135x P/E price charts

The current SGX tech rally is a valuation hallucination where share prices are sprinting miles ahead of actual earnings. If you are buying into these price spikes now, you are not investing in growth — you are providing exit liquidity for institutional players who have already done the math.

Most financial content is built around excitement — what is surging, what is breaking out, what you might be missing. I am deliberately building something different. Retirement-grade investing is not exciting. It is disciplined, forensic, and it is designed to still be working when you need it most.

You will walk away from this audit knowing exactly which counters are overbought traps and why only one name currently qualifies as a forensic sanctuary for your SRS capital.

In This Article:

The Dangerous Lure Of Momentum

The Illusion Of The Tech Boom

Scenario Table SGX Tech Stress Test

Decoding The Debt Burden Yield Trap Alert

The Wealth Check Yield and Cash Flow

The Price Check Peer Comparison

Iggys Classification V27

Iggys Forensic Disclaimer

The Dangerous Lure Of Momentum

We see the green candles on the screen and the heart starts to race. In May 2026, retail investors are flocking to local tech stocks, driven by the fear that the “AI train” is leaving the station without them. But momentum is a fickle friend. When headlines scream about record-breaking daily gains, they rarely mention that the underlying profitability has remained stagnant for quarters.

Contrast the visual appeal of a rising chart against the reality of a quarterly filing. In the heartland, we call this the “Wet Market Lobang” effect. Just because everyone is crowding around a stall does not mean the fish is fresh. It just means the noise is loud. The uncle selling the loudest is not always selling the best sotong.

For a 55-year-old investor in Bedok managing an SRS portfolio, chasing a stock that has already run 500% in a year is not a strategy. It is a gamble with your retirement peace of mind. And unlike a bad plate of char kway teow, the consequences do not pass by morning.

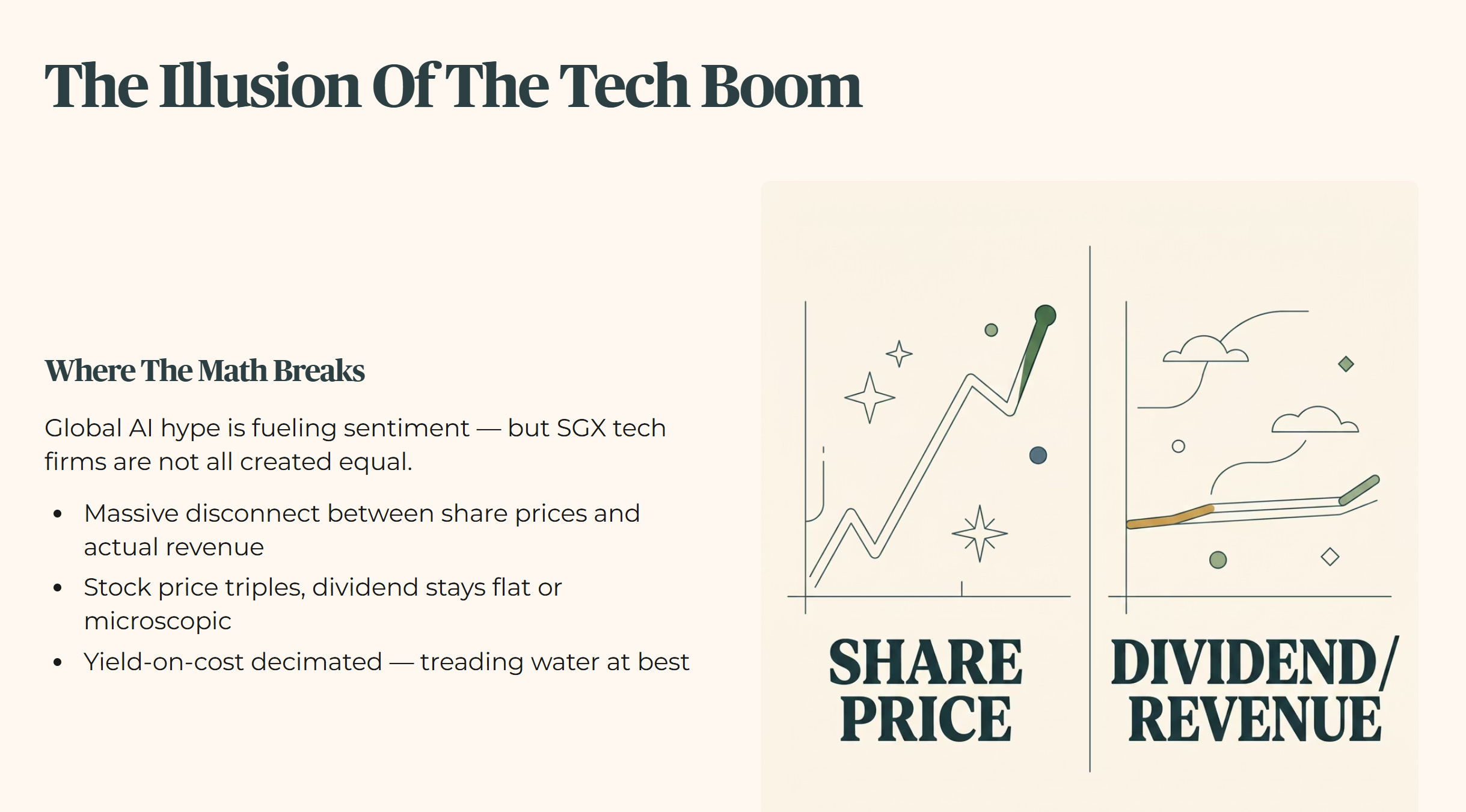

The Illusion Of The Tech Boom

Current market sentiment is being fueled by global AI hype, but Singaporean tech firms are not all created equal. There is a massive disconnect between soaring share prices and the actual revenue these companies generate. While the price moves might look like a Silicon Valley success story, the structural cracks in the balance sheets tell a different tale.

This is where the dividend math breaks. When a stock price triples but the dividend remains flat or microscopic, your yield-on-cost is being decimated. You are not compounding — you are treading water at best, drowning at worst.

We are seeing mid-cap firms with price-to-earnings multiples that make no sense for companies with stagnant revenue growth. It is a “HDB Lift Upgrade” situation: the exterior looks shiny and new, but the mechanicals inside are under immense strain from the high-interest-rate environment. Retail investors see the gleaming new facade and assume the whole building has been renovated. It has not. The pipes are still the same pipes.

The other thing the excitement glosses over is sector cyclicality. Semiconductor and precision engineering names live and die by inventory cycles. When the global chip glut returns — and it always returns — the firms that burned cash chasing capacity expansion are the ones that cut dividends and come back to the market with rights issues at discounts that punish every long-term holder who stayed loyal through the hype.

Scenario Table: SGX Tech Stress-Test

Decoding The Debt Burden — YIELD TRAP ALERT

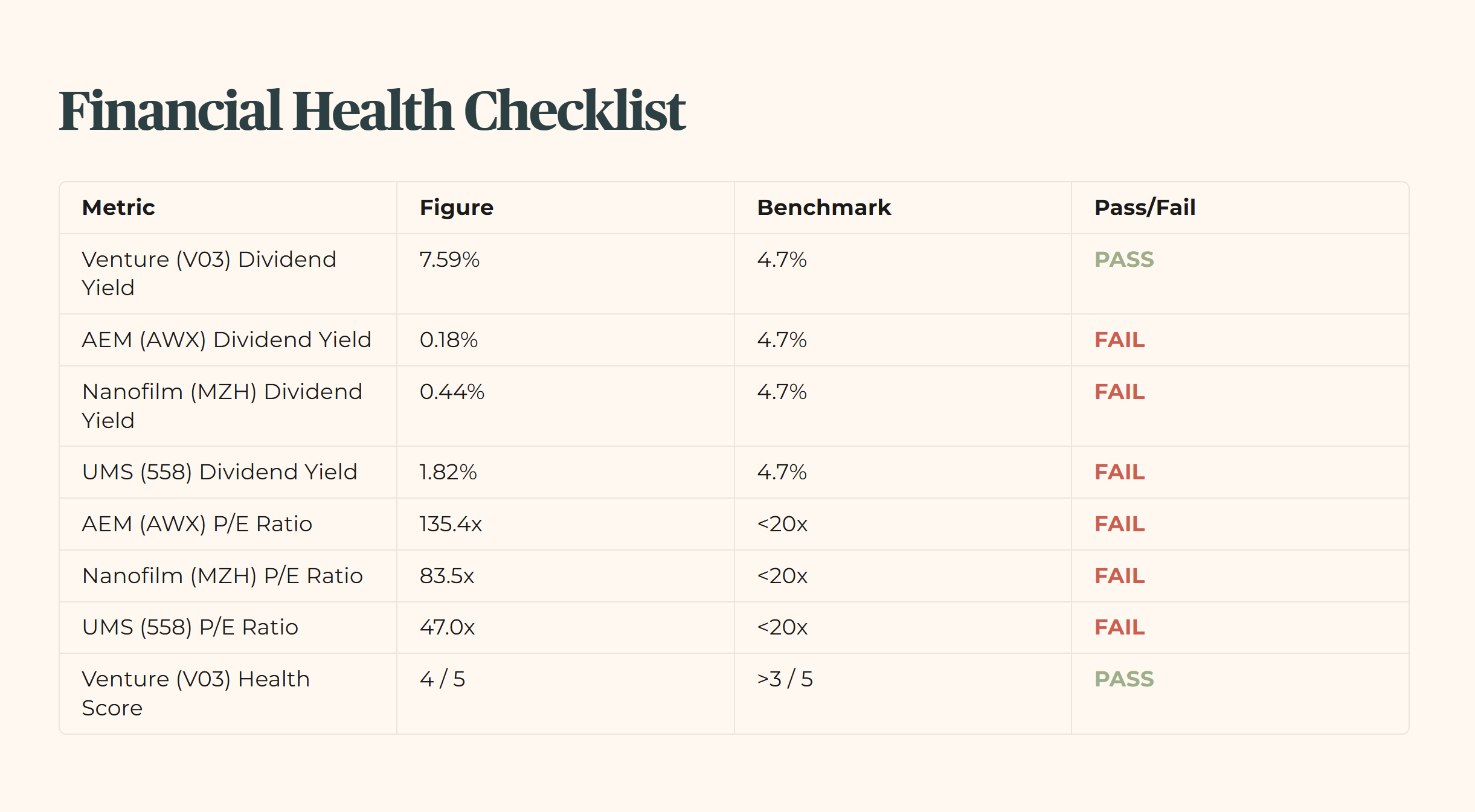

Before we look at the hype, we must look at the health. Most of the current “tech darlings” on the SGX fail the 4.7% minimum yield hurdle decisively — and not by a small margin. We are talking about yields so low that CPF Ordinary Account money sitting at 2.5% is actually doing more work with less risk.

The forensic verdict is not complicated: when you strip away the price momentum and look at what these companies are actually returning to shareholders, the numbers are damning.

Financial Health Checklist: SGX Tech Performance

Iggy’s Forensic Zone System

Every stock I cover receives a forensic zone rating based on yield, gearing, interest coverage, and structural red flags. Here is how I rate every stock:

Zone 1 Fortress: Yield ≥5.5%, gearing <30%, ICR >5x, zero soft flags. Sanctuary capital.

Zone 2 Watchlist: Yield 4.7–5.5%, gearing 30–34%, ICR 4–5x, maximum one soft flag.

Zone 3 Conditional: Yield ≥4.7%, two or more soft flags present.

Zone 4 Caution: Yield <4.7% OR any single hard gate failure.

Zone 5 Red Zone: Yield <3.2% OR structural red flag present.

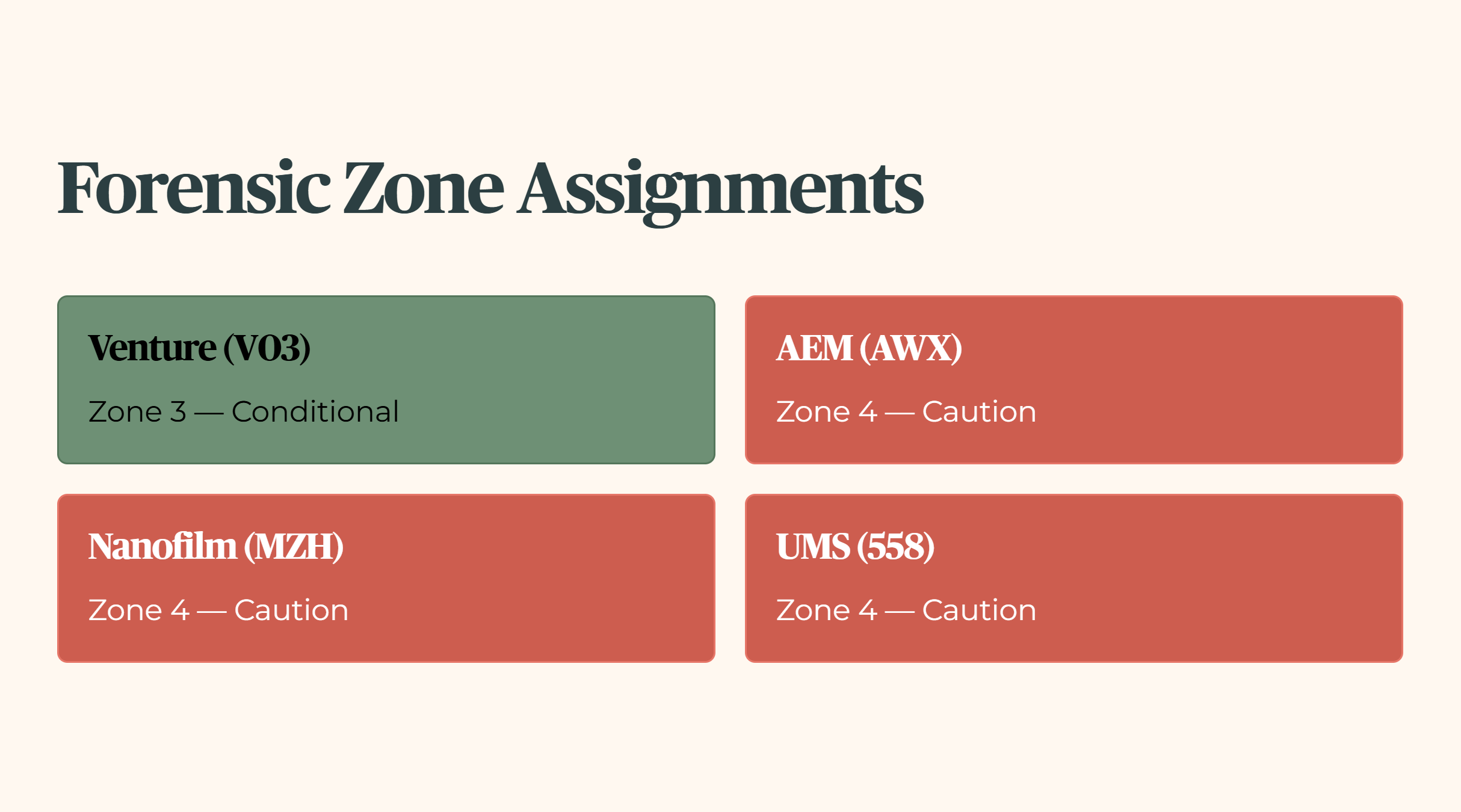

Iggy’s Forensic Zone Assignments (Free-Tier):

Venture (V03): Zone 3 — Conditional

AEM (AWX): Zone 4 — Caution

Nanofilm (MZH): Zone 4 — Caution

UMS (558): Zone 4 — Caution

🦎 Iggy’s Insight

Look at the P/E ratio for AEM Holdings at 135.4x. You are essentially paying for 135 years of current earnings just to own the stock today. In the heartland, if an uncle asked you to invest in his bak chor mee stall but said you would only see a profit in the next century, you would walk away before he finished the sentence. Why do we treat the stock market differently? High multiples without explosive revenue growth are not ambition — they are debt-fueled hope wearing an expensive shirt. Do not let a green chart blind you to the fact that you are buying a very expensive piece of air.

The Wealth Check: Yield and Cash Flow

Asset Yield (%) minus Risk-Free Rate (1.40%) equals Risk Premium. That is the arithmetic. Now apply it to what we are actually looking at.

The 4.7% yield hurdle and 3.2% stress-test floor above are just the setup — the next section applies them counter by counter to show exactly where Venture, AEM, Nanofilm, and UMS clear or fail the sanctuary test.