SG Bankruptcies Hit 5-Year High: The Silent Risk to REITs & Banks 🦖 EP1285

The numbers look grim, but the 2016 legal overhaul turned a life sentence into a strategic reset. Here is the data behind the debt.

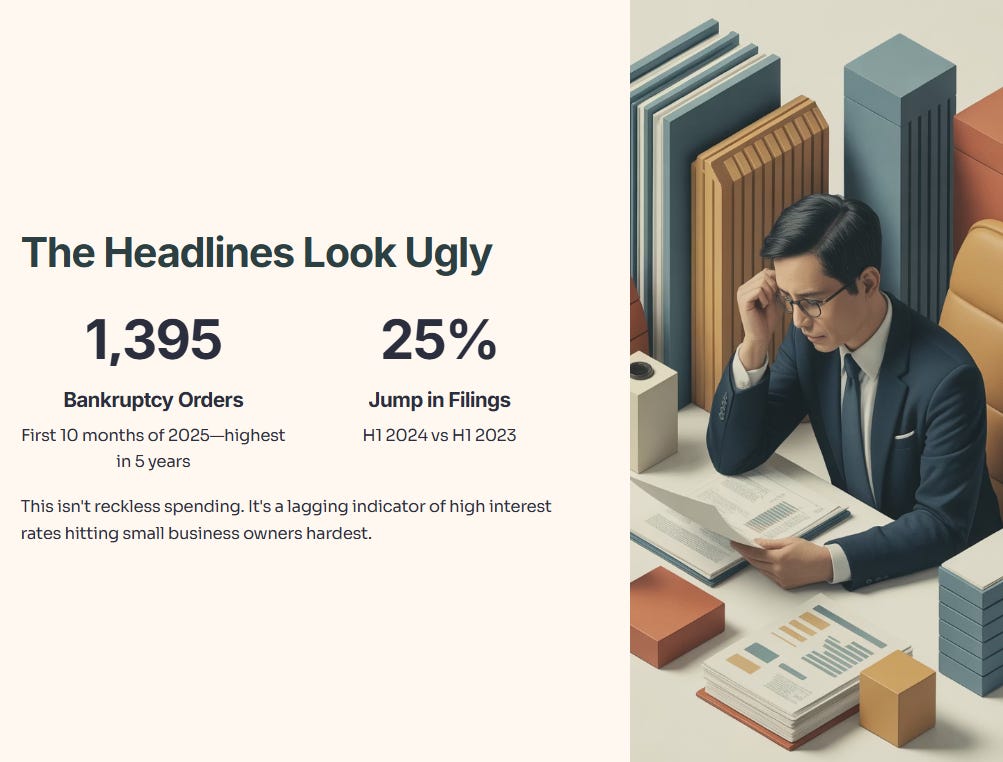

If you are watching the headlines, the picture looks ugly.

Bankruptcy orders in Singapore have climbed to levels we haven’t seen in five years. Recent data from the Ministry of Law reveals 1,395 bankruptcy orders in the first 10 months of 2025 alone.

For the “Premium Lurkers” reading this—the professionals and pre-retirees who pride themselves on prudence—this data might seem like a distant problem. But look closer. This isn’t just about reckless spending. It is a lagging indicator of the high-interest rate environment we have lived through, and it signals a specific stress point in the Singaporean economy: the small business owner.

Here is what the numbers actually mean, how the system has changed to offer a “strategic reset,” and my take on what this signals for our market.

In This Article:

• The Numbers Tell a Story We Can’t Ignore

• What’s Pushing Singaporeans to the Edge?

• The Bankruptcy Framework That Changed Everything

• The Five Exit Routes

• Rebuilding: The “Credit Jail” is Temporary

• The Bottom Line

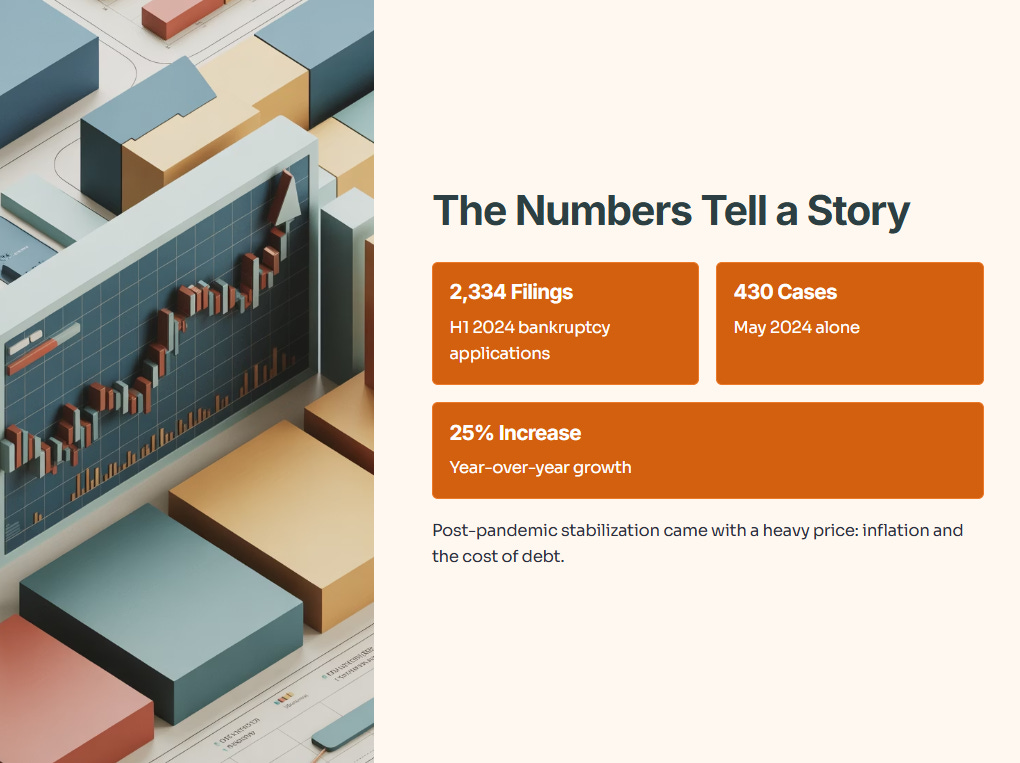

The Numbers Tell a Story We Can’t Ignore

In the first half of 2024, 2,334 individuals filed for bankruptcy—a 25% jump compared to the same period in 2023. May 2024 alone recorded 430 cases.

The sheer volume of applications suggests that the post-pandemic economic stabilization has come with a heavy price tag: inflation and the cost of debt.

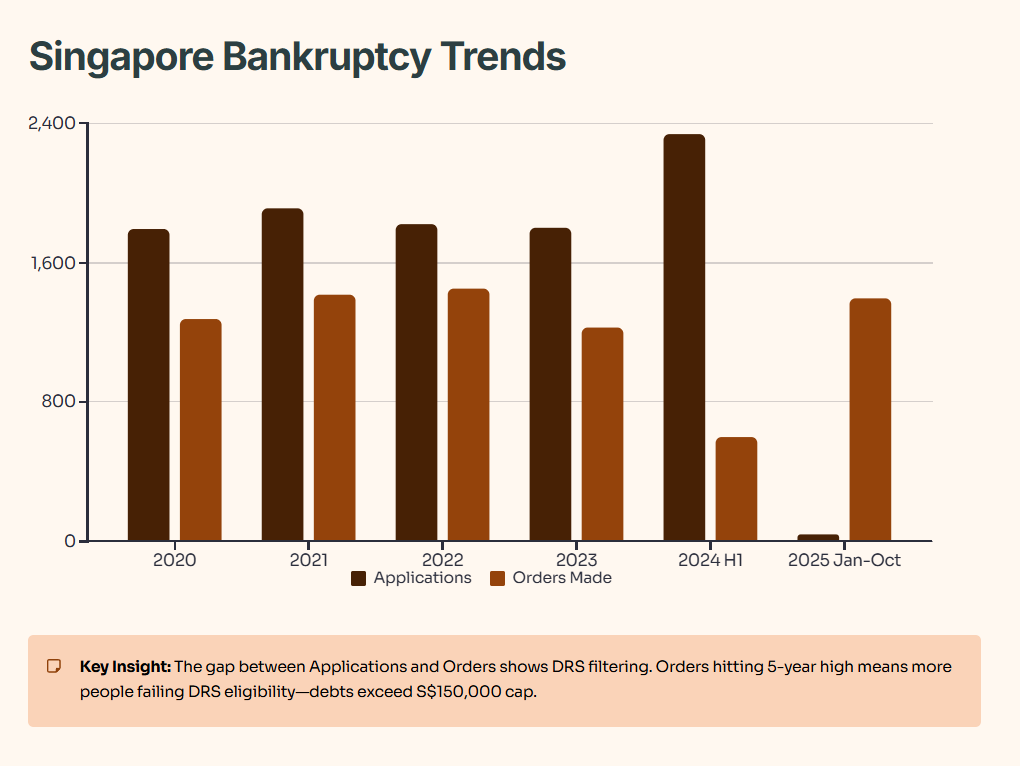

Table 1: Singapore Bankruptcy Trends (2020-2025)

Iggy’s Insight:

Do not just glaze over the “Orders Made” versus “Applications” column. The gap between them often represents the Debt Repayment Scheme (DRS) filtering people out before they hit full bankruptcy. The fact that Orders are hitting a 5-year high suggests that more people are failing the DRS eligibility—likely because their debts exceed the S$150,000 unsecured cap. This implies the average distress ticket size is growing.

What’s Pushing Singaporeans to the Edge?

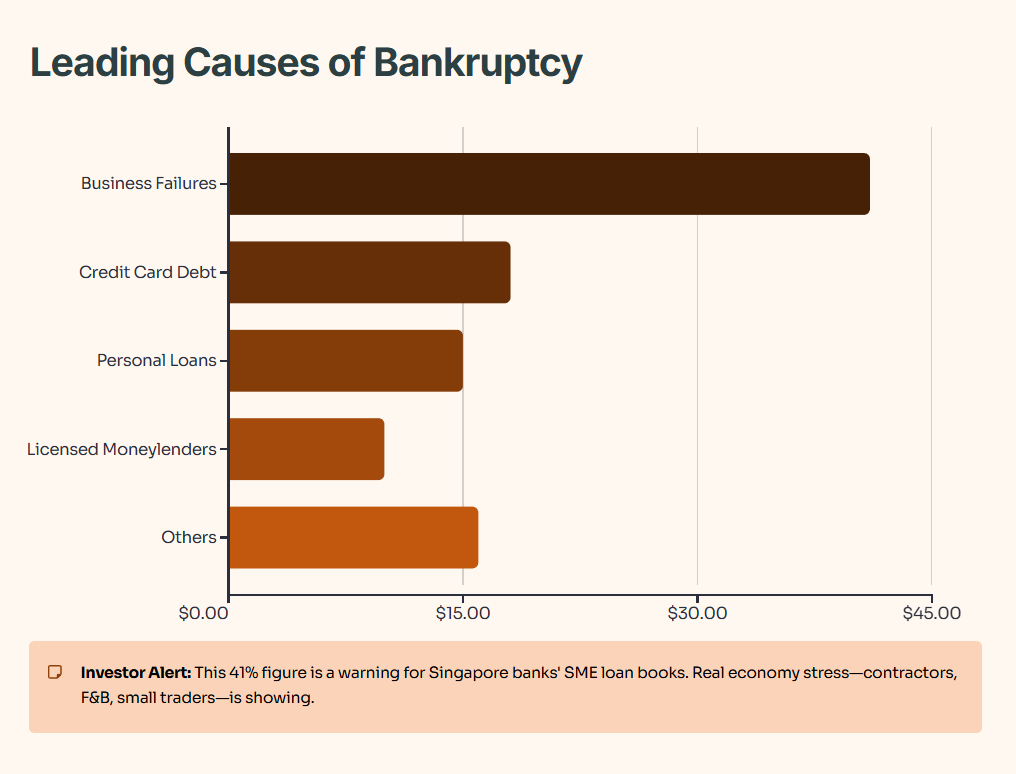

The narrative that bankruptcies are caused by young people buying luxury bags on credit cards is statistically lazy. The data paints a different picture.

Slightly over 40% of bankruptcy orders in H1 2024 were due to business failures.

This is the “Counter-Intuitive Angle.” The stress isn’t primarily consumer consumption; it is entrepreneurial capitulation. High capital costs, supply chain disruptions, and labor shortages have squeezed margins until they broke.

Table 2: Leading Causes of Bankruptcy (2024 Data)

Iggy’s Insight:

For the investors in the room, this 41% figure is a flashing amber light for Singapore banks’ SME loan books. While our local banks are well-capitalized, this metric tells me the “real economy” on the ground—the contractors, the F&B owners, the small traders—is hurting. If you are holding extensive exposure to commercial REITs with non-blue-chip tenants, check your occupancy risks.

The Bankruptcy Framework That Changed Everything

If you went bankrupt before 2016, you were essentially in a financial prison with an indefinite sentence. Some individuals remained bankrupt for 20 to 30 years.

The Bankruptcy Amendment Bill (2015) changed this completely. It introduced a “rehabilitative regime.” Now, discharge is based on a Target Contribution—a fixed sum you must pay, determined by your earning potential.

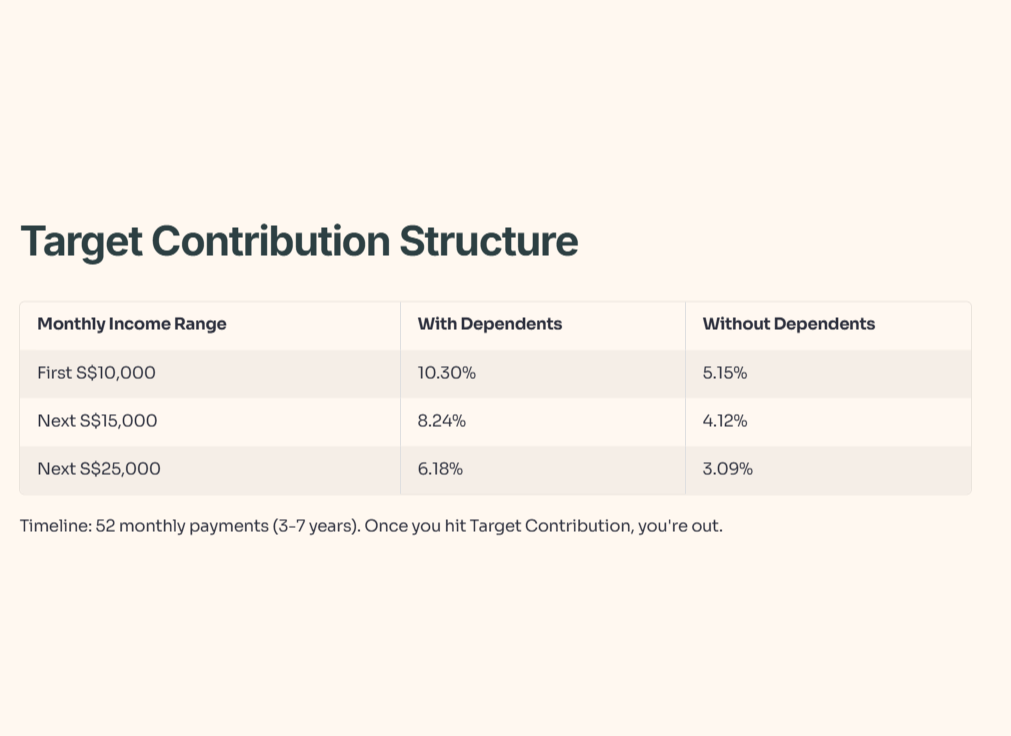

Table 3: Target Contribution Payment Structure

Once you hit that Target Contribution (usually over 3 to 7 years), you are out.

The Five Exit Routes

The modern framework offers certainty. It transforms bankruptcy from a “black hole” into a calculated financial tunnel.