Before I Move a Single CPF Dollar, I Check These Three Things

Most Singaporeans turning 55 this year will leave S$47,000 in compounding returns on the table by making one avoidable CPF decision.

Before I Move a Single CPF Dollar, I Check These Three Things

Most Singaporeans turning 55 this year will leave S$47,000 in compounding returns on the table by making one avoidable CPF decision.

The CPF Ordinary Account (OA) pays a guaranteed 2.5%. The SGX-listed stock you are eyeing might offer a 4.8% dividend yield, making the 2.3% “spread” look like an easy win for your retirement income. But there is an uncomfortable number your broker is not showing you. If that company’s interest coverage ratio (the number of times a company’s earnings can cover its interest payments) is below 4x, you aren’t just investing for yield. You are effectively subsidising their corporate debt with your retirement sanctuary. Here is exactly how to audit your move before you touch a single dollar of your OA capital.

Before we get into the numbers, I want to say who I am doing this for. Not the trader with a twenty-year runway. Not the growth chaser hunting the next ten-bagger. I am doing this for the retiring and retired Singaporean who needs their capital to work reliably — not spectacularly.

In This Article:

Stage 1 — The Compounding Window Age 30–54

Stage 2 — The Pivot Point Age 55–64

Stage 3 — The Drawdown Architecture Age 65+

Stage 4 — The Legacy Layer Estate Planning

The Policy Change Radar

The Worked Example Mr Tan from Ang Mo Kio

Strategic Considerations

Iggy’s Forensic Disclaimer

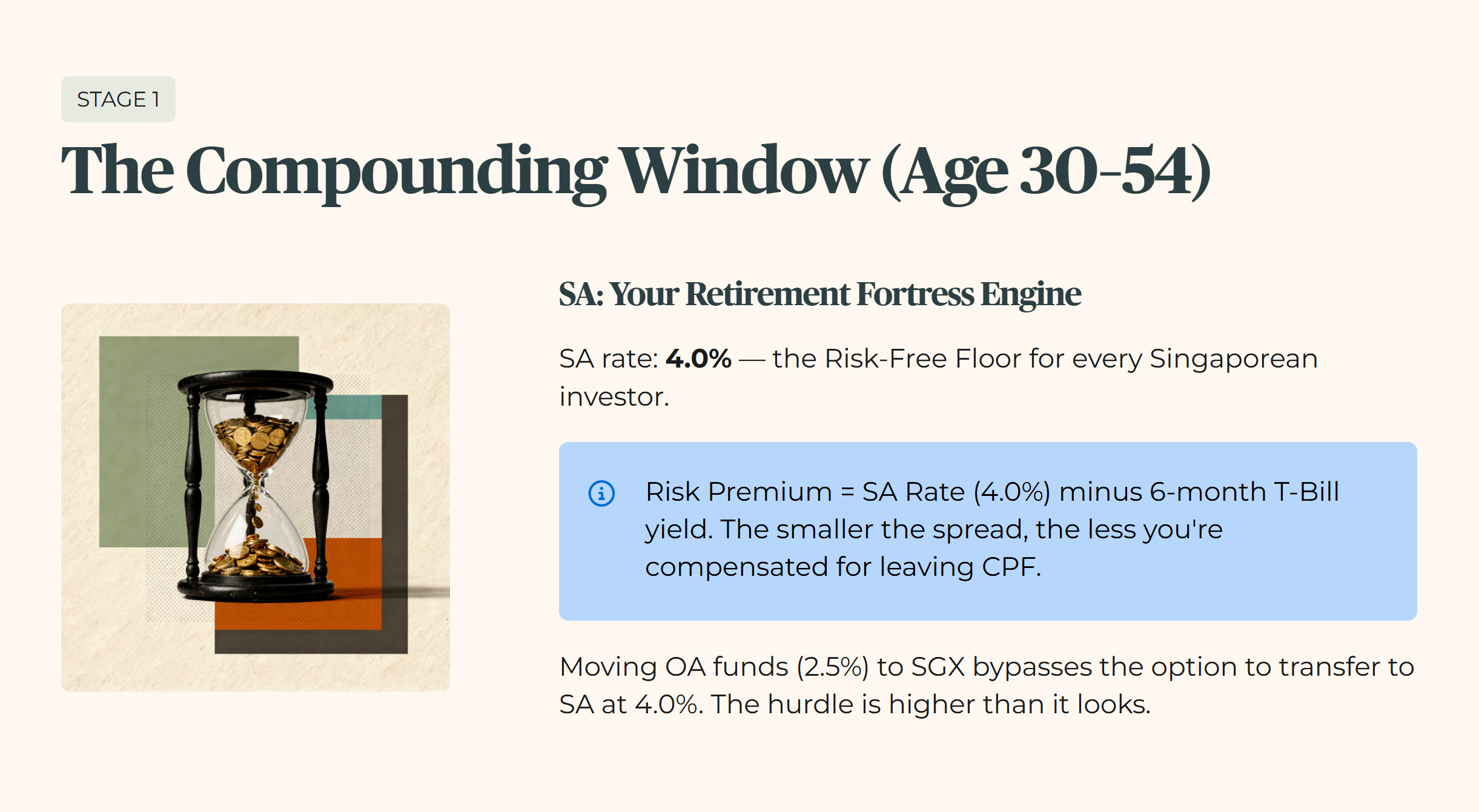

Stage 1 — The Compounding Window (Age 30–54)

In the decades leading up to the statutory pivot at age 55, your CPF Special Account (SA) is the primary engine of your retirement fortress. Currently, the SA interest rate sits at 4.0%, which represents the “Risk-Free Floor” for any Singaporean investor. To understand the gravity of moving funds out of the CPF system, you must first calculate the Risk Premium.

The Risk Premium is the SA Rate of 4.0% minus the current 6-month T-Bill yield. Before you process that number, understand what it means: the smaller this spread, the less you are being compensated for taking on any risk outside the CPF system. If the T-Bill is yielding 3.7%, you are accepting zero market risk for a mere 0.3% advantage. When you consider moving OA funds (paying 2.5%) into the SGX, the hurdle is even higher because you are bypassing the option to transfer those funds to your SA where they could earn a guaranteed 4.0%.

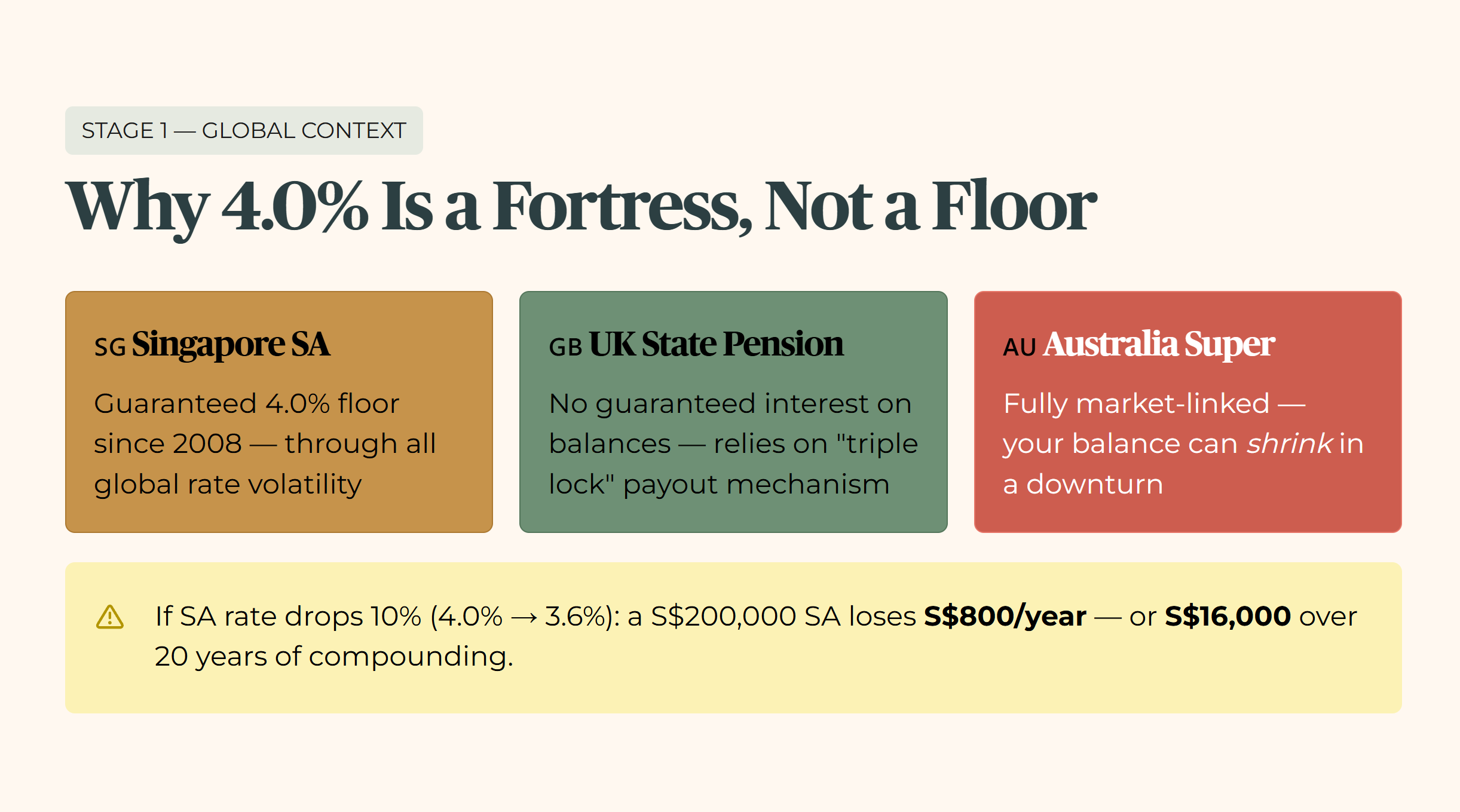

Historically, the SA rate has maintained a floor of 4.0% since 2008, despite global interest rate volatility. In contrast, equivalent pension schemes like the UK’s State Pension do not offer a guaranteed interest return on accumulated balances. They rely instead on a “triple lock” mechanism on the eventual payout. Australia’s Superannuation system is entirely market-linked. That means an Australian worker’s “Special Account” equivalent could actually shrink during a market downturn.

If policy were to shift and the SA rate dropped by 10% (from 4% to 3.6%), a household with S$200,000 in their SA would see an annual interest loss of S$800. That sounds manageable. But the wallet impact over a 20-year compounding horizon is a staggering S$16,000 in “missing” retirement fat. For a 45-year-old in Bedok, every dollar removed from the SA environment must work twice as hard in the private market just to break even against the power of 4.0% compounding.

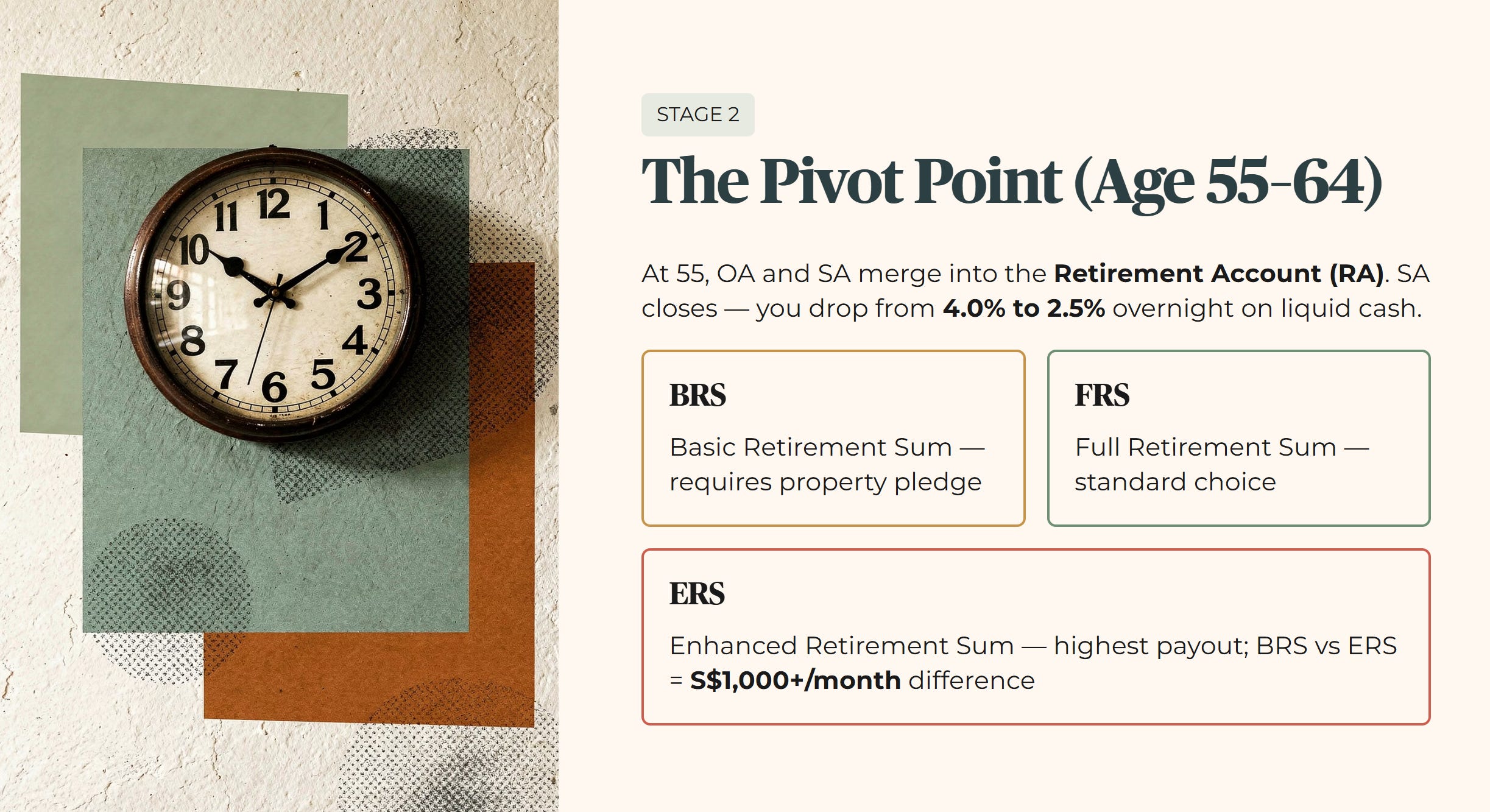

Stage 2 — The Pivot Point (Age 55–64)

When you hit age 55, the CPF system undergoes its most significant mechanical shift: the creation of the Retirement Account (RA). This is the pivot point where your OA and SA balances merge to form your retirement sum.

The most misunderstood mechanic for the 55-year-old heartlander is the closure of the SA. Once the RA is funded up to your chosen sum (be it the Basic Retirement Sum (BRS), Full Retirement Sum (FRS), or Enhanced Retirement Sum (ERS)), any remaining SA funds are often moved to the OA. This is a forensic consequence of the highest order. You move from earning 4.0% to 2.5% overnight on your liquid cash.

The choice between BRS, FRS, and ERS is not just a paperwork exercise. It is a lifestyle ceiling. For a household in Jurong, choosing the BRS (which requires a property pledge) versus the ERS could mean a monthly payout difference of over S$1,000 in their later years.

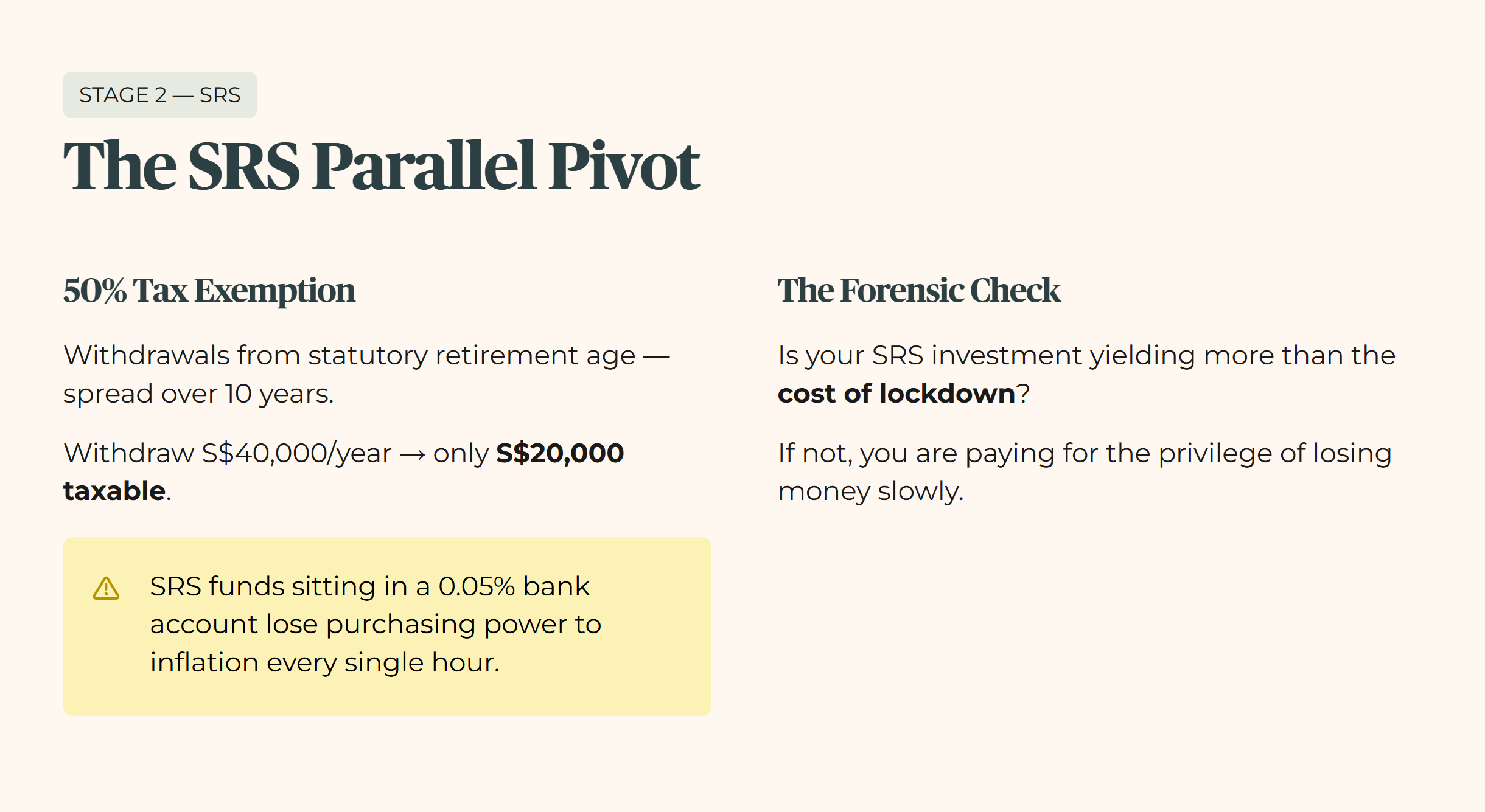

In the private sector, the Supplementary Retirement Scheme (SRS) offers a parallel pivot. You receive a 50% tax exemption on withdrawals starting from the statutory retirement age, provided you spread the drawdown over ten years. If you withdraw S$40,000 a year, only S$20,000 is taxable. For a 60-year-old, the forensic check is simple: is your SRS investment yielding more than the “cost of lockdown”? If your SRS funds are sitting in a bank 0.05% account, you are losing purchasing power to inflation every single hour.

🦎 Iggy’s Insight Block 1

Most heartland investors focus on the “extra” 2% yield they get from buying a REIT versus leaving money in the OA. They miss the silent erosion of the SA closure at 55. By failing to “shield” their SA properly before the RA is created, they effectively allow their highest-yielding sanctuary assets to be downgraded to 2.5%. The cost of this oversight over a decade is often more than the total dividends received from their stock portfolio. Don’t trip over dollars to pick up cents.

Forensic punchline: A high yield on a small capital base is a vanity metric. A guaranteed 4% on a massive sanctuary base is a retirement.

Stage 3 — The Drawdown Architecture (Age 65+)

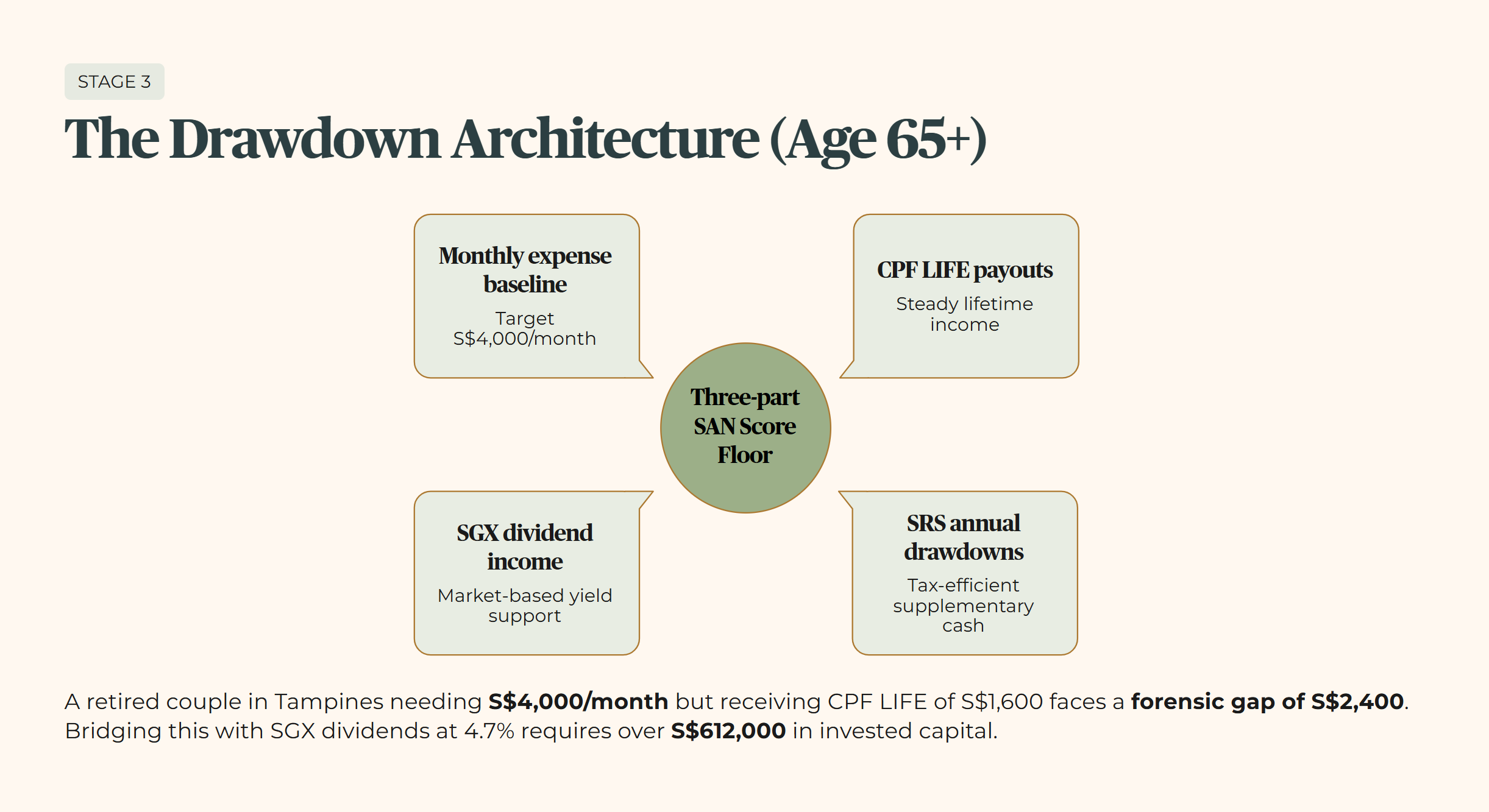

At age 65, the “accumulation” phase ends and the “drawdown” architecture begins. This is where we apply the SAN Score logic. The SAN Score tests whether your combined income floor (comprising CPF LIFE payouts, SRS annual drawdowns, and SGX dividend income) clears your monthly expense baseline.

The income gap is the number that matters most here. If a retired couple in Tampines requires S$4,000 a month to maintain their standard of living, but their CPF LIFE (FRS level) only provides S$1,600 [DATA GAP], they face a forensic gap of S$2,400. To bridge this with SGX dividends at a 4.7% yield requires over S$612,000 in invested capital.

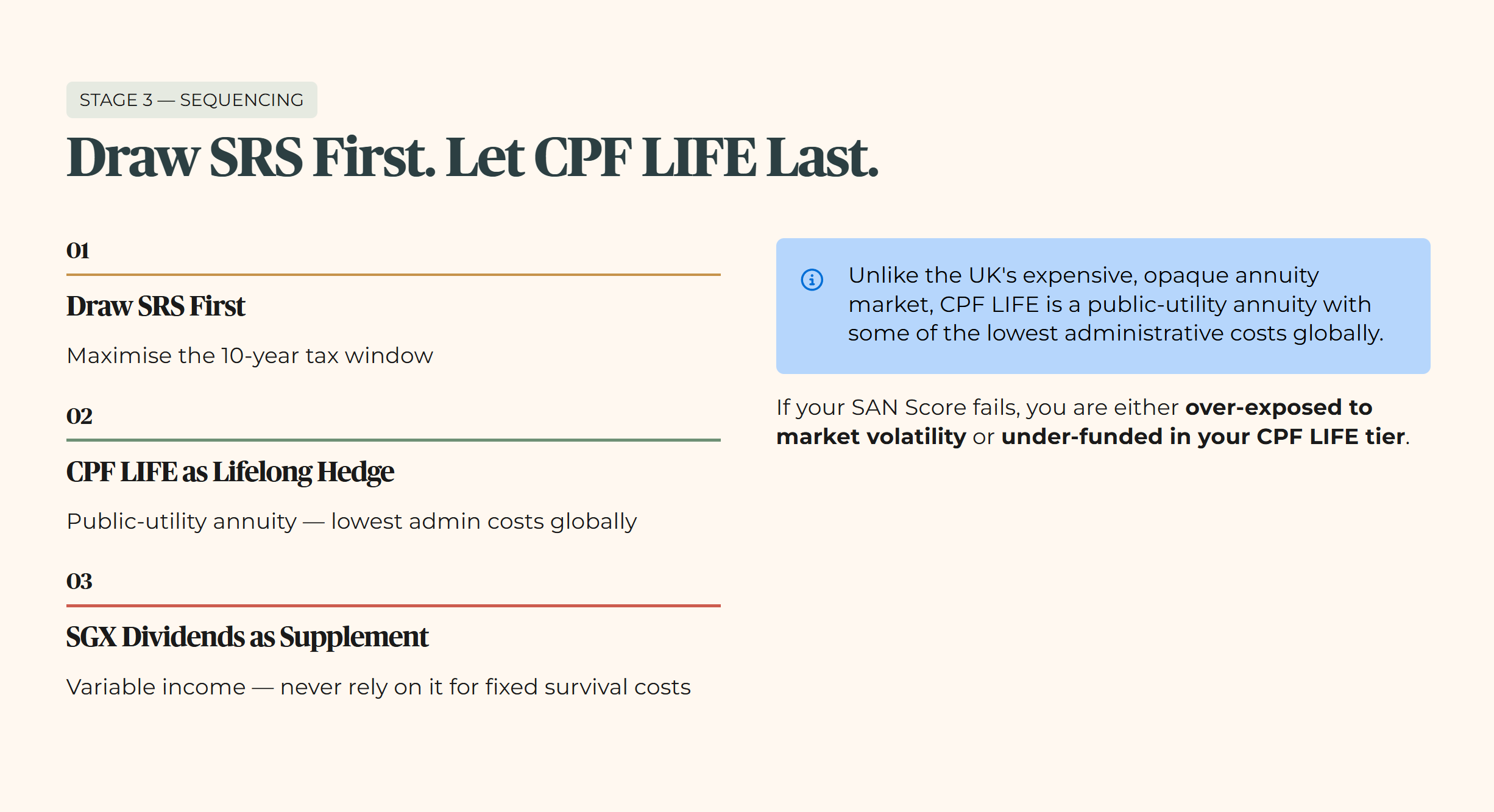

The sequencing here is vital. You should draw from the SRS first to maximise the 10-year tax window, while allowing CPF LIFE to provide the lifelong hedge against longevity risk. Unlike the UK’s annuity market (which can be expensive and opaque), CPF LIFE is a public-utility annuity with some of the lowest administrative costs globally. If your SAN Score fails, the forensic gap suggests you are either over-exposed to market volatility or under-funded in your CPF LIFE tier.

Stage 4 — The Legacy Layer (Estate Planning)

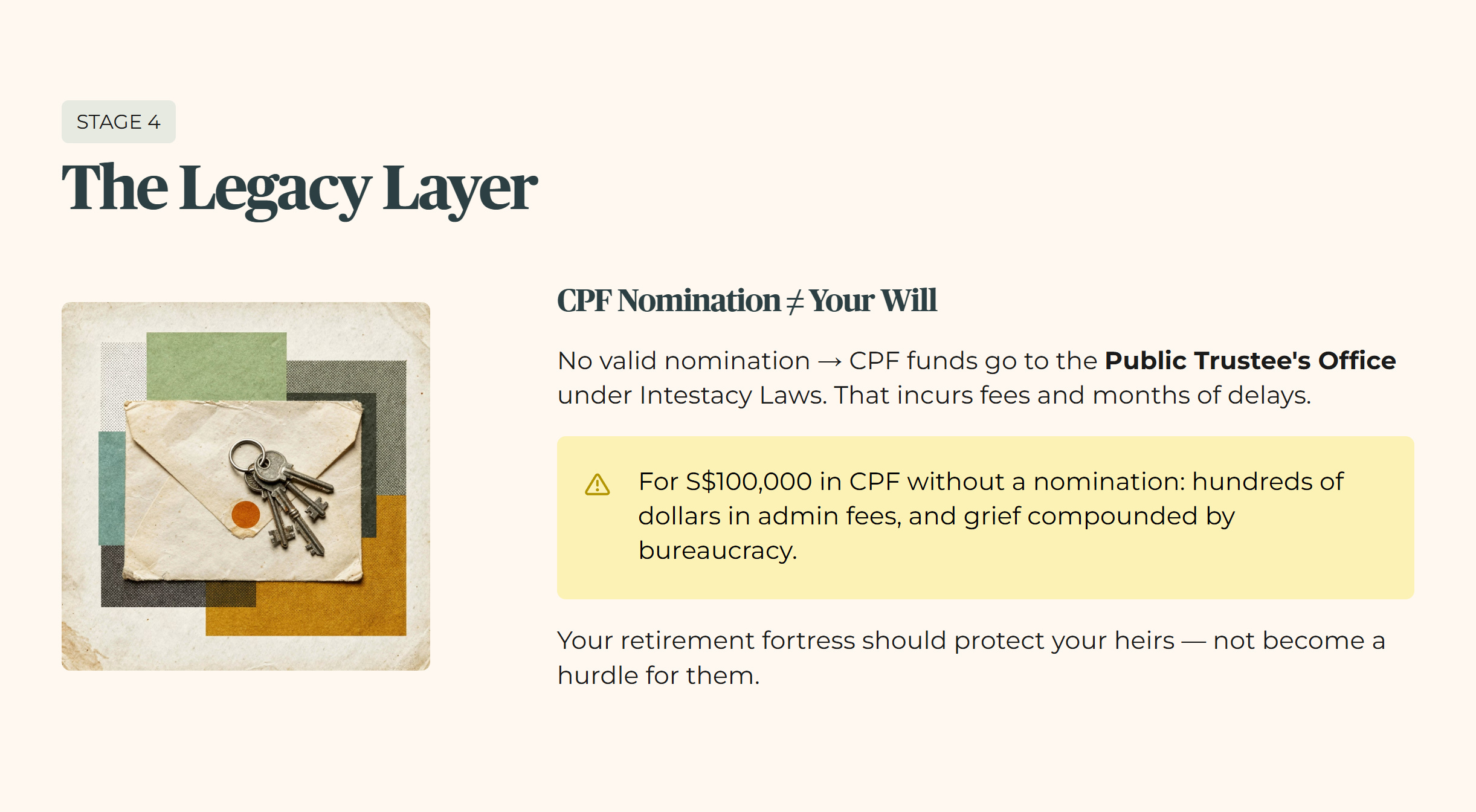

The final layer is one many prefer not to discuss: what happens to the fortress when the architect is gone? CPF nomination mechanics are distinct from a standard Will. If you do not have a valid nomination, your CPF funds are handed to the Public Trustee’s Office for distribution under Intestacy Laws. That incurs a fee.

For a deceased member with S$100,000 in CPF, the lack of a nomination could result in hundreds of dollars in administrative fees and months of delays for the grieving family. This is educational context only. Awareness of this mechanic ensures that your retirement “fortress” actually protects your heirs, rather than becoming a bureaucratic hurdle.

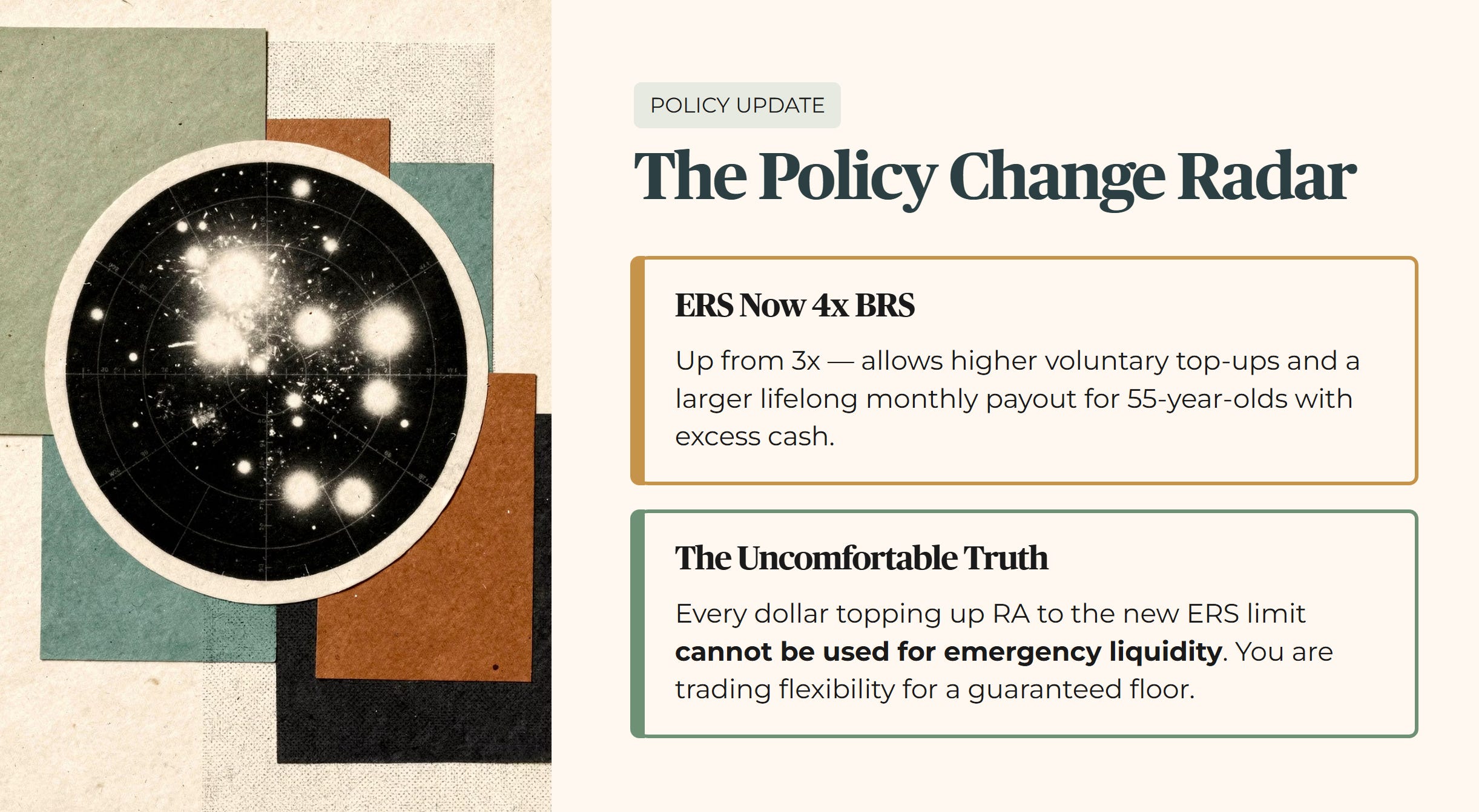

The Policy Change Radar

The most recent Singapore Budget has introduced a significant shift in the retirement landscape. The Enhanced Retirement Sum (ERS) limit has been raised to four times the Basic Retirement Sum.

Policy Fact: The ERS is now 4x the BRS, allowing for higher voluntary top-ups.

Wallet Impact: For a 55-year-old in Toa Payoh with excess cash, this change allows them to lock in a higher lifelong monthly payout. That could increase their CPF LIFE check by several hundred dollars compared to the previous 3x BRS cap.

And let’s be honest, they are not wrong to be excited about higher caps. But here is the uncomfortable truth: every dollar used to top up the RA to the new ERS limit is a dollar that cannot be used for emergency liquidity. You are trading flexibility for a guaranteed floor.

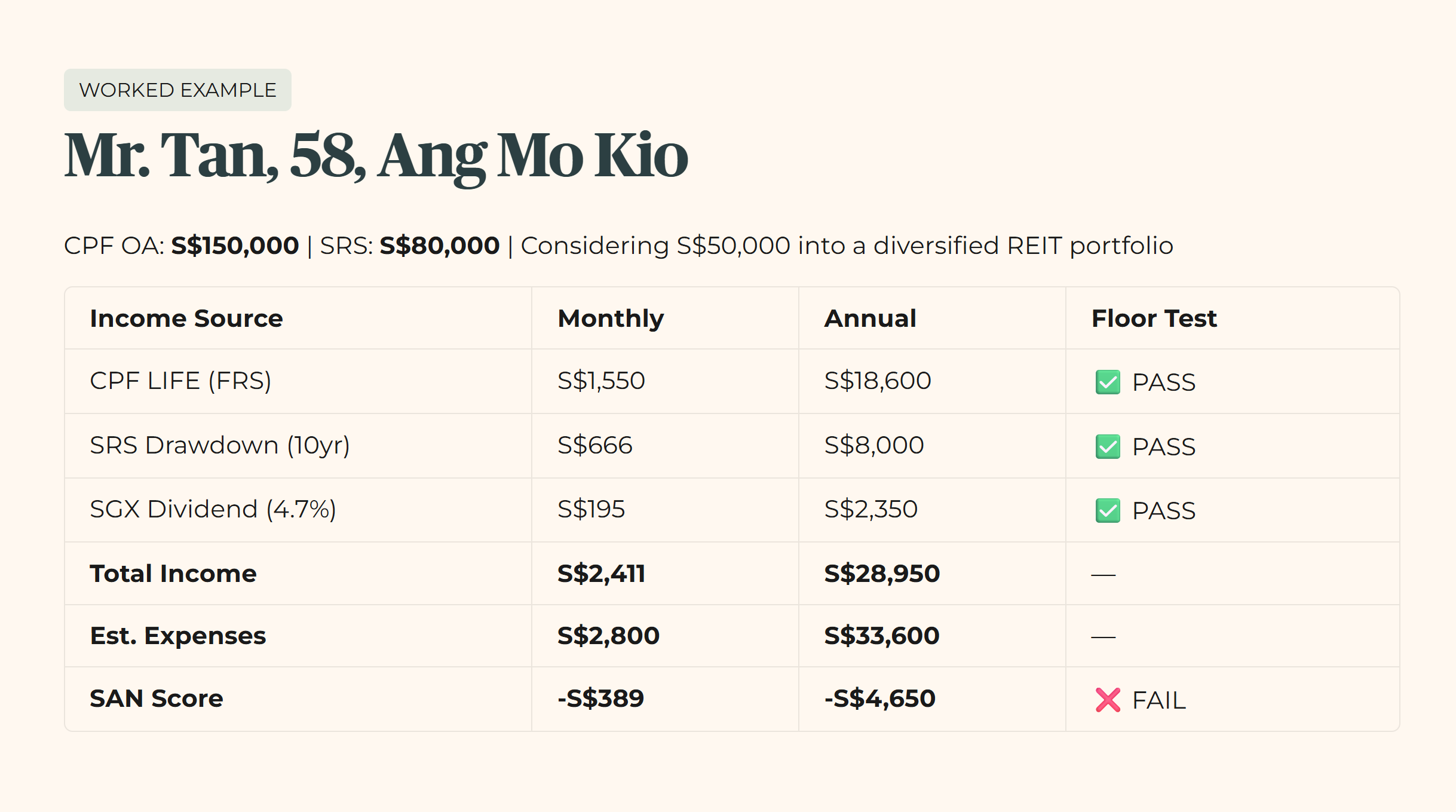

The Worked Example: Mr. Tan from Ang Mo Kio

Mr. Tan is 58 years old, living in a 4-room HDB in Ang Mo Kio. He has S$150,000 in his CPF OA and is considering moving S$50,000 into the SGX to boost his retirement income. He also has S$80,000 in his SRS account.

Age: 58 Location: Ang Mo Kio CPF OA Balance: S$150,000 [DATA GAP] SRS Position: S$80,000 (Current annual contribution cap: S$15,300) SGX Holdings: Considering a diversified REIT portfolio.

Note on the Stress-Test Buffer: When projecting SGX dividend income against guaranteed CPF rates, I apply a conservative floor of 3.2%. We plan for the storm, not just the sunny day. While the T-Bill sits at [DATA GAP], I do not lower my standards to match a temporary market dip. My floor remains at 3.2% to ensure sanctuary assets can withstand a return to long-term average interest rates. The minimum yield hurdle for any SGX holding in this portfolio is 4.7%. That is the 3.2% floor plus 150 basis points of mandatory risk premium.

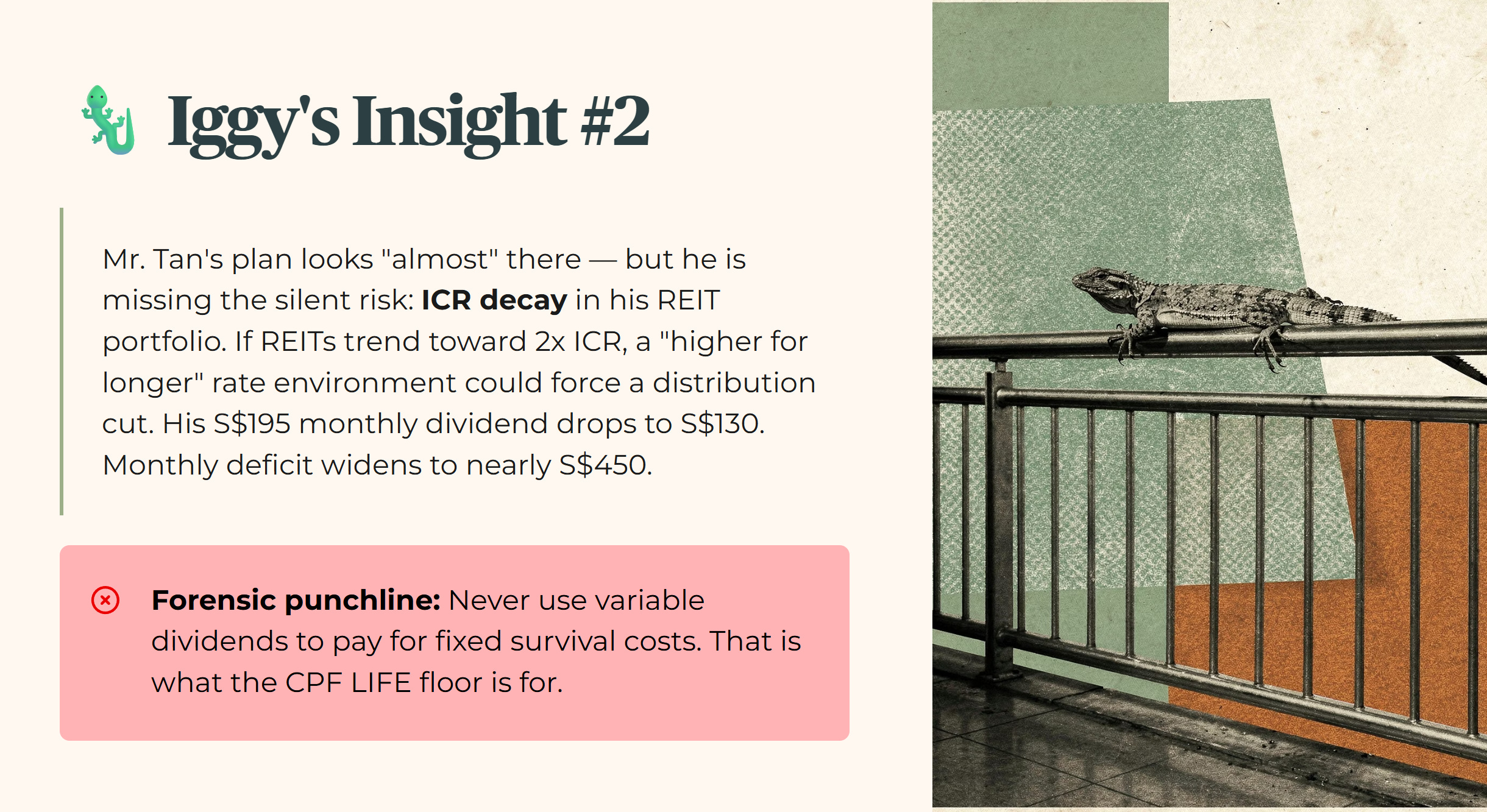

🦎 Iggy’s Insight Block 2

Mr. Tan’s plan looks “almost” there, but he is missing the silent risk: Interest Coverage Ratio (ICR) decay in his REIT portfolio. If the REITs he buys have an ICR trending toward 2x, a “higher for longer” rate environment could force a distribution cut. Suddenly, his S$195 monthly dividend drops to S$130, widening his monthly deficit to nearly S$450. He is relying on market-linked income to cover a basic survival gap.

Forensic punchline: Never use variable dividends to pay for fixed survival costs. That is what the CPF LIFE floor is for.

Strategic Considerations

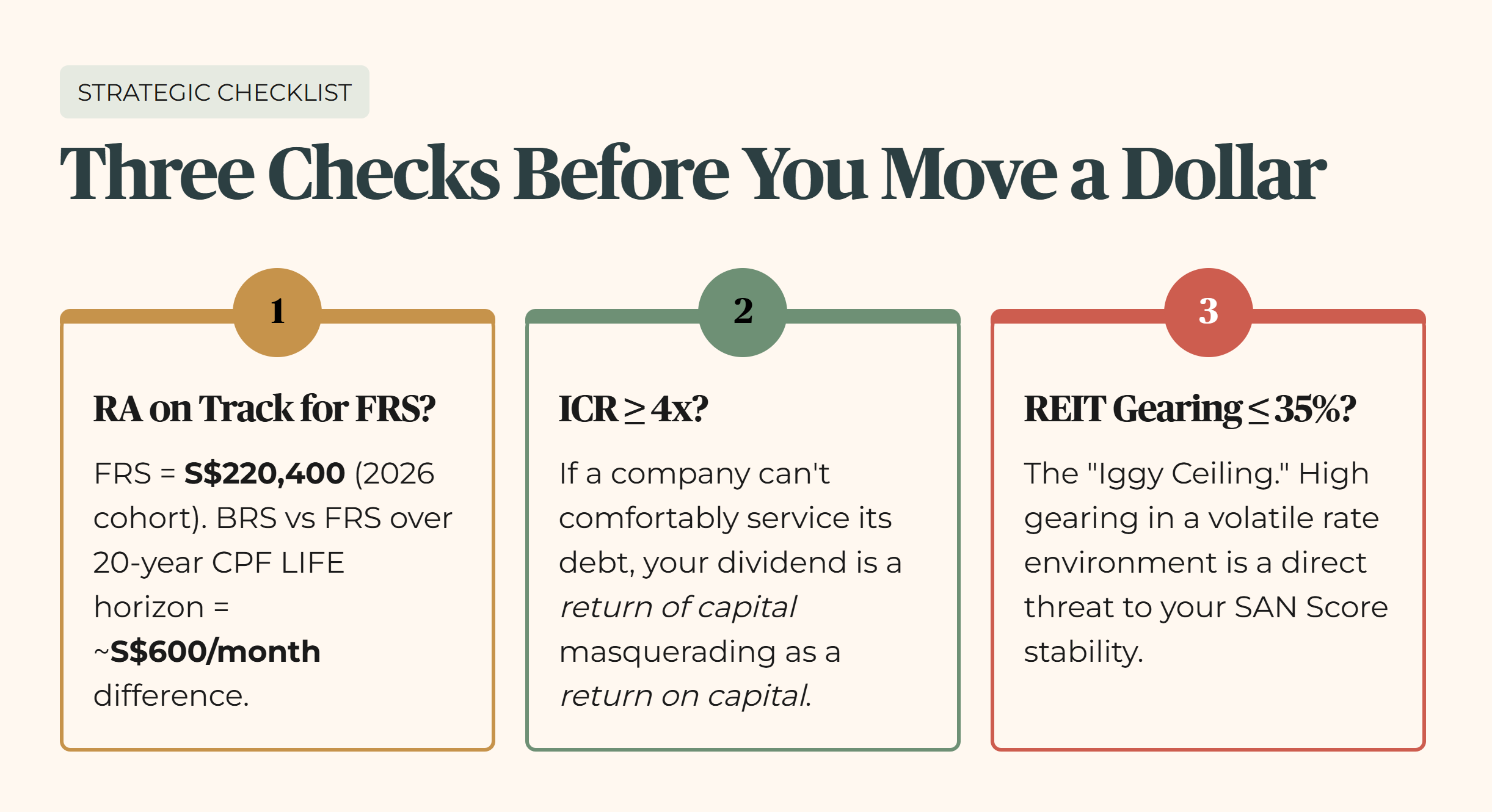

Strategic Consideration 1: If you are between 55 and 60, check whether your RA balance is on track for FRS (S$220,400 for 2026 cohort) before the next contribution window closes. The monthly payout difference between BRS and FRS over a 20-year CPF LIFE horizon is approximately S$600.

Strategic Consideration 2: Audit your SGX dividend stocks for an ICR of at least 4x. If a company cannot comfortably service its debt, your dividend is a “return of capital” masquerading as a “return on capital.”

Strategic Consideration 3: Verify the gearing (the proportion of a company’s assets funded by debt) of any REIT in your portfolio against the 35% “Iggy Ceiling.” High gearing in a volatile rate environment is a direct threat to the stability of your SAN Score.

If your broker’s “4.8% yield” pick fails the 4x ICR test, are you actually investing, or are you just lending money to a distressed balance sheet?

LongBridge Promo

This analysis is brought to you by Longbridge SG.

Fixing the analysis is the easy part. Fixing the execution requires the right tools.

I’ve shifted my own deployment to for one forensic reason: they are currently the only platform in Singapore offering Lifetime S$0 Commission on US, HK, and SG stocks. For a DCA investor running monthly tranches, that single change eliminates the entire minimum commission drag we just calculated. Their data visualisation is also fast enough for volatile entry windows — which matters when you are trying to time a position, not just place one.

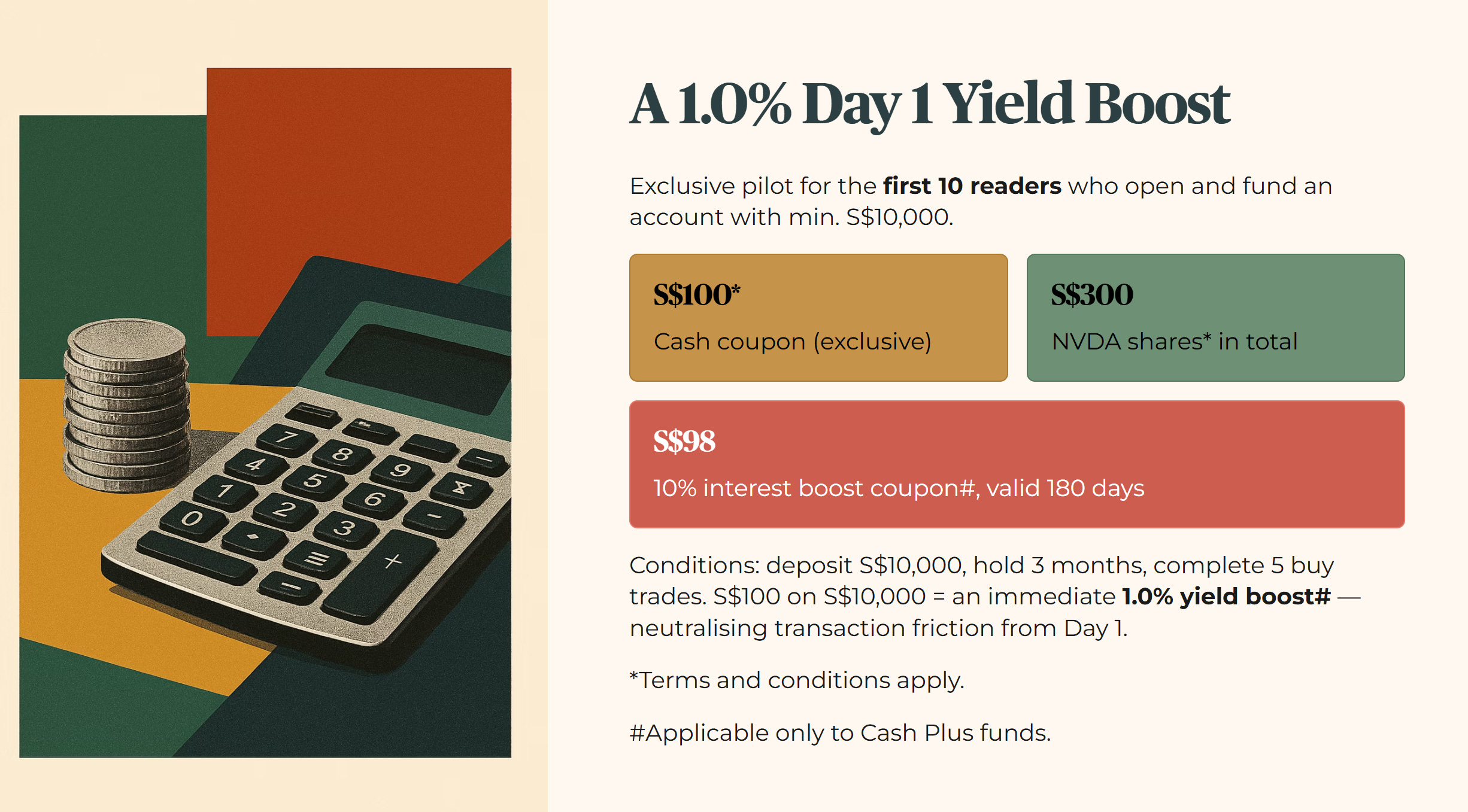

I’ve partnered with Longbridge on a specific pilot for this community. The first 10 readers to open and fund an account with a minimum of S$10,000 will receive a direct S$100 cash credit.

The forensic math: S$100 on a S$10,000 deployment is a 1.0% Day 1 Yield Boost — effectively neutralising your entry cost before you’ve bought a single share. For context, that’s better than the yield spread on several SGX blue chips I’ve reviewed this quarter.

This is strictly limited to 10 spots. Full terms and conditions are linked below — read them before committing, as standard platform fees apply.

All CPF figures, contribution rates, BRS/FRS/ERS limits, and SRS caps referenced in this article are subject to change. Figures are current as of the most recent Singapore Budget announcement at time of writing. Always verify current figures directly at cpf.gov.sg before making any CPF or SRS decision.

Iggy’s Forensic Disclaimer

This content is produced for educational and informational purposes only. I am not a financial advisor — I am a retail investor who applies forensic analysis to my own portfolio and shares that process publicly. Nothing here constitutes a recommendation to buy, sell, or hold any security, and no specific target prices or personalised financial advice are offered. All data is sourced from public filings and verified sources; where data is unverified it is explicitly flagged. All investments carry risk, including the potential loss of principal, and past performance is not indicative of future results. If you are making investment decisions involving CPF, SRS, or personal capital, please conduct your own due diligence or consult a MAS-licensed financial adviser before committing funds.

Important Partner Disclosure

This content is a paid collaboration with Longbridge Singapore. It is intended for general awareness and does not constitute investment advice or a recommendation for any specific financial product.

Licensing Note: The presenter is not a licensed financial adviser. Views expressed are solely those of the presenter and do not necessarily reflect the position of Longbridge Singapore. Investments involve risk; you may lose your principal. This advertisement has not been reviewed by the Monetary Authority of Singapore. Always seek independent professional advice if unsure.