Before You Buy July's Watchlist: Three Names, Three Very Different Verdicts

One name clears my balance sheet test easily. One fails on cash. One I'm still not confident enough to rate.

One name clears my balance sheet test easily. One fails on cash. One I’m still not confident enough to rate.

Mainstream financial journalism is heavily promoting a fresh July 2026 corporate watchlist, shifting stock prices based entirely on top-line press release summaries. Heartland retail investors buying into these headline expansions are unknowingly exposing their retirement capital to silent structural deficits and hard threshold breaches. Today, we strip away the media noise and apply our non-negotiable forensic filters to Seatrium, OUE REIT, and Singapore Airlines to expose exactly where the top-line numbers flatten out.

If you are chasing growth and momentum, a higher-risk profile may clear your hurdle. But if you are a retiree focused on wealth preservation and dependable drawdown income, my forensic standard is built to protect that. The immediate pressure of the newly hiked July 2026 household electricity tariff of 34.78 cents per kWh inclusive of GST means your portfolio cash must be real, not an accounting adjustment. Let’s look at the actual cash on the table.

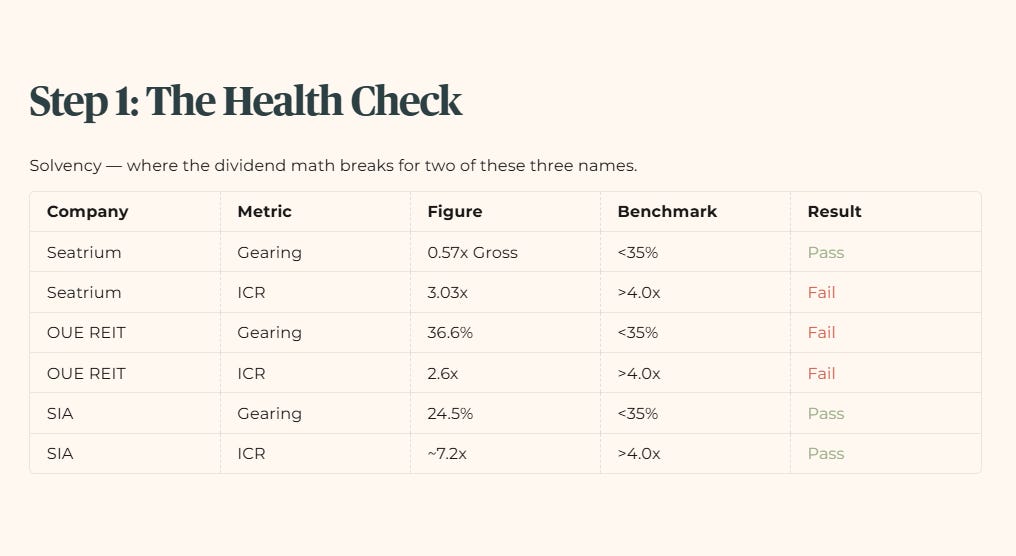

STEP 1: THE HEALTH CHECK (Solvency)

Financial Health Checklist

STEP 2: THE WEALTH CHECK (Yield and Cash Flow)

Dividend Trajectory

Block 1: Seatrium Limited (SGX: 5E2): The Cash Flow Mirage

Scenario Table 1: Seatrium Cash Commitment Deficit

Block 2: OUE REIT (SGX: TS0U): The Gearing Ceiling Breach, Yield Under Review

Scenario Table 2: OUE REIT Capital Allocation to Sub-35%

Block 3: Singapore Airlines Ltd (SGX: C6L): The Peak Margin Squeeze

Scenario Table 3: SIA Margin Variable Impact

STEP 3: THE PRICE CHECK (Valuation)

STEP 4: THE BOTTOM LINE (Forensic Stance)

Seatrium Limited (SGX: 5E2)

OUE REIT (SGX: TS0U)

Singapore Airlines Ltd (SGX: C6L)

STEP 1: THE HEALTH CHECK (Solvency)

This is where the dividend math breaks, for two of these three names.

Financial Health Checklist

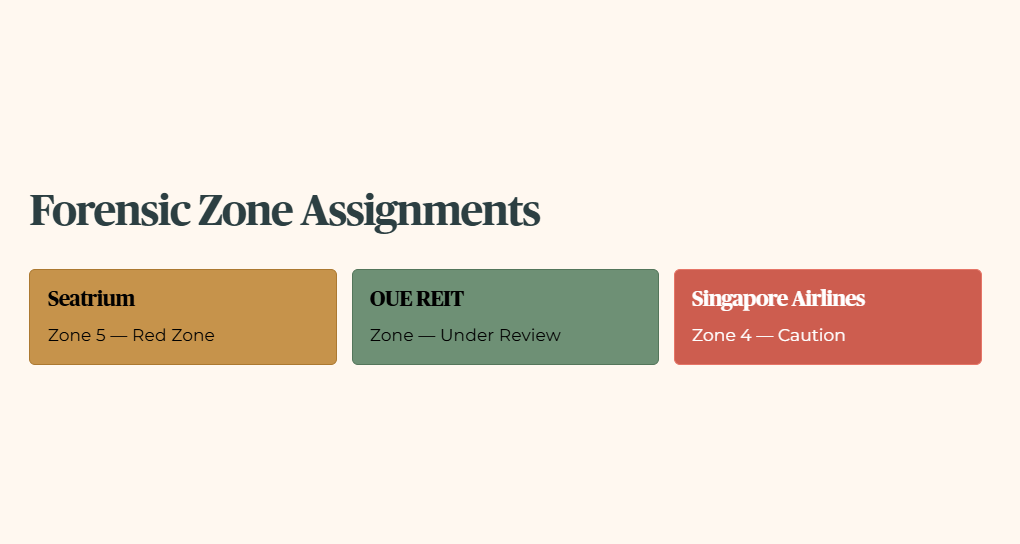

Iggy’s Forensic Zone: Zone 4, Caution applies to Singapore Airlines. Iggy’s Forensic Zone: Zone 5, Red Zone applies to Seatrium. OUE REIT’s zone assignment is under review, more on that below.

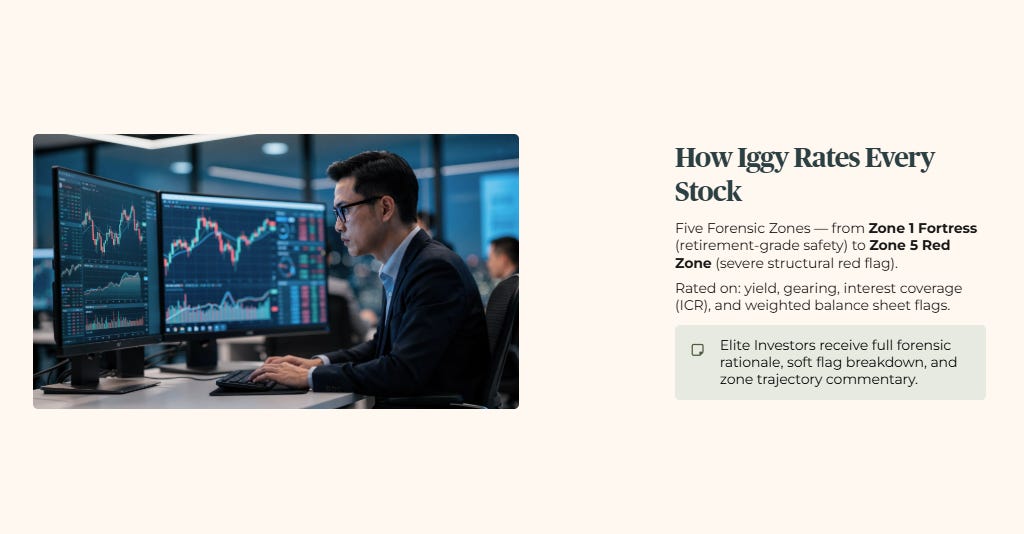

How Iggy Rates Every Stock: Every stock I track receives a Forensic Zone rating based on yield, gearing or capital strength, interest coverage (ICR, or interest coverage ratio, the number of times a company’s operating profit can cover its interest bill), and weighted balance sheet flags. There are five zones running from Zone 1 Fortress, retirement-grade safety, to Zone 5 Red Zone, a severe structural red flag. Elite Investors receive the full forensic rationale, soft flag breakdown, and zone trajectory commentary for every stock covered.

STEP 2: THE WEALTH CHECK (Yield and Cash Flow)

Paper profits do not pay for your wet market groceries.

Dividend Trajectory

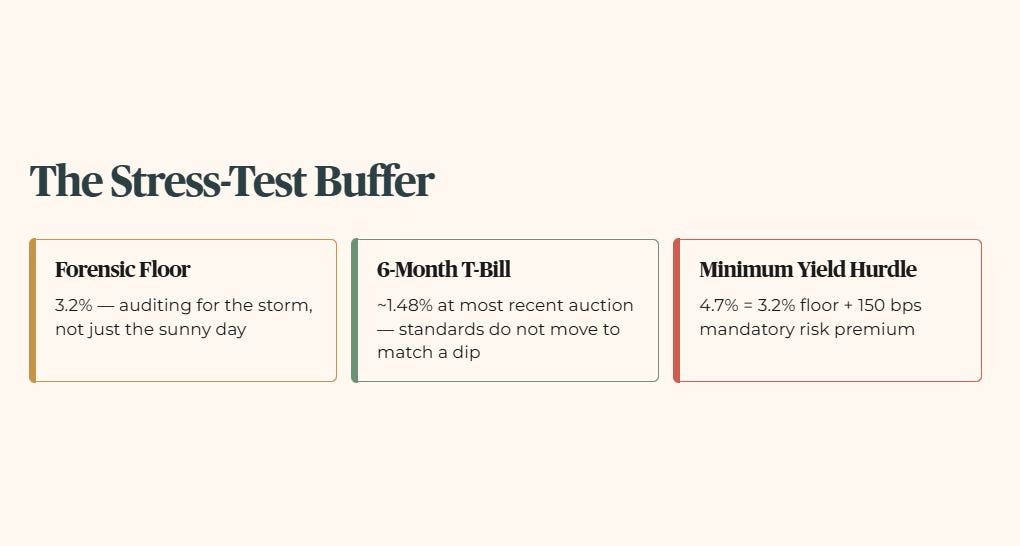

Note on the Stress-Test Buffer: for this audit, I apply a conservative floor of 3.2%. We audit for the storm, not just the sunny day. The 6-month T-bill sits at approximately 1.48% as at the most recent completed auction. I do not lower my standards to match a temporary market dip. My floor remains at 3.2% to ensure sanctuary assets can withstand a return to long-term average interest rates. The minimum yield hurdle is 4.7%, that is the 3.2% floor plus 150 basis points of mandatory risk premium.

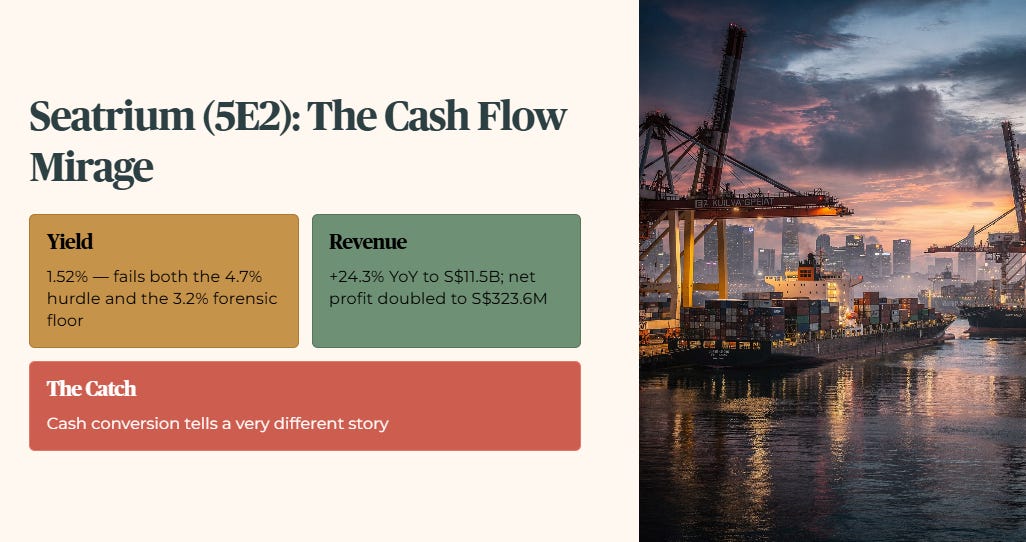

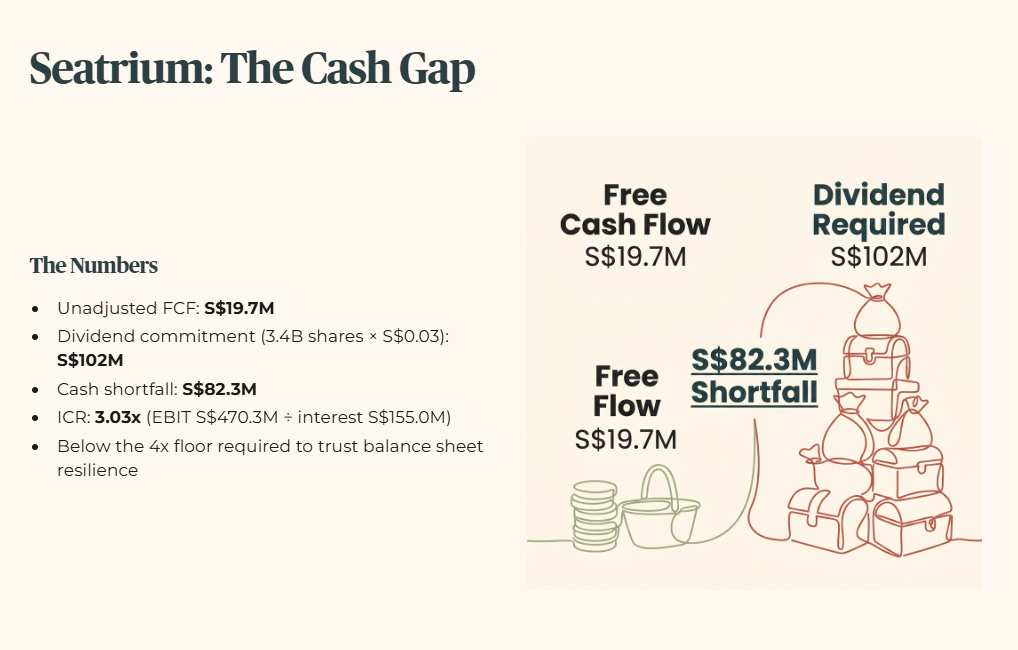

Block 1: Seatrium Limited (SGX: 5E2): The Cash Flow Mirage

The annualised distribution stands at S$0.03 against a current closing price of S$1.98. This places the yield at a thin 1.52%, failing not just our 4.7% Minimum Yield Hurdle but the 3.2% Forensic Floor itself. While total revenue scaled 24.3% year on year to S$11.5 billion and net profit doubled to S$323.6 million, the cash conversion tells a different story, and so does the interest coverage.

Unadjusted free cash flow, the cash left after operating expenses and maintaining capital assets, sits at a razor-thin S$19.7 million. With 3.4 billion shares outstanding, the S$0.03 dividend commitment demands S$102 million in cash, an S$82.3 million shortfall funded partly by legacy settlement drag rather than core operations. Interest coverage, EBIT of S$470.3 million against gross interest expense of S$155.0 million, comes to 3.03x, below the 4x floor I require before I trust a balance sheet to absorb a rate shock.

Scenario Table 1: Seatrium Cash Commitment Deficit

🦎 Iggy’s Insight

Seatrium looks like a spectacular turnaround story on paper because accounting profits have surged. But an engineering giant cannot pay tangible dividends with paper profits when unadjusted free cash flow is pinned at S$19.7 million and interest coverage sits below my 4x floor. This is not a single-gate miss. Yield fails the 3.2% floor outright, coverage fails independently, and cash conversion confirms both readings point the same direction. For a retiree needing dependable income, this is an industrial turnaround project, not an income sanctuary. You are funding capital-heavy engineering execution, with borrowed time on the balance sheet, rather than collecting extraction.

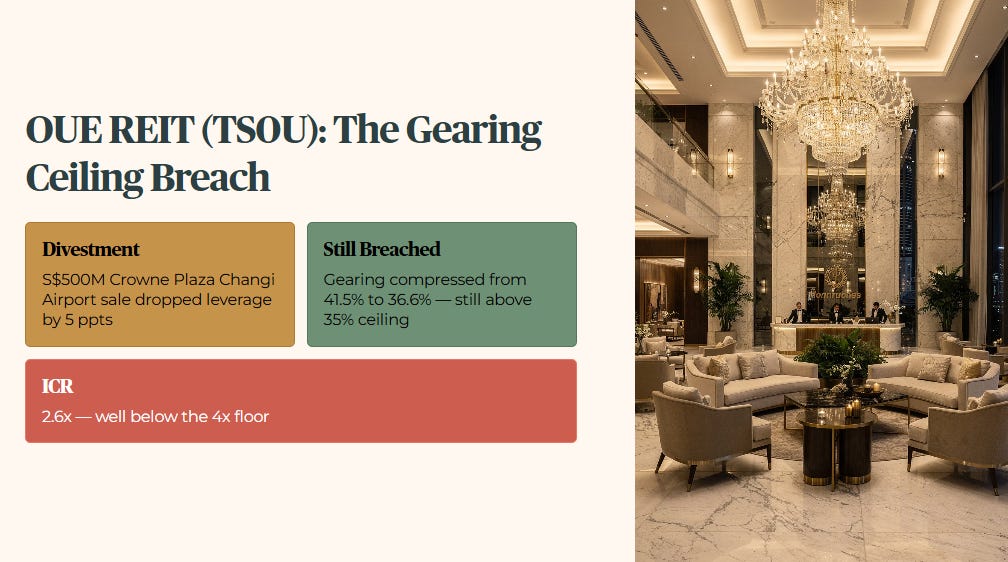

Block 2: OUE REIT (SGX: TS0U): The Gearing Ceiling Breach, Yield Under Review

OUE REIT’s high-profile S$500 million asset divestment of the Crowne Plaza Changi Airport hotel dropped pro-forma aggregate leverage by 5 percentage points. However, the trust’s gearing (the proportion of the trust’s assets funded by debt) compressed only from 41.5% down to 36.6%. At 36.6%, the trust remains in structural breach of our strict 35% S-REIT Gearing Ceiling. Interest coverage, meanwhile, sits at a weak 2.6x, well below the 4x floor.

Those two figures are independently confirmed and are not in dispute. What I am holding back is the zone verdict itself. OUE REIT’s headline distribution yield is quoted at 6.19%, but that number carries a payout ratio north of 400%, a strong signal that a meaningful share of the distribution is not recurring rental income.

My own sourcing has come back contradictory on how much: one read says roughly a fifth of the trailing payout traces to earlier divestment-linked capital distributions, another says the most recent full year was entirely ordinary income with the divestment-linked special distribution still to come. I am not going to hand you a Forensic Zone built on a coin flip. Until I can confirm the ordinary-only distribution figure against OUE REIT’s own annual report, this stock’s zone stays open. The gearing and coverage breaches above are real and stated regardless of how that resolves.

The gearing and coverage breaches above are hard fails against my 35% ceiling and 4.0x floor — but the ordinary-only yield calculation in the next section is what decides whether OUE REIT clears the forensic standard or stays under review.