Beng Kuang Marine Stock Analysis: The Truth Behind UOB’s Bullish S$0.75 Target | EP1605🦖

Singapore ships, ports, rigs wait on ASOM

An institutional BUY call slapped on a stock yielding just 1.0 percent is not an income play, it is a high stakes bet on corporate execution. When UOB Kay Hian upgrades Beng Kuang Marine to an S$0.75 target price, the narrative pivots entirely on future FPSO contracts and an asset light transformation. Today we put that institutional growth thesis through the forensic wringer to see if it holds water for a retirement portfolio.

I have been tracking the maritime support services sector closely as the structural demand for offshore vessels shifts gears. It is always interesting when a research house pounds the table on a small cap player in the middle of a major operational pivot. Let us strip away the narrative and look at the raw mechanics driving this stock.

In This Article:

Section 1: The Analyst’s Case

Section 2: Iggy’s Forensic Screen

Financial Health Checklist

Section 3: The Dividend Trajectory

Section 4: The Forensic Gap

The Analyst’s Desk vs. Iggy’s Forensic Screen

Dimension 1: How We Value the Stock

Dimension 2: How We Treat Income

Dimension 3: How We Weight Execution Risk

Dimension 4: How We Read the Ownership Signal

Dimension 5: Who This Verdict Is Actually For

Section 5: What To Watch Next

Closing: The Forensic Stance

Iggy’s Forensic Disclaimer

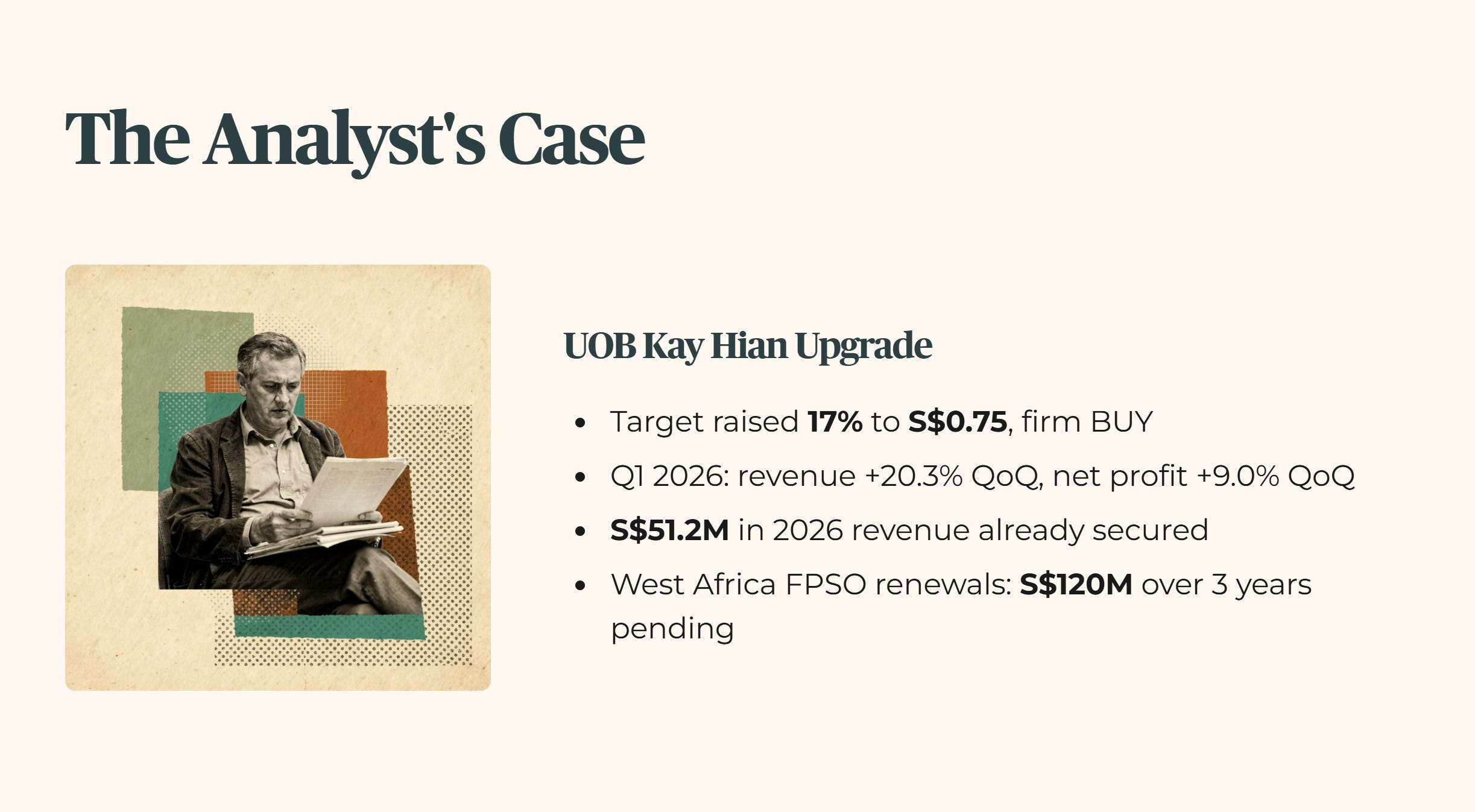

Section 1: The Analyst’s Case

UOB Kay Hian recently issued an upgraded research note on Beng Kuang Marine (SGX:BEZ), raising their target price by 17 percent to S$0.75 and maintaining a firm BUY rating.

The institutional thesis is aggressively bullish on the company’s growth prospects following its first quarter 2026 performance. While net profit dipped 12.7 percent year over year to S$2.8 million, the analyst focuses heavily on the strong quarter over quarter momentum, where revenue climbed 20.3 percent and net profit rose 9.0 percent. The research house highlights the firm’s strong contract pipeline, noting S$51.2 million in 2026 revenue already secured and an impending finalization of West Africa FPSO renewals estimated at S$120 million over three years.

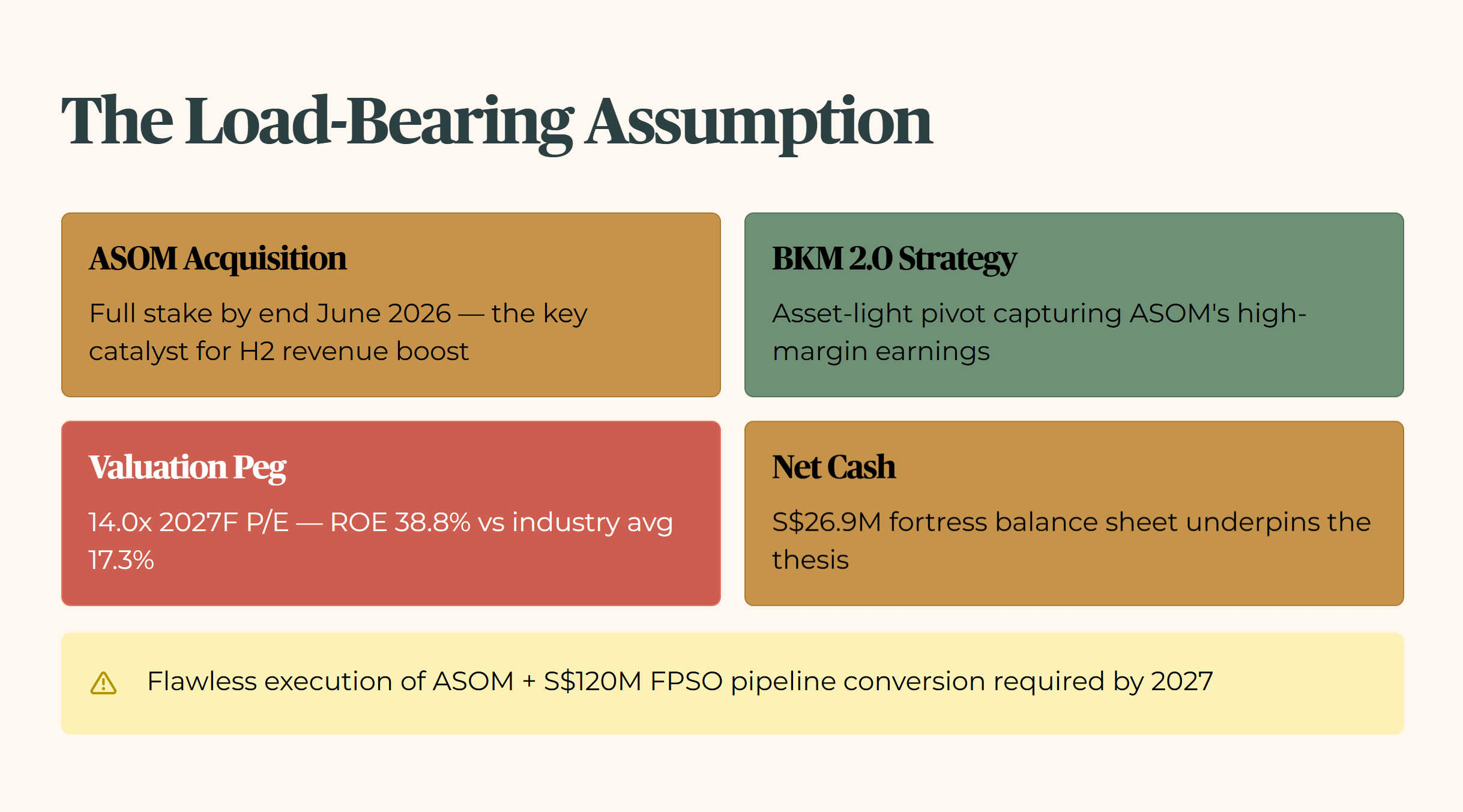

Furthermore, the planned acquisition of the remaining ASOM stake by end of June 2026 is championed as a massive catalyst. UOB projects this transaction will heavily boost second half 2026 revenue and align perfectly with Beng Kuang Marine’s “BKM 2.0” strategy, a move toward an asset light business model capturing ASOM’s high margin earnings.

The valuation target of S$0.75 is pegged to a 14.0x 2027F P/E, justified by a superior ROE of 38.8 percent against an industry average of 17.3 percent and a strong net cash position of S$26.9 million. THE LOAD-BEARING ASSUMPTION: Beng Kuang Marine will flawlessly execute its asset light BKM 2.0 pivot and successfully convert its S$120 million West Africa FPSO pipeline into high margin, recognized revenue by 2027.

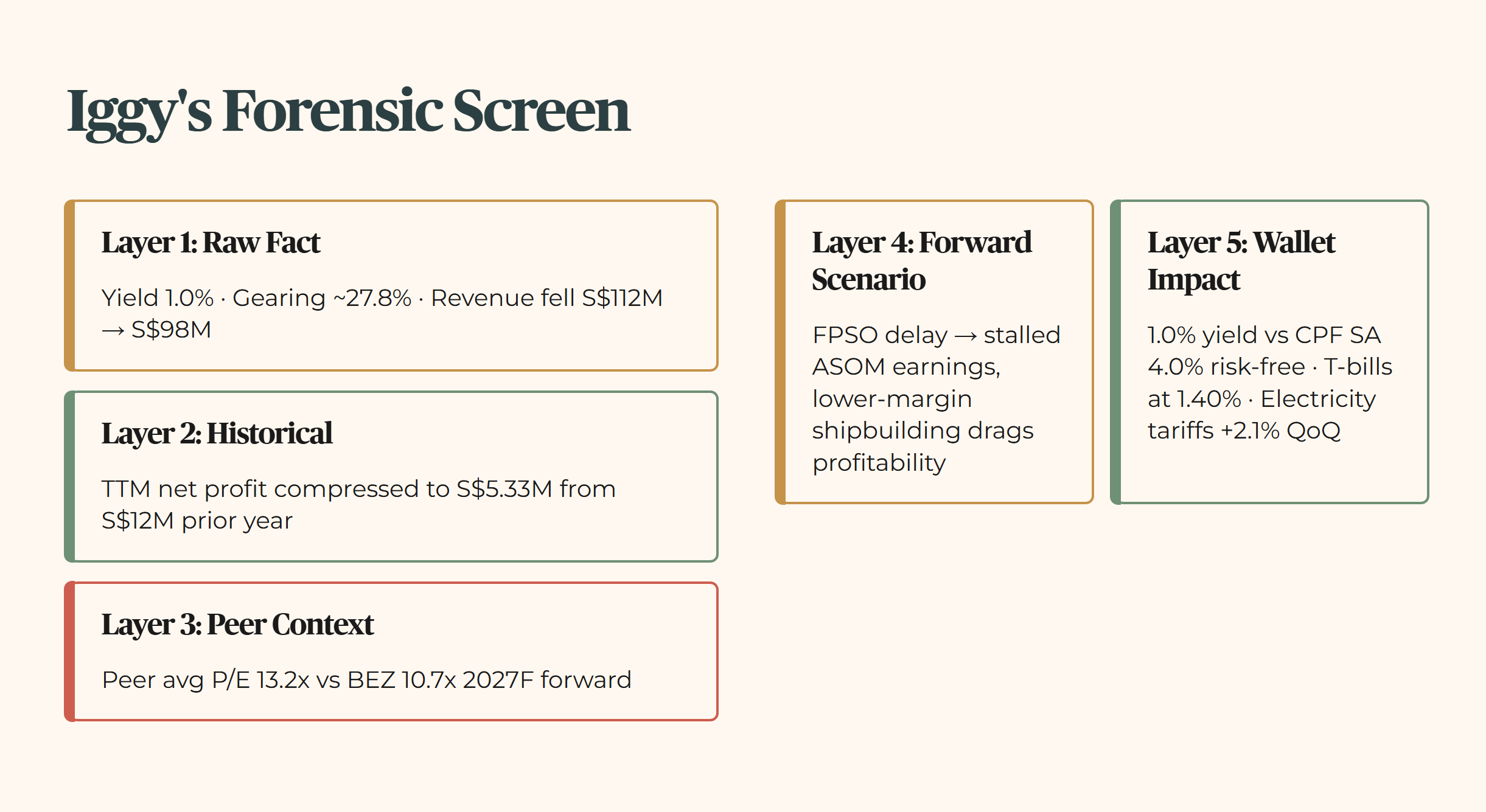

Section 2: Iggy’s Forensic Screen

We evaluate the raw data against our strict retirement income standards. Here is the five layer audit based on the verified figures provided.

Layer 1: Raw Fact. The trailing dividend yield is an anemic 1.0 percent. Total debt stands at S$10 million against total equity of S$36 million, placing gearing well within safe limits at roughly 27.8 percent. However, revenue dropped from S$112 million in FY2024 to S$98 million in FY2025.

Layer 2: Historical Benchmark. An extended three to five year dividend average was not supplied. We can observe that recent trailing twelve month net profit compressed to S$5.33 million from S$12 million in the prior year, marking a distinct operational contraction before the current quarter’s narrative.

Layer 3: Peer Context. Specific peer financial data was not supplied for a direct fundamental comparison, though the analyst notes a peer average P/E of 13.2x versus the company’s 10.7x 2027F forward estimate.

Layer 4: Forward Scenario. If the West Africa FPSO renewals are delayed by a minus 10 percent macro shift in offshore contract finalizations, the projected jump in high margin ASOM earnings could stall. This scenario would keep the company reliant on lower margin early stage shipbuilding work, dragging down profitability while overheads for the new floatel deployment expand.

Layer 5: Wallet Impact. For a 55 year old Singapore investor managing a CPF or SRS portfolio, this is entirely a capital appreciation play. The 1.0 percent yield does not pay the utility bills or offset the recent 2.1 percent quarter on quarter increase in electricity tariffs. With T-bills offering 1.40 percent and the CPF SA providing a risk free 4.0 percent sanctuary, accepting a 1.0 percent equity yield requires absolute faith in capital gains.

Financial Health Checklist

Soft Flag Count: 3. We have revenue declining consecutively from FY24 to FY25, net profit declining over the same period, and total debt trending upward from S$8.31 million to S$10 million.

Section 3: The Dividend Trajectory

For a retail investor, a growth narrative must eventually translate to physical distributions into your bank account. Let us look at the distribution facts.

Dividend Trajectory

The current 1.0 percent yield falls severely short of our 3.2 percent Forensic Floor and completely misses the 4.7 percent Minimum Yield Hurdle. There are no sponsor top ups present in the figures, but the distribution footprint is minimal. Under a forward scenario where margin compression continues from project mix changes, specifically a heavier reliance on early stage shipbuilding over premium FPSO services, free cash flow may be directed entirely toward the ASOM acquisition and Angola floatel deployment rather than shareholder distributions.

Section 4: The Forensic Gap

This brings us to the divergence between the institutional desk and the retail reality.

The gap here exists because institutional analysts and retail income investors are playing two fundamentally different games. UOB Kay Hian is evaluating Beng Kuang Marine as a turnaround to growth story. They are pricing in the successful execution of the BKM 2.0 strategy, the absorption of ASOM’s earnings, and the eventual margin expansion from West African and Guyanese FPSO contracts. It is a valid thesis for an institutional fund with a capital appreciation mandate and a multi year runway.

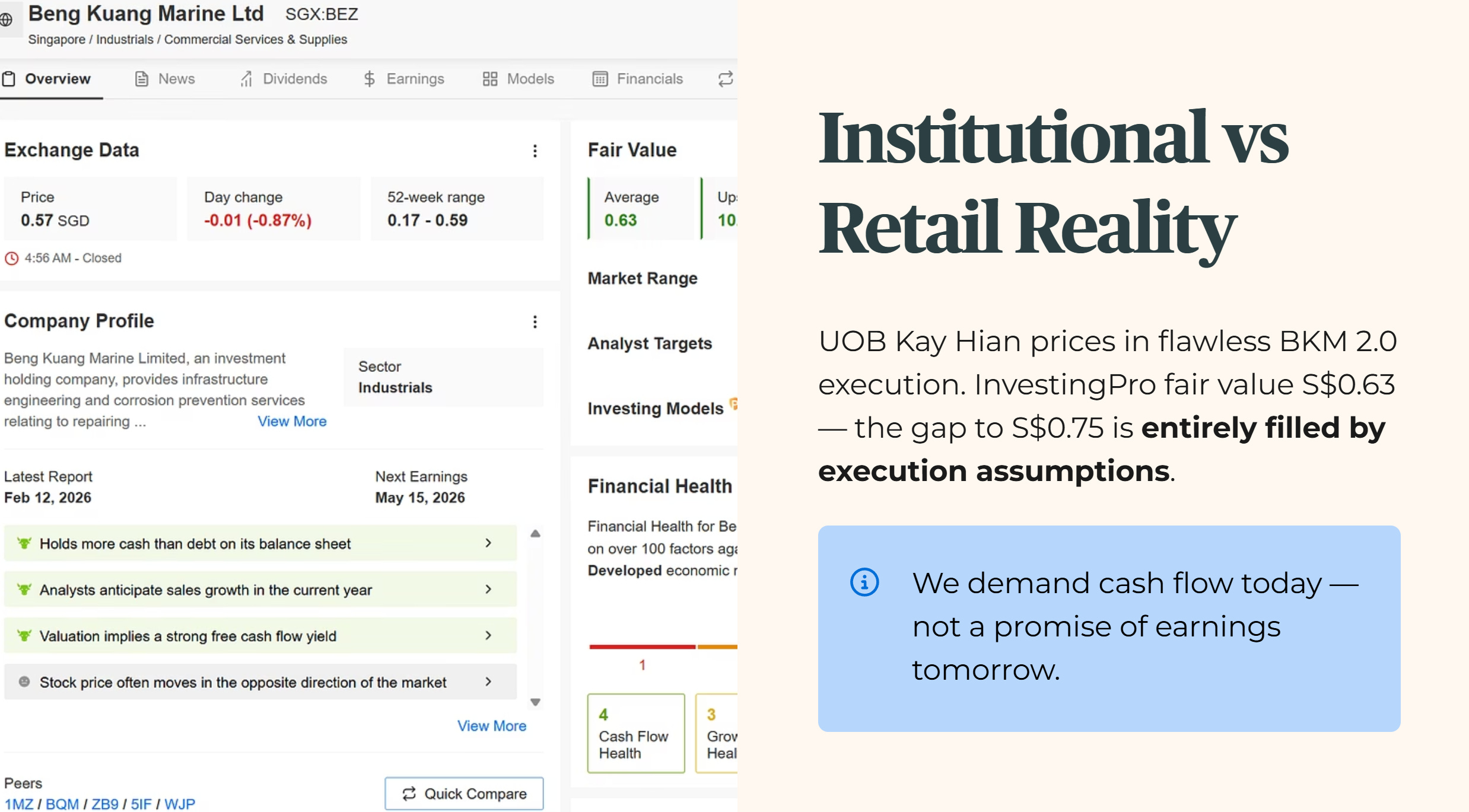

However, our forensic screen is built for capital preservation and immediate income. The InvestingPro fair value sits at S$0.63, suggesting the stock is already trading near its current fundamental limit of S$0.57 before those 2027 earnings actually materialize. We demand cash flow today, not a promise of earnings tomorrow. When your core household expenses like electricity are rising, you cannot pay for them with a target price.

Institutional desks love a compelling turnaround narrative, especially when backed by a net cash position of S$26.9 million. The load-bearing assumption here is flawless execution of the ASOM acquisition by June 2026. If Beng Kuang Marine integrates ASOM seamlessly and secures those S$120 million West Africa renewals, the S$0.75 target is mathematically sound. But if offshore timelines slip, you are holding a 1.0 percent yield in a market where even the risk free T-bill outpaces you. For an income investor, paying a premium for future execution without a dividend safety net is a pure speculation play.

The Analyst’s Desk vs. Iggy’s Forensic Screen

Two legitimate frameworks. Two completely different verdicts. Let me show you exactly where UOB Kay Hian and I part ways — and why neither of us is simply wrong.

Dimension 1: How We Value the Stock

UOB Kay Hian anchors their S$0.75 target to a 14.0x forward P/E on projected 2027 earnings. That is a growth multiple — they are paying today for profits that have not yet been recognised, contingent on the ASOM consolidation closing cleanly and the West Africa FPSO pipeline converting into booked revenue. The ROE justification is compelling on paper: 38.8% against an industry average of 17.3% is genuinely superior capital efficiency if the number holds. The analyst is essentially saying the market is mispricing a high-quality compounder because it cannot yet see the 2027 earnings clearly.

My forensic screen works from a different starting point. InvestingPro’s fair value sits at S$0.63 — built from fundamental models anchored to current verified cash flows, not projected ones. At S$0.57, the stock is not obviously cheap on today’s numbers. The gap between S$0.63 and S$0.75 is entirely filled by execution assumptions. I do not pay a premium for assumptions. I pay for verified cash flow today, with growth as a bonus — not the other way around.

The yield gap between a 1.0% payout and a 4.7% Minimum Yield Hurdle is one thing — but when you stack that 370 basis point shortfall directly against CPF SA and T‑bill rates in the next section, the retirement-grade math stops being a theory and becomes a hard line in your portfolio.