The "Safe" CPF Strategy Killing Your Retirement

We love the safety, but mismanaging the OA-SA split and the “Housing Trap” is costing Singaporeans six figures. Here’s the “boring” strategy that actually works.

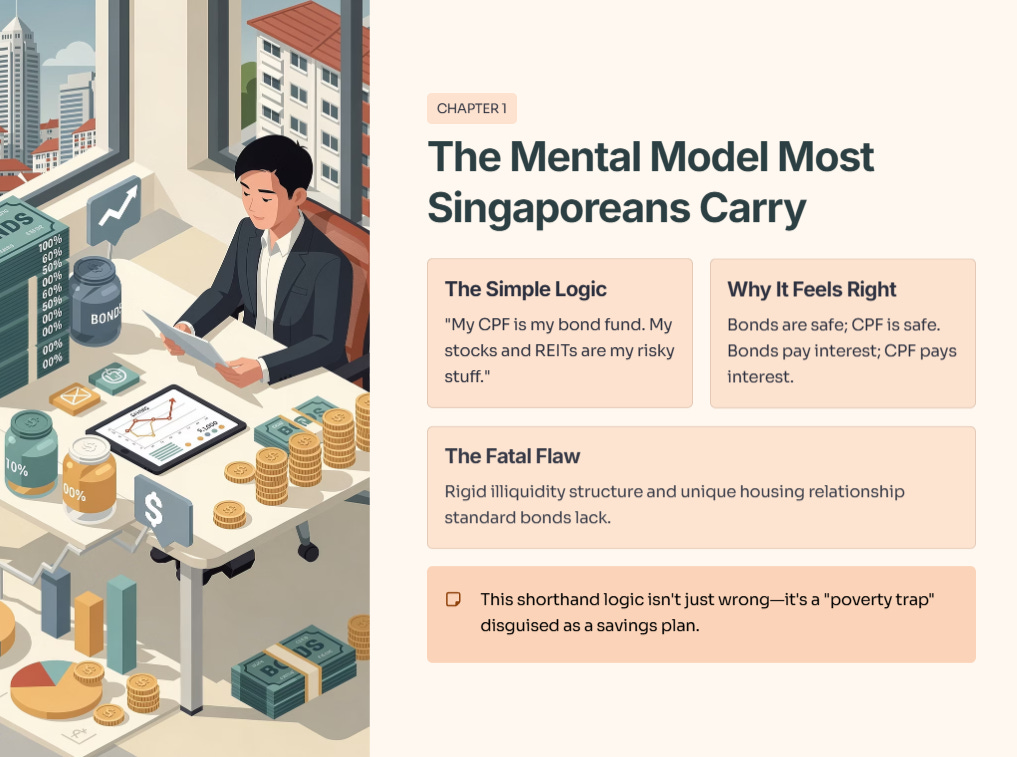

Most Singaporeans carry a simple mental model: “My CPF is my bond fund. My stocks and REITs are my risky stuff.”

It feels intuitive. Bonds are safe; CPF is safe. Bonds pay interest; CPF pays interest. Therefore, if I treat my CPF like the bond portion of my portfolio, I can be aggressive with my cash.

But this shorthand logic is flawed. While CPF shares characteristics with bonds, it has a rigid illiquidity structure and a unique relationship with housing that standard bonds do not. If you misunderstand this, you aren’t just playing it safe—you are locking yourself into a “poverty trap” disguised as a savings plan.

Table of Contents

Who Am I & Why You Should Listen

The "Bond Fund" Illusion: Why It Exists

Where the Model Breaks: The "Housing Trap"

The CPFIS Temptation: Losing Money to "Beat" 2.5%

The "InvestingPro" Data Check: When To Actually Move Money

The Age-Based Playbook: Allocating for "Boring" Success

6.1 The Early Career (Age 30-35)

6.2 The Critical Junction (Age 45)

6.3 The Landing (Age 55)

The "Inflation Illusion" (Why 2.5% is Fine)

Investor's Action Plan

Closing: CPF as Foundation, Not Your Only StrategyWho Am I & Why You Should Listen

If you’re new here, welcome. I’m Iggy, your Singapore-based Private Investor and Market Researcher. Since October 2025, we’ve built a community of over 5,300 investors and produced over 1,300 videos and 400 articles. We are home to a growing ‘Inner Circle’ of over 100 paid members across YouTube and Substack.

Quick Housekeeping: If you want the best value, the YouTube Premium Membership (S$9/mth) bundles these deep-dive articles with the podcast videos. Substack alone is US$6, so the bundle is the ‘smart money’ move. Now, let’s get to the numbers.

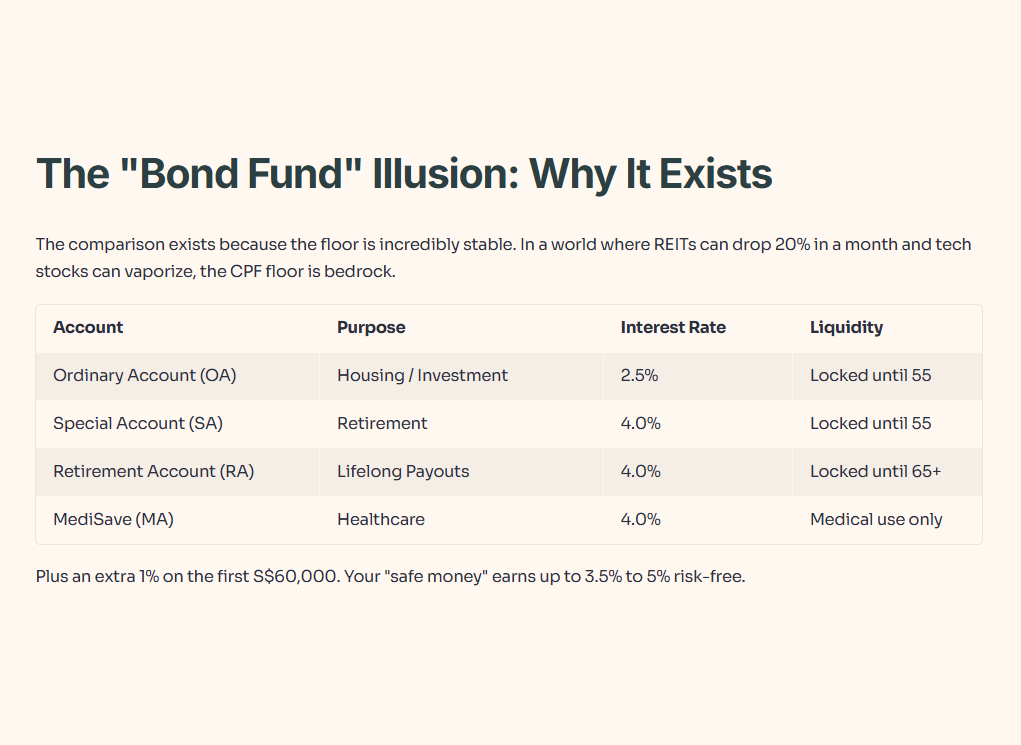

The “Bond Fund” Illusion: Why It Exists

The comparison exists because the floor is incredibly stable. In a world where REITs can drop 20% in a month and tech stocks can vaporize, the CPF floor is bedrock.

Here is the current landscape for Q1 2026:

On top of this, the government adds an extra 1% on the first S$60,000. Effectively, your “safe money” is earning up to 3.5% to 5% (for seniors) risk-free.

Iggy’s Insight:

The “CPF = Bond Fund” analogy works for psychology, but fails for utility. A real bond fund can be sold in 2 days if you have a medical emergency or a business opportunity. CPF cannot. This forced illiquidity is a feature, not a bug—it protects your future self from your present panic.

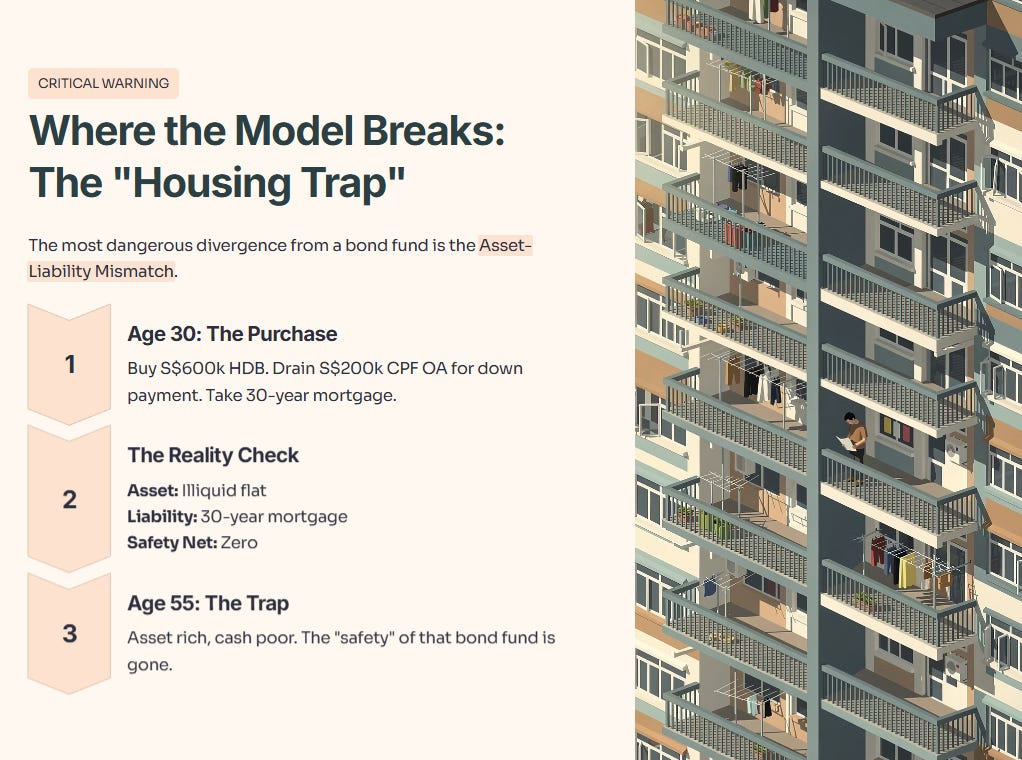

Where the Model Breaks: The “Housing Trap”

The most dangerous divergence from a bond fund is the Asset-Liability Mismatch.

When you buy a bond fund, you don’t usually leverage it to buy a house. But with CPF OA, that is exactly what the system encourages.

The Scenario:

You are 30. You buy a S$600k HDB. You drain your S$200k CPF OA for the down payment and take a mortgage pegged to the OA rate.

Asset: A flat (illiquid).

Liability: A 30-year mortgage.

Safety Net: Zero (because you emptied the OA).

When you turn 55, the “safety” of that bond fund is gone. You are “asset rich, cash poor.” If you had treated CPF strictly as a bond fund (meant for income), you wouldn’t have liquidated it for property.

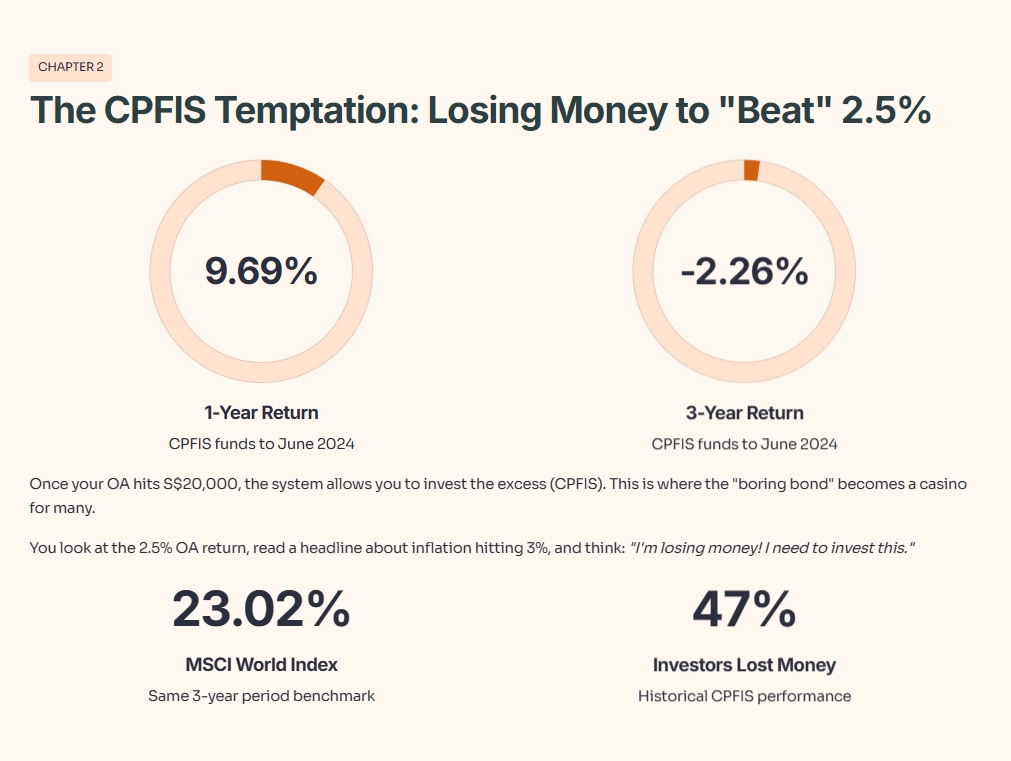

The CPFIS Temptation: Losing Money to “Beat” 2.5%

Once your OA hits S$20,000, the system allows you to invest the excess (CPFIS). This is where the “boring bond” becomes a casino for many.

You look at the 2.5% OA return, read a headline about inflation hitting 3%, and think: “I’m losing money! I need to invest this.”

The Grim Reality of CPFIS Performance:

1-Year Return (to June 2024): CPFIS funds returned ~9.69%. (Looks good).

3-Year Return (to June 2024): CPFIS funds returned -2.26%.

Benchmark: The MSCI World Index returned +23.02% in that same period.

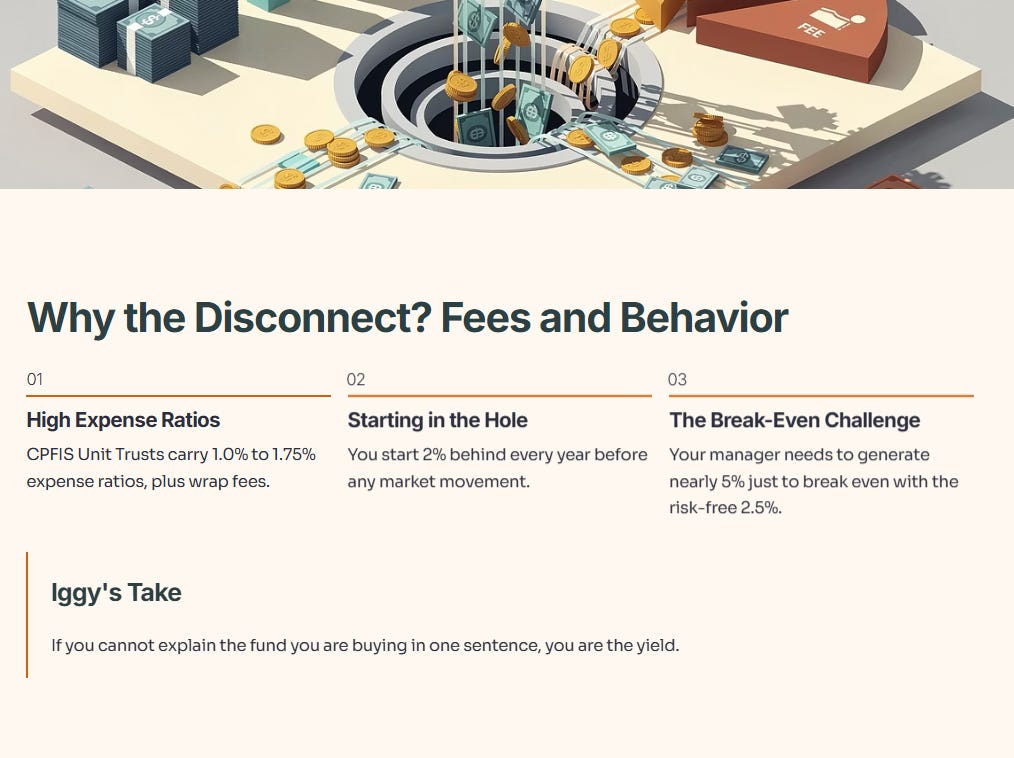

Why the disconnect? Fees and Behavior.

CPFIS Unit Trusts often carry expense ratios of 1.0% to 1.75%, plus wrap fees. You start 2% in the hole every year. To beat the risk-free 2.5%, your manager needs to generate nearly 5% just to break even.

Iggy’s Take:

If you cannot explain the fund you are buying in one sentence, you are the yield. The data shows that 47% of CPFIS investors historically incurred losses. You are paying high fees to take on equity risk, often to end up with returns lower than the guaranteed floor.

The “InvestingPro” Data Check: When To actually Move Money?