Boustead Singapore Analysis: S$154M Gain from REIT IPO Explained

Forensics of a S$154M Windfall: Is the REIT Catalyst Masking a Margin Squeeze in the Engine Room?

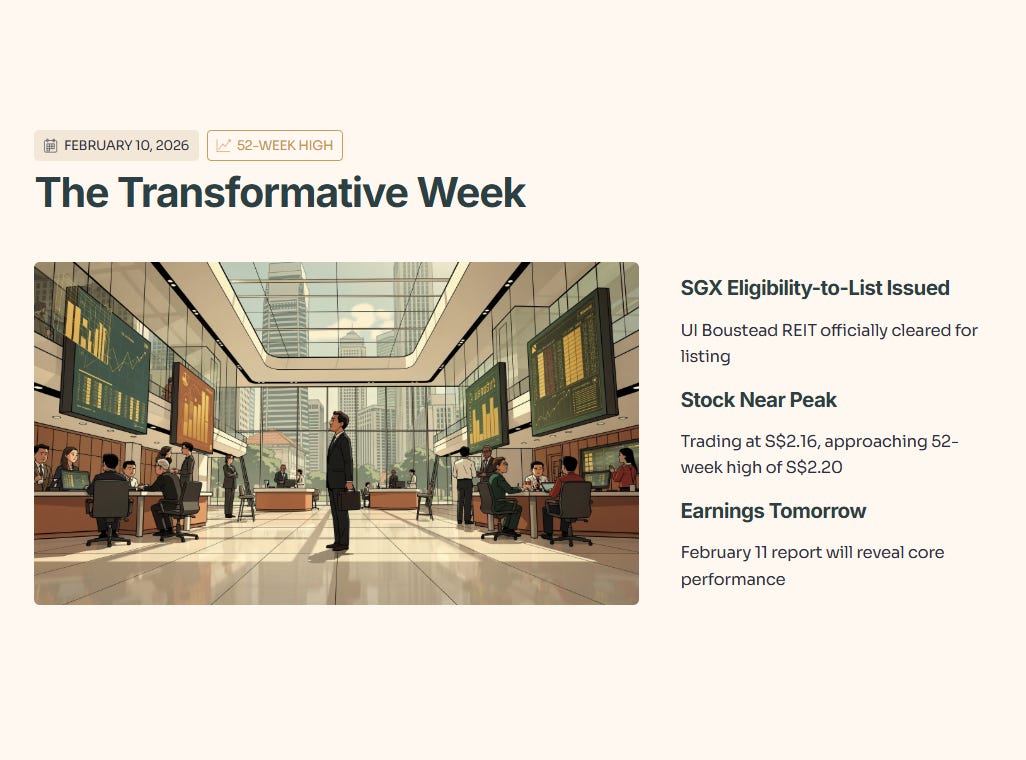

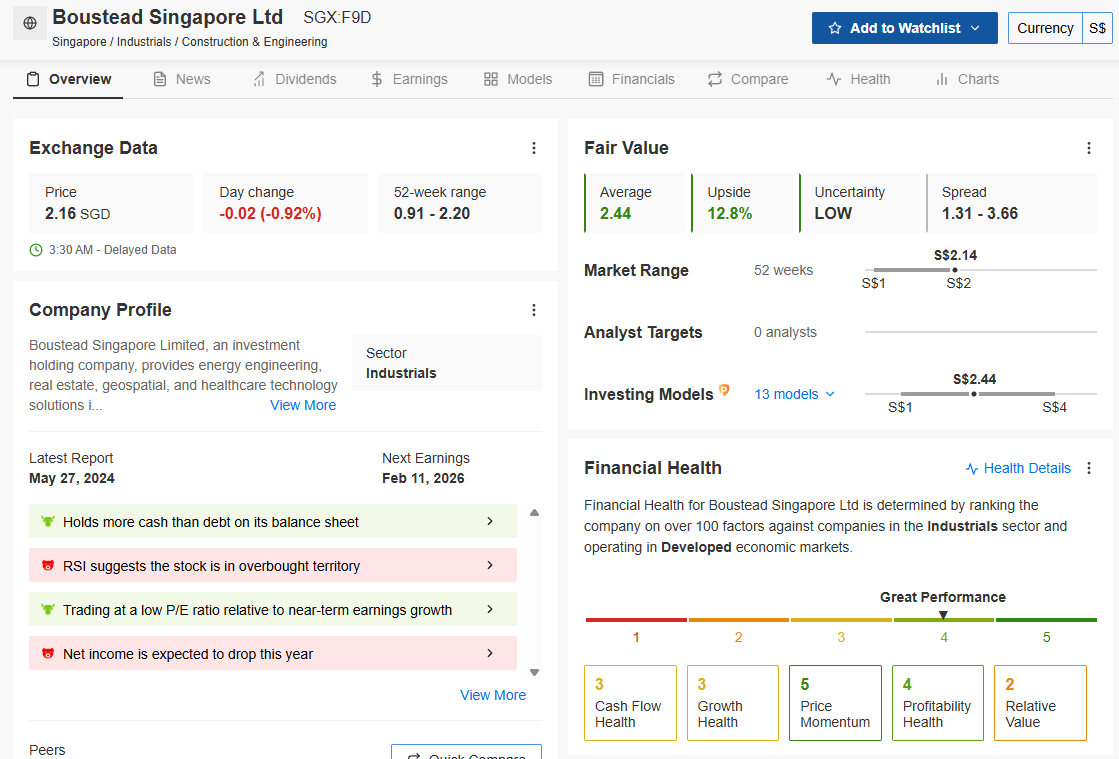

The Singapore market is holding its breath as Boustead Singapore (F9D.SI) enters a transformative week. The headline is significant: SGX has officially issued the “Eligibility-to-List” letter for the UI Boustead REIT as of today, February 10, 2026. With the earnings report due tomorrow, February 11, the stock is hovering near its 52-week high of S$2.20, currently trading at S$2.16.

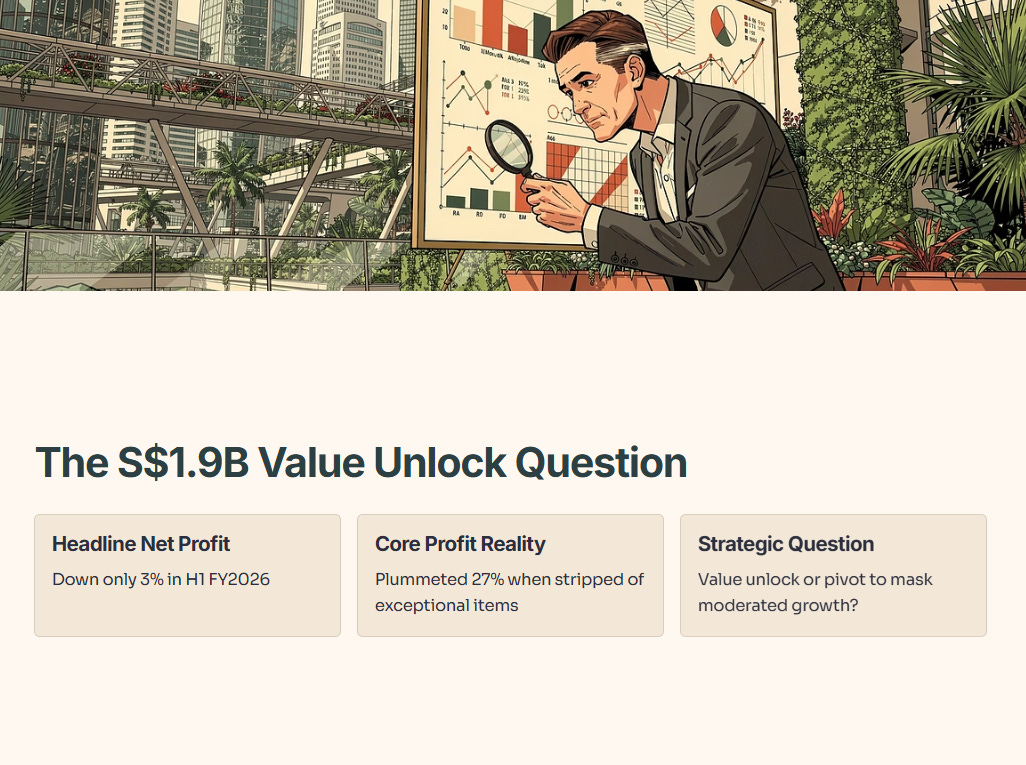

While retail interest is piqued by the S$1.9 billion “Value Unlock,” a forensic look at the H1 FY2026 results reveals a subtle nuance. Headline net profit dipped only 3%, but the adjusted “core” profit—stripped of exceptional items—plummeted 27%. Analytically, one must weigh whether this REIT spin-off represents a structural value unlock or a strategic pivot to mask moderated core growth in the engineering and healthcare segmen

About Iggy & the Elite 150

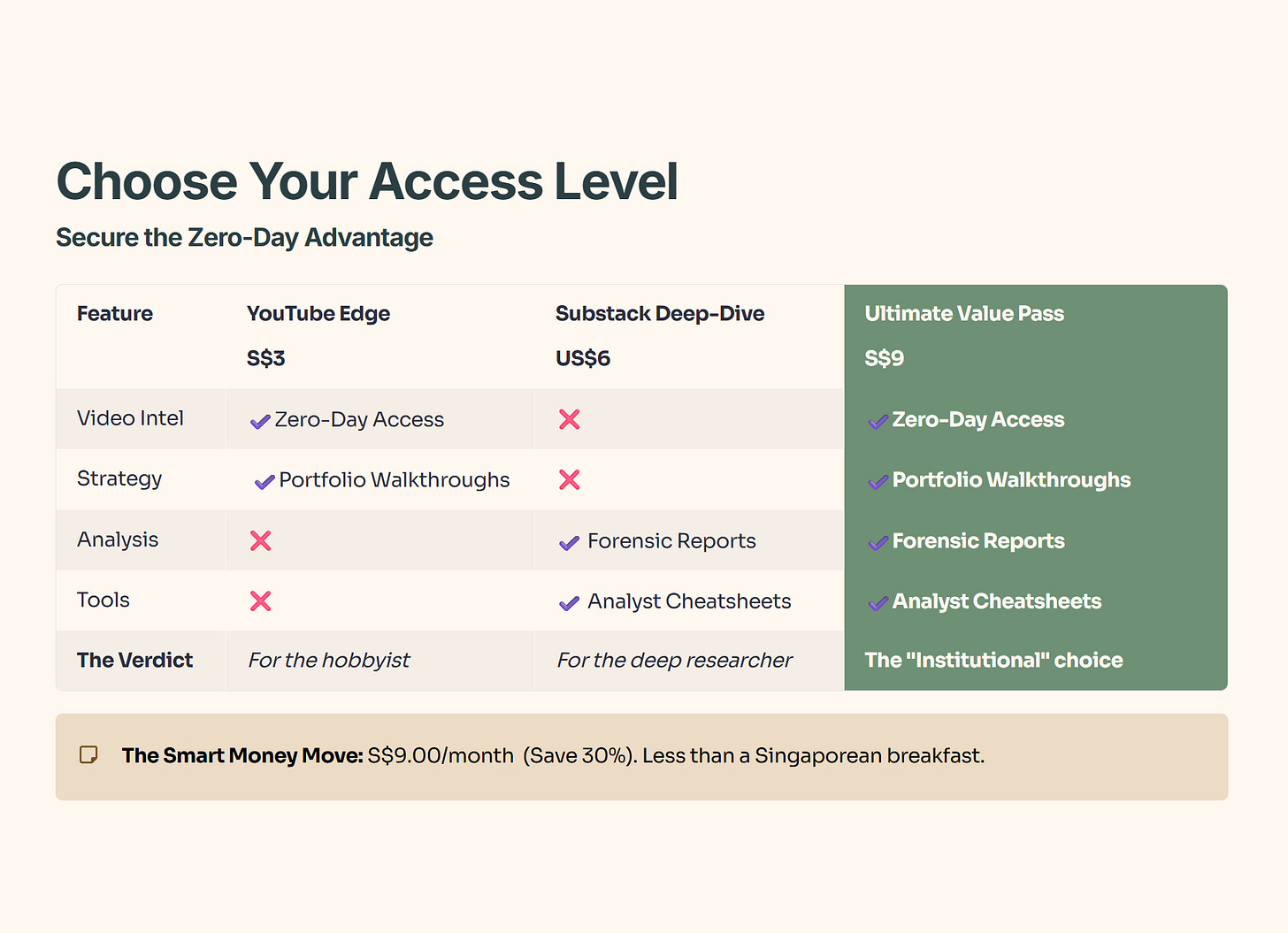

🦎 Join the Inner Circle: Secure Your Zero-Day Advantage

In this market, 48 hours can turn profit into pain. Inner Circle members see my analysis in real time; free readers get it two weeks later.

Choose Your Edge:

⚡ Zero-Day Access: Watch every deep-dive video the second it’s rendered. No delays, no missed entries.

📂 The Forensic Vault: Get the full forensic reports and portfolio walkthroughs where I strip away the corporate hype to reveal the hard math behind every Singapore blue chip.

💎 The “Smart Money” Bundle: Get the full S$9/mo Pass (YouTube + Substack). It’s less than the cost of two coffees at Toast Box to trade with the same data as the pros.

[👉Join 150+ Investors in the Inner Circle Here]

https://www.youtube.com/@InvestingIguana/membership

The Masterclass: Crystallising Value

Before we dive into the numbers, we must understand the strategy at play. Boustead is executing a “Value Unlock” via a REIT spin-off.

🎓 Educational Note: Crystallising Value

In finance, “crystallising” occurs when a company moves an asset from its balance sheet (often recorded at historical cost) and sells it into a new vehicle (like a REIT) at current market value. This turns “paper wealth” into “cash wealth,” allowing the parent company to potentially distribute special dividends while retaining a management fee stream.

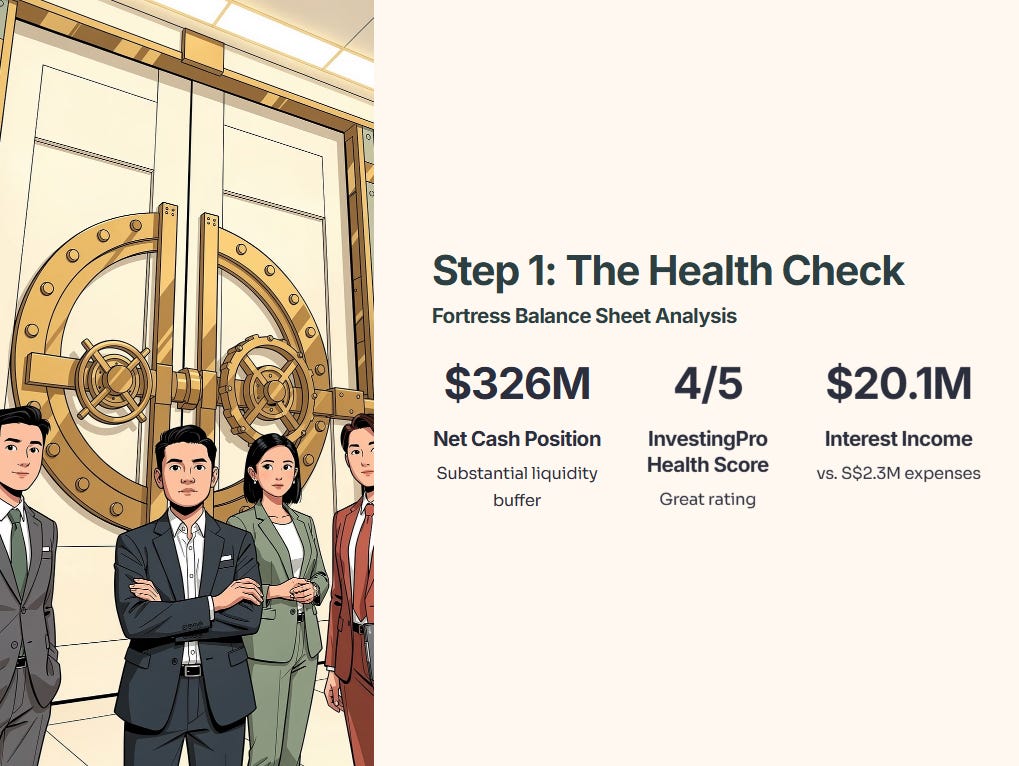

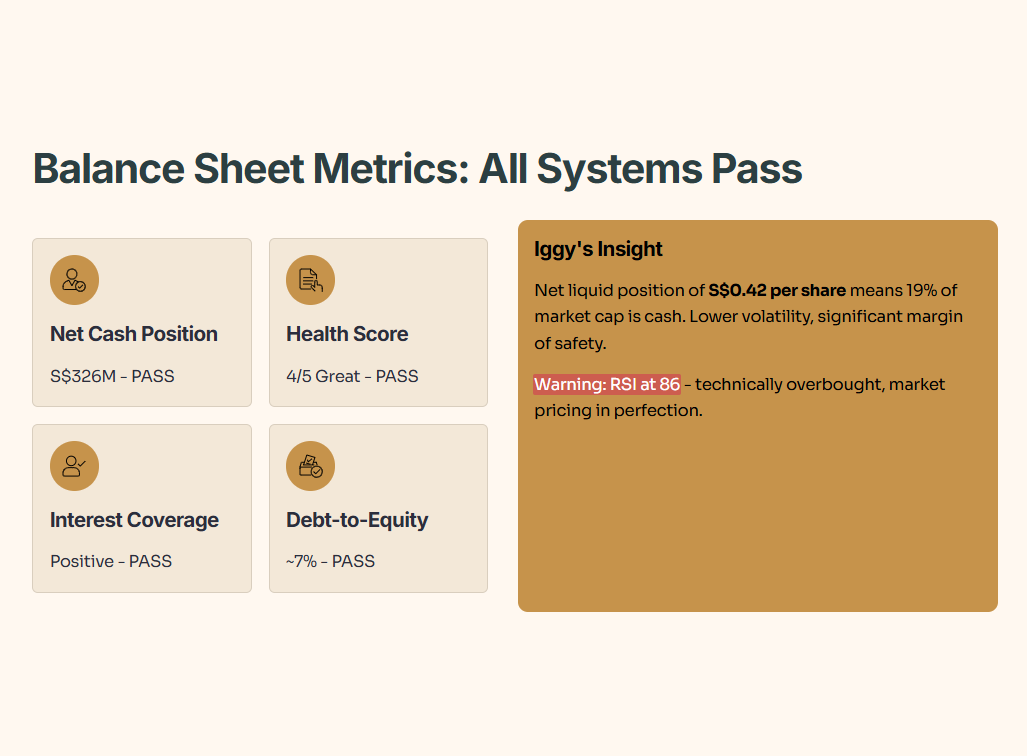

Step 1: The Health Check (Balance Sheet & Net Debt)

The Narrative: “Before we look at the dividend, can they pay their bills?”

In the case of Boustead, the answer is backed by a substantial cash reserve. The data shows a “Fortress Balance Sheet” with a net cash position of approximately S$326 million. Their interest income (S$20.1m) vastly exceeds their finance expenses (S$2.3m), meaning they are effectively a net beneficiary of the current interest rate environment.

🦎 Iggy’s Insight: A net liquid position of S$0.42 per share means that at a price of S$2.16, roughly 19% of the company’s market cap is represented by cash and equivalents. From a risk-mitigation perspective, this capital structure historically correlates with lower volatility, providing a significant margin of safety against project delays. However, observe the RSI (currently 86)—the stock is in technically overbought territory, suggesting the market may be pricing in perfection ahead of tomorrow’s earnings.

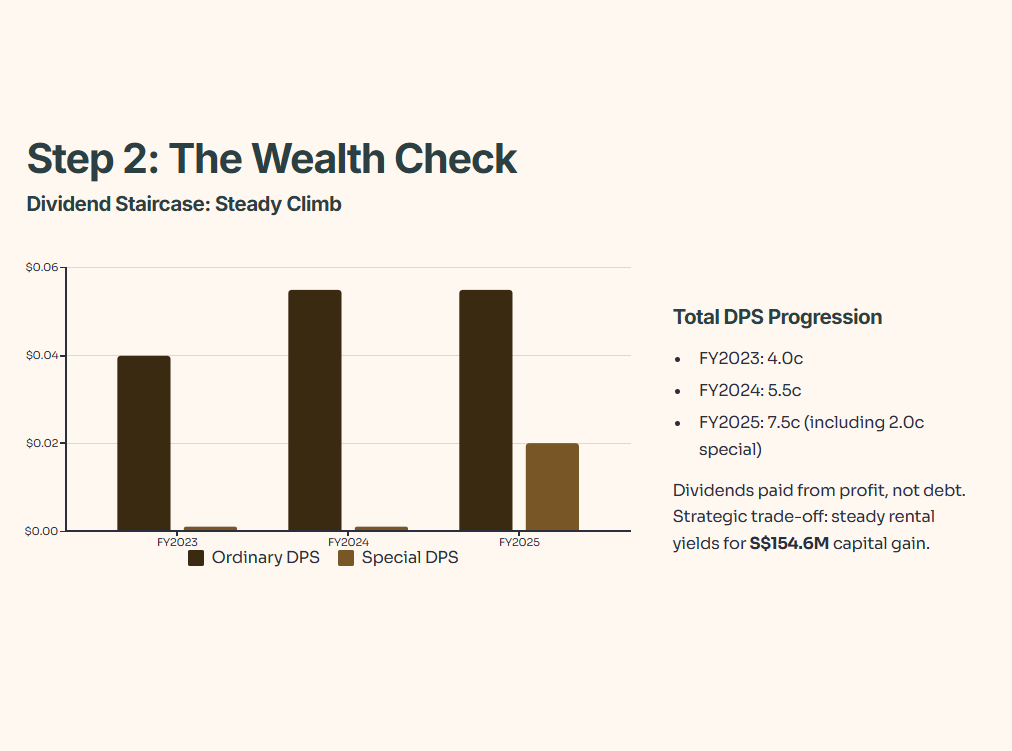

Step 2: The Wealth Check (Dividends & Cash Flow)

The Narrative: “Are they paying us from profit or debt?”

Boustead has demonstrated a “Dividend Staircase,” increasing from 4.0c to 7.5c over the last two fiscal years.

🦎 Iggy’s Insight: An expected dip in core net income is a common mathematical artifact when a company divests recurring rental assets to seed a REIT. The strategic trade-off involves exchanging steady rental yields for a one-off S$154.6 million capital gain and the potential for subsequent special distributions.

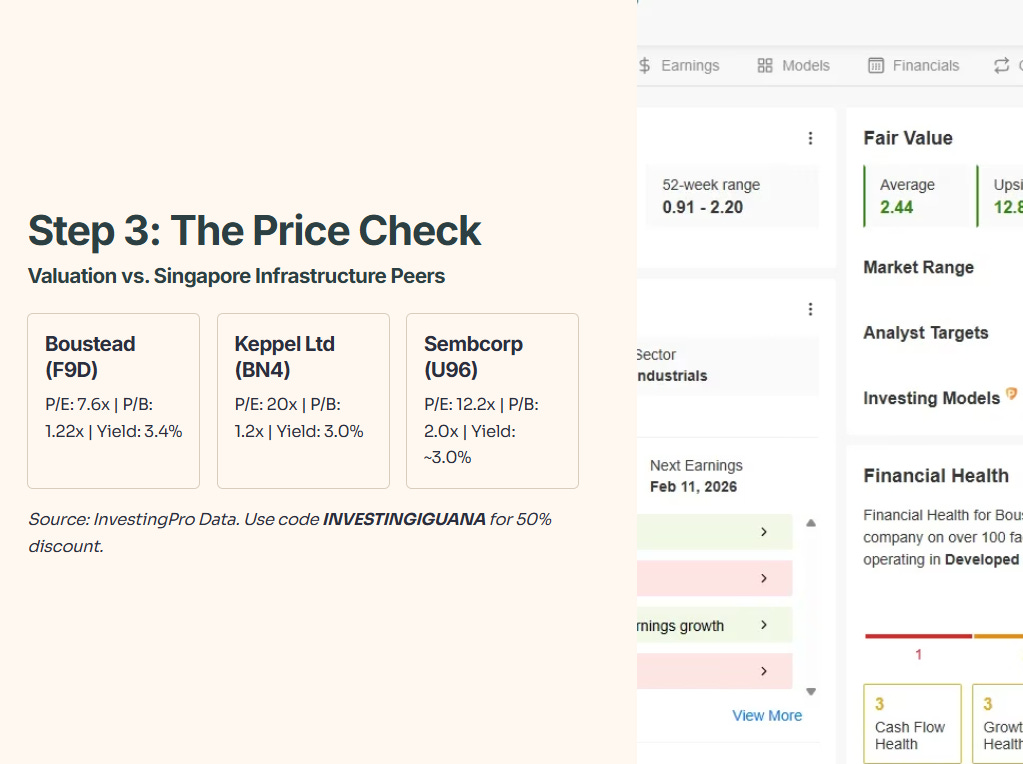

Step 3: The Price Check (Valuation & Peers)

The Narrative: “Is it at a discount, or is the pricing justified?”

Boustead’s valuation metrics remain distinct when compared to larger Singapore infrastructure peers.

“I don’t just guess at valuations. I check the institutional models.”Source: InvestingPro Data. Unlock these institutional tools for your own portfolio: Use code INVESTINGIGUANA for an exclusive 50% Discount. 🏛️

[Claim Your 50% Discount Here]

The “What-If” Test (Risk & Upside Scenarios)

Before we look at the REIT IPO details, let’s run two quick scenarios. Think of this as stress-testing the investment thesis.

Scenario A: The REIT Surprises to the Upside

What happens if the REIT IPO crushes expectations? If property valuations jump ten percent above current estimates, the cash windfall for Boustead balloons. That extra cash could trigger a massive special dividend. The stock could re-rate higher and break through the next psychological resistance level. The market loves surprises like this.

Scenario B: Engineering Margins Get Squeezed

Now flip the script. What if core engineering profit drops another ten percent? Even in that worst-case scenario, the fortress balance sheet acts as a cushion. With forty-two cents of cash per share, the downside risk is mathematically limited. Historical support sits around the one dollar and ninety cent range. Below that price, value hunters will pile in. The cash-in-hand becomes too tempting to ignore.

The Key Takeaway: Boustead’s high cash levels provide a margin of safety. Most other engineering stocks don’t have this cushion. The downside is protected. The upside has multiple catalysts.

“Now that we’ve boxed the downside and mapped the upside, the only question left is this: what specific REIT IPO numbers will decide whether Boustead’s S$154.6m ‘windfall’ becomes a real re-rating catalyst—or just a headline?”