BRC Asia - 3 Good and 3 Red Flags You Need to Know

Curious how BRC Asia is cashing in on Singapore’s construction frenzy? Discover why their mega-project wins could mean bigger growth—and better dividends—for your portfolio.

Editor’s Note: This post has been updated on October 19, 2025. We’ve streamlined the analysis for a faster, more direct read and expanded our ‘Iggy’s Take’ to include a deeper look at BRC Asia’s strategic move into Malaysia—a key update for our SG and MY-based readers.

BRC Asia (SGX:BEC) stands at the center of Singapore’s construction revival. With a dominant market position, the company is translating a surge in government-led infrastructure projects—from the landmark Changi Terminal 5 to a robust HDB housing pipeline—into a multi-year earnings runway.

For income-focused investors, BRC presents a compelling case: it’s a direct play on Singapore’s domestic growth, offers a steady dividend, and is eligible for CPF/SRS portfolios. But is this stability worth the risk from steel price volatility and heavy project concentration? We break down the 3 Good and 3 Red Flags.

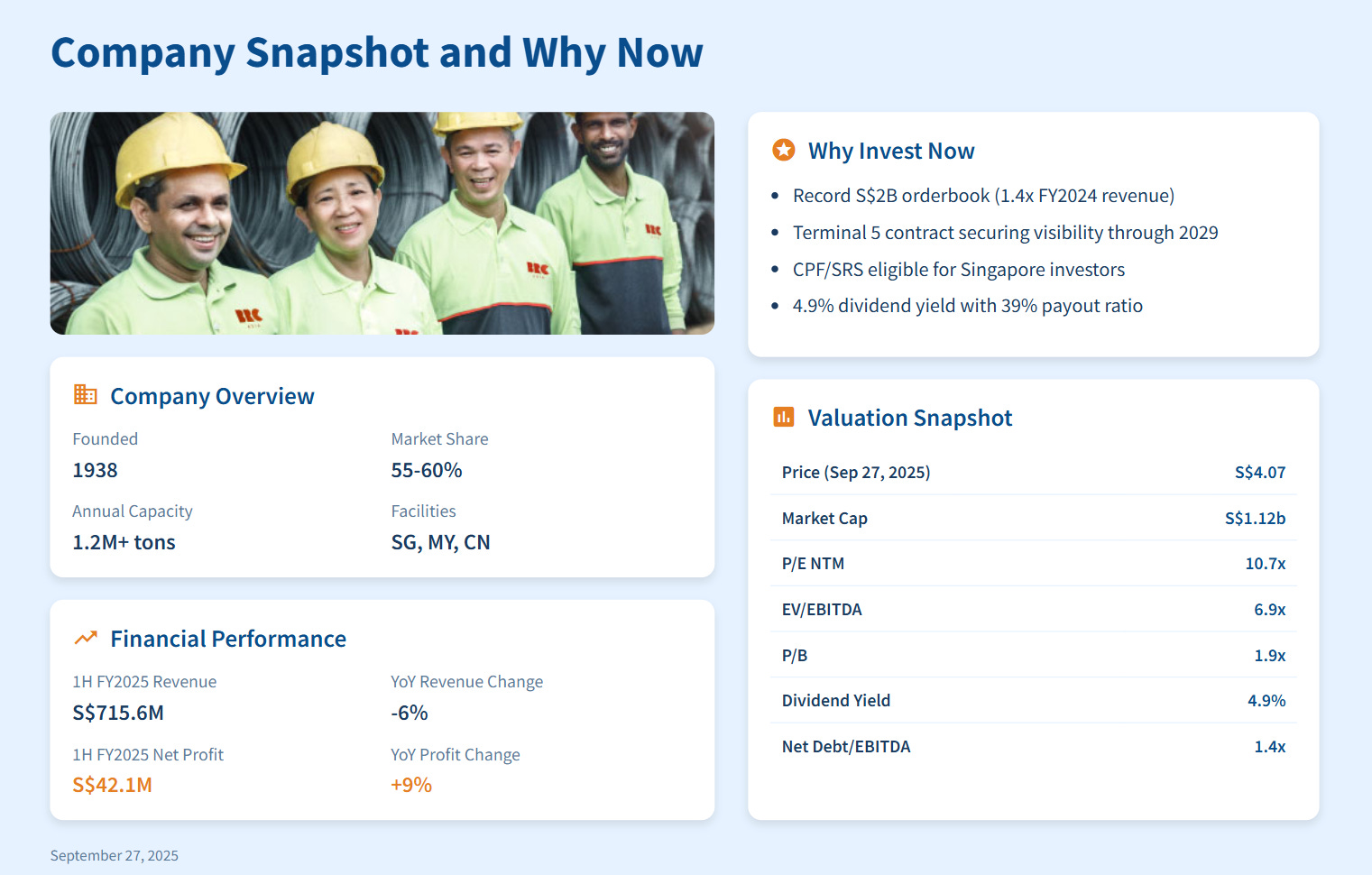

Company Snapshot & The Core Thesis

BRC Asia Limited (SGX:BEC) is Singapore’s leading steel reinforcement provider, controlling 55-60% of the market. It fabricates prefabricated steel for everything from HDB flats to commercial towers and major infrastructure.

The investment thesis rests on three core pillars:

Unprecedented Orderbook: As of July 2025, its orderbook hit a record S$2 billion, driven by the landmark S$570 million Changi Terminal 5 contract. This provides clear earnings visibility through 2029, a rarity for the sector.

Local Market Exposure: The company is a direct beneficiary of Singapore’s construction pipeline, fueled by robust HDB demand and other major infrastructure projects.

Investor-Friendly Profile: For local investors, the stock is CPF/SRS eligible and currently offers a 4.9% dividend yield (at a conservative 39% payout ratio), blending domestic growth with steady income.

While 1H FY2025 revenue dipped 6% to S$715.6 million (due to lower steel prices), net profit *rose* 9% to S$42.1 million, highlighting strong operational efficiency and a focus on profitability.

Table: Valuation and income snapshot (Current)

Caption: This valuation shows BRC’s moderate premium over sector lows, justified by backlog depth and visible income. Yield and manageable debt support its case for steady returns in volatile times.

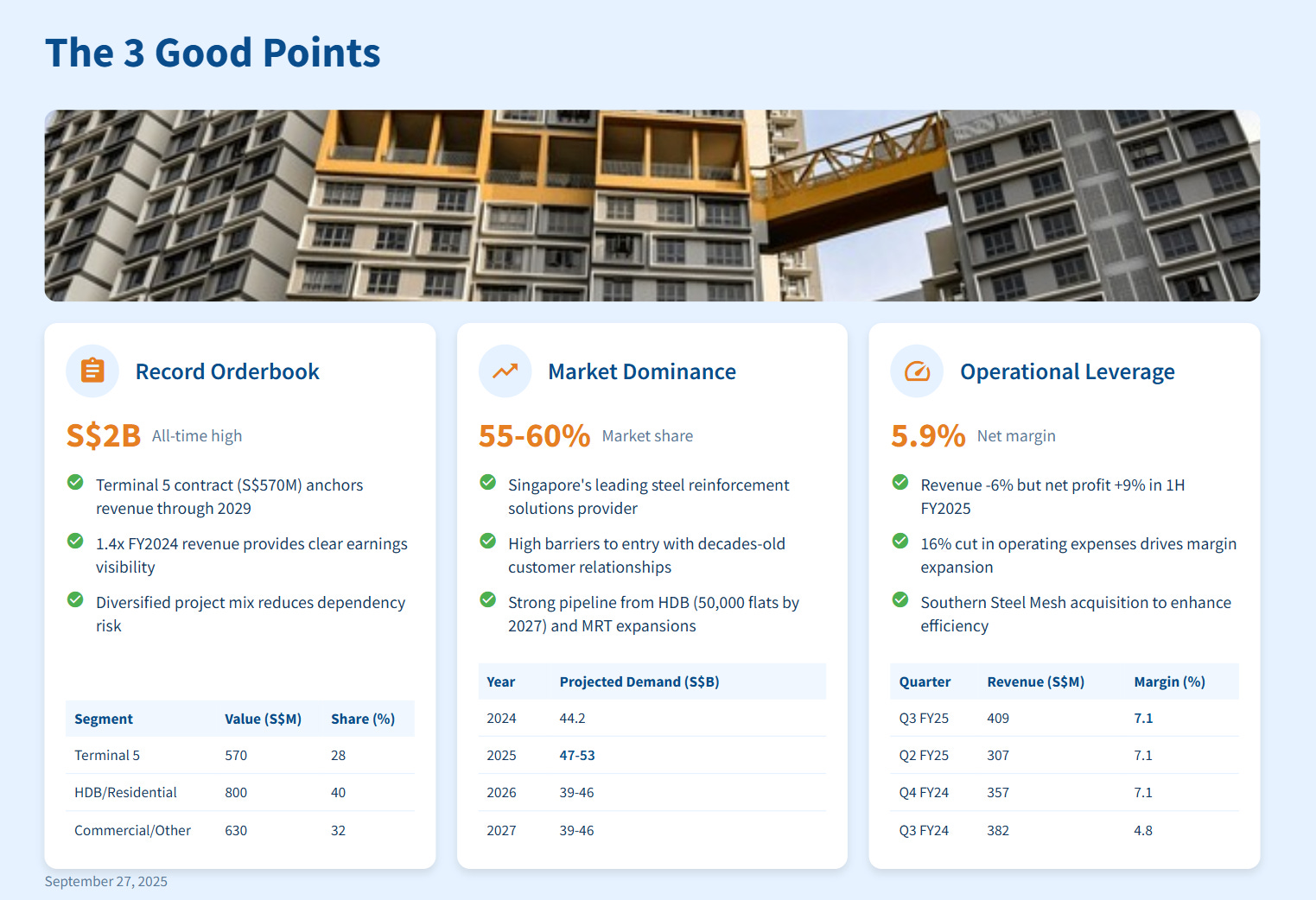

The 3 Good

Good #1: Record orderbook provides unprecedented earnings visibility

BRC’s S$2 billion orderbook as of July 2025 marks an all-time high, driven mainly by the S$570 million Changi Terminal 5 contract—comprising 28% of backlog. This level provides clear revenue float through 2029 and insulates earnings from short-term project shocks, a rarity in a cyclical sector.

Terminal 5, Singapore’s largest aviation build, runs to the mid-2030s and ensures multi-year revenue. The rest of the orderbook mixes HDB flats, commercial towers, and infra projects. Diversity here provides recurring streams, lessening single-project dependency.

Quick tip: Track orderbook renewals and completions every quarter to watch for sustainability beyond Terminal 5.

Good #2: Dominant market position in resilient Singapore construction

Owning 55–60% of the steel reinforcement market, BRC’s scale generates pricing power, sticky client relationships, and high margins relative to commodity traders. Barriers to entry are high, and decades-old customer and regulatory ties shore up BRC’s lead.

Singapore’s construction spend is forecast to remain strong through 2029, driven by HDB (50,000 flats by 2027), MRT expansions, and major infrastructure renewal. BRC’s capacity (over 1.2 million metric tons per year) means it can meet large demand shifts without major cost or delays.

Quick tip: Track BCA construction forecasts and HDB announcement schedules—they give advance signals of BRC’s next wave of orders.

Good #3: Operational leverage driving margin expansion

Despite revenue slipping 6% in 1H FY2025, net profit rose 9%, supported by a 16% cut in operating expenses and reduced financing and FX costs. The company’s net margin expanded to 5.9%. Q3 FY2025 results highlight robust volume growth (about 22%) even as steel prices declined 14%, with gross margins rebounding to 11%.

This efficiency focus is now extending into its regional operations. The recent acquisition of a 55% stake in Malaysia’s Southern Steel Mesh (August 2025) is a key strategic move.

Iggy’s Take (For our MY Investors): This acquisition is a significant headline. It’s not just about “machine efficiency”; it’s BRC’s first major step to build a secondary growth engine outside of the mature Singapore market.

For our Malaysian readers, this gives BRC a solid foothold in the local construction market, which has its own tailwinds (e.g., RTS Link, major industrial parks). More importantly, it offers BRC a new, lower-cost production base and a way to diversify its revenue away from 100% reliance on Singapore government contracts.

Quick tip: Watch how gross margins move relative to steel price—this signals if BRC can keep outpacing cost inflation.

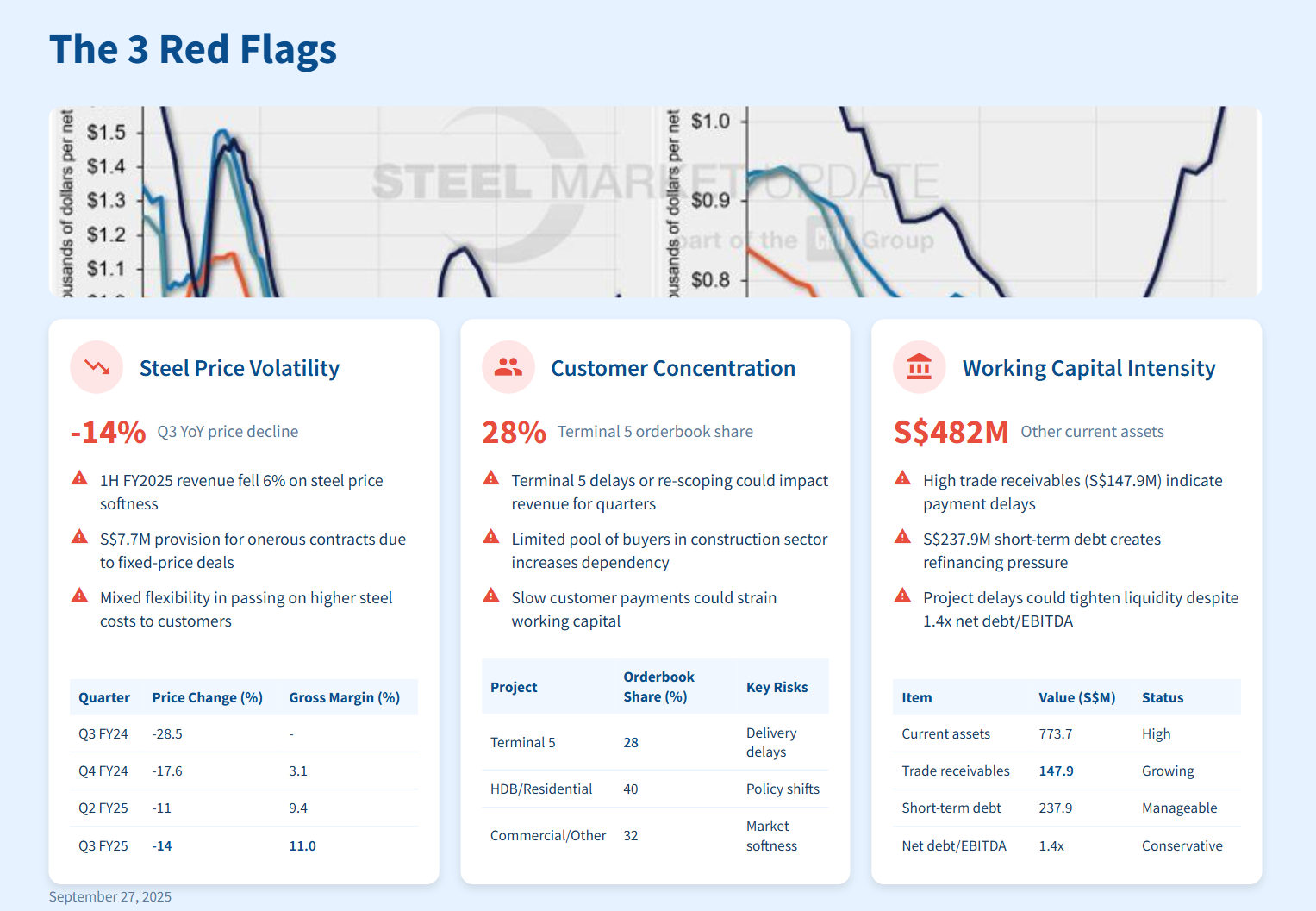

The 3 Red Flags

Red flag #1: Steel price volatility compresses margins during downturns

Despite stable volumes, BRC’s revenues are vulnerable—1H FY2025 revenue fell 6% on steel price softness, while Q3 saw 14% price drops. Margins narrowed, with gross profit margin slipping to 9.4%. A S$7.7 million provision for onerous contracts reflects the risk of long-term fixed-price projects during unpredictable commodity swings.

Contractual flexibility in passing on higher steel costs is mixed; fixed-price deals expose BRC during inflationary periods.

Quick tip: Keep an eye on steel futures and quarterly margin guides for signs of risk or resilience.

Red flag #2: High customer concentration increases project execution risk

Terminal 5 accounts for 28% of the current orderbook—a valuable anchor but also a source of concentration risk. If this mega-project is delayed or re-scoped, it can hit revenue and cash flows for several quarters. The construction sector’s limited pool of buyers further heightens dependency.

Slow customer payments or problems with a major developer could strain working capital. BRC’s strong share grants pricing power but limits local growth, forcing close watch on project diversity.

Quick tip: Watch orderbook changes for customer mix and updates on Terminal 5 execution milestones.

Red flag #3: Working capital intensity during growth phases

BRC’s balance sheet supports growth, but rising working capital needs create risk. Current assets reach S$773.7 million (S$482 million other current assets). High trade receivables (S$147.9 million) and S$237.9 million short-term debt point to dependence on smooth customer payments.

Net debt/EBITDA is a conservative 1.4x, but any uptick in project delays, payment lags, or sector slowdown could tighten liquidity.

Quick tip: Monitor trade receivables, short-term borrowings, and free cash versus orderbook growth each quarter.

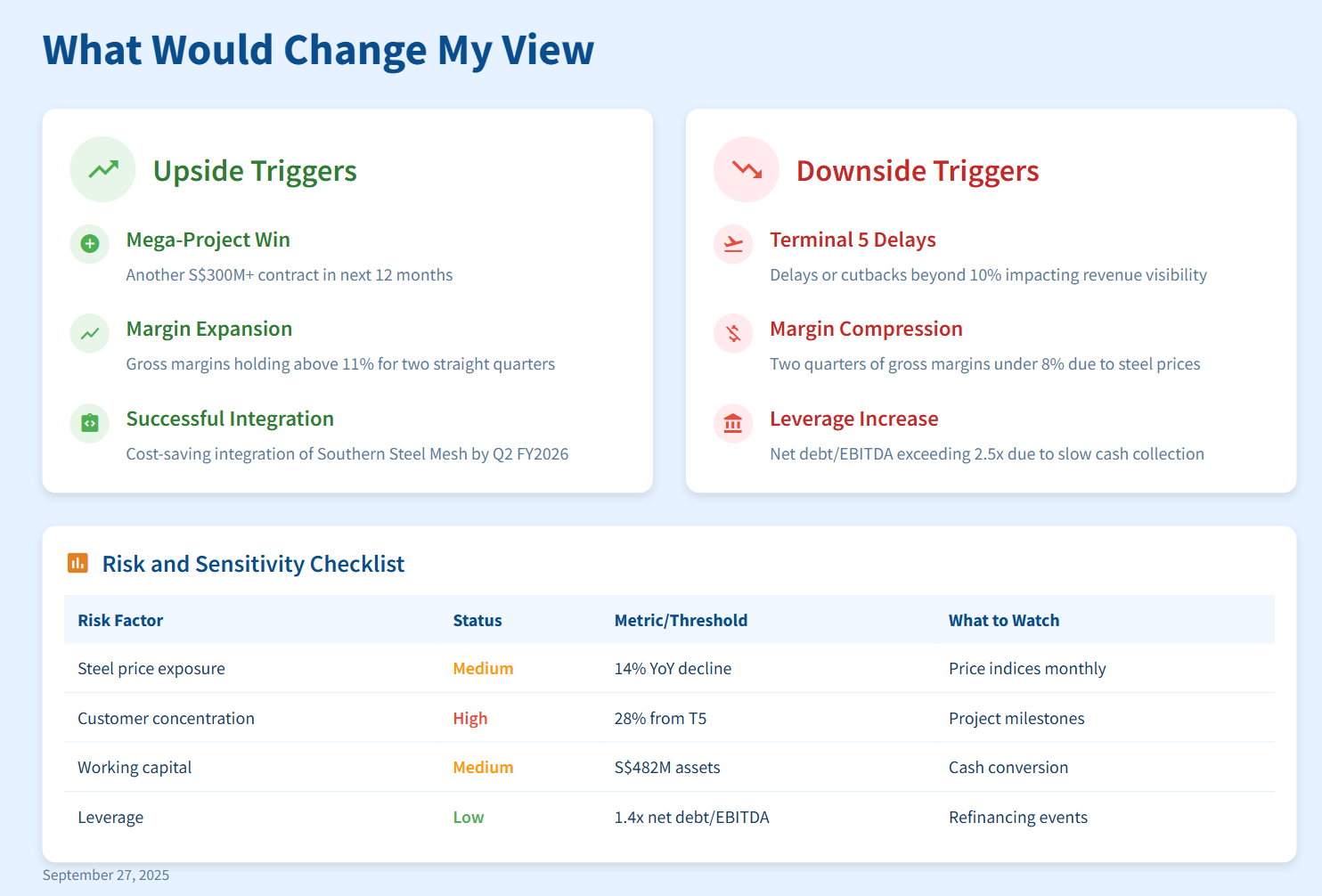

What would change my view (upside/downside triggers)

Upside triggers: Winning another S$300 million-plus mega-project in the next 12 months, gross margins holding above 11% for two straight quarters, or smooth, cost-saving integration of Southern Steel Mesh by Q2 FY2026.

Downside triggers: Terminal 5 delays or cutbacks beyond 10%, two quarters of gross margins under 8%, or net debt/EBITDA exceeding 2.5x on the back of slow cash collection or project setbacks.

Iggy’s verdict and positioning (non-advisory)