Broadcom Analysis: Goldman Sees $435. My Model Says $321

Why the “AI Arms Dealer” just got a $435 price target, and what it means for your SRS portfolio.

Broadcom isn’t sexy. It doesn’t have a leather-jacket-wearing CEO like Nvidia, and it doesn’t capture headlines like Tesla. But while everyone was watching the AI hype train, Broadcom quietly became the tracks it runs on. If you are holding this in your SRS or cash portfolio, you might be asking: Is the recent dip a buying opportunity, or is the China tariff risk too high?

If you’re new here, welcome. I’m Iggy, your Singapore-based market analyst. Since October 2025, we’ve produced over 1,300 videos and 400 articles with 1.1 million watch hours. We are also home to a growing community of over 60 YouTube Premium subscribers and 30 paid Substack members.

Quick Housekeeping: If you want the best value, the YouTube Premium Membership (S$9/mth) bundles these deep-dive articles with the podcast videos. Substack alone is US$6, so the bundle is the ‘smart money’ move. Now, let’s get to the numbers.

In This Article:

• The Goldman Sachs “Bull Case”: Why $435?

• The “Custom Silicon” Moat: The Google-Meta Deal

• InvestingPro Reality Check

• The Dividend: Is it Safe?

• The “Bear Case”: The Tariff Trap

• Summary: The “Smart Money” Move?

The Goldman Sachs “Bull Case”: Why $435?

In December 2025, Goldman Sachs raised their price target on Broadcom to $435 (and subsequently adjusted to $450 in some notes). This isn’t just a random number; it’s a statement.

Most retail investors think of Broadcom as a “boring dividend stock” or just “the company that bought VMWare.” Institutional analysts, however, see something else: The AI “Arms Dealer.”

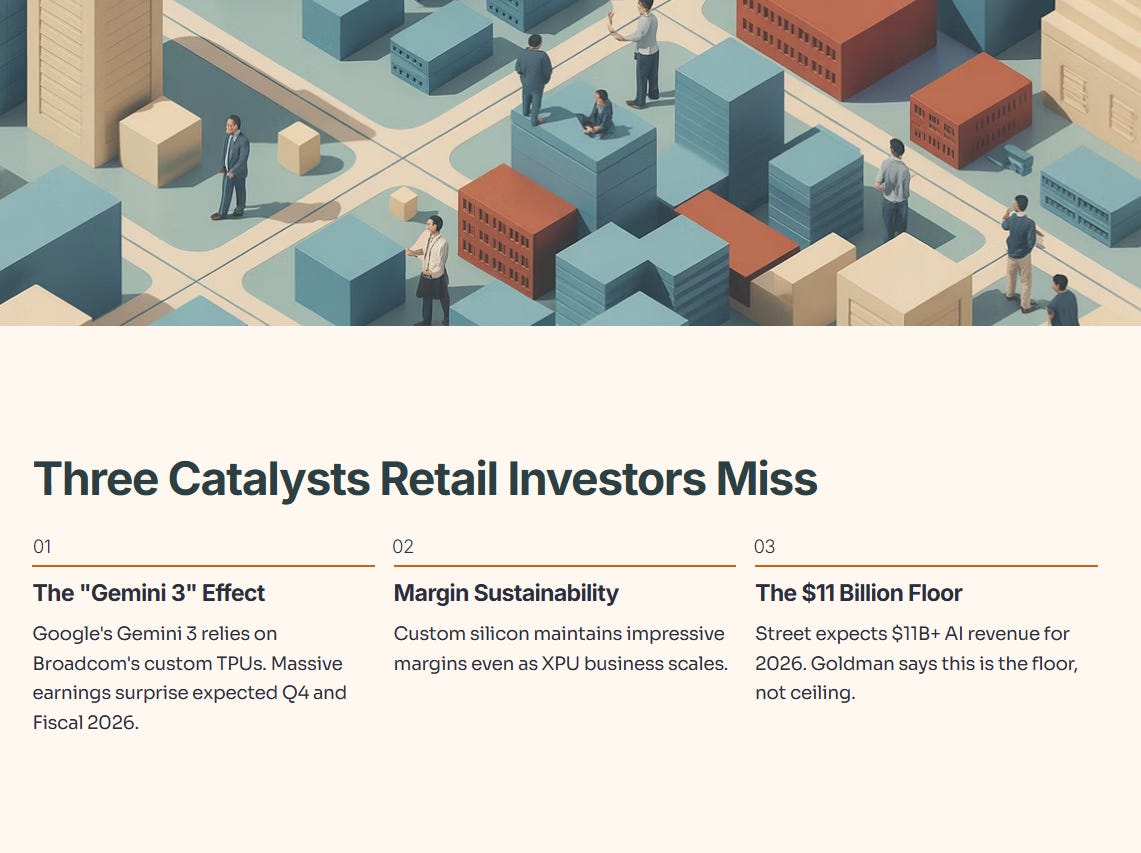

Goldman’s bullishness hinges on three specific catalysts that most retail investors are missing:

The “Gemini 3” Effect: Google’s recent launch of Gemini 3 relies heavily on Broadcom’s custom TPUs (Tensor Processing Units). Goldman expects this to drive a massive earnings surprise in Q4 and Fiscal 2026.

Margin Sustainability: There was fear that custom silicon (making chips for others) would have lower margins than selling off-the-shelf chips. Goldman’s data suggests Broadcom has maintained “impressive margins” even as its custom XPU business scales.

The $11 Billion Floor: The street is expecting $11 billion+ in AI revenue for 2026. Goldman argues this is the floor, not the ceiling, especially given the new deals with OpenAI and Meta.

Iggy’s Take:

The market loves Nvidia for the possibility of growth. But institutions love Broadcom for the predictability of it. You aren’t betting on a single AI model winning (like betting on ChatGPT vs. Claude); you are betting on the infrastructure that all of them need. In a Singaporean context, this is like owning the land the kopitiam sits on, rather than running the stall.

[...End of Free Section...]

🔒 The Deep Dive Continues Below...

You’ve seen the Bull Case, but is Broadcom actually safe to buy at these levels?

Keep reading to unlock:

The “Moat” Map: Exactly how the Google & Meta deals protect Broadcom’s margins.

The Valuation Check: We use the institutional models to see if the stock is Cheap, Fair, or Expensive right now.

The Dividend Verdict: Is the payout safe after the massive VMWare debt?

Iggy’s Action Plan: Specific buy zones portfolio.