Is Your Cash Flow Safe After Budget 2026? (CPF & Inflation Data Review)

The government is sandbagging your fortress, but who's paying for the sand?

The Singapore Budget 2026 marks a structural shift in how the nation manages its wealth. Framed as a post-GE pivot, it signals a move toward a “smaller but smarter” fiscal cushion. The government is trimming the surplus to approximately S$8.5 billion, a sharp drop from the previous year. This isn’t a retreat; it’s a deliberate deployment of capital to address the “Three Pillars”: easing the cost of living, supporting an aging population, and accelerating AI-driven growth.

For the Singaporean investor, the most visceral shift is the “Silver Tilt.” The state is shifting from “hoarding” to “shielding”—spending now to prevent a social crisis later as the demographic “silver tsunami” finally hits.

💡 Iggy’s Insight: Don’t view the falling surplus as a leak; view it as Defensive Capex. If the state doesn’t “sandbag” the social floor now, the silver tsunami will eventually erode the floor of our GDP and, by extension, your property valuations. We are paying for the “System Upgrade” today to avoid a “System Crash” tomorrow.

In This Article:

The Local Impact: Your Wallet vs. The “Silver Tsunami”

The Data Proof: Hard Stats for the 50+ Investor

The “Silver Economy” Cheat Sheet

Sector Watch: Winners, Squeezes, and Traps

The Strategic Landscape: Scenarios for your SRS & CPF

4. The Actionable “Hard Math”: Stop Being a Liquidity Provider

The Bottom Line

InvestingPro Reality Check

Iggy's VerdictAbout Iggy & the Elite 150

🦎 Join the Inner Circle: Optimize Your Informational Latency: In the Singapore market, the gap between a calculated entry and becoming a liquidity provider for others is often just 48 hours. While 5,800+ readers wait two weeks for the “Old News” version, my Inner Circle observes the data while the market structure is still evolving.

🚨 Mitigate Informational Lag: Free subscribers wait 14 days to see my analysis. In this jungle, informational asymmetry is a primary driver of portfolio variance. Access the data while the market dynamics are still being priced in.

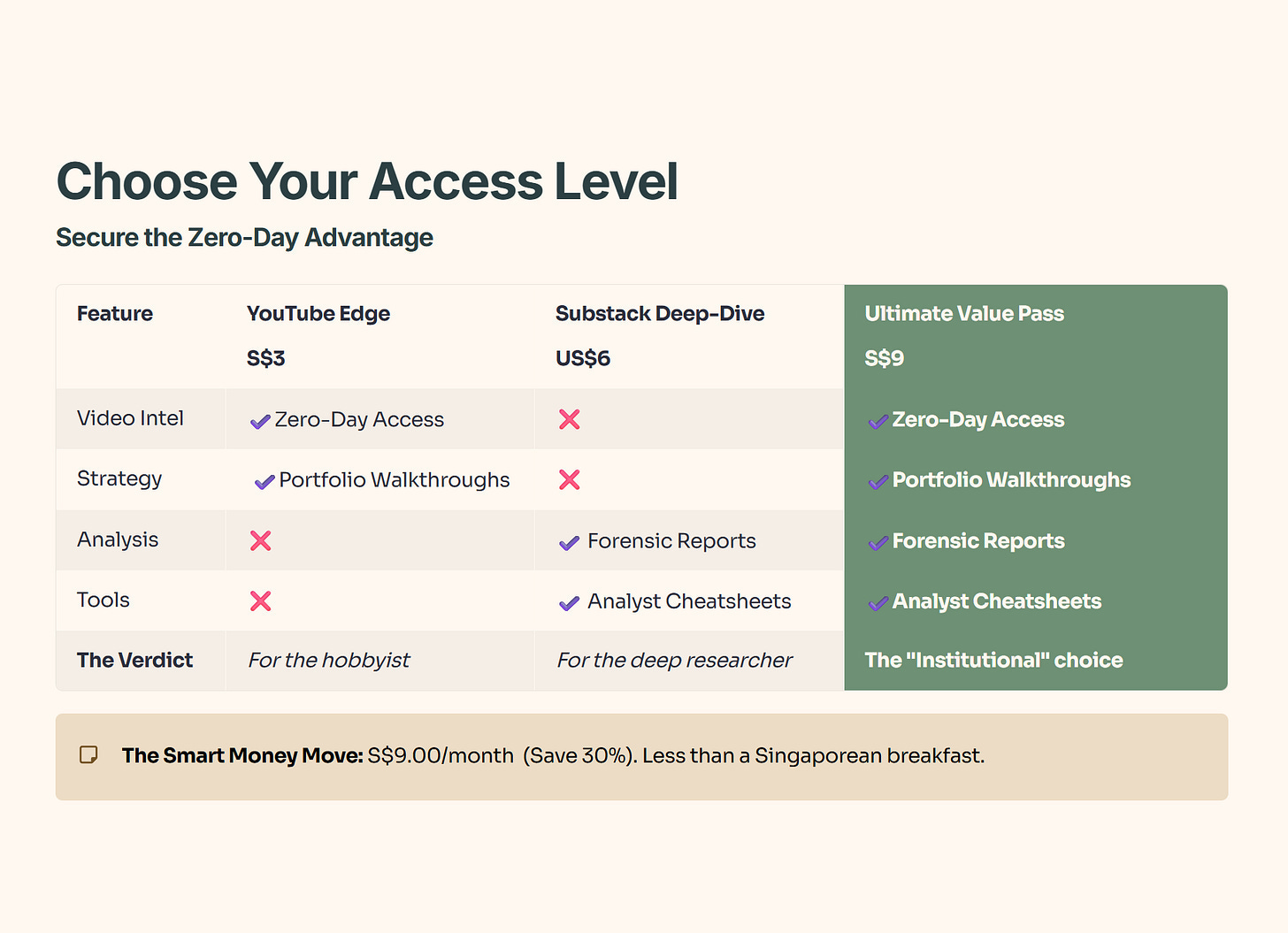

Choose Your Edge:

⚡ Zero-Day Access: Observe every deep-dive video the second it’s rendered. No delays, no missed data points.

📂 The Forensic Vault: Access the full forensic reports and portfolio walkthroughs where I strip away the corporate hype to reveal the hard math behind every Singapore blue chip.

💎 The “Smart Money” Bundle: Secure the full S$9/mo Pass (YouTube + Substack).

It’s a nominal overhead—less than the cost of two coffees at Toast Box—to analyze the market with the same datasets as institutional participants.

Get the data while it’s fresh. 👉 Join the Inner Circle Here

The Local Impact: Your Wallet vs. The “Silver Tsunami”

If you are aged 50 and above, Budget 2026 is a capital injection into your future self, though it may feel like a liquidity squeeze today. The headline move is a one-time CPF top-up of up to S$1,500 in late 2026 for those born in 1976 or earlier. However, this is tightly tiered—if you are “asset rich” in a high-value property, you might see very little.

The real “Kitchen Table” impact hits in 2027, when CPF contribution rates for older workers rise again. For those aged 55 to 60, the jump bolsters your retirement “fortress” but reduces your immediate take-home pay. Simultaneously, core inflation is projected to bounce back to the 1.0–2.0% range in 2026.

💡 Iggy’s Insight: This budget is a “sandbagging” exercise. The CDC vouchers and cash support are short-term bandages. The government is warning you: inflation is bottoming out. They are giving you vouchers for groceries today because they know your electricity and transport bills are likely to stay sticky.

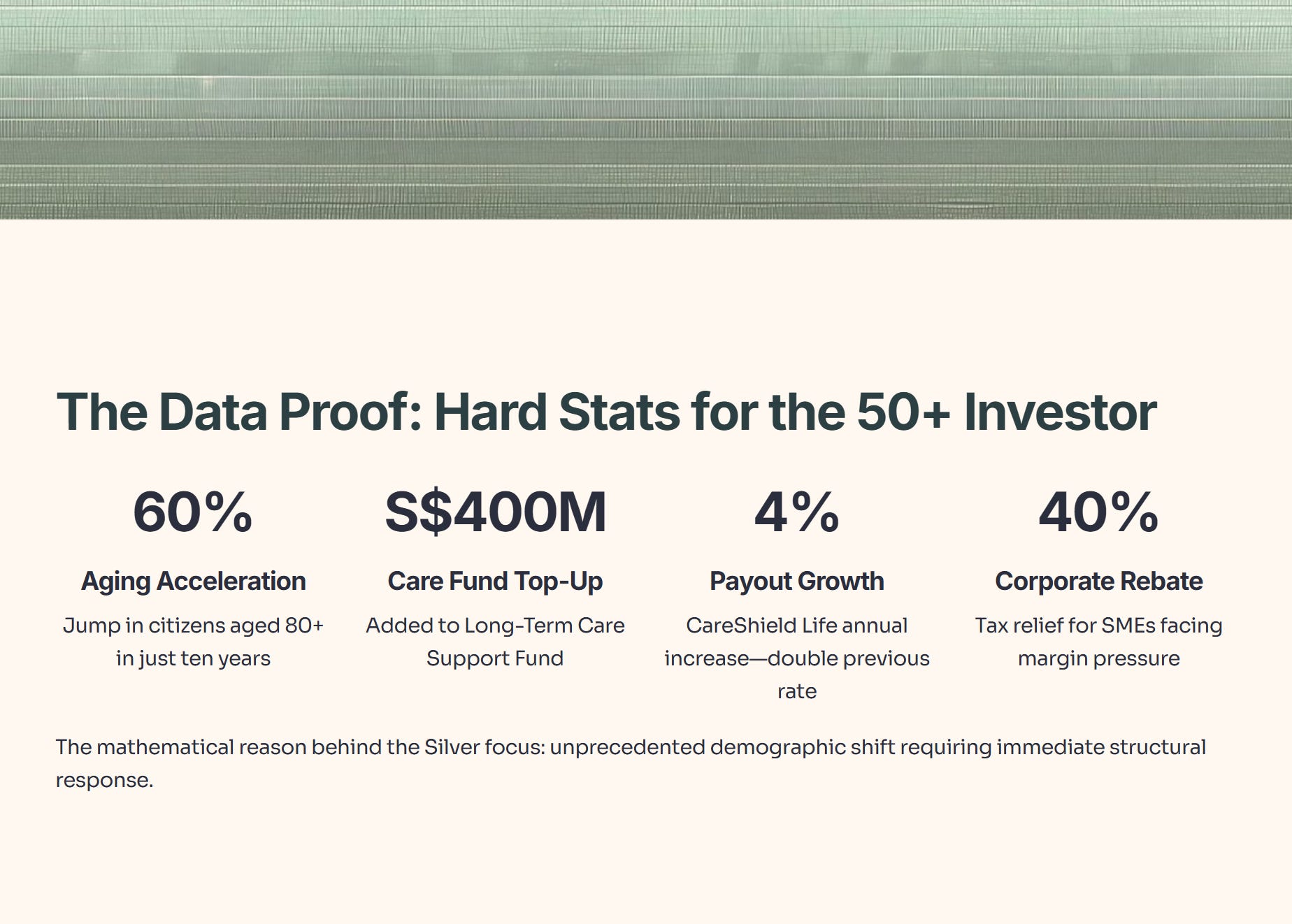

The Data Proof: Hard Stats for the 50+ Investor

The data reveals why the “Silver” demographic is the priority. The speed of aging in Singapore is staggering: the number of citizens aged 80 and above has jumped by a massive 60% in just ten years. This is the mathematical reason behind the S$400 million top-up to the Long-Term Care Support Fund. CareShield Life payouts are now set to grow at 4% per year, double the previous rate, to keep pace with rising nursing home and medical costs.

For those tracking corporate health, the 40% corporate tax rebate is a lifeline for SMEs, but it is also a signal of the margin pressure they face from rising wage floors and higher CPF costs.

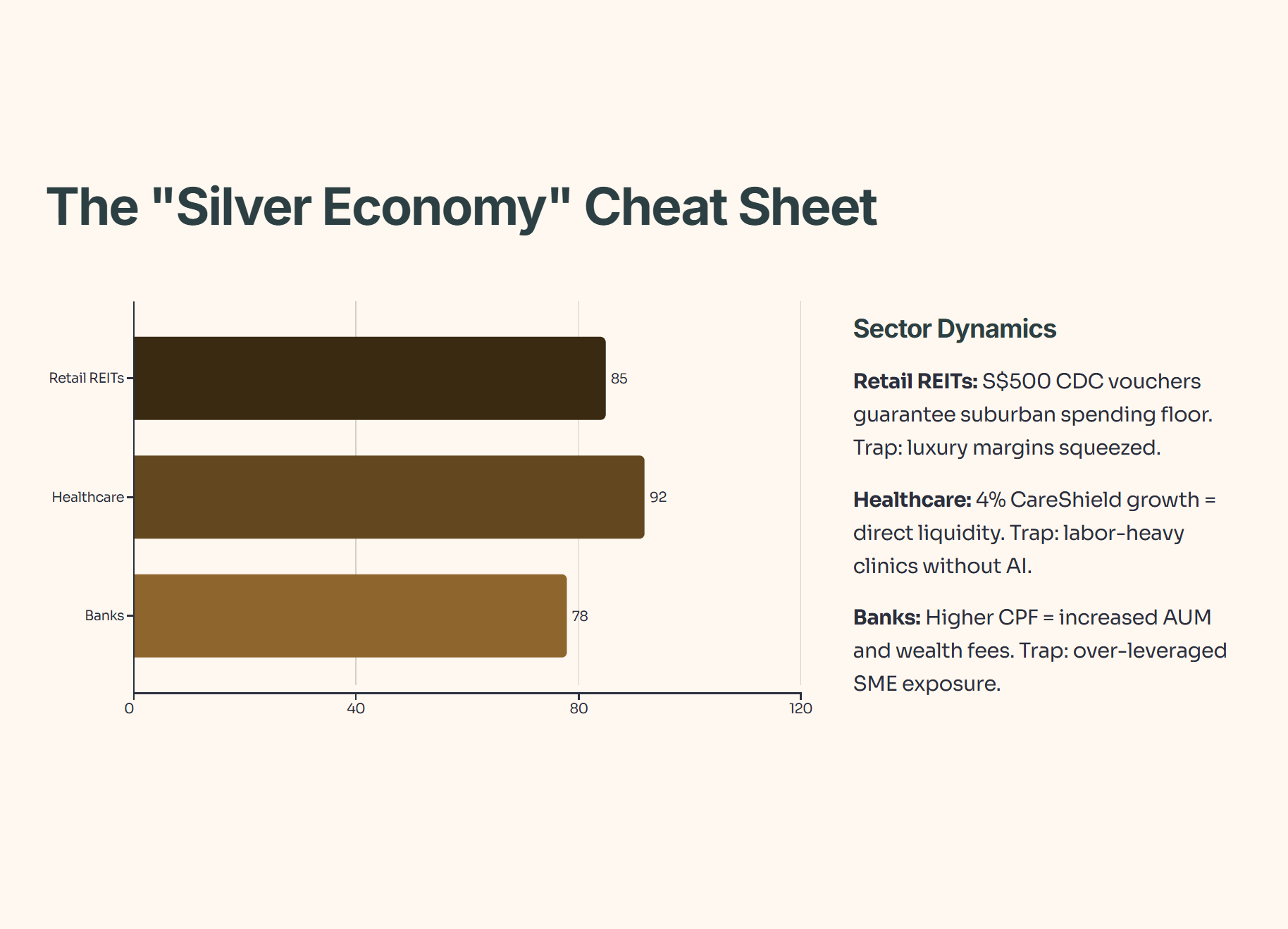

The “Silver Economy” Cheat Sheet

The “Silver Economy” Cheat Sheet breaks down the structural winners and the margin traps that most retail investors will miss until it’s priced in. Healthcare is the clear alpha play with a 92/100 conviction score, fueled by the state’s decision to hike CareShield payouts by 4% annually—effectively injecting direct liquidity into the sector. Retail REITs (Score: 85) are your defensive play; the S$500 CDC vouchers act as a government-subsidized “revenue floor” for heartland malls, while Orchard Road luxury faces a “margin squeeze” as the silver demographic pivots to value. Meanwhile, Banks (Score: 78) will harvest higher fees from the CPF contribution hike, but the “trap” lies in their exposure to SMEs that are currently being choked by rising labor levies.

💡 Iggy’s Insight: In this jungle, you either hunt the yield or become the liquidity for someone else’s exit—position yourself where the state is mandate-spending, not where the corporate hype is.

“Below, I break down the exact ‘Short Game’ portfolio structure I use to hit that 4-6% yield target—including the three Singapore REITs and dividend plays the institutions are quietly accumulating.”