Can Keppel DC REIT Keep Rising After a 55% Income Jump? (Analysis of Q3 2025 Update)

Iggy's Take: After a massive Q3, is KDC REIT a 'Buy' or 'Hold' for your CPF & SRS portfolio?

When a REIT boosts its distributable income by 55 percent in one year, investors naturally wonder: is this sustainable, or just a lucky break?

Every quarter, Singaporean investors wrestle with the same questions about data centre REITs. Are these AI-fueled growth stories real? Can these trusts keep paying higher dividends when interest rates stay unpredictable? Most importantly, should you add more units to your CPF or SRS portfolio right now?

I’m Iggy, host of The Investing Iguana channel and Substack. For years, I’ve tracked Singapore REITs with a focus on finding solid income plays for everyday investors like you and me. My analysis combines detailed financial breakdowns with real-world context so you can make smarter decisions with your hard-earned savings.

Today, we’re diving deep into Keppel DC REIT’s third quarter 2025 operational update. This report landed on October 24, and it reveals some fascinating moves: a massive preferential offering, portfolio reshuffling, and aggressive expansion into hyperscale assets. I’ll break down what the numbers actually mean and give you my honest take on whether this REIT deserves a spot in your portfolio.

Let’s get started.

In This Article:

• The Headline: A 55.5% Income Jump (Is It Real?)

• The Strategy: Doubling Down on Hyperscale & AI

• The Foundation: A Fortress Balance Sheet

• The Assets: Locked-in, Blue-Chip Income

• Iggy’s Assessment: Hold with Positive Outlook

• The Good

• The Challenges

• The Verdict: Hold

• Key Risks to Monitor

• Why This Matters for CPF and SRS Investors

• Your Next Steps

• Closing ThoughtsThe Headline: A 55.5% Income Jump (Is It Real?)

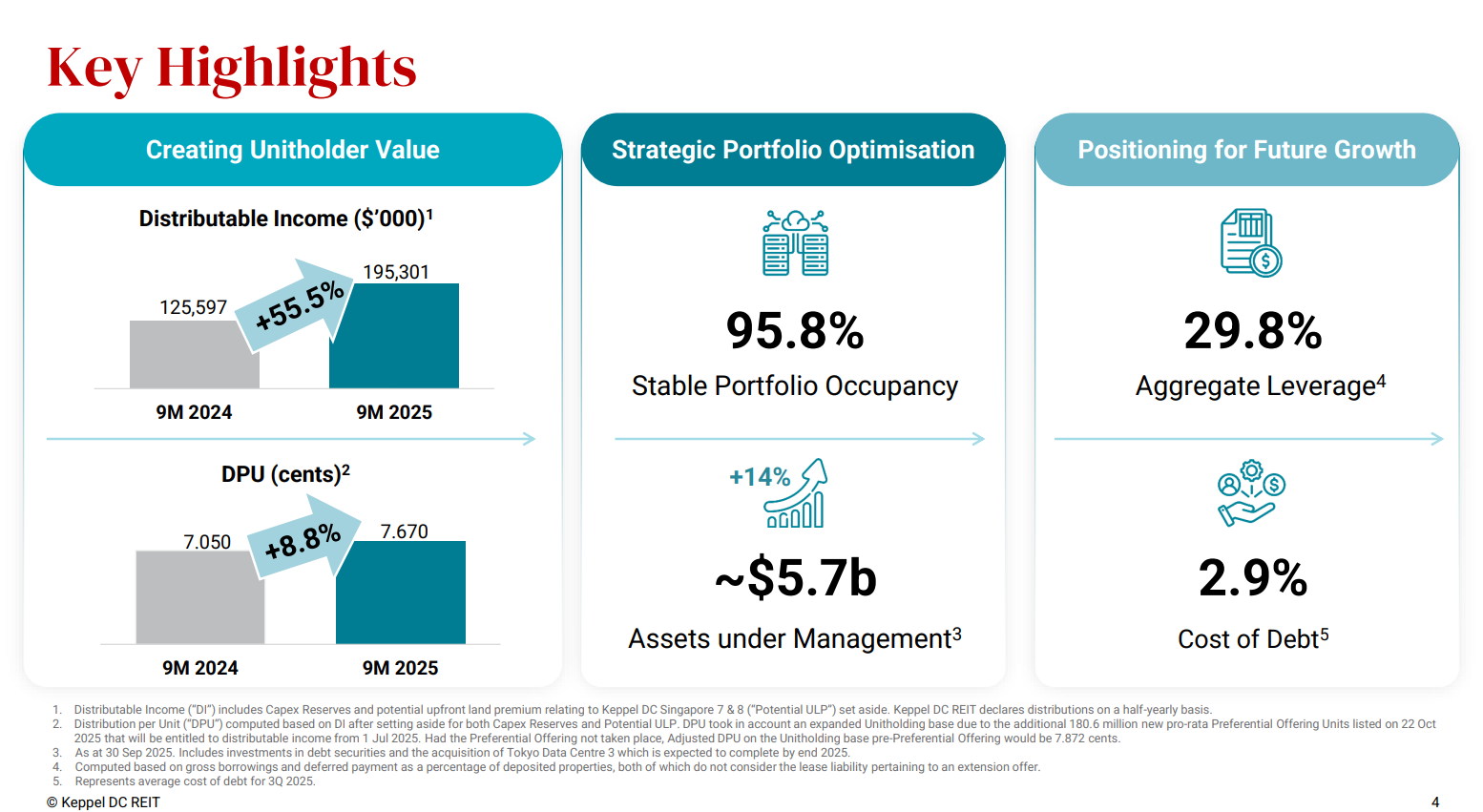

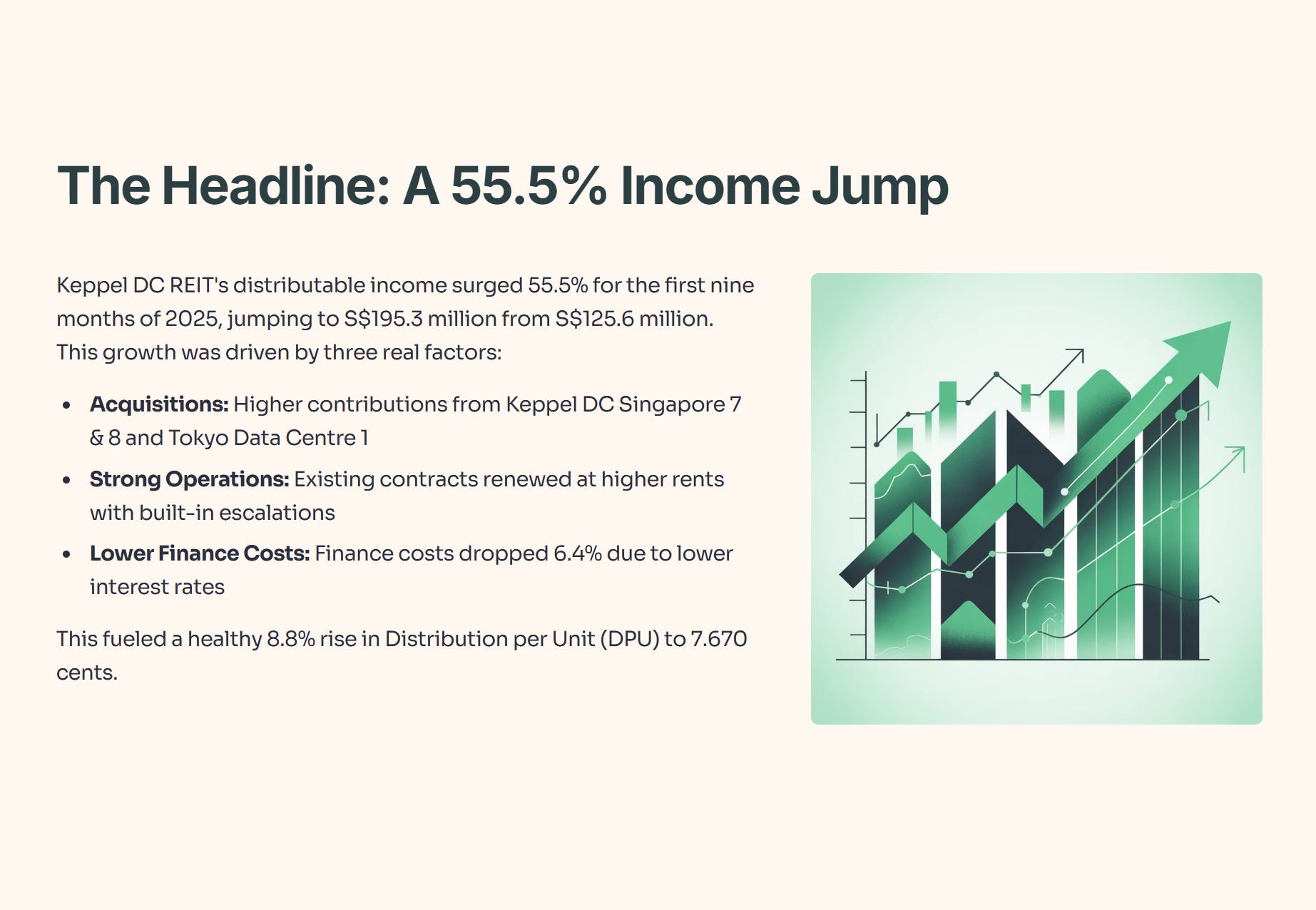

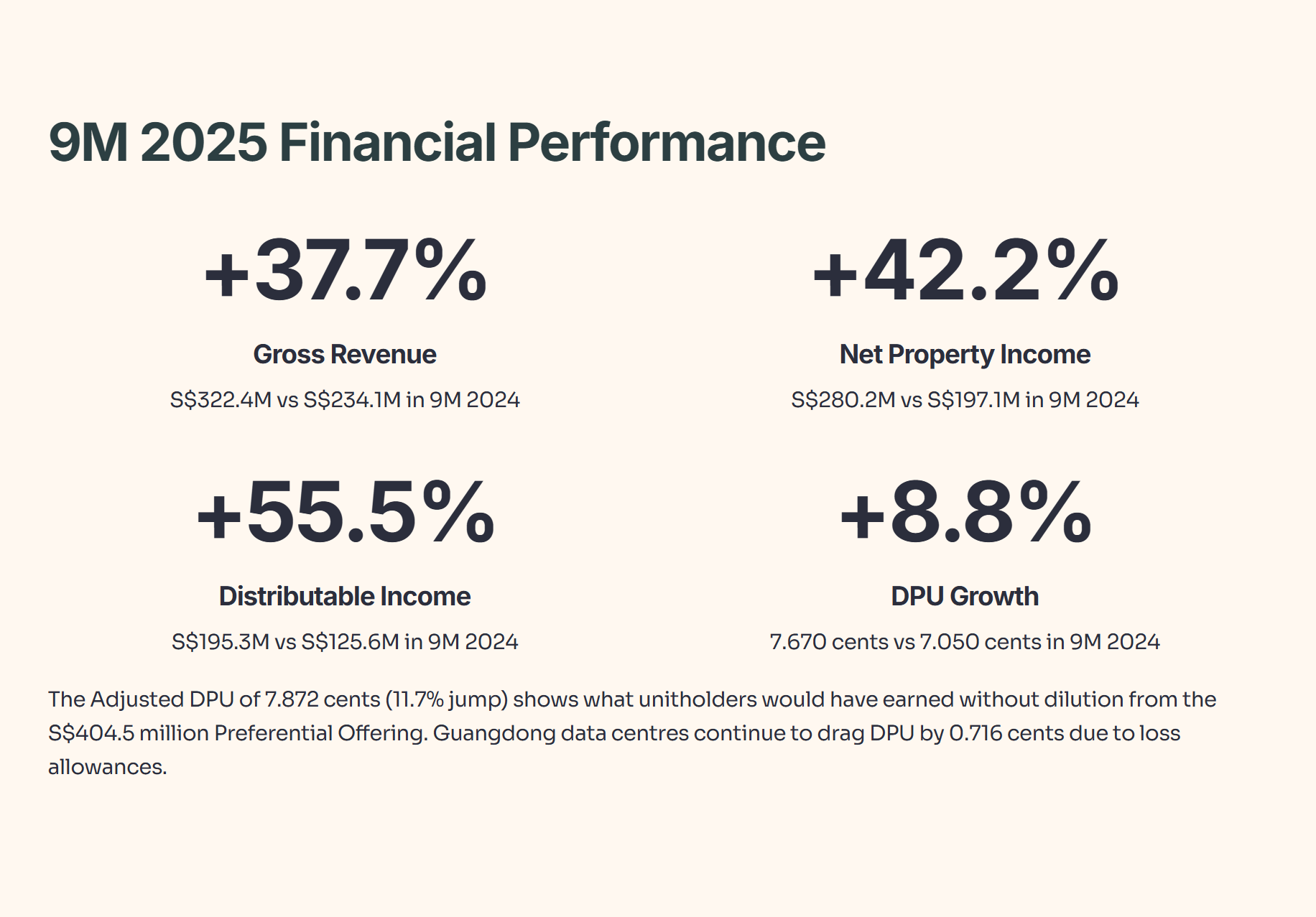

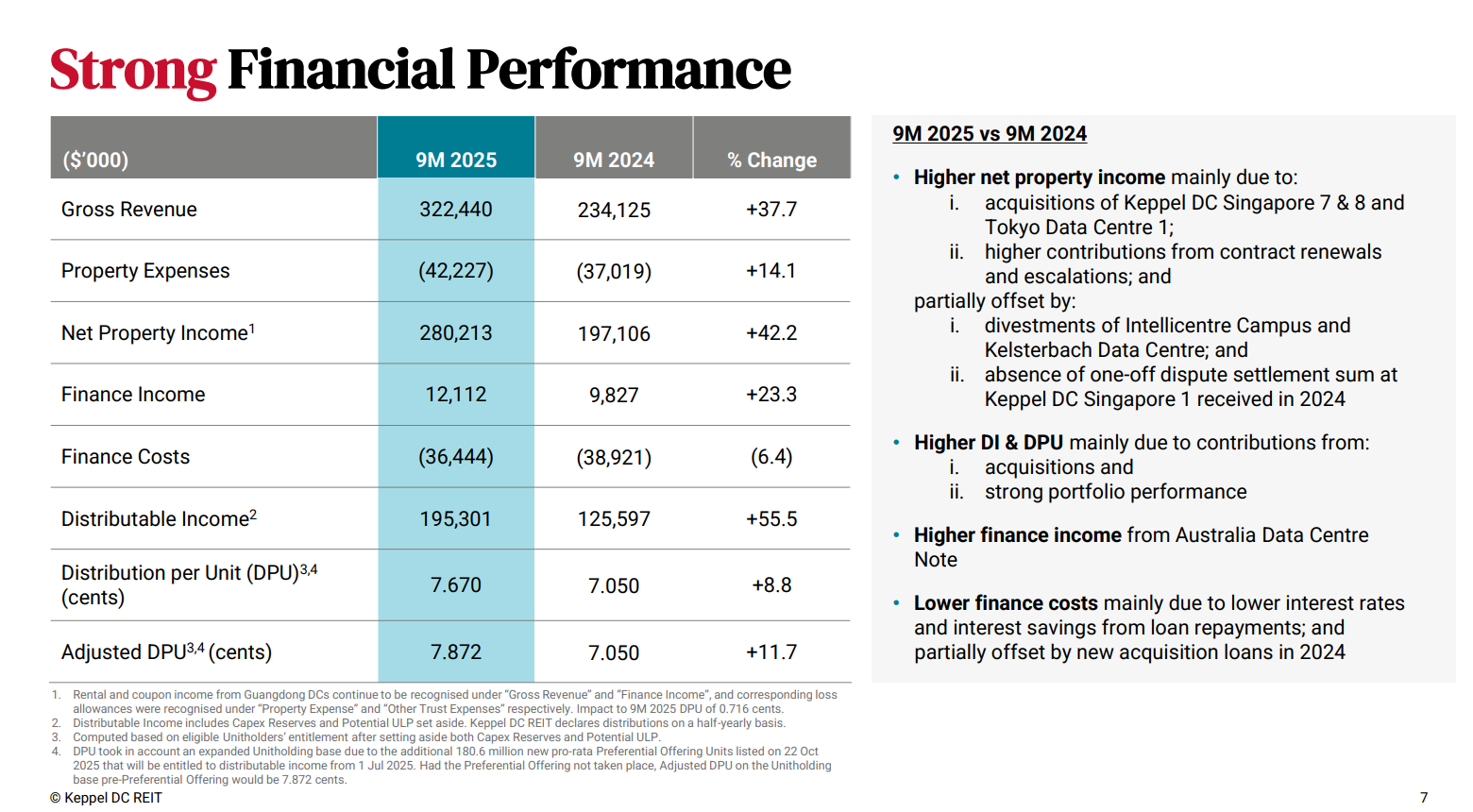

Let’s get right to the headline number. Keppel DC REIT’s distributable income surged an incredible 55.5% for the first nine months of 2025, jumping to S$195.3 million from S$125.6 million last year.

This wasn’t just accounting magic. The growth was driven by three real factors:

Acquisitions: The trust saw higher contributions from its recent buyouts, including Keppel DC Singapore 7 & 8 and Tokyo Data Centre 1.

Strong Operations: Existing contracts were renewed at higher rents, and built-in escalations kicked in, boosting income from the core portfolio.

Lower Finance Costs: Finance costs actually dropped by 6.4%, mainly due to lower interest rates and savings from loan repayments.

This fueled a healthy 8.8% rise in Distribution per Unit (DPU) to 7.670 cents.

Now, you might see “Adjusted DPU” of 7.872 cents, an 11.7% jump. Why the difference? This “Adjusted DPU” shows what you would have earned without the new units from the recent S$404.5 million Preferential Offering. The reported 7.670 cents is what unitholders will get, as it accounts for this larger unitholder base. The key takeaway is that management is growing the pie fast enough to (mostly) overcome the dilution from raising new capital.

It wasn’t all perfect. The trust continues to set aside loss allowances for its Guangdong data centres in China, which dragged down the 9-month DPU by 0.716 cents. This remains a small, nagging risk to monitor.

9M 2025 Financial Performance

The Strategy: Doubling Down on Hyperscale & AI

This strong performance isn’t just happening in a vacuum. It’s the result of a clear strategy: focus on pure data centre assets and capture the massive growth from AI and the cloud.

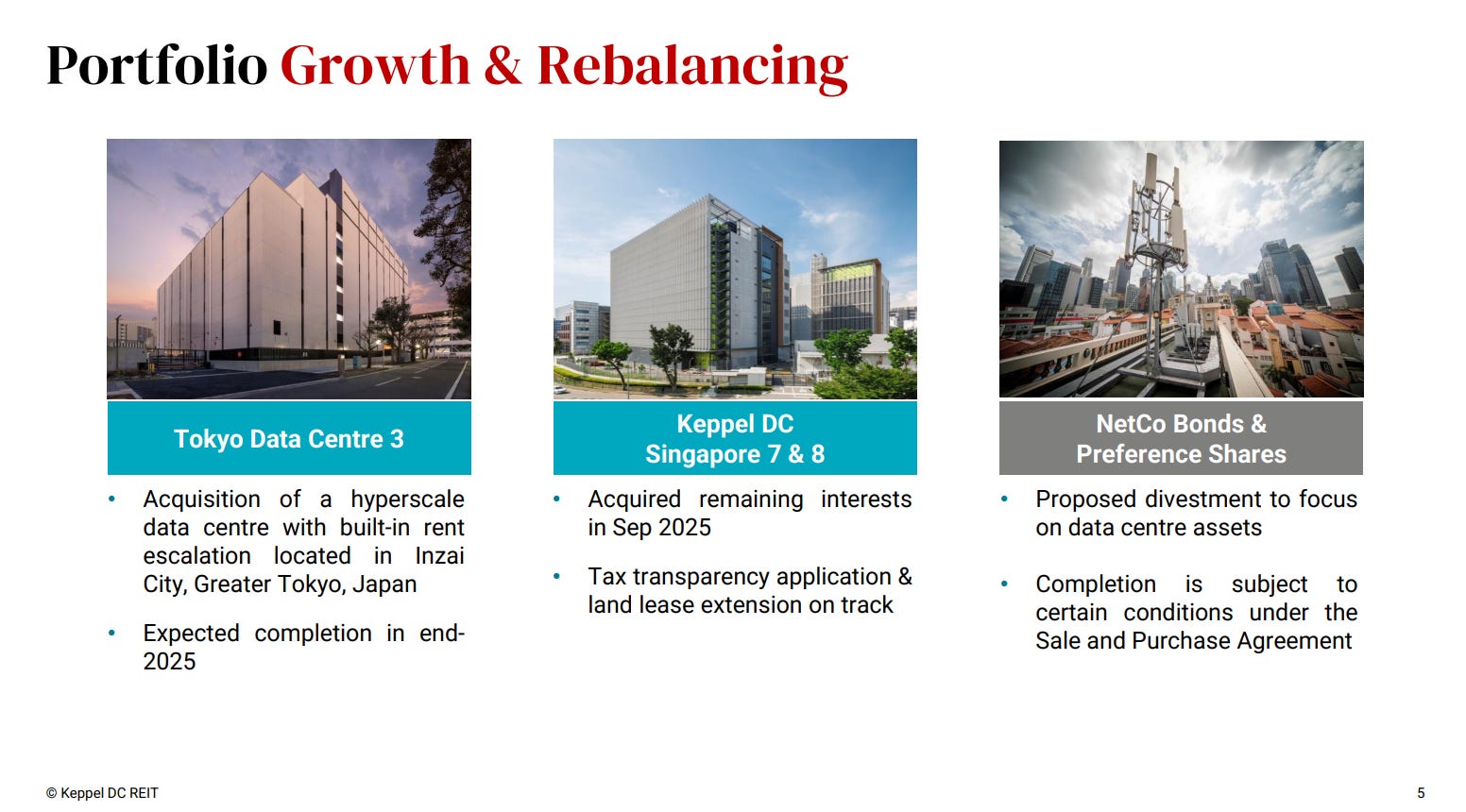

The trust is making three big moves:

Consolidating at Home: It acquired the remaining interests in Keppel DC Singapore 7 & 8, giving it 100% ownership of these key local assets.

Selling Non-Core: It’s divesting its NetCo bonds and preference shares. This is a smart move to shed financial assets and become a “pure-play” data centre REIT, which investors tend to value more highly.

Expanding into Hyperscale: The REIT is acquiring Tokyo Data Centre 3, a hyperscale facility in Japan with built-in rent escalations.

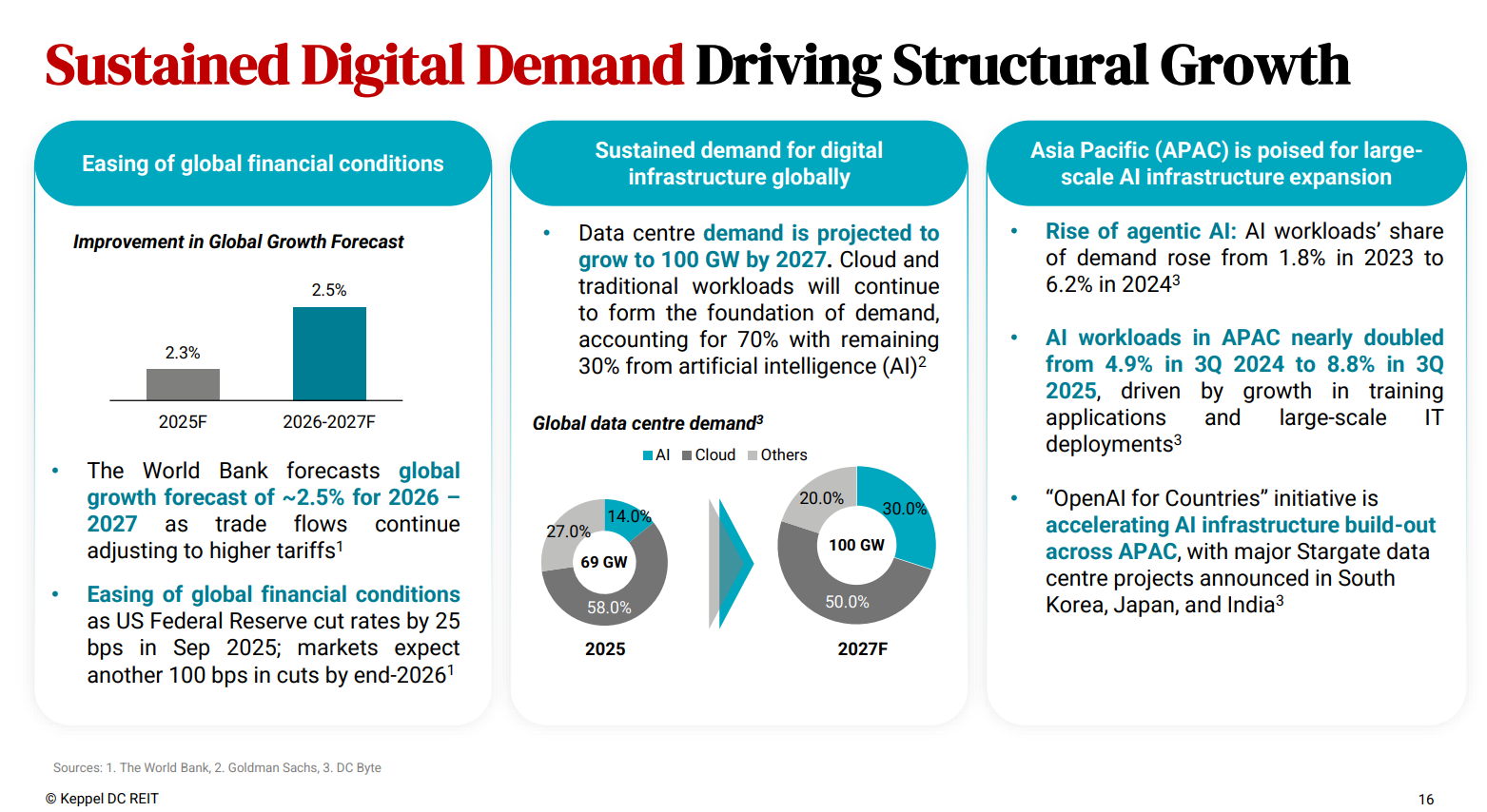

This strategy directly targets the AI boom. Global data centre demand is projected to grow to 100 GW by 2027 (from 69 GW in 2025), and AI workloads are expected to make up 30% of that new demand. Asia Pacific, in particular, is seeing an explosion in AI infrastructure, with AI workloads in the region nearly doubling in the past year alone.

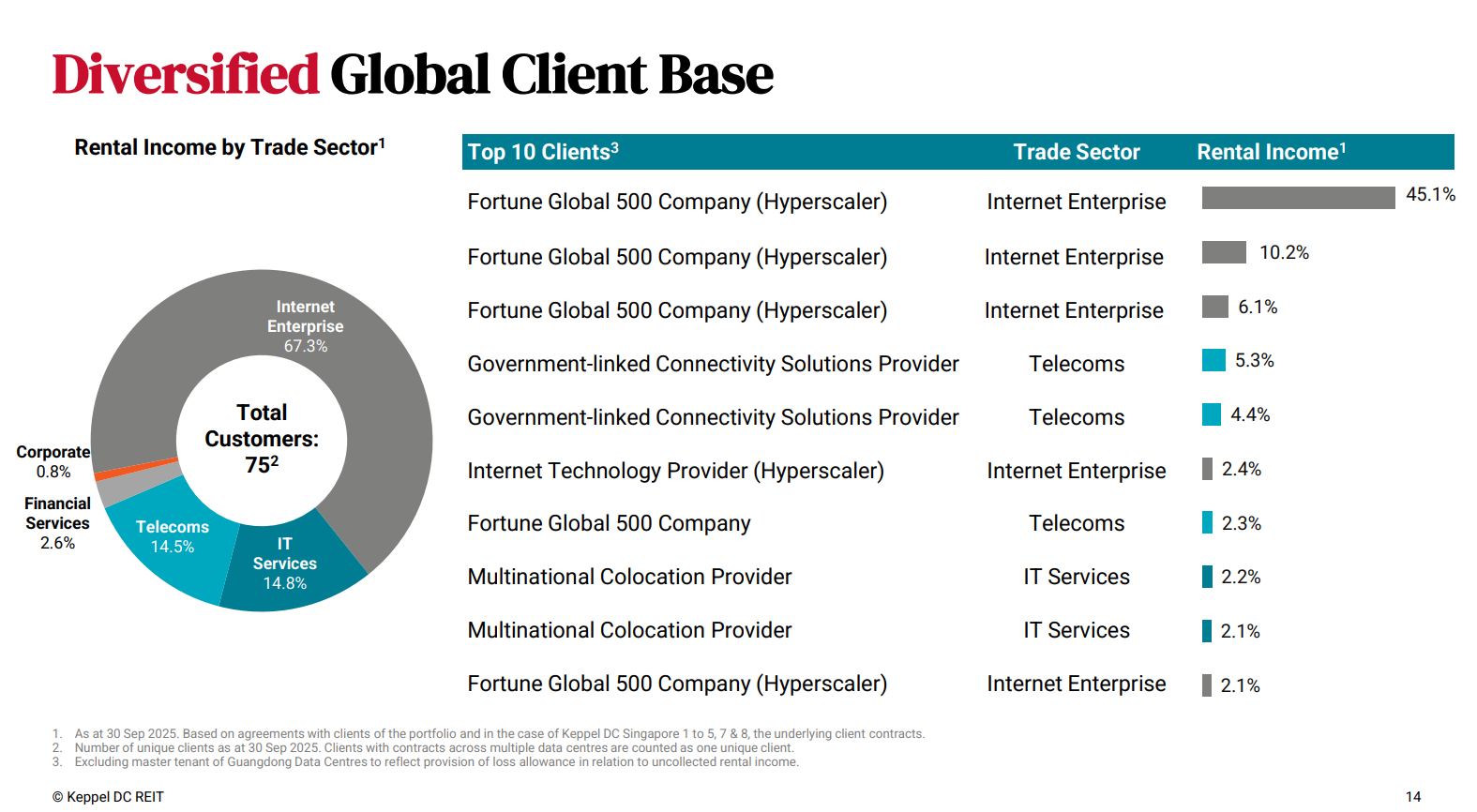

By buying in Tokyo, Keppel DC is placing itself right in the middle of this growth. This also complements its existing blue-chip tenant base, which is already dominated by “Internet Enterprise” clients (67.3% of rental income) and includes multiple Fortune Global 500 hyperscalers.

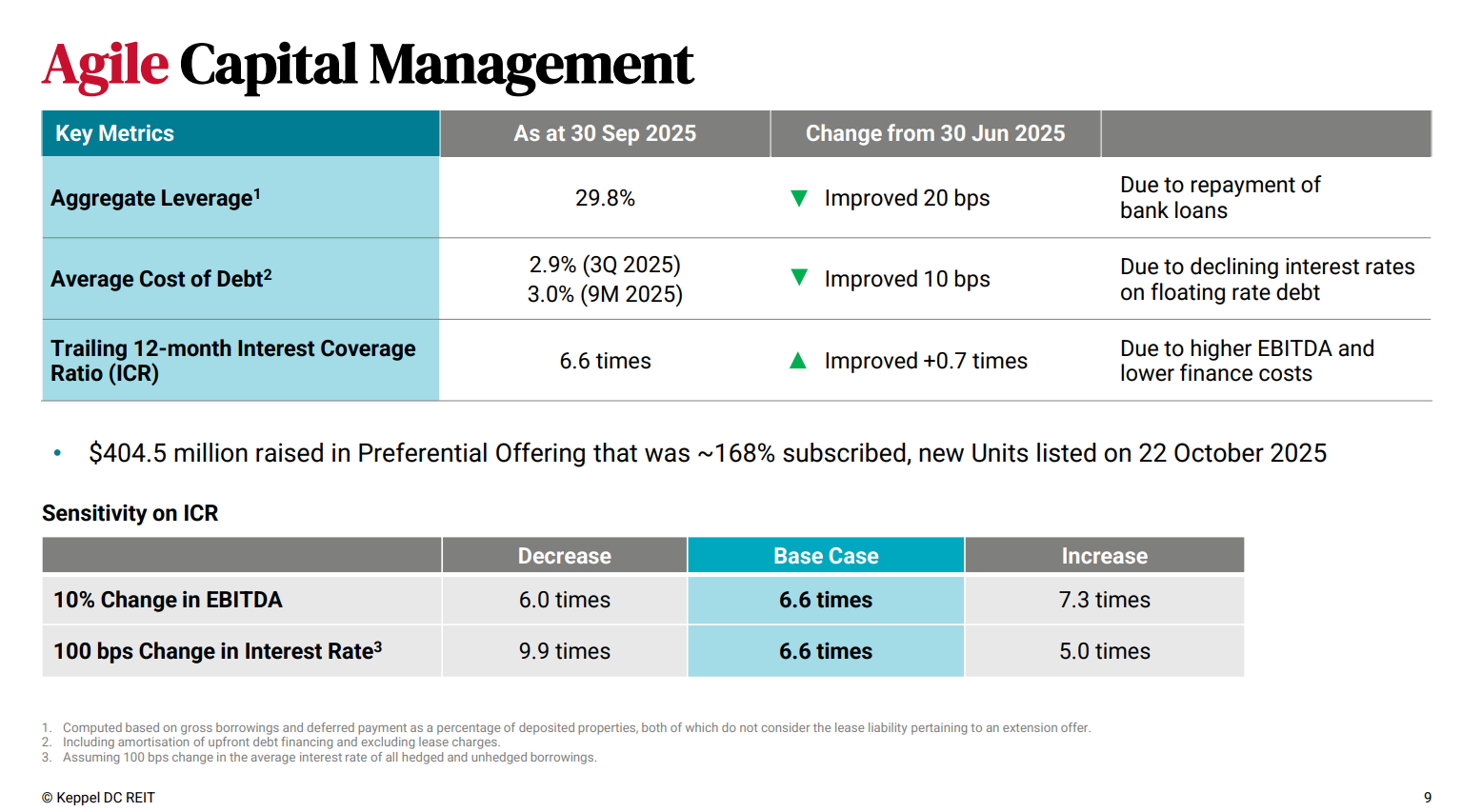

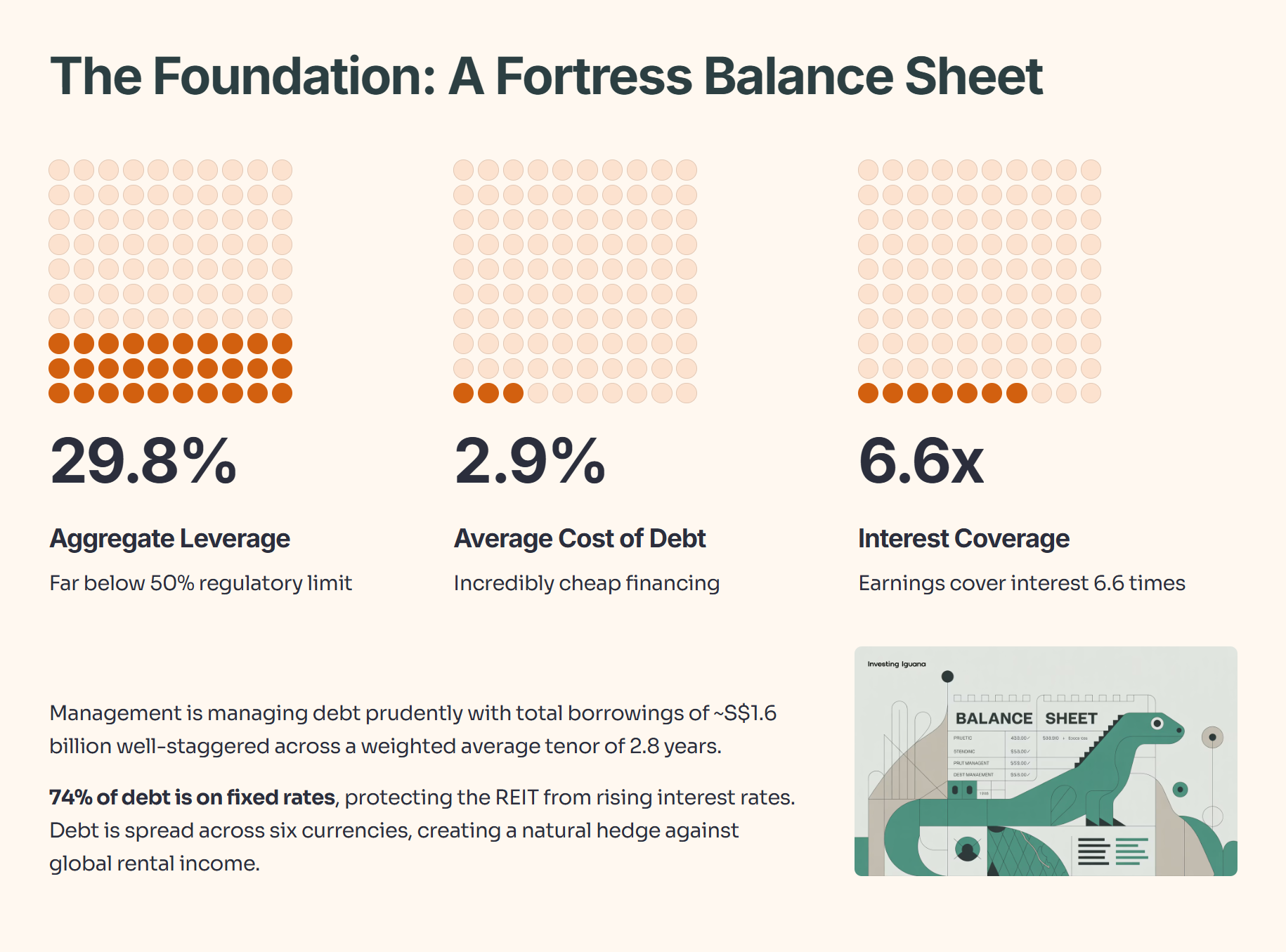

The Foundation: A Fortress Balance Sheet

Growth is great, but safety comes first. For a REIT, that means a rock-solid balance sheet. Keppel DC’s financials look stronger than ever.

Aggregate Leverage is low at 29.8%, far below the 50% regulatory limit. This gives it a huge debt headroom for future acquisitions.

Average Cost of Debt for the quarter fell to just 2.9%. This is incredibly cheap financing in the current environment.

Interest Coverage Ratio (ICR) improved to 6.6 times, meaning its earnings can cover its interest payments more than six times over.

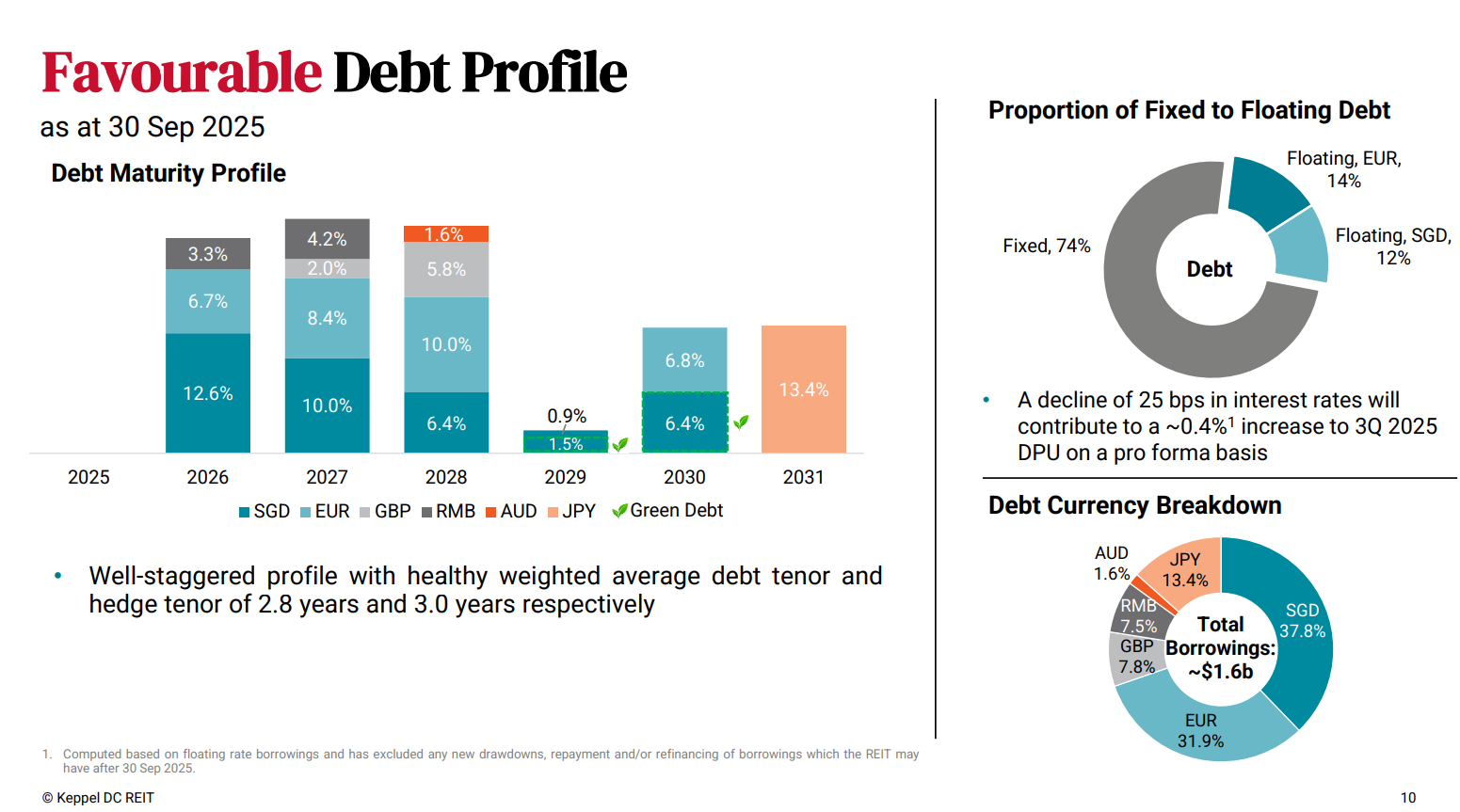

Management is also managing its debt profile prudently. Total borrowings of ~$1.6 billion are well-staggered, with a healthy weighted average debt tenor of 2.8 years. Critically, 74% of the debt is on fixed rates, protecting the REIT from rising interest rates. The debt is also spread across six different currencies, creating a natural hedge against its global rental income.

This financial prudence was validated by the market. The REIT’s recent S$404.5 million preferential offering was ~168% subscribed. This means investors were lining up to give them more money, signaling strong confidence in this growth story.

Capital Management Health Check

The Assets: Locked-in, Blue-Chip Income

Finally, let’s look at the properties themselves. A REIT is only as good as the rent it collects.

Keppel DC’s portfolio is in excellent health.

Portfolio Occupancy is a high 95.8%.

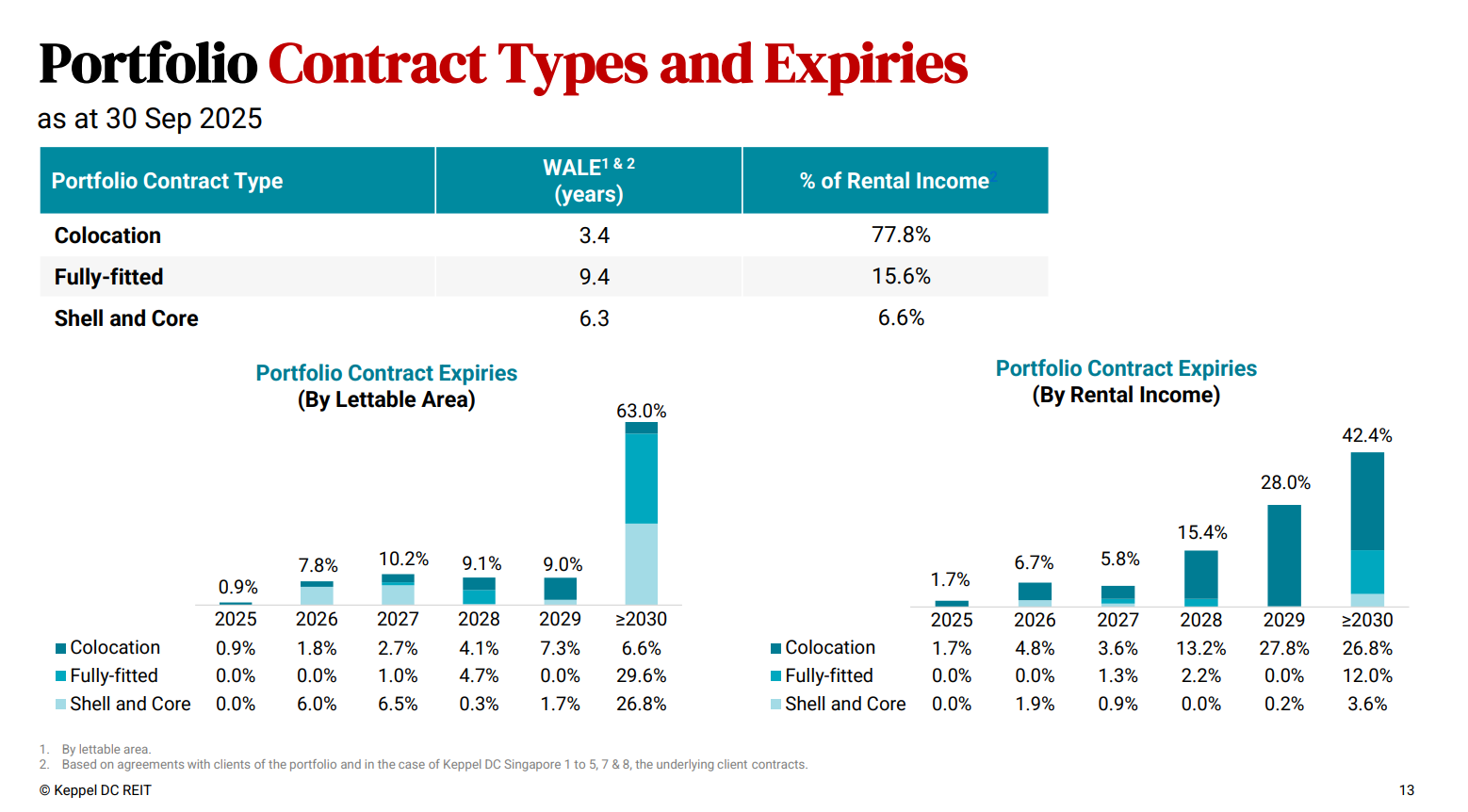

Weighted Average Lease Expiry (WALE) is a long 6.7 years (by lettable area).

This long WALE provides incredible income stability. It’s like having a 6.7-year employment contract. The trust’s revenue is diversified across three lease types: colocation (77.8% of rental income), fully-fitted (15.6%), and shell-and-core (6.6%).

Best of all, there is no scary “maturity wall.” Only 0.9% of the portfolio’s rent is up for renewal in the rest of 2025. A massive 63.0% of the leases don’t expire until 2030 or beyond. This means the vast majority of its income is locked in for the long haul, providing a predictable stream of cash to fund distributions.

Iggy’s Assessment: Hold with Positive Outlook

After dissecting the update, here’s my take on Keppel DC REIT.