Can Keppel Pay Dividends With China Drag (Keppel Q1 2026 Report) | 🦖EP1566

When Q1 2026 net profit falls on legacy fair value losses but DPU and yield data are missing from slides

Overall Assessment

Overall net profit is down due to massive fair value losses in legacy assets, but management wants full attention on a 13% rise in asset management fees. For investors relying on dividends for CPF Life payouts, this gap between accounting spin and operational reality is material. The difference determines whether retirement income is stable or exposed to sudden compression. This audit strips away the asset-light narrative and evaluates Keppel’s actual capacity to protect capital.

In This Article:

Overall Assessment

The Slide-by-Slide Audit

The Transition and the Smoke Screen

Infrastructure and the Cash Engine

Connectivity and Data Centres

Real Estate and the China Anchor

The Reality Check

The Scorecard and Yield Spread

Forward Outlook

Classification and Closure

The Slide-by-Slide Audit

The Transition and the Smoke Screen

The transformation from heavy industrial builder to asset-light global manager is the core management narrative. It is also the most forensically loaded claim in the entire results pack.

Performance is presented through the construct of “New Keppel” — a ring-fenced view that conveniently excludes the Non-Core Portfolio for Divestment and Discontinued Operations. Under this isolated metric, net profit appears only slightly lower year-on-year. The framing is deliberate. By drawing a line around the parts of the business that are working and relabelling everything else as transitional noise, management creates a narrative where the transformation is already succeeding.

But retail investors own the entire company, not a curated subset. You cannot opt out of the legacy drag. Group-level results reveal a harsher reality:

Overall net profit declined YoY in Q1 2026, driven by fair value losses and weaker monetisation from legacy assets.

Corporate transition costs cannot be erased by reclassification. They are real cash and real drag.

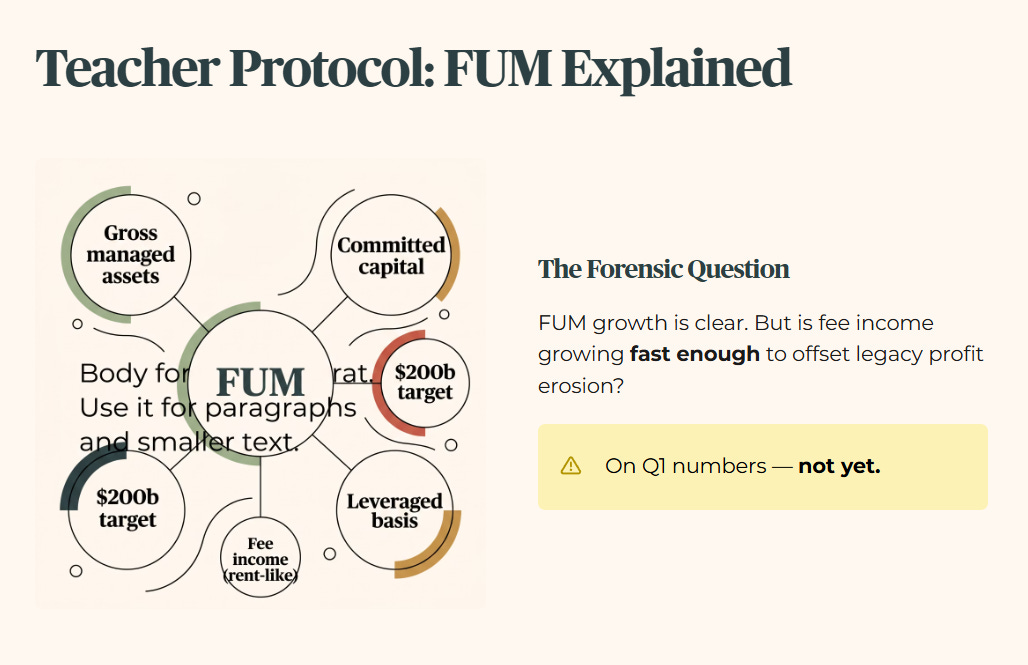

Asset management fees grew 13% to $108m, supported by $0.4b of new FUM added in the quarter.

Iggy Explains: Funds Under Management (FUM) is the gross value of managed assets and committed capital, measured on a leveraged basis. Fees collected on FUM represent recurring “rent-like” income from institutional capital. The higher the FUM, the larger the fee base — which is why Keppel’s $200b FUM target is the centrepiece of the investor relations story.

The forensic question is not whether the asset management business is growing. It clearly is. The question is whether the fee income is growing fast enough to offset the profit erosion from legacy assets while the transition completes. On current Q1 numbers, the answer is not yet.

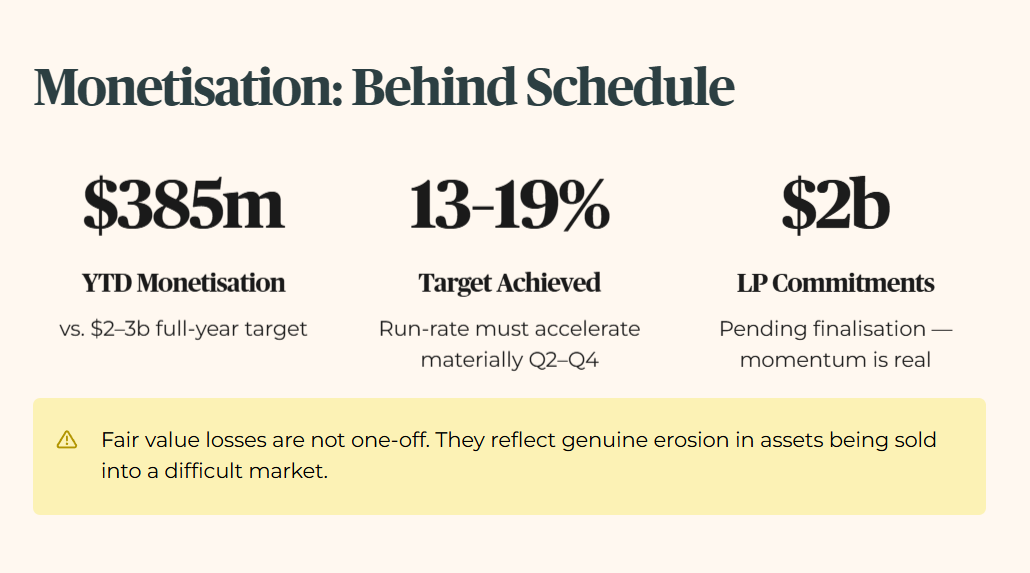

Keppel has $2b of LP commitments pending finalisation. Momentum is real. However:

$385m of asset monetisation has been achieved YTD in 2026 versus a $2–3b full-year target. That is approximately 13–19% of the target in the first quarter. The run-rate needs to accelerate materially in Q2 through Q4.

Cash flows improved, but profit drag from legacy assets remains unresolved.

Fair value losses are not a one-off accounting adjustment. They reflect genuine erosion in the carrying value of assets that need to be sold into a difficult market

The “New Keppel” construct is not dishonest. It is a legitimate way to show investors what the business looks like once the transition completes. The problem is the timeline. Management has not committed to a hard completion date for the non-core wind-down. For a 50-year-old investor funding retirement, this transition demands patience while dividends remain exposed. Patience is a luxury that not every portfolio can afford.

Infrastructure and the Cash Engine

Infrastructure and Connectivity remains the group’s most resilient pillar. Earnings rose YoY, with Integrated Power showing resilience despite a slight Q1 EBITDA decline due to softening electricity spreads.

Iggy Explains: EBITDA reflects core operating cash generation before financing and accounting adjustments. Softening spreads indicate shrinking profit margins in power markets.

Mitigation actions:

Long-term power sales are being locked in.

The 600MW hydrogen-compatible Keppel Sakra Cogen Plant is fully contracted for 2026–2027, improving income visibility.

In Decarbonisation and Sustainability Solutions:

More than $700m of new long-term contracts were secured in Q1 alone.

Total backlog: $7.6b, spanning 10–15 years.

Notable wins include a 20-year Tengah centralised cooling contract and an AI-enabled cooling partnership with Midea.

The book-to-bill ratio of approximately 4.0x confirms strong pipeline conversion. Execution discipline is now the critical variable.

Iggy’s Insight

Management buried Middle East geopolitical risk in a single back-of-deck slide. While claiming limited impact, disclosures admit reliance on diversified gas supply, including international LNG cargoes. Any supply disruption risks rapid margin compression. The most critical omission is the percentage of unhedged fuel costs. Cost pass-through exists, but with delay. Hope is never a valid hedging strategy.

Connectivity and Data Centres

The Connectivity division targets AI-driven demand:

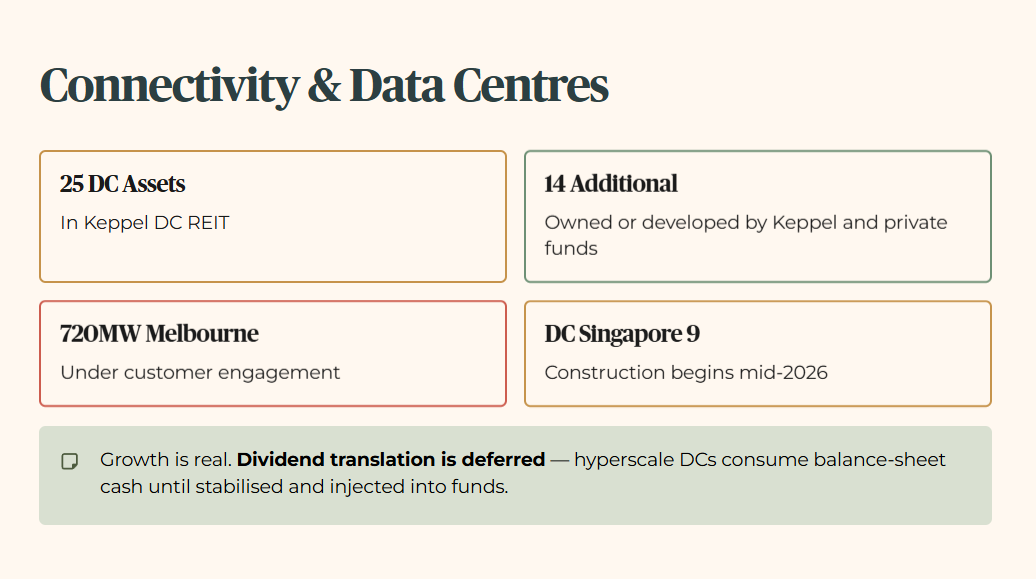

25 data centre assets in Keppel DC REIT.

14 additional assets owned or developed by Keppel and private funds.

720MW Melbourne site under customer engagement.

Keppel DC Singapore 9 construction begins mid-2026.

Bifrost subsea cable discussions nearing completion, H1 2026.

Risk note: Hyperscale data centres require heavy upfront capital. Until assets are stabilised and injected into funds or REITs, they consume balance-sheet cash. Fee extraction is delayed. Growth is real. Dividend translation is deferred.

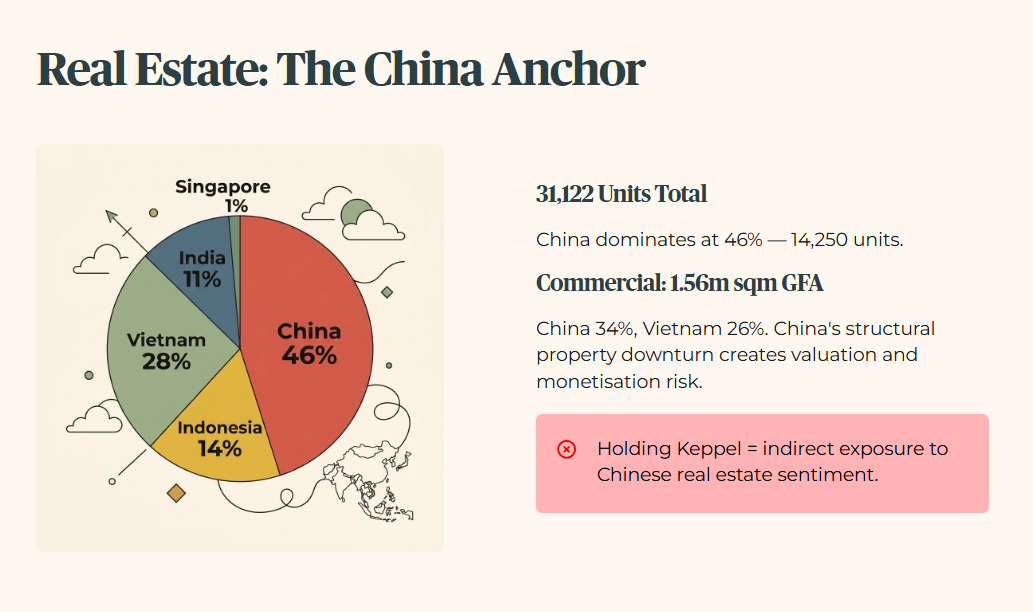

Real Estate and the China Anchor

Real Estate is the largest drag on the transition. Earnings were materially lower YoY due to the absence of valuation and divestment gains seen in Q1 2025.

Residential landbank: 31,122 units total — China 46% (14,250 units), Vietnam 28%, Indonesia 14%, India 11%, Singapore 1%.

Commercial portfolio: 1.56m sqm GFA — China 34%, Vietnam 26%, under development approximately 39%.

China’s structural property downturn creates valuation and monetisation risk. While $382m of real estate monetisation has been reported YTD (including i12 Katong), large China and Vietnam portfolios remain difficult to exit without steep haircuts. Holding Keppel implies indirect exposure to Chinese real estate sentiment.

The Reality Check

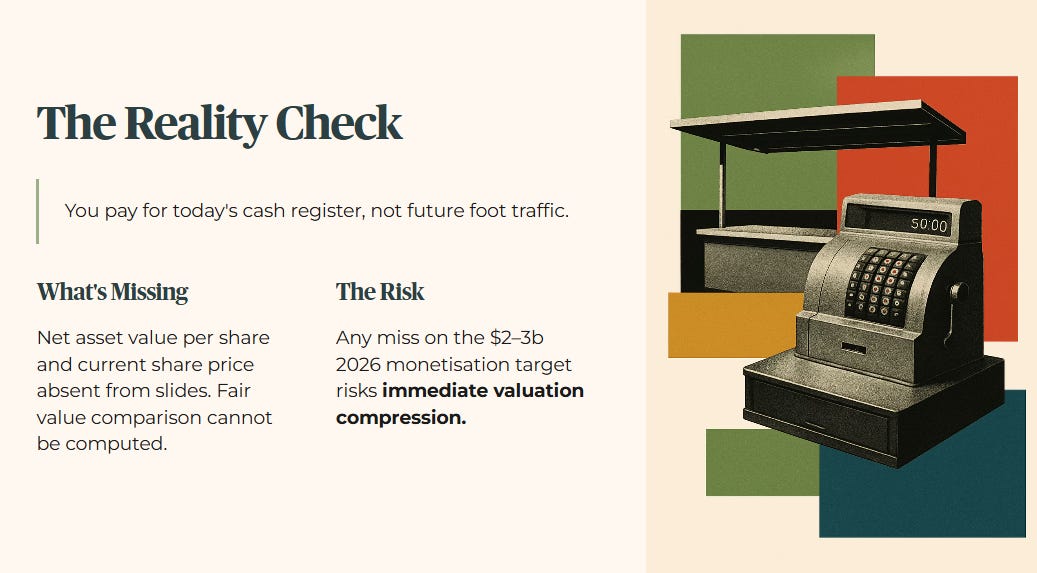

Management highlights a $200b FUM target and rising recurring fees. However, net asset value per share and current share price are absent from the slides. An InvestingPro Fair Value comparison cannot be computed due to deliberate data omission.

Kopitiam Logic: You pay for today’s cash register, not future foot traffic. When price runs ahead of forensic value, investors are paying for hope.

Absent clear discount-to-fair-value data, forensic caution applies. Any miss in the $2–3b 2026 monetisation target risks immediate valuation compression.

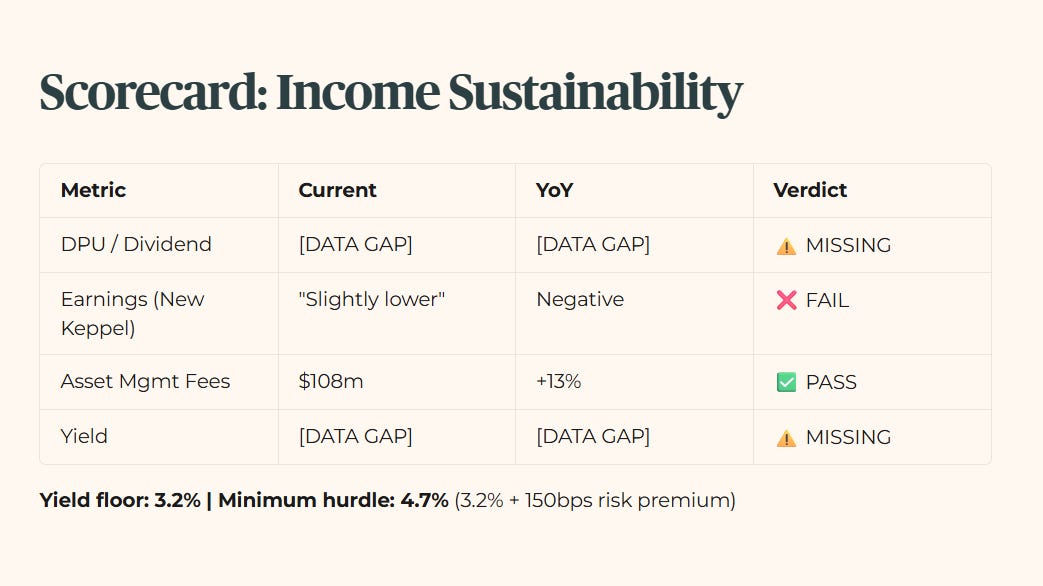

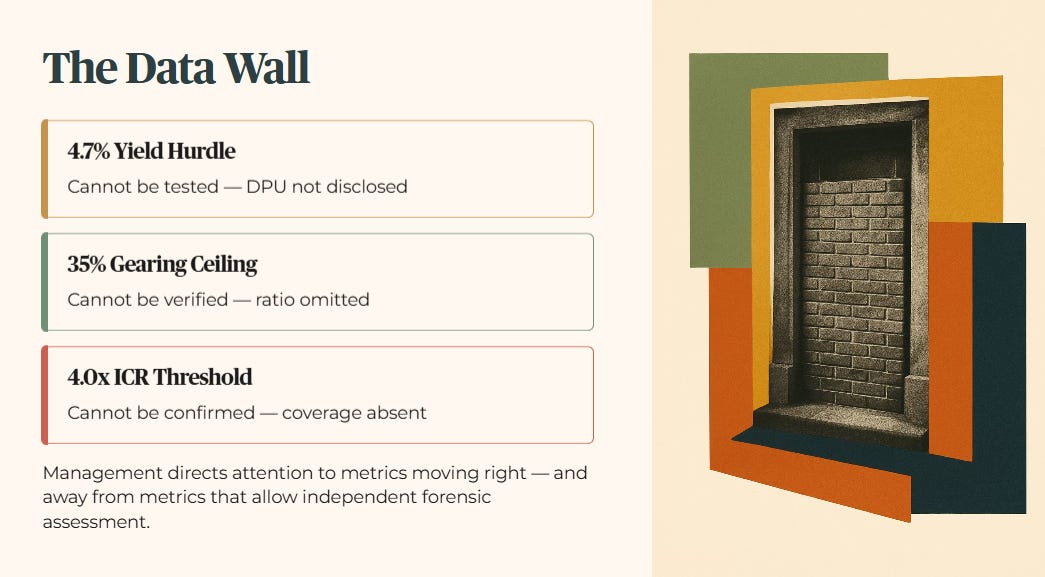

The Scorecard and Yield Spread

Stress-Test Buffer: Yield floor 3.2% | Minimum hurdle 4.7% (3.2% + 150bps risk premium)

Income Sustainability — Data Missing

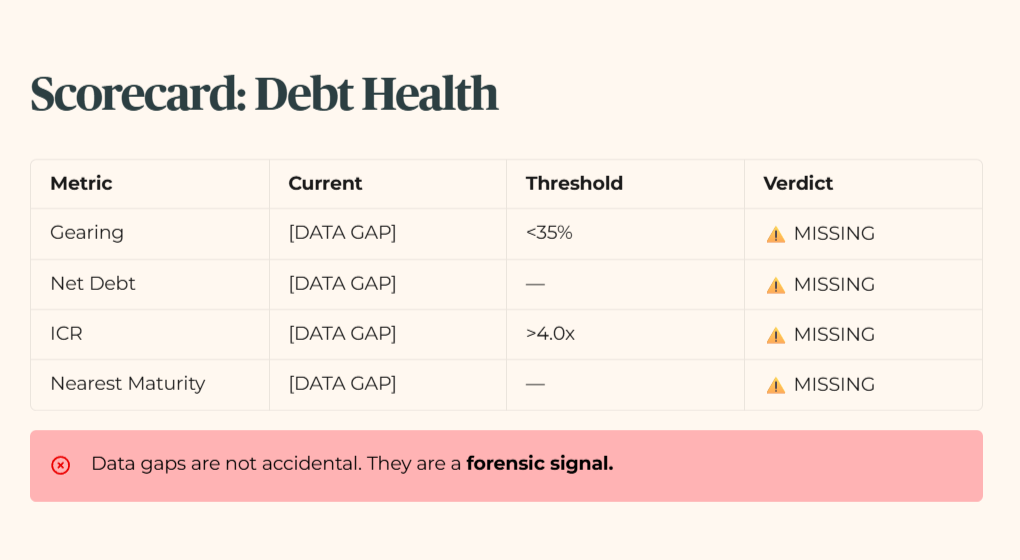

Debt Health — Data Missing

The data gaps in this scorecard are not an accident of incomplete reporting. They are a forensic signal in themselves.

When a company releases quarterly results without disclosing its current dividend per unit, yield, gearing ratio, or interest coverage ratio, it is making a choice. The choice is to direct investor attention toward the metrics that are moving in the right direction — asset management fee growth, FUM momentum, backlog wins — and away from the metrics that would allow a forensic investor to independently assess whether the stock is fairly priced and whether the income is sustainable.

For a retail investor running the Iggy forensic framework, this creates an immediate problem. The 4.7% yield hurdle cannot be tested. The 35% gearing ceiling cannot be verified. The ICR threshold of 4.0x cannot be confirmed. Every core forensic filter is blocked by a data wall that management built.

The only way to answer whether Keppel actually clears the 4.7% yield hurdle from here is to rebuild the missing scorecard from first principles — and that forensic reconstruction is where the verdict finally turns.