CLCT 40.7% Leverage Signals Dividend Danger

Bank brochures show 7% yield, but Iggy’s Forensic Floor reveals a leak. Don't be a volunteer for the bank's balance sheet.

Your Singapore REIT Has a China Problem: The Forensic Audit Nobody Is Running

Three SGX REITs are quietly insulated from the China property overhang. Three are directly exposed. Here is how to tell the difference before the market does it for you.

The silent threat is rarely the one making headlines.

In mid‑March 2026, the financial media is focused on whether the Straits Times Index can hold above its 5,000‑point psychological ceiling.

Meanwhile, a structural fault line is widening beneath a specific segment of the SGX REIT market — and most retail investors have absolutely no idea it runs directly through their CDP accounts.

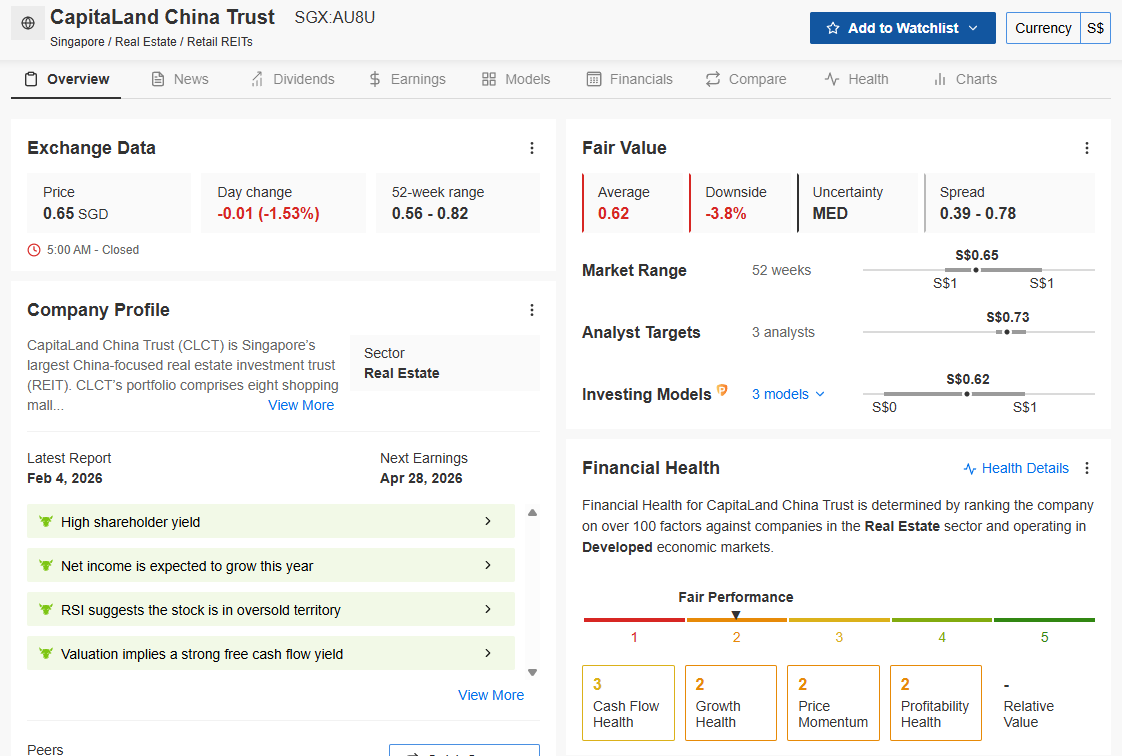

The China commercial and logistics property overhang is not a distant macro story. It is sitting inside your dividend portfolio right now, quietly compressing the net property income that funds your quarterly distribution cheque. CapitaLand China Trust has been using divestment gains and capital recycling to top up distributions despite weaker underlying NPI. CapitaLand China Trust has reported -24.5% rental reversions in its logistics portfolio, a brutal datapoint in an oversupplied market where anchor tenants are aggressively re‑pricing leases. And the RMB has been weakening against the SGD in a way that most retail investors have never modelled.

At the same time, three other SGX REITs are sitting in a structurally different position — diversified away from China’s property stress, generating organic cash flows, and trading at discounts to intrinsic value that the headline yield figures do not reveal.

This is the forensic audit nobody is running. We are going to run it today.

In This Article:

The Macro Setup: What Is Actually Happening in China

The Forensic Framework: Three Sanctuaries vs. Three Red Flags

The Three Sanctuaries

Sanctuary 1: Mapletree Industrial Trust (SGX: ME8U)

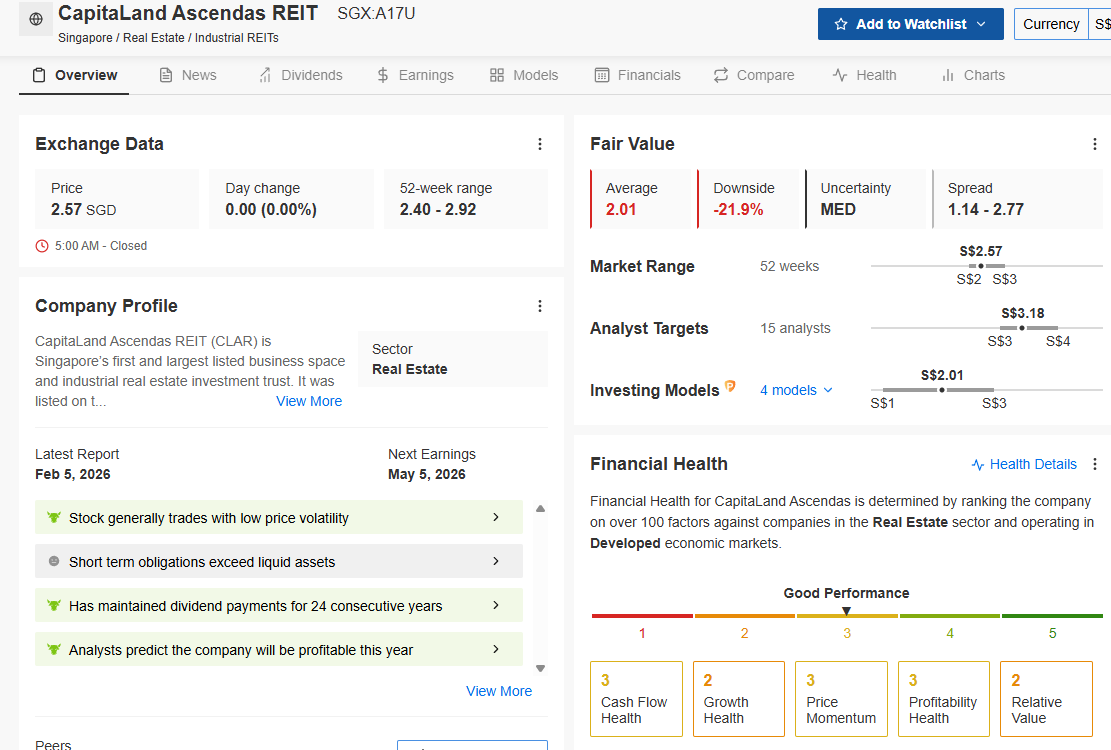

Sanctuary 2: CapitaLand Ascendas REIT (SGX: A17U)

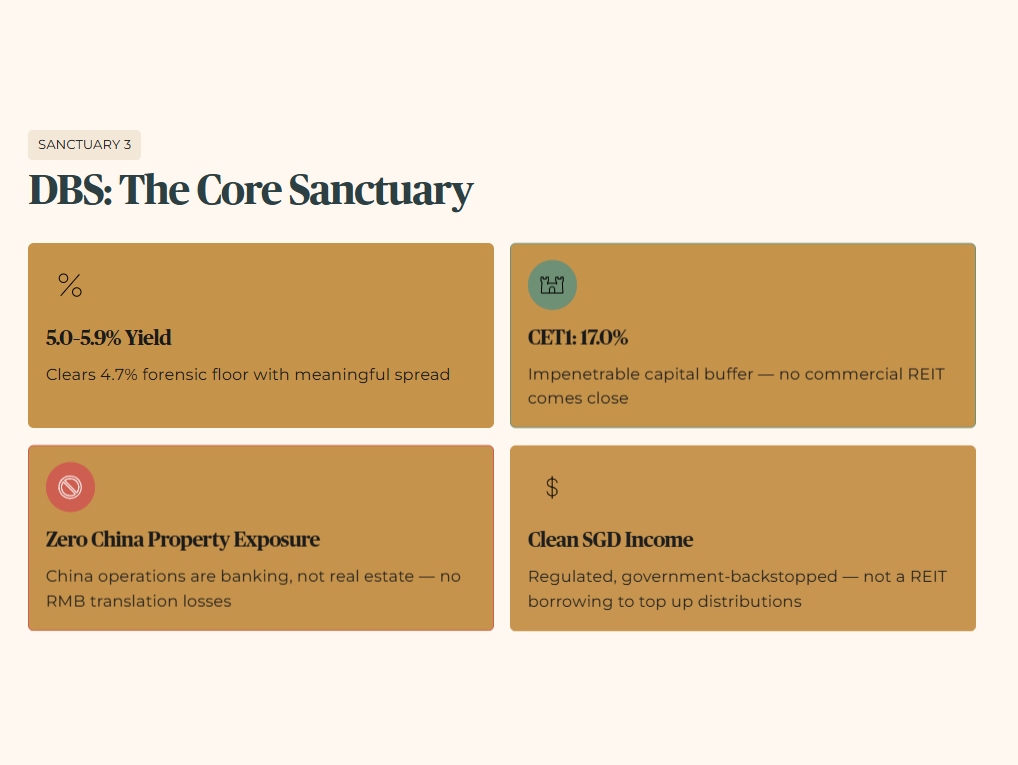

Sanctuary 3: DBS Group (SGX: D05)

The Three Red Flags

Red Flag 1: CapitaLand China Trust (SGX: AU8U)

Red Flag 2: Mapletree Logistics Trust (SGX: M44U)

Red Flag 3: Mapletree Pan Asia Commercial Trust (SGX: N2IU)

The Forensic Stress-Test: The Comparative Table

The Singaporean Context

InvestingPro Reality Check

The Verdict

About Iggy & the Elite Investors

One Community. One Forensic Lens. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. While free subscribers are reading yesterday’s story, Iggy’s Elite Investors are already cross-checking the next setup — together, in real time.

Iggy’s Elite Investors don’t just get the report earlier. They get the full forensic picture the moment it’s finalised — zero-day breakdowns, the complete “Red Zone” watchlist, and institutional-grade cheatsheets built around the same Five-Layer Audit you see here. The difference is they get it before the market opens, not after it has already moved.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

The Macro Setup: What Is Actually Happening in China

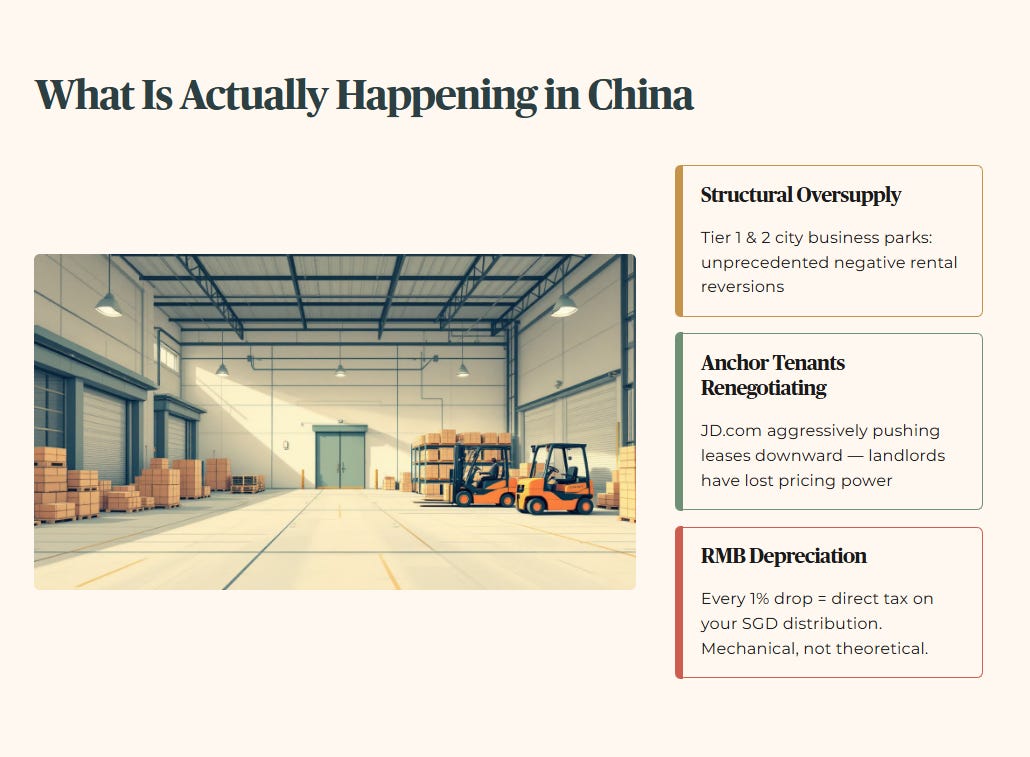

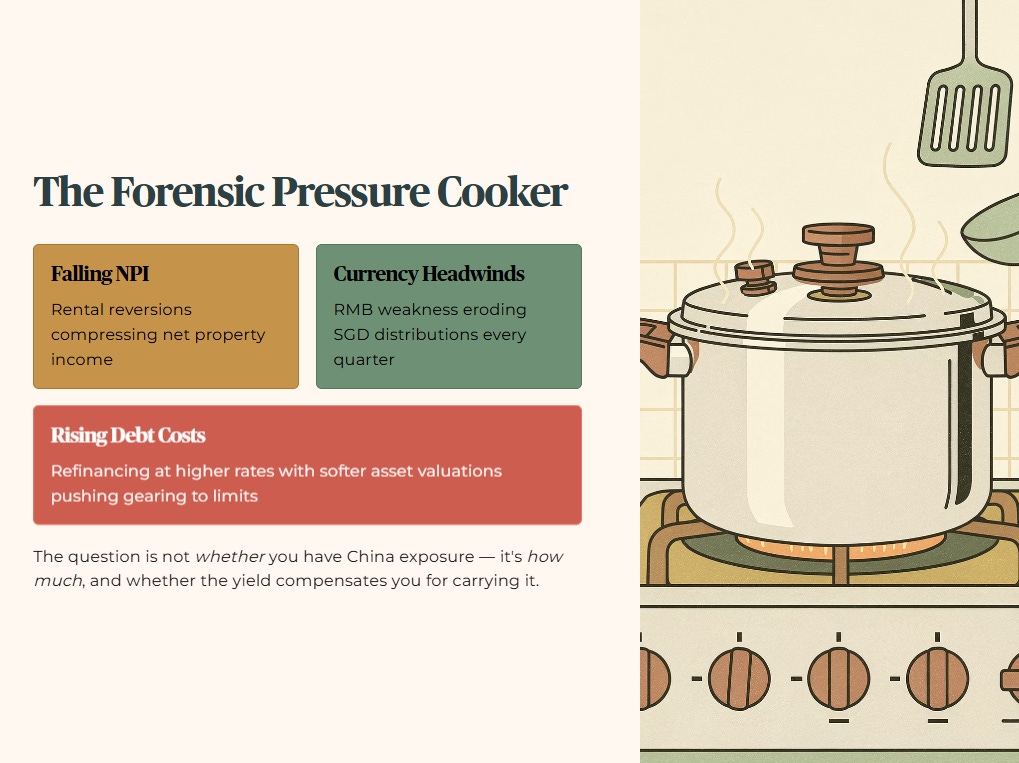

The Chinese commercial and logistics property sector entered 2026 carrying structural excess supply that government stimulus has not cleared. Tier 1 and Tier 2 city business parks are experiencing unprecedented negative rental reversions. Logistics parks — once the darling of the new economy narrative — are seeing anchor tenants like JD.com aggressively renegotiate leases downward, exploiting an oversupplied market where landlords have lost their pricing power entirely.

The RMB dimension compounds the damage for Singapore investors specifically. When a China-exposed REIT collects rent in RMB and distributes in SGD, every percentage point of RMB depreciation is a direct tax on your distribution. This is not a theoretical risk — it is a mechanical reality that flows directly from the income statement to your bank account every quarter.

The debt wall dimension is the third layer. China-exposed Singapore REITs that were gearing up during the boom years are now refinancing that debt in a higher-rate environment, with softer asset valuations pressing gearing ratios toward regulatory limits. The combination of falling NPI, currency headwinds, and rising debt costs creates a forensic pressure cooker that retail investors holding these assets inside SRS accounts cannot afford to ignore.

The question is not whether you have China exposure in your REIT portfolio. The question is how much — and whether the yield you are receiving actually compensates you for carrying it.

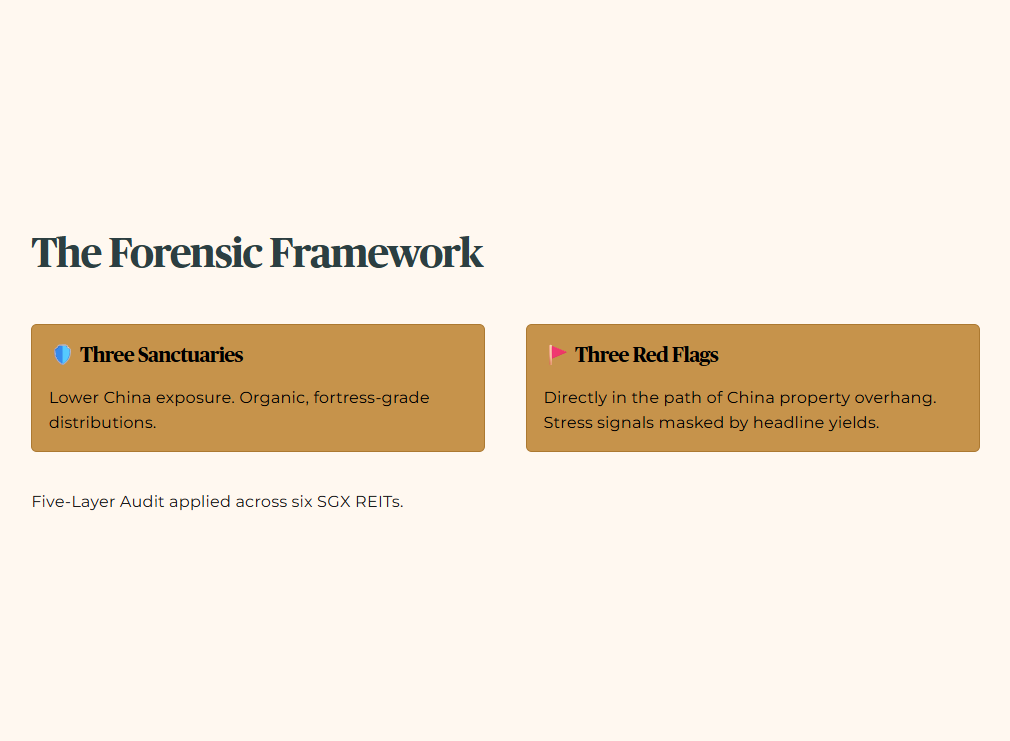

The Forensic Framework: Three Sanctuaries vs. Three Red Flags

We are applying the Five-Layer Audit across six SGX REITs today. Three have meaningfully lower China exposure and are generating organic, fortress-grade distributions. Three are directly in the path of the China property overhang and are showing forensic stress signals that the headline yields are masking.

The Three Sanctuaries

Sanctuary 1: Mapletree Industrial Trust (SGX: ME8U)

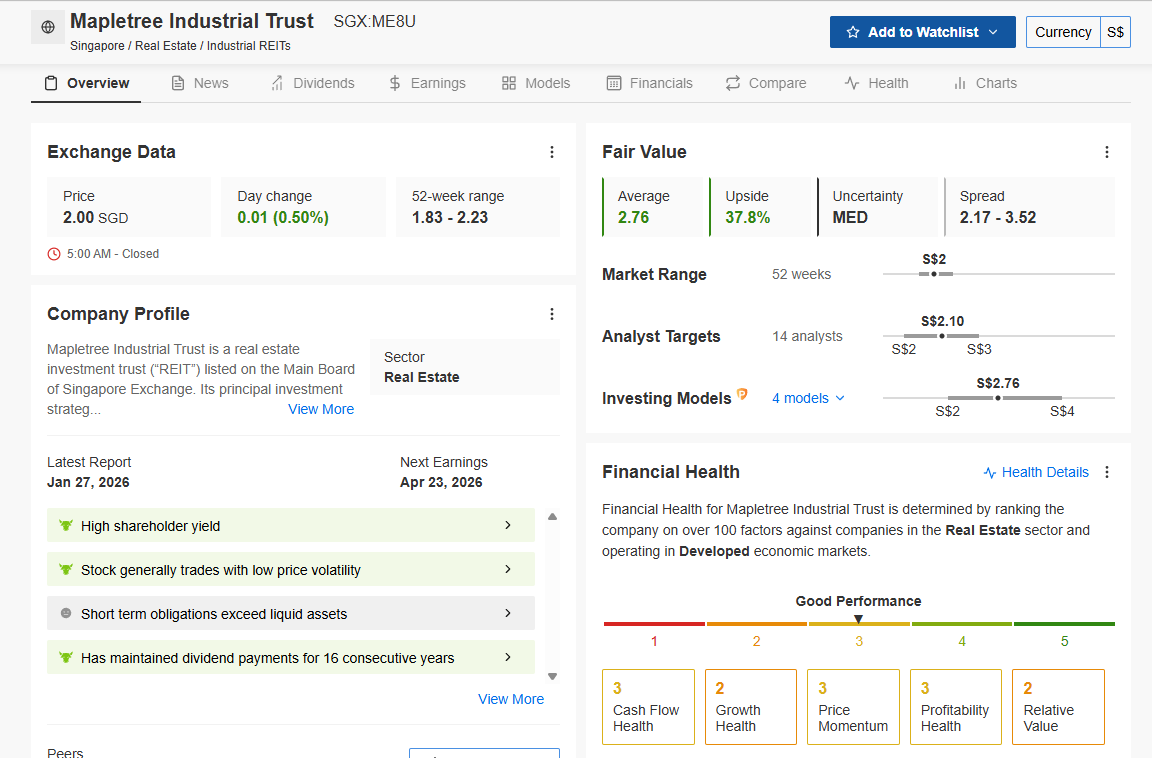

MIT is the clearest forensic sanctuary in the industrial REIT space right now, and the InvestingPro data makes the case emphatically.

“Don’t overpay for the hype. See the math behind the momentum.” .....Use the Fair Value models I use in every video. Code INVESTINGIGUANA gets you 50% off the world’s most powerful stock screener.

🦎 [Spot Undervalued Gems Here]

The raw fact is compelling. MIT is trading at a meaningful discount to third‑party estimates of intrinsic value, with a forward yield comfortably above our 4.7% forensic floor. Independent models like InvestingPro consistently show fair values above the current market price, indicating a margin of safety rather than a premium. The 52‑week trading band has been tight for an industrial REIT, signalling low volatility even as the market chases yield traps elsewhere. MIT has maintained uninterrupted distributions for more than 15 years — a forensic track record that CLCT cannot approach.

Historically, MIT’s portfolio has been anchored in Singapore flatted factories, business parks, and hi-tech industrial buildings, with a meaningful data centre component through its US joint venture with Mapletree Investments. This is structurally insulated from Chinese commercial property stress. The data centre demand tailwind — driven by AI infrastructure build-out across the US and Singapore — provides a forward growth engine that has nothing to do with Chinese rental reversions.

In peer context, while China-exposed REITs are fighting negative reversions, MIT’s Singapore industrial portfolio operates in a supply-constrained environment where modern industrial space commands stable or positive rental revisions. The forward scenario is structurally positive — Singapore’s industrial land scarcity and the data centre demand wave are secular tailwinds that will persist regardless of what happens to Chinese logistics vacancy rates.

The wallet impact for a 50-plus Singaporean investor is straightforward. MIT gives you a clear margin of safety to intrinsic value based on independent fair‑value models, over a decade of uninterrupted distributions, and minimal direct Chinese commercial property exposure.

That is the definition of a forensic sanctuary — an asset that protects your capital during the storm, not just the sunny day.

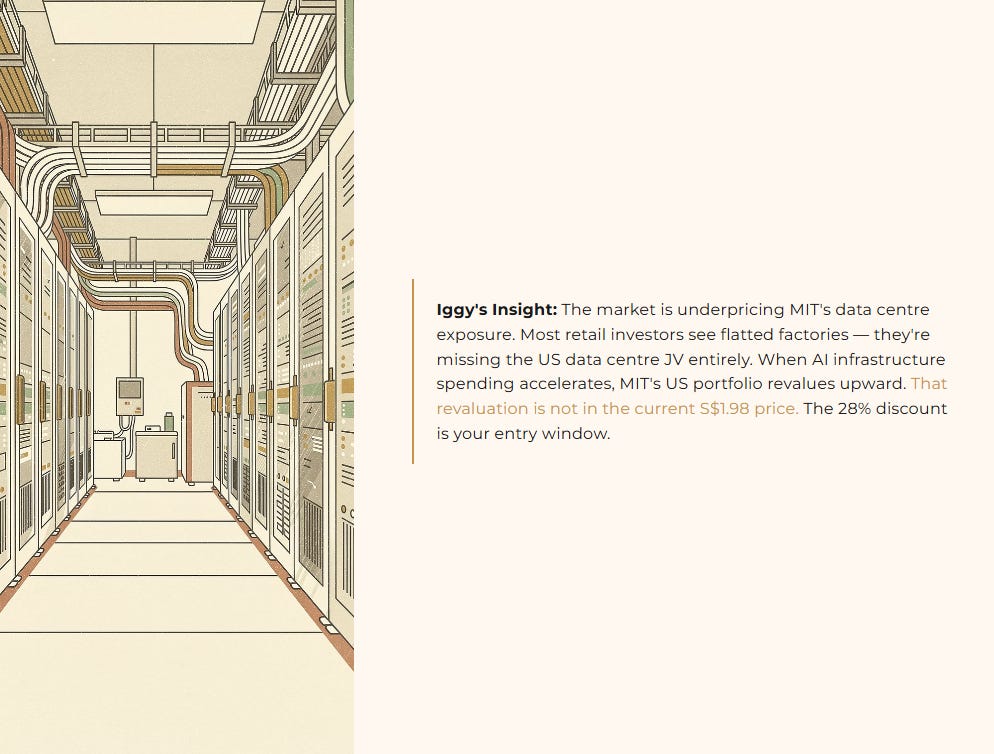

Iggy’s Insight The market is underpricing MIT’s data centre exposure. Most retail investors see an industrial REIT and think flatted factories. They are missing the US data centre JV entirely. When AI infrastructure spending accelerates, MIT’s US portfolio revalues upward. That revaluation is not fully reflected in today’s price. The valuation gap that independent models like InvestingPro are flagging is your entry window.

This sanctuary thesis holds as long as Singapore industrial land supply remains constrained and US data centre demand continues its structural expansion.

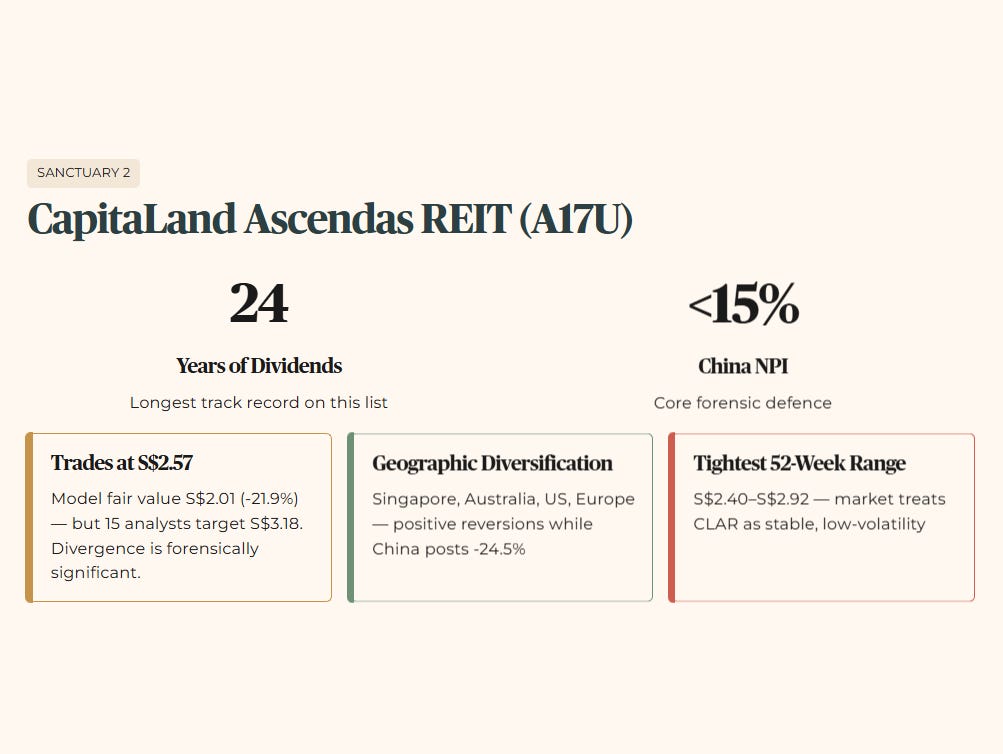

Sanctuary 2: CapitaLand Ascendas REIT (SGX: A17U)

CLAR is Singapore’s first and largest listed business space and industrial REIT — more than two decades of dividend payments is the longest track record on this list and the strongest forensic signal of distribution reliability.

The raw fact requires a nuanced reading. Model‑based fair values for CLAR are more divided: some quantitative screens flag mild downside from today’s price, while the sell‑side analyst community still sees upside. This divergence is forensically significant — the quantitative model and the analyst community are in disagreement, which means the sanctuary premium is genuinely contested. The trading range over the past year has been relatively tight compared with peers, confirming that the market treats CLAR as a stable, low‑volatility holding.

Historically, CLAR’s portfolio spans Singapore, Australia, the United States, and Europe — with China exposure well below 15% of total NPI. This geographic diversification is the core forensic defence. When CLCT’s China logistics parks are posting -24.5% rental reversions, CLAR’s Australian business parks and US logistics assets are generating positive or flat reversions in supply‑constrained markets.

In peer context, CLAR’s financial health scores — Cash Flow 3, Price Momentum 3, Profitability 3 — sit comfortably above CLCT’s across-the-board scores of 2. The 24-year dividend track record versus CLCT’s deteriorating DPU trajectory tells the entire story in a single comparison.

The forward scenario is stable rather than spectacular. CLAR is not going to deliver the capital upside of MIT’s undervaluation story. But for the 55-year-old Singaporean managing SRS capital, stability and 24 years of uninterrupted distributions is precisely what you need. The wallet impact is predictable quarterly income backed by genuine geographic diversification, not a China-concentration bet dressed up as a yield.

One forensic caution: the InvestingPro model’s 21.9% downside signal means CLAR’s sanctuary status is currently fully priced into the market. You are paying a premium for the safety — which is appropriate for retirement capital, but means the margin of safety on entry is thin at current levels.

This sanctuary thesis holds as long as CLAR’s non-China portfolio continues generating positive or flat rental reversions across its Singapore, Australian, and US assets.

Sanctuary 3: DBS Group (SGX: D05)

We are stepping outside the REIT universe for the third sanctuary — deliberately. When every REIT in the China-exposure cohort is showing forensic stress, the forensic question is not which China REIT is least bad. The question is whether the REIT universe is the right address for your retirement capital at all right now.

DBS answers that question directly. Based on its 2025 dividend, DBS currently yields a little above 5%, clearing our 4.7% forensic floor with room to spare. Its CET1 capital ratio sits comfortably above regulatory minima and far beyond what any commercial REIT can offer, giving you a fundamentally different loss‑absorption profile. DBS’s China footprint is primarily through banking relationships rather than owning commercial property, which is a very different exposure profile from a China‑heavy REIT.

The forward scenario is rate-sensitive but structurally sound. In a higher-for-longer rate environment, DBS’s net interest margin holds up. In a rate-cutting environment, its fee income and wealth management division provide an offset. Neither scenario involves Chinese logistics rental reversions or RMB translation losses eating your distribution.

The wallet impact for a retiree is clean, regulated, SGD-denominated income backed by a balance sheet the Singapore government would never allow to fail. That is not the same risk profile as a China‑exposed REIT relying on divestment gains and financial engineering to support its distributions.

The Three Red Flags

Red Flag 1: CapitaLand China Trust (SGX: AU8U)

“Is your yield a trap? Check the Health Score before you buy.” Stop trading on gut feelings. Get the same data the banks keep for themselves. Use code INVESTINGIGUANA to lock in your edge at half price. 💎

📈 [Verify Your Portfolio Safety Here]

This is where the 6.2% headline yield stops looking comforting and starts failing the forensic checklist—once you see how the gearing, interest coverage, and reliance on top‑ups from divestment gains actually line up, you will never look at a China REIT dividend the same way again…