CapitaLand Integrated Commercial Trust (CICT, SGX: C38U) – 3 Good, 3 Red Flags, and Iggy’s Verdict

CapitaLand Integrated Commercial Trust (CICT, SGX: C38U): Big Name, Big REIT—But Is It Still the Safe Choice?

Imagine picking the anchor store in Singapore’s REIT “shopping mall.” CICT has size, prime malls, and those shiny office towers—but does bulk mean better, or just bigger risk?

If you’re parking your CPF or SRS for stable payouts, CICT always catches your eye. Lately, it’s also been in the news for higher dividends (DPU) and expansion. But SG investors often ask: are the payouts as steady as they look, or is something shifting under the surface?

Let’s break it down. Here are 3 wins, 3 red flags, and the honest outlook for those eyeing income with peace of mind.

Company Snapshot: Why Look at CICT Now?

CapitaLand Integrated Commercial Trust (CICT, SGX: C38U) is Singapore’s flagship commercial REIT. It owns 26 properties across Singapore, Germany, and Australia—but almost all (95%) are right here in the Lion City. Its blue-chip sponsor, CapitaLand Investment, gives CICT serious scale and local edge.

In 1H2025, CICT doubled down on premium offices, launched new upgrades, and kept leverage under that key 40% ceiling CPF/SRS investors love. Steady payouts stay in focus.

Valuation & Income at a Glance (as of Aug 2025):

At present, CICT trades just above book—pretty standard for SG blue-chip REITs. The yield is a little below its 5-year average, but still attractive if you want CPF/SRS-safe income. Debt is well-managed for now, but keep an eye on leverage if rates stay higher for longer, okay?

The 3 Good

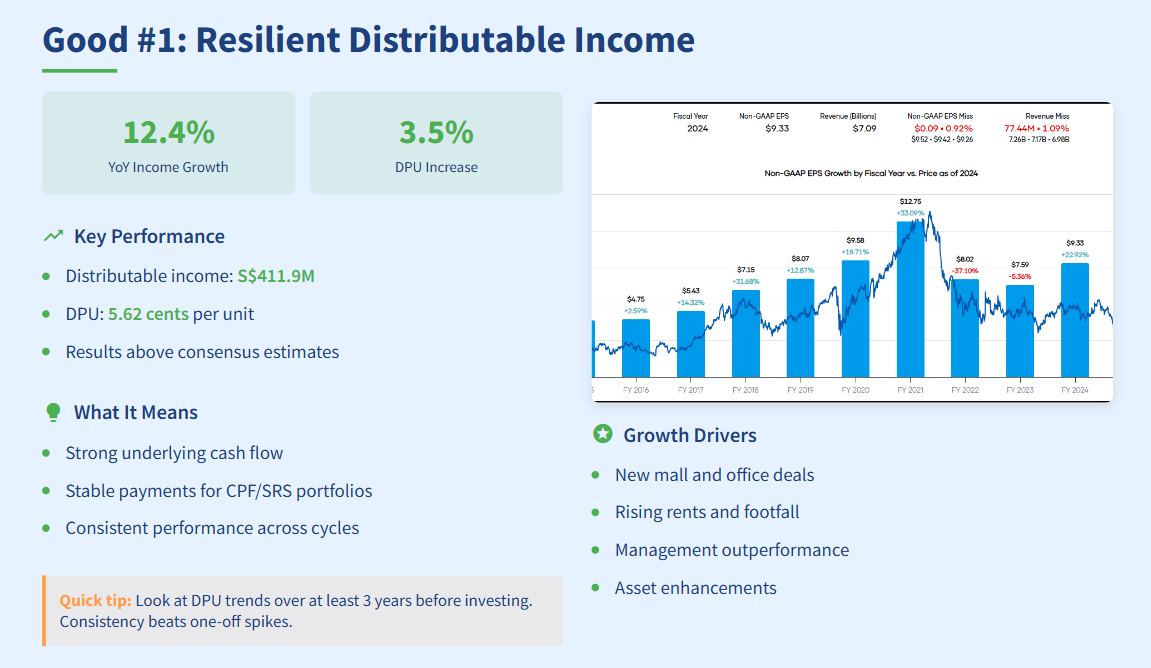

Good #1: Resilient Distributable Income and Steady DPU Growth

CICT turned in a strong 1H2025. Distributable income climbed 12.4% year-on-year to S$411.9 million, while DPU grew 3.5% to 5.62 cents per unit. That means more money lands in unitholders’ pockets—even with higher costs and interest rates.

What boosted income?

New mall and office deals: Fresh acquisitions and asset upgrades added to returns.

Rising rents and footfall: More visitors and higher rents at key properties lifted profits.

Smart management: Results beat market expectations, showing a knack for timing.

Why does this matter for you?

DPU growth shows strong, steady cash flow—perfect for CPF, SRS, and yield-focused investors.

If you want payouts that keep rising (not wild swings!), this record signals reliability.

Quick tip: Always check DPU trends covering at least three years before buying. Consistency wins over flashy, one-off spikes. Short bursts look good, but real strength shows up over cycles. CICT proves it delivers—even when things get rough.