CAREIT 1Q 2026: Debt Hits 31% While Yield Stays 7.47% (Earnings Deep Dive)

No low leverage means no safety net, no sleep comfort, no buffer when rates rise for CAREIT holders

Centurion Accommodation REIT (CARE) — 1Q 2026 Earnings Audit

The headline says revenue beat. The footnotes say something else entirely.

If you are holding this for retirement income, the capital structure shift that happened in a single quarter deserves more of your attention than the 2.7% revenue variance. Aggregate leverage moved from 22.1% to 31.0% in ninety days. That is not organic growth. That is a bet — and you are the one holding the position if it does not pay off.

My job is simple, even if the balance sheet is not. I read the numbers that the headline skips — the interest coverage, the gearing, the free cash flow sustainability — so that the Singaporean building or living off a dividend portfolio gets the same forensic clarity that institutional money takes for granted.

In This Article:

The Slide by Slide Audit

Iggys Insight The Financing Cost Illusion

The Reality Check

The Scorecard

The Forward Outlook

Iggys Insight The Engineered Yield Beneath the Master Lease

Forensic Classification

Iggys Forensic Disclaimer

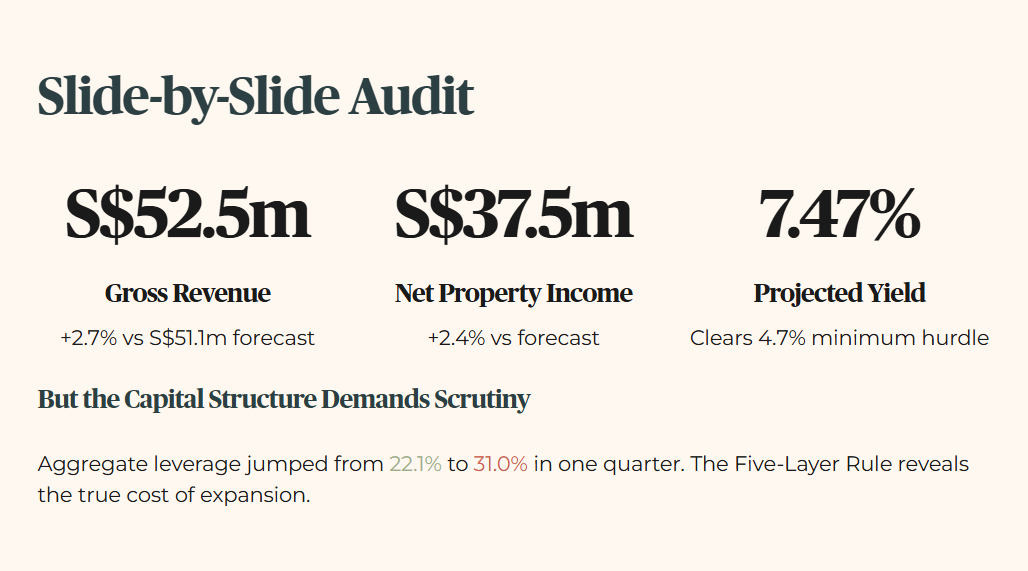

1. The Slide-by-Slide Audit

For a REIT, we always lead with yield sustainability and capital structure. Centurion Accommodation REIT reported gross revenue of S$52.5 million for 1Q 2026. That is a 2.7% variance above the projected S$51.1 million. Net Property Income followed, hitting S$37.5 million, which is 2.4% higher than the forecast. The projected yield stands at 7.47%, comfortably clearing the 4.7% minimum hurdle. For a retail investor looking for cash flow, this headline performance looks solid.

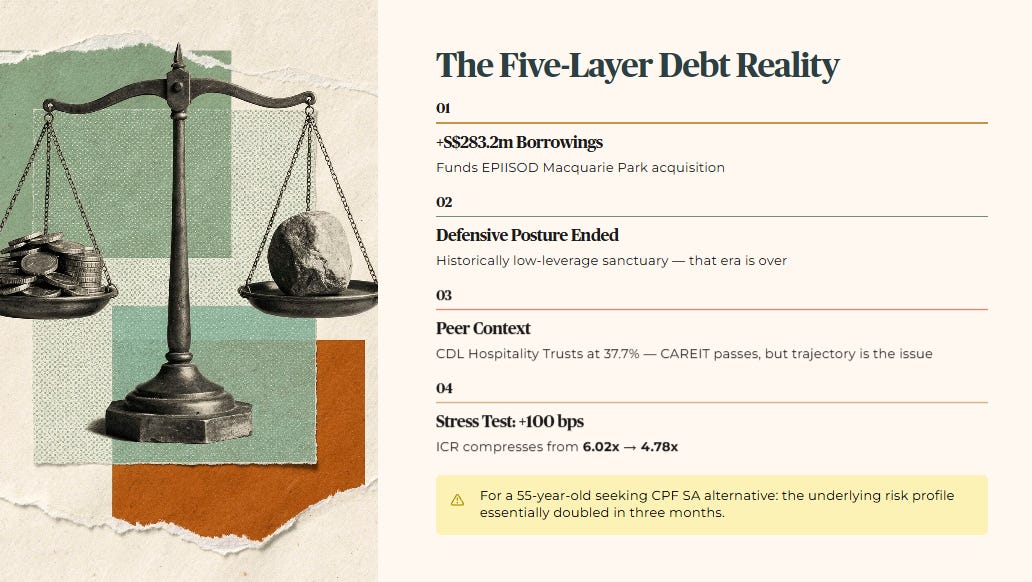

However, the capital structure demands severe forensic scrutiny. The aggregate leverage jumped from 22.1% at end-December 2025 to 31.0% by 31 March 2026. Applying the Five-Layer Rule to this shift reveals the true cost of expansion.

First, gross borrowings increased by S$283.2 million to fund the EPIISOD Macquarie Park acquisition. Second, this trust historically operated as a low-leverage sanctuary vehicle. This sudden spike ends that defensive posture. Third, looking at SGX peers, CDL Hospitality Trusts operates with 37.7% gearing. CAREIT currently passes the peer comparison, but the rapid trajectory of its debt accumulation is the core issue. Fourth, a forward stress test shows that a 100 basis point increase in weighted average interest rates would compress the Interest Coverage Ratio from 6.02x to 4.78x.

The wallet impact for a 55-year-old investor seeking a CPF Special Account alternative is clear. The underlying risk profile of this asset essentially doubled in three months to secure that yield.

The portfolio valuation increased by 16.5% to S$2.19 billion. This is not organic growth. It is entirely driven by the inorganic addition of the Australian asset and new blocks in Singapore. The reporting also confirms that the revenue beat was partially bolstered by a strengthening British Pound and Australian Dollar against the Singapore Dollar.

The Purpose-Built Workers Accommodation segment remains the anchor, contributing 71.9% of net property income. Occupancy in Singapore hit 94.0%. This is operationally strong, but the looming transition standards risk means capacity will eventually shrink unless significant capital expenditure is deployed.

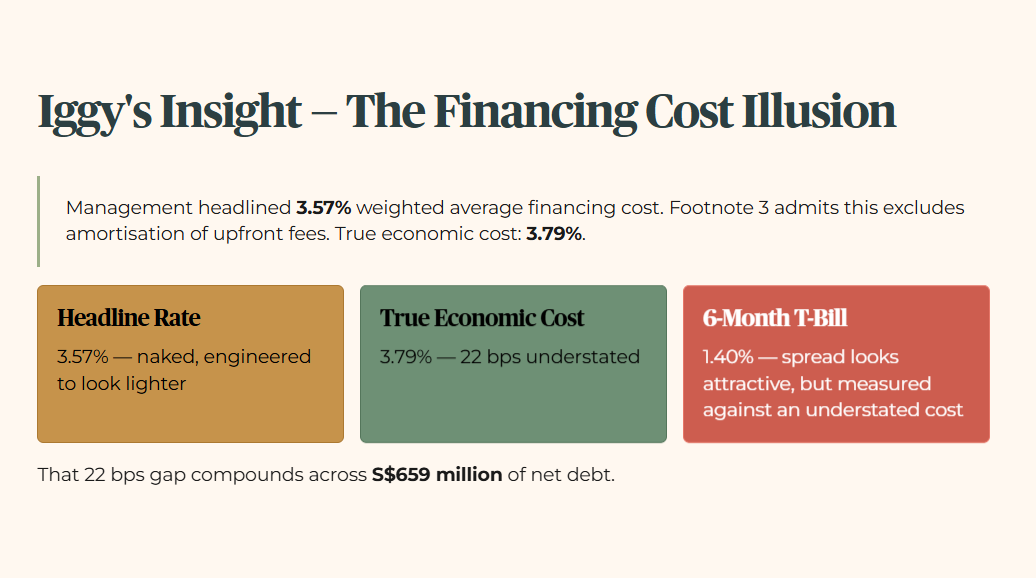

Iggy’s Insight — The Financing Cost Illusion

Management spotlighted their 3.57% weighted average financing cost. They spent almost no time explaining Footnote 3 on Page 5. That footnote admits the 3.57% figure excludes the amortisation of upfront and other fees. When you include the actual costs of securing that debt, the true economic cost rises to 3.79%. Headlining the lower, naked rate is a classic engineered yield tactic designed to make the debt burden look lighter than it is. The 6-month T-Bill currently yields 1.40% — down from 1.47% at the prior auction. The spread looks attractive on the surface. What management did not headline is that the spread is being measured against a cost figure that understates the true economic burden by 22 basis points. That gap compounds across S$659 million of net debt.

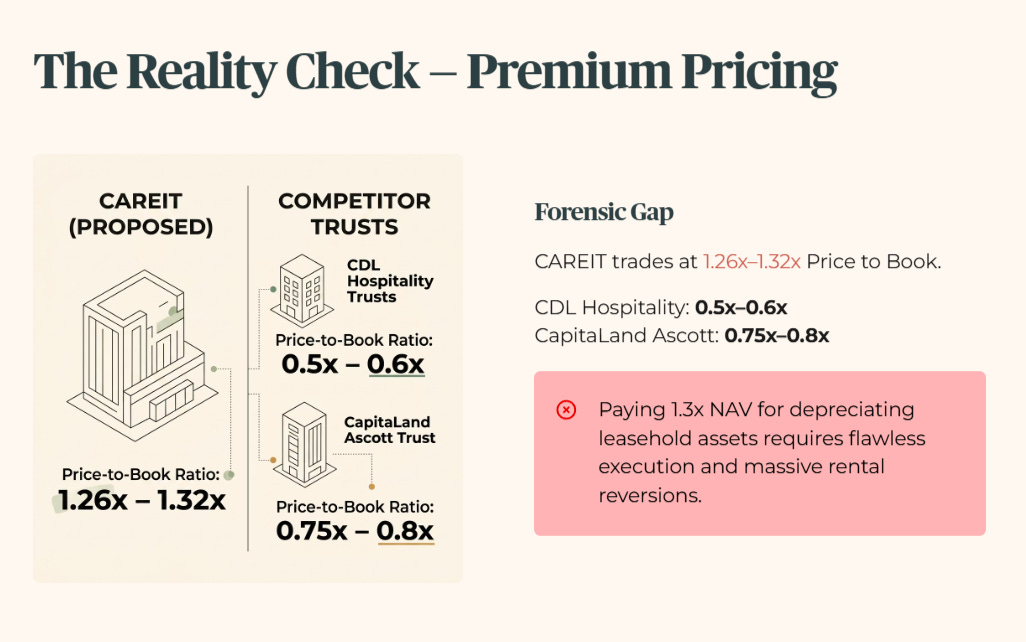

2. The Reality Check

The market is currently pricing CAREIT at a significant premium to its fundamental value. The stock trades at a Price to Book ratio of 1.26x to 1.32x. This creates a glaring Forensic Gap.

When you contrast this with established peers, the divergence is stark. CDL Hospitality Trusts trades at a 0.5x to 0.6x multiple, while CapitaLand Ascott Trust sits at 0.75x to 0.8x. Paying 1.3x Net Asset Value for a REIT holding depreciating leasehold assets requires flawless execution and massive rental reversions.

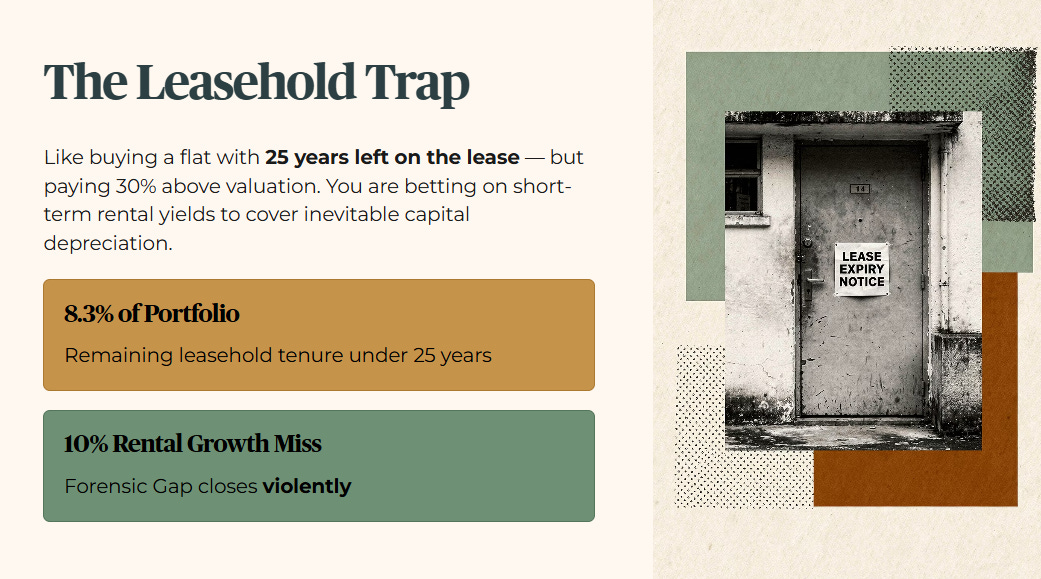

Think of it like buying a flat with only 25 years left on the lease, but paying 30% above the recent valuation price. You are betting entirely on short-term rental yields to cover the inevitable capital depreciation. Currently, 8.3% of the CAREIT portfolio by valuation has a remaining leasehold tenure of less than 25 years. If management guidance on rental growth falters by even 10%, this Forensic Gap will close violently.

3. The Scorecard

Note on the Stress-Test Buffer: For this audit, I apply a conservative floor of 3.2%. We audit for the storm, not just the sunny day. The 6-month T-Bill currently sits at 1.40% — down from 1.47% at the prior auction. I do not lower my forensic standards to match a temporary rate trough. My floor remains at 3.2% to ensure sanctuary assets can withstand a return to long-term average interest rates. The minimum yield hurdle is 4.7% — that is the 3.2% floor plus 150 basis points of mandatory risk premium.

Table 1 — Income Sustainability