CareShield Life 2026: Smart Strategies for Rising Premiums

CareShield Life's 2026 changes will cost you more but pay out 75% higher—here's how to prepare your MediSave and maximize the new benefits without overpaying for supplements.

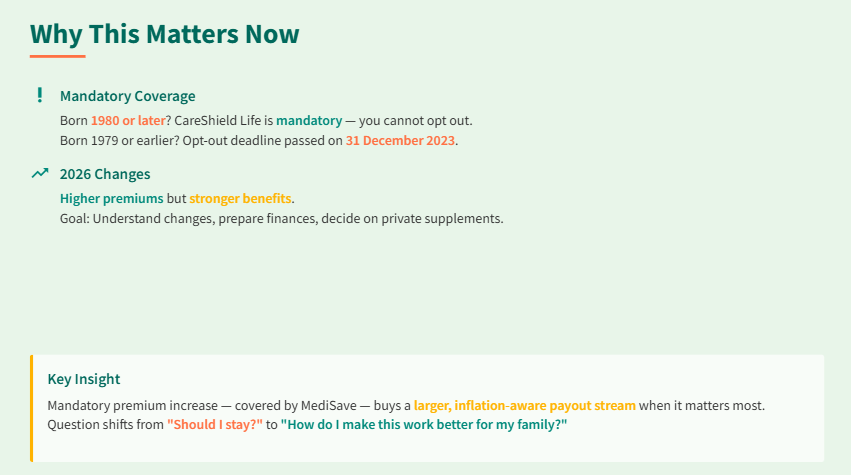

Important clarification first: If you're born in 1980 or later, CareShield Life is mandatory—you cannot opt out. If you're born in 1979 or earlier and were auto-enrolled, the opt-out deadline passed on 31 December 2023. For most readers, this isn't about whether to stay—it's about how to optimize what you already have.

The 2026 changes bring higher premiums but also stronger benefits. Since you're staying anyway, the goal is to understand what's coming, prepare your finances, and decide if private supplements make sense.

Here's the key insight: a mandatory premium increase—covered by MediSave—buys a much larger, inflation-aware payout stream when it matters most. The question shifts from "Should I stay?" to "How do I make this work better for my family?"

What is changing from 2026

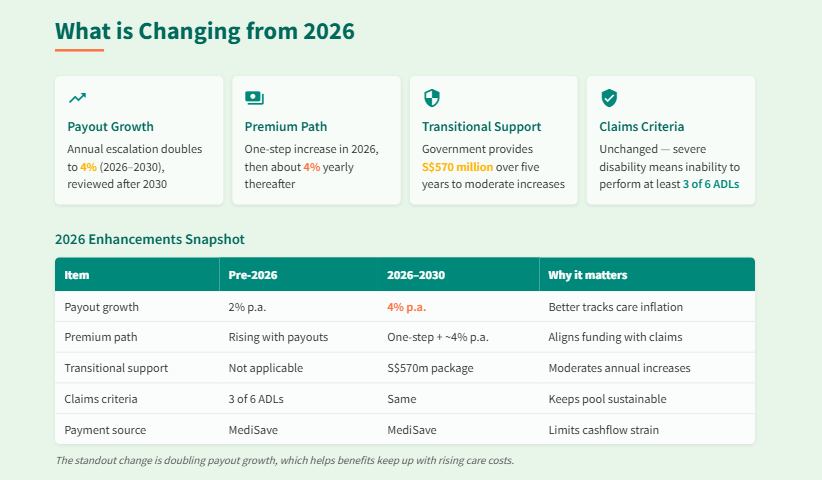

Payout growth: Annual escalation doubles to 4% (2026–2030), reviewed after 2030

Premium path: One-step increase in 2026, then about 4% yearly thereafter

Transitional support: Government provides S$570 million over five years to moderate increases

Claims criteria: Unchanged—severe disability means inability to perform at least 3 of 6 Activities of Daily Living (ADLs)

Administration: Coverage remains compulsory for those born 1980+; premiums fully MediSave-payable

Caption: The standout change is doubling payout growth, which helps benefits keep up with rising care costs. Transitional support tempers premium increases so households can maintain coverage without large cash outlays.