Understanding RevPAR vs NPI: Why Your REIT Dividends Are Leaking

Is your REIT a busy chicken rice stall with no profit? Let’s check the gas bill.

Forensic Audit: Singapore Hospitality REITs (S-REITs) – Q1 2026 Performance

The News Hook:

The hospitality sector in early 2026 is feeling the heat—and not just from the Year of the Fire Horse. Recent performance updates for Singapore’s heavyweights—CDL Hospitality Trusts (CDREIT), Far East Hospitality Trust (FEHT), and CapitaLand Ascott Trust (CLAS)—reveal a sector caught between two worlds: resilient international tourism and the cold reality of plateauing room rates. While headlines cheer for the “Return of the Traveler,” the ledger tells a more nuanced story of rising operational costs and the “Yield Trap” of expiring hedges.

The Contrarian Truth:

Market sentiment is currently high on “Recovery” fumes, but the forensic truth is that Revenue Per Available Room (RevPAR) growth is slowing. We are seeing a “Forensic Gap” where busy hotels aren’t necessarily translating into busy wallets for shareholders. It’s like a popular chicken rice seller with a never-ending queue—if the cost of poultry, electricity, and labor outpaces his price hikes, his actual profit spread is thinner than a neighborhood auntie’s patience at the 4D counter. We aren’t just looking for full beds; we are looking for the cash that survives the journey to the bottom line.

In This Article:

The Masterclass:

Step 1: The Health Check (Balance Sheet & Solvency)

Step 2: The Wealth Check (Cash Flow & Yield)

Step 3: The Price Check (Valuation & Peers)

Step 4: The Future Check (Scenarios & Fair Value)

Step 5: The Future Check (Scenarios & Fair Value)

The Bottom Line (Strategic Conclusion)

InvestingPro Reality Check

Iggy's VerdictAbout Iggy & the Elite 170

🦎 Join the Inner Circle: Optimize Your Informational Latency: I am Iggy, the voice of The Investing Iguana. We are a high-conviction group of 170 Elite Members—private investors and retirees who value the audit over the hype. We don’t chase “insane” returns; we build an Iron Bastion of capital protected by math, not hope.In the Singapore market, the gap between a calculated entry and becoming a liquidity provider for others is often just 48 hours. While 5,800+ readers wait two weeks for the “Old News” version, my Inner Circle observes the data while the market structure is still evolving.

🚨 Mitigate Informational Lag: Free subscribers wait 14 days to see my analysis. In this jungle, informational asymmetry is a primary driver of portfolio variance. Access the data while the market dynamics are still being priced in.

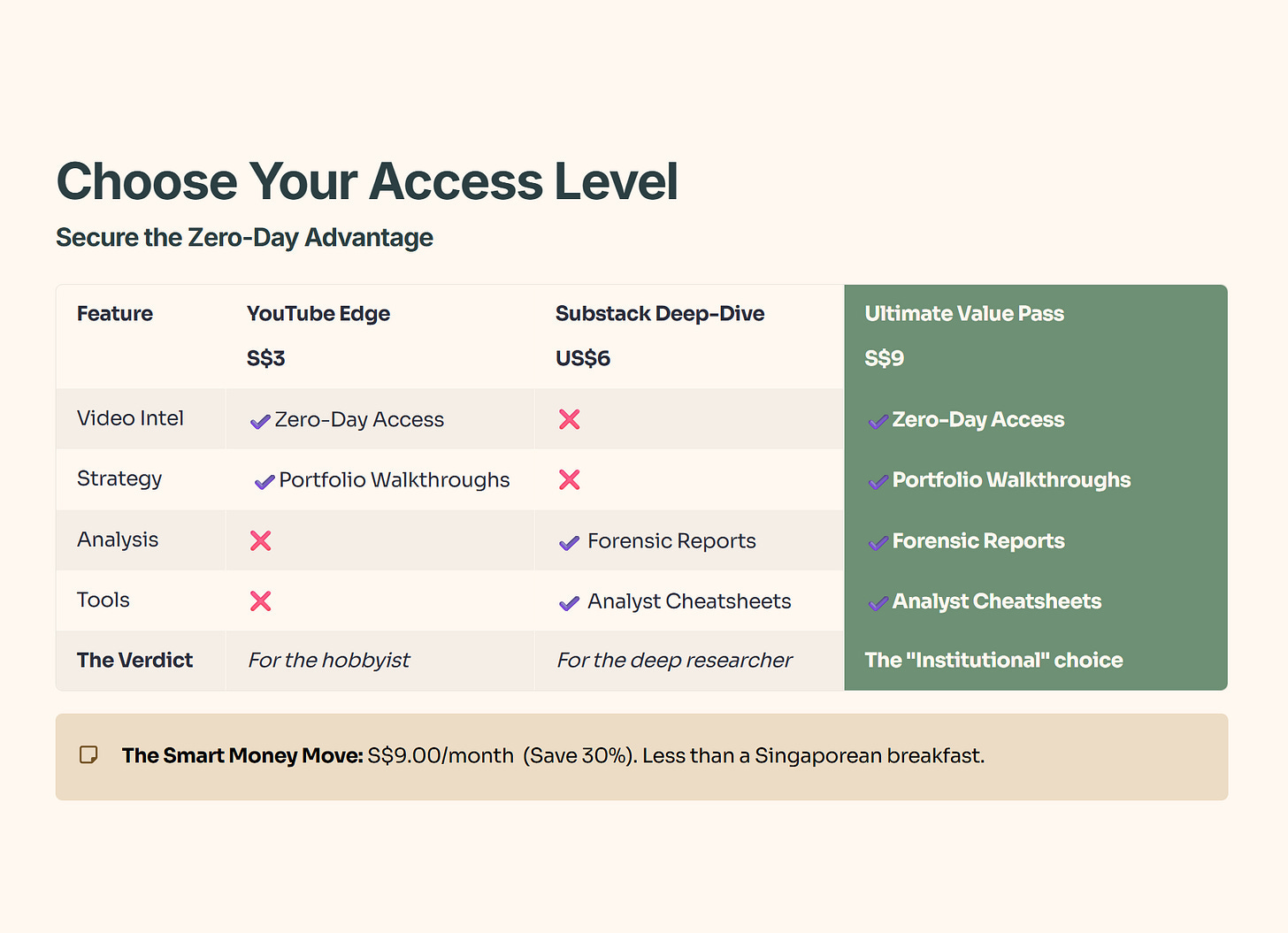

Choose Your Edge:

⚡ Zero-Day Access: Observe every deep-dive video the second it’s rendered. No delays, no missed data points.

📂 The Forensic Vault: Access the full forensic reports and portfolio walkthroughs where I strip away the corporate hype to reveal the hard math behind every Singapore blue chip.

💎 The “Smart Money” Bundle: Secure the full S$9/mo Pass (YouTube + Substack).

It’s a nominal overhead—less than the cost of two coffees at Toast Box—to analyze the market with the same datasets as institutional participants.

Get the data while it’s fresh. 👉 Join the Inner Circle Here

The Masterclass:

🎓 Educational Note: RevPAR vs. NPI

RevPAR (Revenue Per Available Room) is a top-line metric calculated by dividing total room revenue by the number of available rooms. However, NPI (Net Property Income) is what remains after paying for staff, maintenance, and the “mint on the pillow.” A rising RevPAR with a falling NPI signals a cost-of-living crisis within the REIT’s balance sheet.

2. Step 1: The Health Check (Balance Sheet & Solvency)

The narrative here is about the Floor. In this Fire Horse year of high volatility, leverage is the difference between a fortress and a house of cards. With the macro environment shifting toward balance sheet reduction, cheap money isn’t coming back to rescue the over-leveraged. We look at Gearing (debt vs. assets) and Interest Coverage (how easily they pay their bank fees).

Financial Health Checklist

Forensic Audit of CDREIT:

A closer look at the audit logs reveals that short-term obligations currently exceed liquid assets for CDREIT. This is a common hurdle for REITs managing multi-year renovations, but it demands tight liquidity management. While net income is expected to grow this year following the completion of major refurbishments at flagship properties, the market currently ranks their “Profitability Health” at the lowest possible tier (1 out of 5) compared to regional peers.

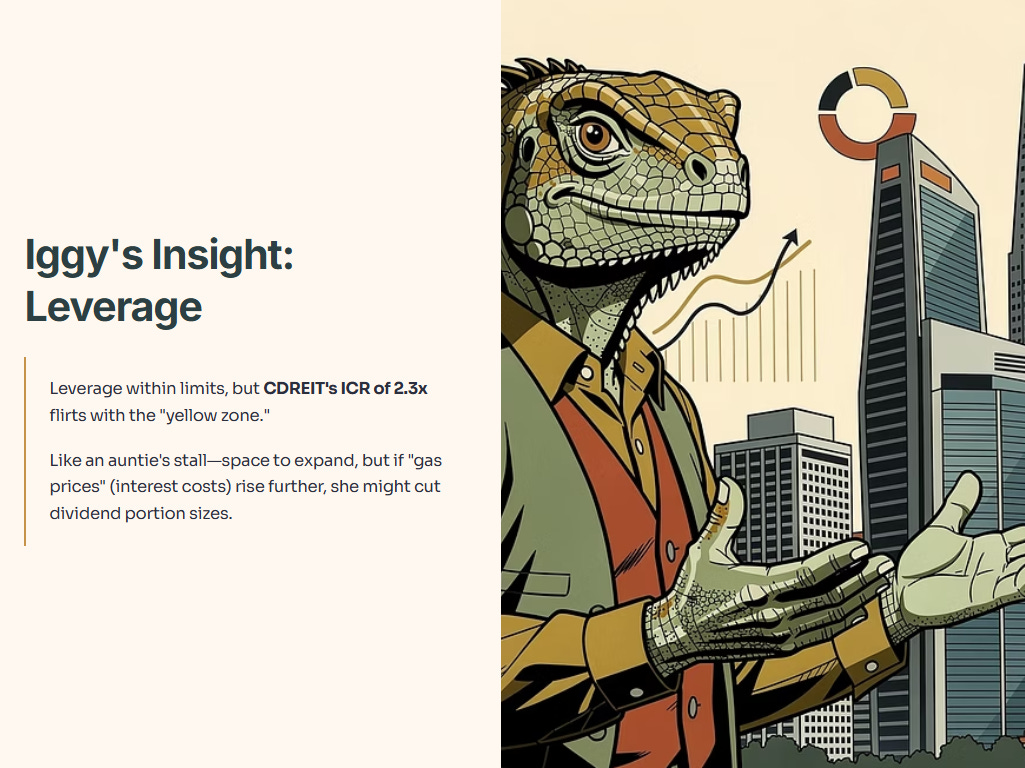

🦎 Iggy’s Insight: Leverage is within limits, but CDREIT’s ICR of 2.3x is flirting with the “yellow zone.” It’s like an auntie’s stall—she has the space to expand, but if the “gas prices” (interest costs) rise any further, she might have to cut the portion size of her dividends to stay afloat.

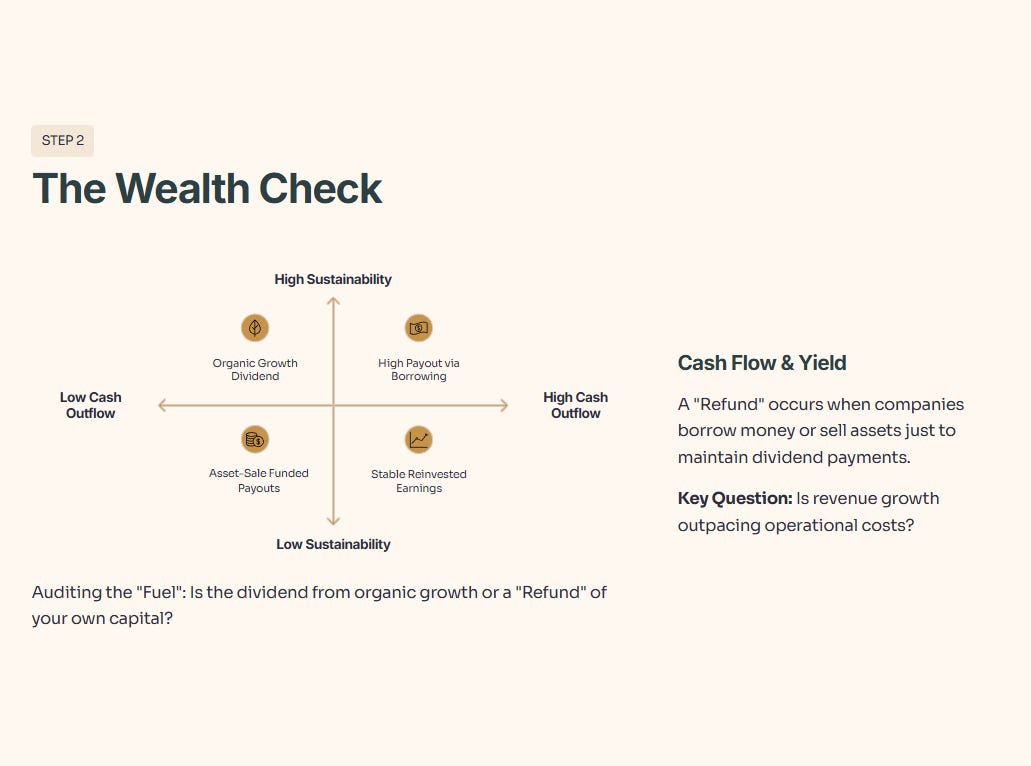

3. Step 2: The Wealth Check (Cash Flow & Yield)

We audit the “Fuel” here. Is the dividend coming from organic growth, or is it a “Refund” of your own capital? A “Refund” occurs when a company borrows money or sells its own furniture just to keep paying you a dividend.

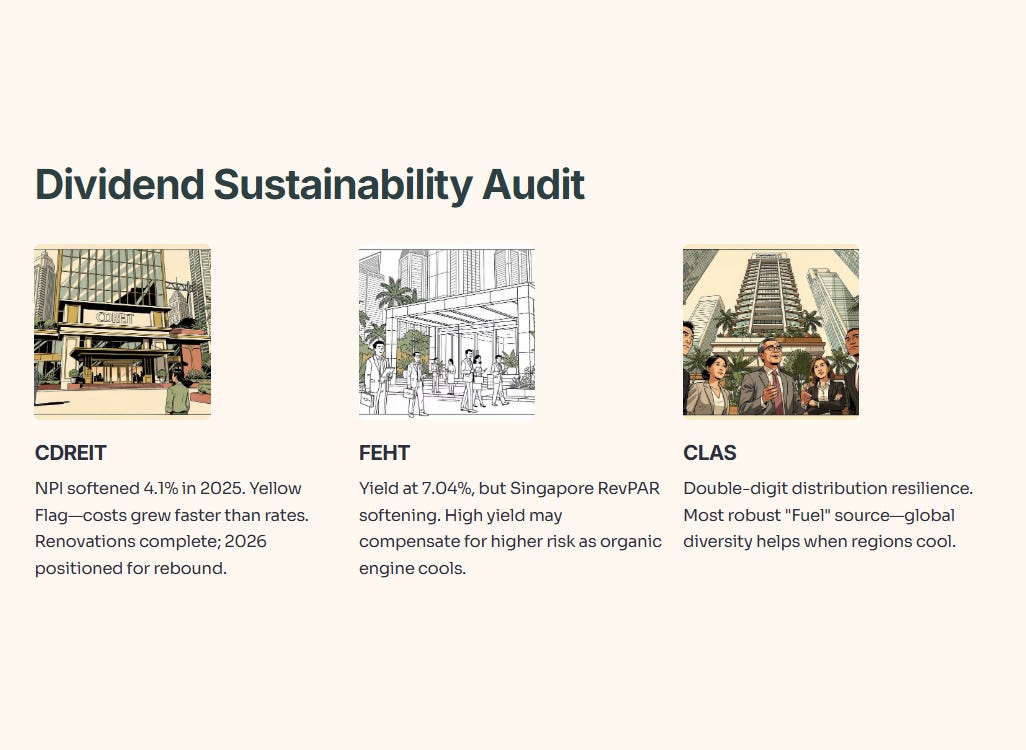

Dividend Sustainability Audit

CDL Hospitality Trusts (CDREIT) Net Property Income (NPI) for the full year 2025 softened by 4.1%. This is a “Yellow Flag”—revenue is holding, but the “leaks” (operational costs) grew faster than room rates. However, with renovations finished, 2026 is positioned as a “rebound” year.

Far East Hospitality Trust (FEHT): Yield looks incredibly high at 7.04%, but Singapore RevPAR is softening. This suggests the organic engine is cooling, and the high yield might be a compensation for higher risk.

CapitaLand Ascott Trust (CLAS): Distribution income has shown double-digit resilience. This is currently the most robust “Fuel” source in the group, showing that global diversity helps when one region gets cold.

“Now that we know which REITs have ‘fuel’ and which have ‘leaks,’ the next step is the part that decides whether this is a safe yield—or a yield trap: the exact pricing and valuation signals.”