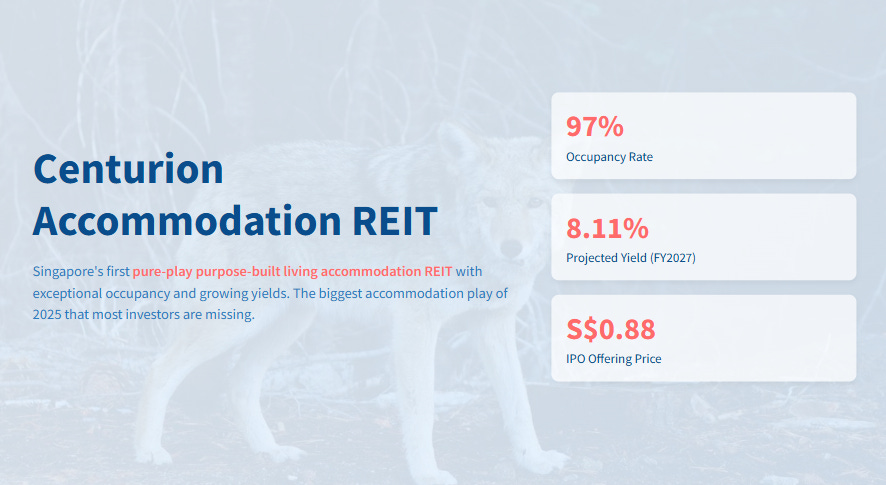

Centurion REIT IPO: 8.11% Yield & Global Housing Exposure — Is It SG’s Next Income Giant?

Most Singapore investors are missing the biggest accommodation play of 2025—while focusing on tired hospitality REITs, a pure-play accommodation giant with 97% occupancy and growing 8%+ yields .......

Most Singapore investors are missing the biggest accommodation play of 2025—while focusing on tired hospitality REITs, a pure-play accommodation giant with 97% occupancy and growing 8%+ yields is about to hit the market at a discount.

The Singapore REIT scene has been starving for fresh blood. After years of watching the same hospitality names struggle with post-COVID recovery and cyclical headwinds, investors finally have something genuinely different to consider. Centurion Accommodation REIT isn't just another hotel play dressed up with fancy marketing—it's the first pure-play purpose-built living accommodation REIT in Singapore, backed by a parent company that's been quietly dominating the worker and student accommodation space for over a decade.

But here's what most investors are getting wrong about this IPO. They're treating it like another speculative listing when the fundamentals tell a completely different story. With 96.9% occupancy across Singapore worker accommodation and 96.8% across international student housing, plus projected yields climbing from 7.47% to 8.11%, this REIT is launching with metrics that established players would envy.

The bigger question isn't whether Centurion Accommodation REIT deserves your attention—it's whether you can afford to miss what could be the most compelling income story Singapore has seen all year.

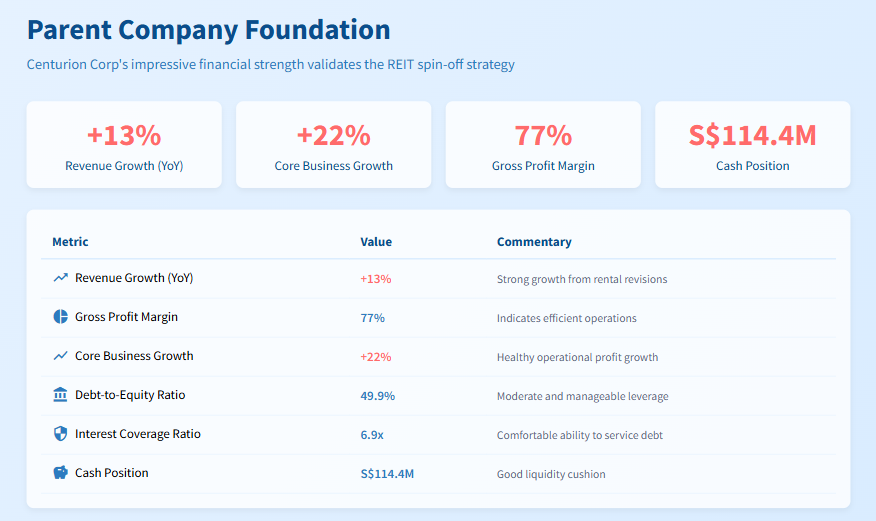

The Parent Company Foundation: Why Centurion Corp's Strength Matters

Understanding Centurion Accommodation REIT means first understanding the powerhouse behind it. Centurion Corporation delivered impressive first-half 2025 results that directly validate the REIT spin-off strategy. Revenue jumped 13% year-over-year to S$140.7 million in 1H 2025, driven by positive rental revisions across all properties and strong occupancies in Singapore. More importantly, the core business—excluding volatile fair value adjustments—grew net profit by 22% to S$65.4 million. This isn't financial engineering; it's genuine operational improvement.

This table outlines Centurion Corporation's key financial results for the first half of 2025. It shows a company with remarkable operational growth, healthy profit margins, and a prudent balance sheet. This underlying strength provides a stable foundation for the new REIT and its future prospects.

What makes these numbers particularly compelling is the diversification story. Centurion operates 37 assets but is only placing 14 of the most suitable ones into the REIT. This selective approach means the REIT gets premium assets while the parent company retains growth optionality across other markets, particularly Malaysia where it plans to double bed capacity over five years.

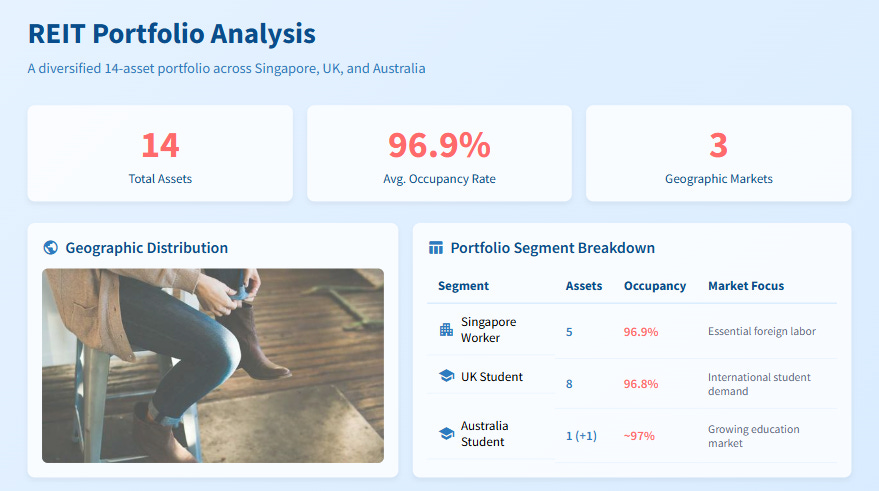

Dissecting the REIT: Portfolio Quality and Geographic Strategy

Centurion Accommodation REIT's initial portfolio tells a sophisticated diversification story that addresses multiple demographic and economic trends simultaneously. The 14-asset portfolio splits strategically: five purpose-built worker accommodation (PBWA) assets in Singapore, eight purpose-built student accommodation (PBSA) assets in the UK, and one PBSA in Australia, with plans to add another Australian property post-listing. This geographic spread is intentional—Singapore for steady government-supported foreign worker demand, the UK for robust international student flows, and Australia for a growing education market.

Table: Portfolio Segment Breakdown by Geography & Asset Type

This table shows the REIT’s balanced portfolio across Singapore, the UK, and Australia. By targeting different long-term demographic trends in each country, the portfolio builds in a layer of resilience that single-market or single-purpose REITs lack.

The occupancy metrics reveal operational excellence. Singapore PBWA assets maintain 96.9% occupancy while international PBSA properties achieve 96.8% occupancy. These aren't temporary peaks; they reflect sustained demand. Revenue growth patterns validate this resilience. Singapore worker accommodation rents grew significantly from FY2022 to FY2024, while student accommodation rents also increased at a healthy clip. Both growth rates demonstrate pricing power.