CICT C38U: 3 Greens and 3 Red Flags on the REIT Everyone Owns But Few Have Audited

If CapitaLand Integrated Commercial Trust is in your CPF or SRS portfolio, here are the three numbers your broker never told you to check.

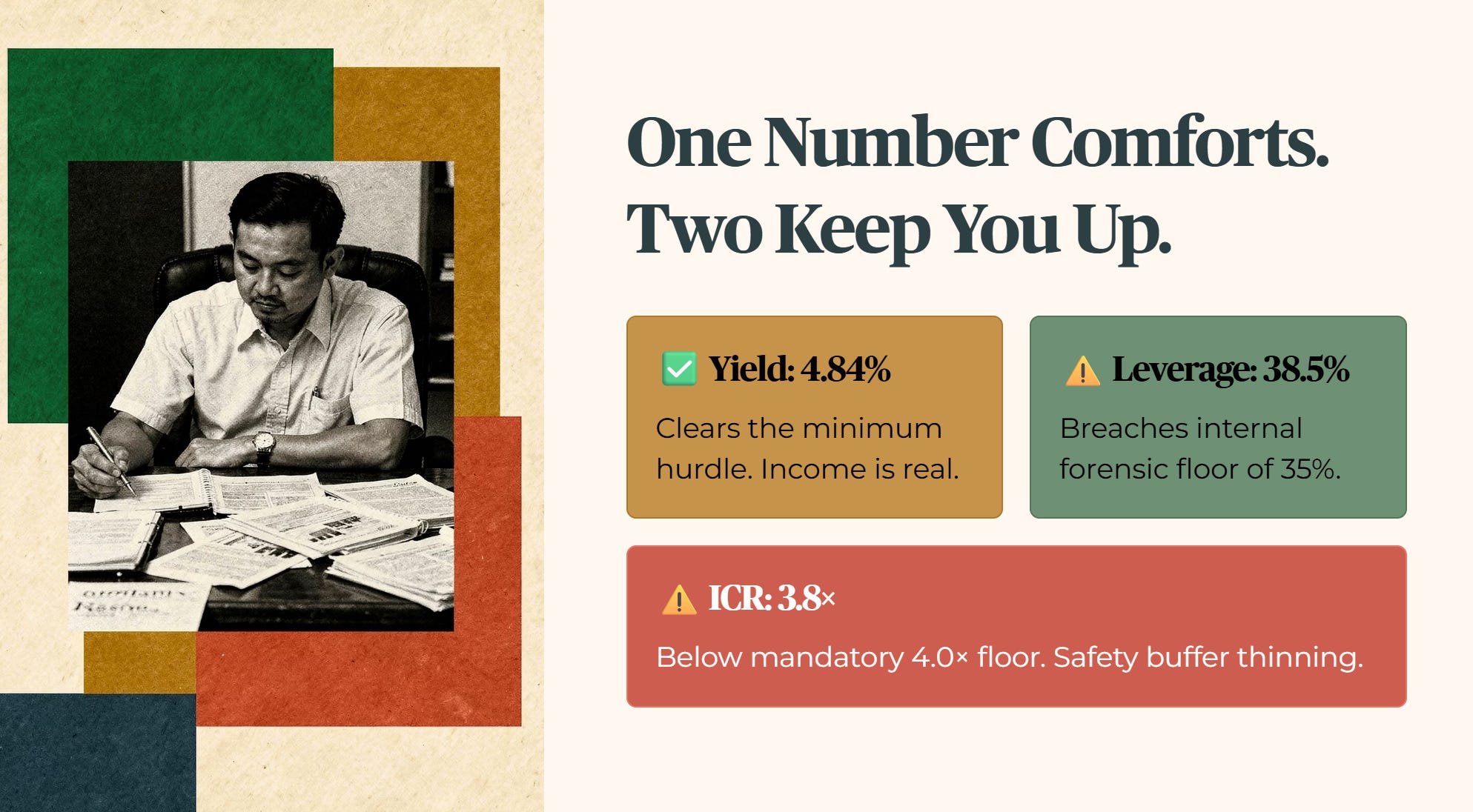

One number in this audit will comfort you. The other two will keep you up at night. CapitaLand Integrated Commercial Trust is paying a trailing yield of 4.84%, the income is real, and it clears my minimum hurdle. But the aggregate leverage, the proportion of this trust’s total assets funded by borrowed money, sits at 38.5%. The interest coverage ratio, which measures how comfortably the trust’s earnings cover its interest bill, has compressed to 3.8 times. Both figures breach my internal forensic floors. If you are holding this for retirement income, here is exactly what the balance sheet audit found.

The Financial Snapshot

The 3 Good (The Bull Case)

Good 1: The Yield is Real and Clearing the Bar

Good 2: Scale, Sponsor, and Disciplined Capital Management

Good 3: The Paragon Acquisition is Strategically Sound and DPU Accretive

The 3 Red Flags (The Bear Case)

Red Flag 1: Gearing is Outside My Range

Red Flag 2: The Interest Coverage Ratio is Below My Floor

Red Flag 3: Office Occupancy Has Fallen Below the Prime Asset Floor

The Window Is Already Open

The Window Closes Fast.

Iggy’s Elite Investors

The Singaporean Context

The Weighing Scale

Iggy’s Insight Block 1

Iggy’s Insight Block 2

Iggy’s Conclusion

Iggy’s Forensic Disclaimer

The Financial Snapshot

CapitaLand Integrated Commercial Trust has delivered operating performance that clears my baseline income hurdle. The distribution is real, supported by organic property income growth and contributions from major assets including the fully consolidated CapitaSpring and the completed Gallileo handover in Frankfurt. But when you look at the capital structure, the safety buffers are thinning.

The yield looks attractive until you read the balance sheet behind it.

All figures in this audit are sourced from CapitaLand Integrated Commercial Trust’s 1Q 2026 Business Update, published 24 April 2026, available on CICT’s official investor website at cict.com.sg. This is the primary source of truth for all financial and operational metrics referenced below.

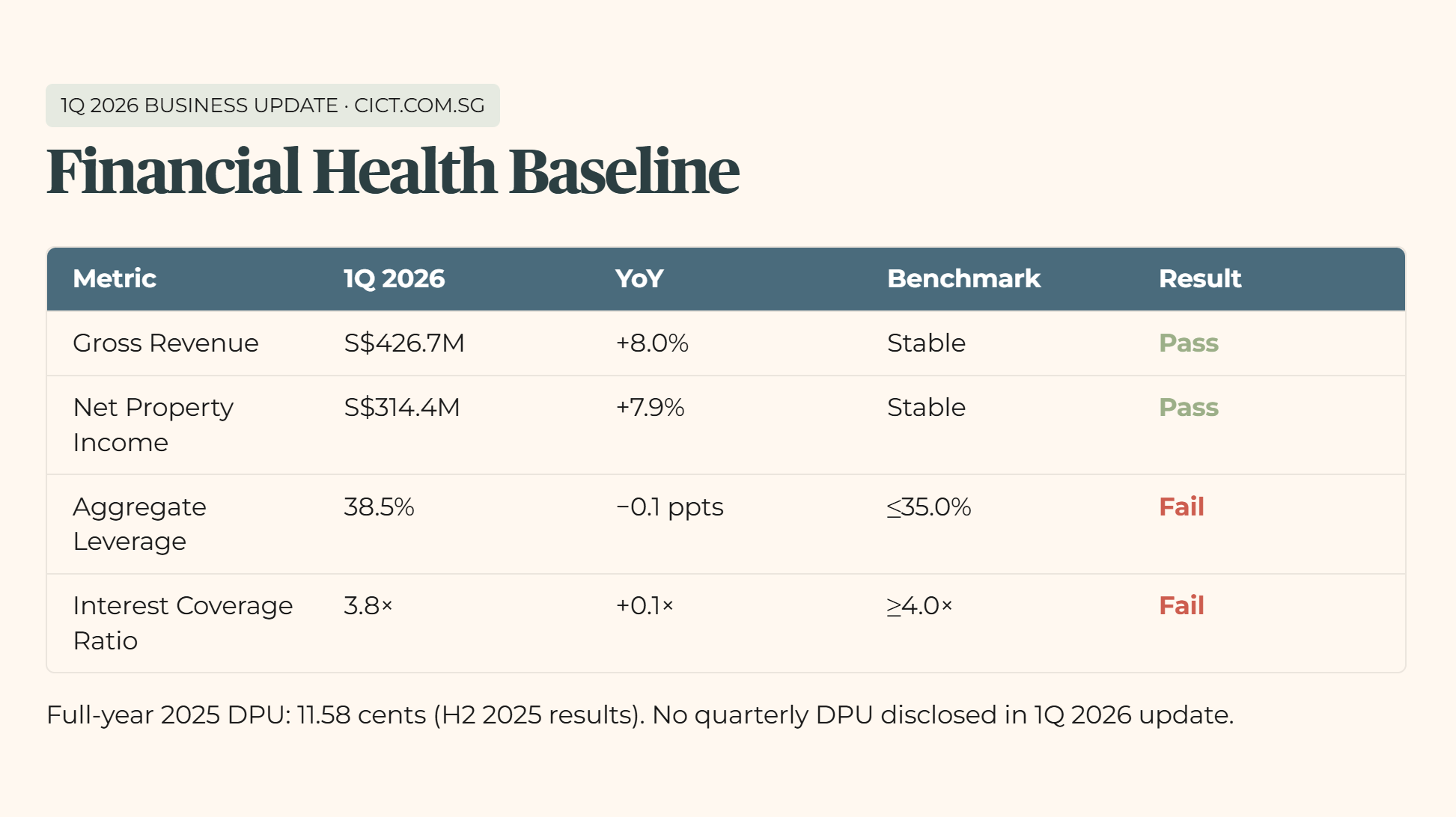

Financial Health Baseline: CapitaLand Integrated Commercial Trust (C38U)

Note on DPU: The 1Q 2026 Business Update does not disclose a quarterly DPU figure. Full-year 2025 DPU of 11.58 cents is sourced from CICT’s H2 2025 results. A peer comparison table has been omitted as peer data was not available for this audit cycle.

My job is simple, even if the balance sheet is not. I read the numbers that the headline skips, the interest coverage, the gearing, the free cash flow sustainability, so that the Singaporean building or living off a dividend portfolio gets the same forensic clarity that institutional money takes for granted.

The 3 Good (The Bull Case)

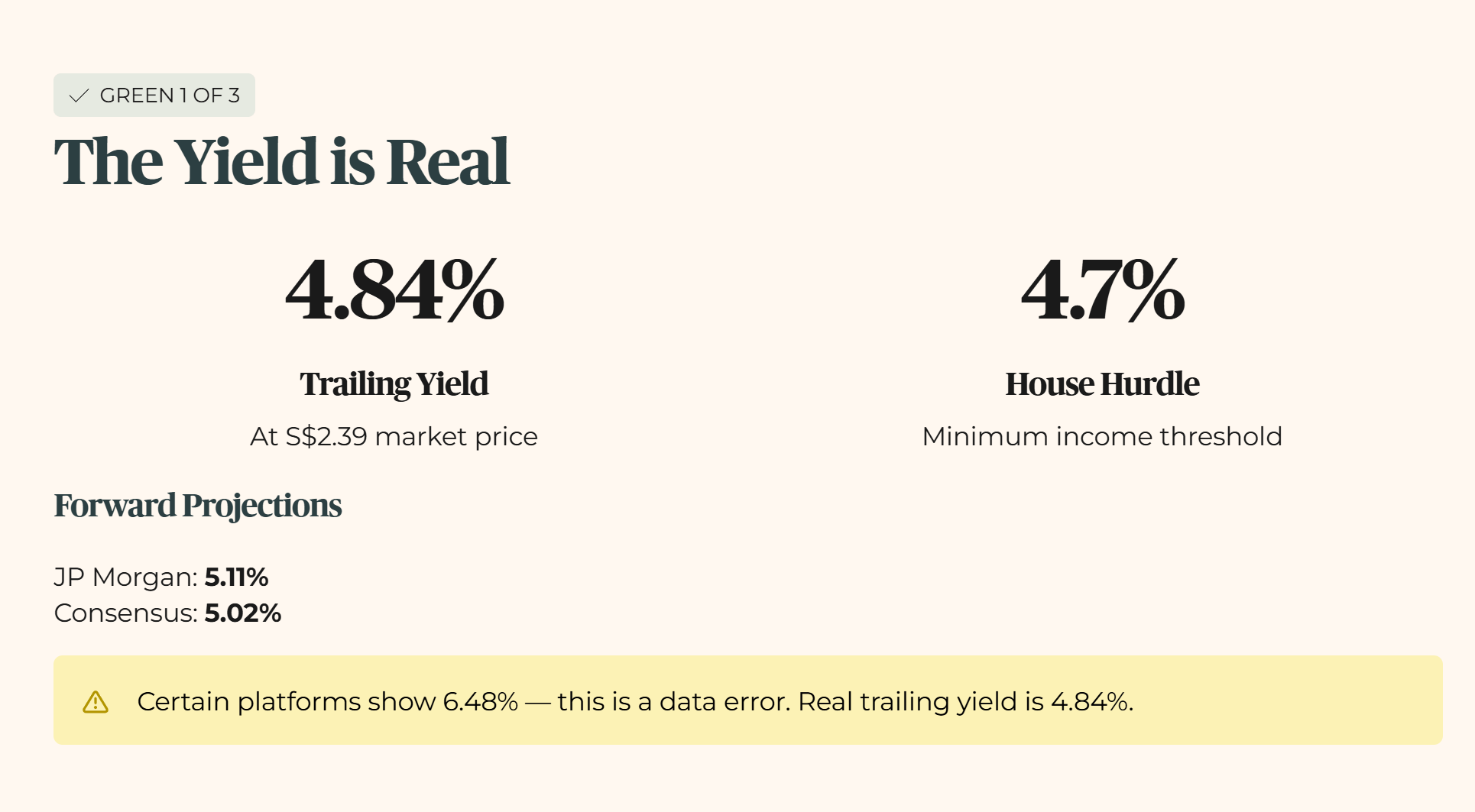

Good 1: The Yield is Real and Clearing the Bar

The primary distribution case for CapitaLand Integrated Commercial Trust rests on clean operating performance. The full-year 2025 DPU (distribution per unit, the income paid out to unitholders each year) of 11.58 cents translates into a trailing yield of 4.84% at the current market price of S$2.39. That comfortably clears my house hurdle of 4.7%, the minimum income threshold I require before any stock qualifies for a retirement portfolio. Forward projections from JP Morgan indicate an expansion toward 5.11%, while broader consensus data tracks at 5.02%.

The income growth engine behind this yield is structural, not manufactured. The 1Q 2026 gross revenue of S$426.7 million represents an 8.0% jump year on year, and NPI of S$314.4 million grew 7.9% over the same period. Management attributed this directly to two completed acquisitions: the full step-up to a 100% interest in CapitaSpring, which began contributing fully from August 2025, and the Gallileo asset in Frankfurt, where handover was largely completed in 1Q 2026. These are recurring income streams from operational assets, not one-off windfalls.

One platform data distortion worth flagging directly: certain data providers are reporting a forward yield of 6.48% for CICT. This figure is an error caused by incorrect parsing of an advance distribution payment. Do not rely on it. The real trailing yield based on the clean 11.58 cents full-year payout is 4.84%.

This bull case only holds if the annualised DPU stays above 11.50 cents over the next twelve months.

Good 2: Scale, Sponsor, and Disciplined Capital Management

CapitaLand Integrated Commercial Trust is the largest commercial REIT in Singapore. Its portfolio holds dominant retail and office assets across prime locations including Orchard Road, Raffles Place, and the wider Central Business District. The backing of CapitaLand as sponsor, alongside Temasek ownership, provides institutional stability. Moody’s affirmed CICT’s A3 rating with a stable outlook on 21 April 2026. S&P maintains an A minus rating, also with a stable outlook. That tells you the credit profile is solid at the institutional level even as the internal forensic metrics sit under pressure.

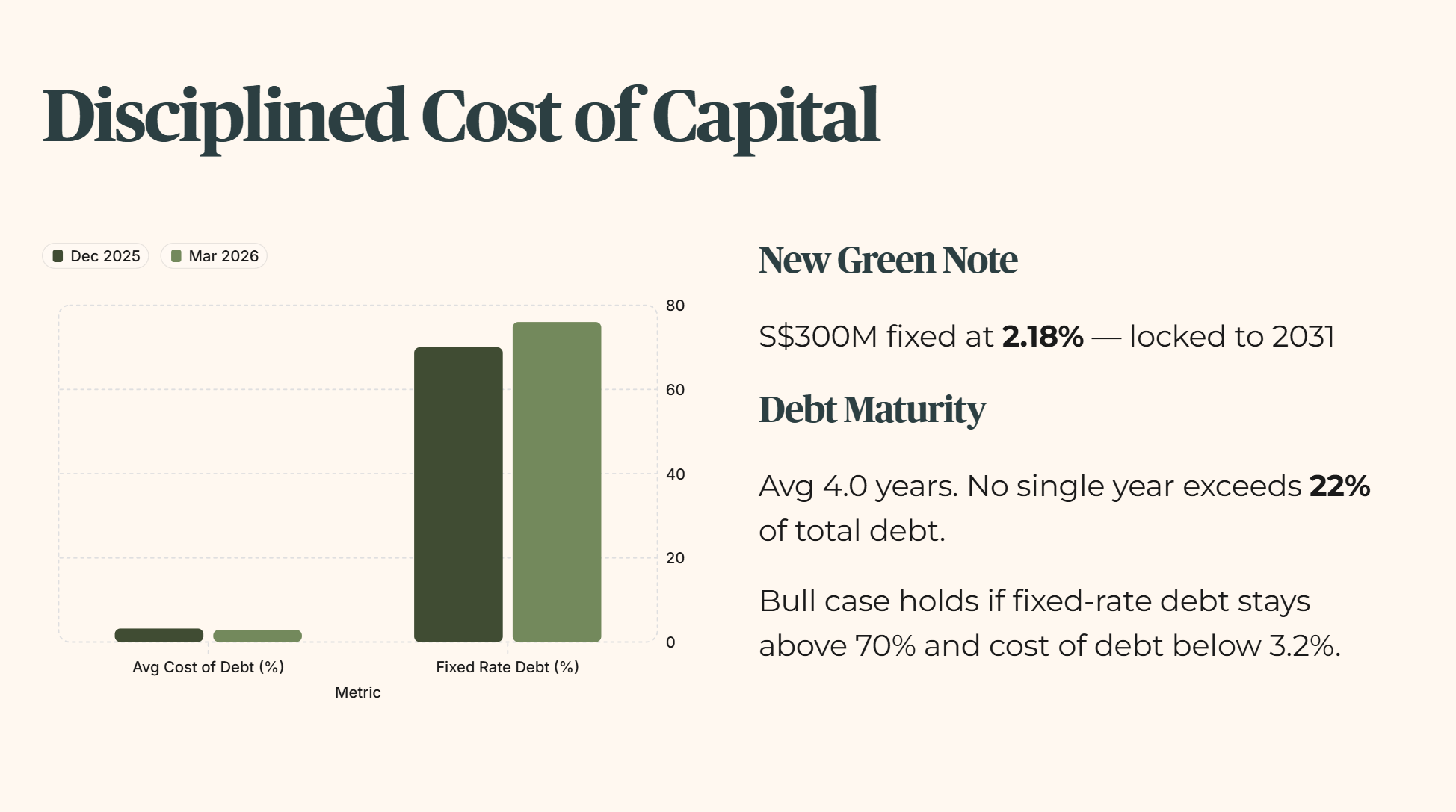

On cost of capital, management delivered better than its own guidance. The average cost of debt fell to 2.9% as at 31 March 2026, down meaningfully from 3.2% at 31 December 2025. That improvement came partly from a new S$300 million fixed rate green note issued in March 2026 at a tight 2.18%, locking in low-cost funding through to 2031. Management has fixed 76% of its total borrowings at fixed rates, reducing exposure to SORA (the Singapore Overnight Rate Average, the benchmark that determines how much floating-rate debt costs when market rates move). The average term to maturity across the debt book sits at 4.0 years, with maturities spread across multiple years and no single year carrying more than 22% of total debt.

This bull case only holds if the proportion of fixed-rate debt stays above 70% and the average cost of debt remains below 3.2% through the financial year.

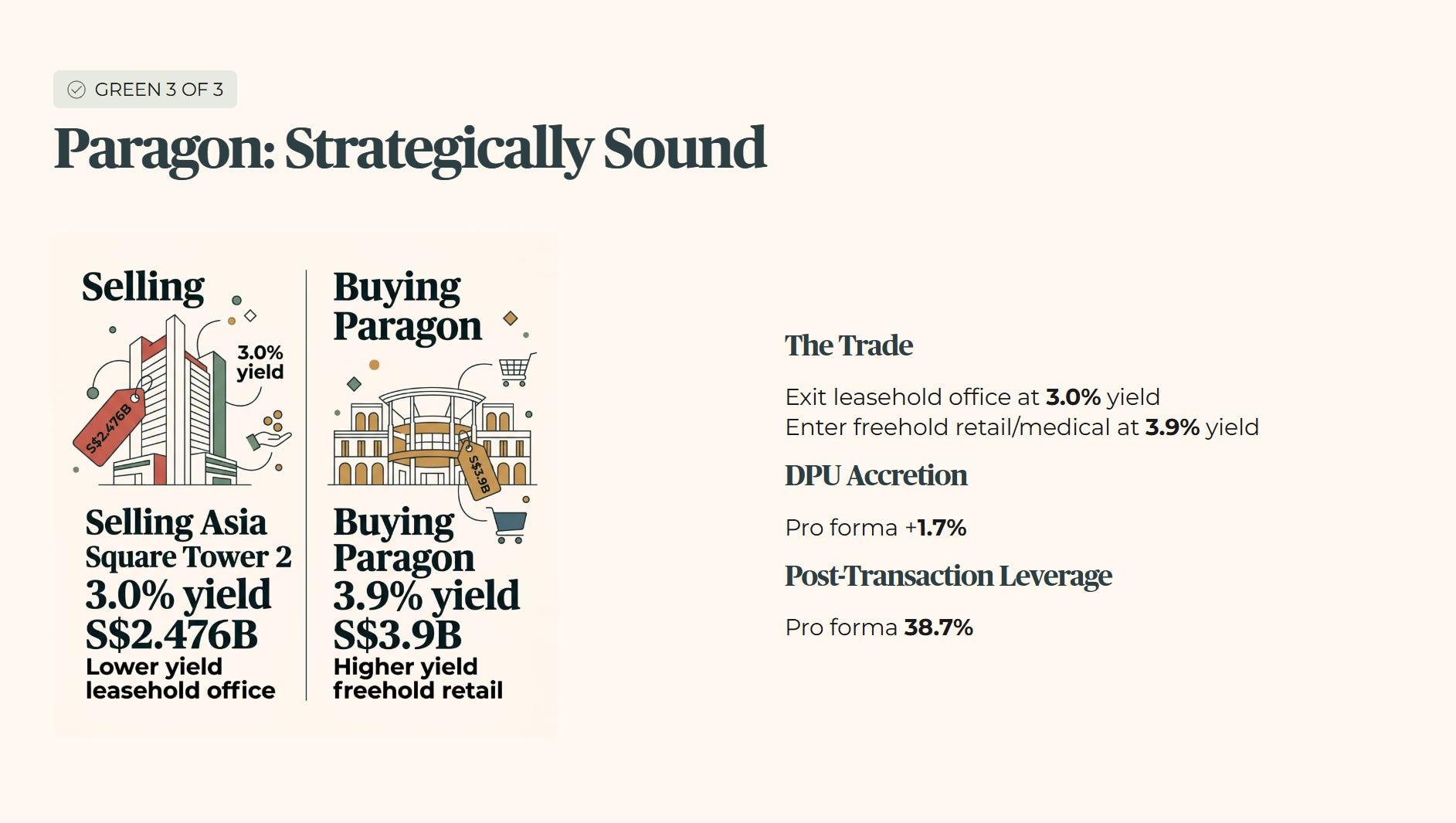

Good 3: The Paragon Acquisition is Strategically Sound and DPU Accretive

The announced acquisition of Paragon on Orchard Road for S$3.9 billion at a 3.9% net asset yield represents disciplined capital recycling. To fund this, the trust is divesting Asia Square Tower 2 for S$2.476 billion at a tighter 3.0% exit yield, capturing a 9.9% premium over its December 2025 independent valuation of S$2.252 billion. Rotating capital out of a lower-yielding leasehold office asset into a higher-yielding freehold retail and medical asset makes structural sense.

The immediate financial impact is a pro forma DPU accretion of 1.7% and a post-transaction pro forma aggregate leverage of 38.7%, assuming the Paragon acquisition and Asia Square Tower 2 divestment are completed as announced. Paragon brings a historically full committed occupancy rate across its retail and medical spaces, a freehold tenure that removes lease decay risk, and direct exposure to Orchard Road’s tourism recovery tailwinds. The formal injection of this asset in the third quarter of 2026 is modelled to lift consolidated portfolio occupancy back toward 97%. An organic asset enhancement pipeline at Plaza Singapura and Capital Tower, running from 3Q 2026 to 4Q 2028 at an estimated cost of S$160 million with a target return on investment of 6% to 7%, adds a further layer of income growth beyond the acquisition.

This bull case only holds if the Paragon acquisition closes by October 2026 and portfolio occupancy holds above 96%.

The 3 Red Flags (The Bear Case)

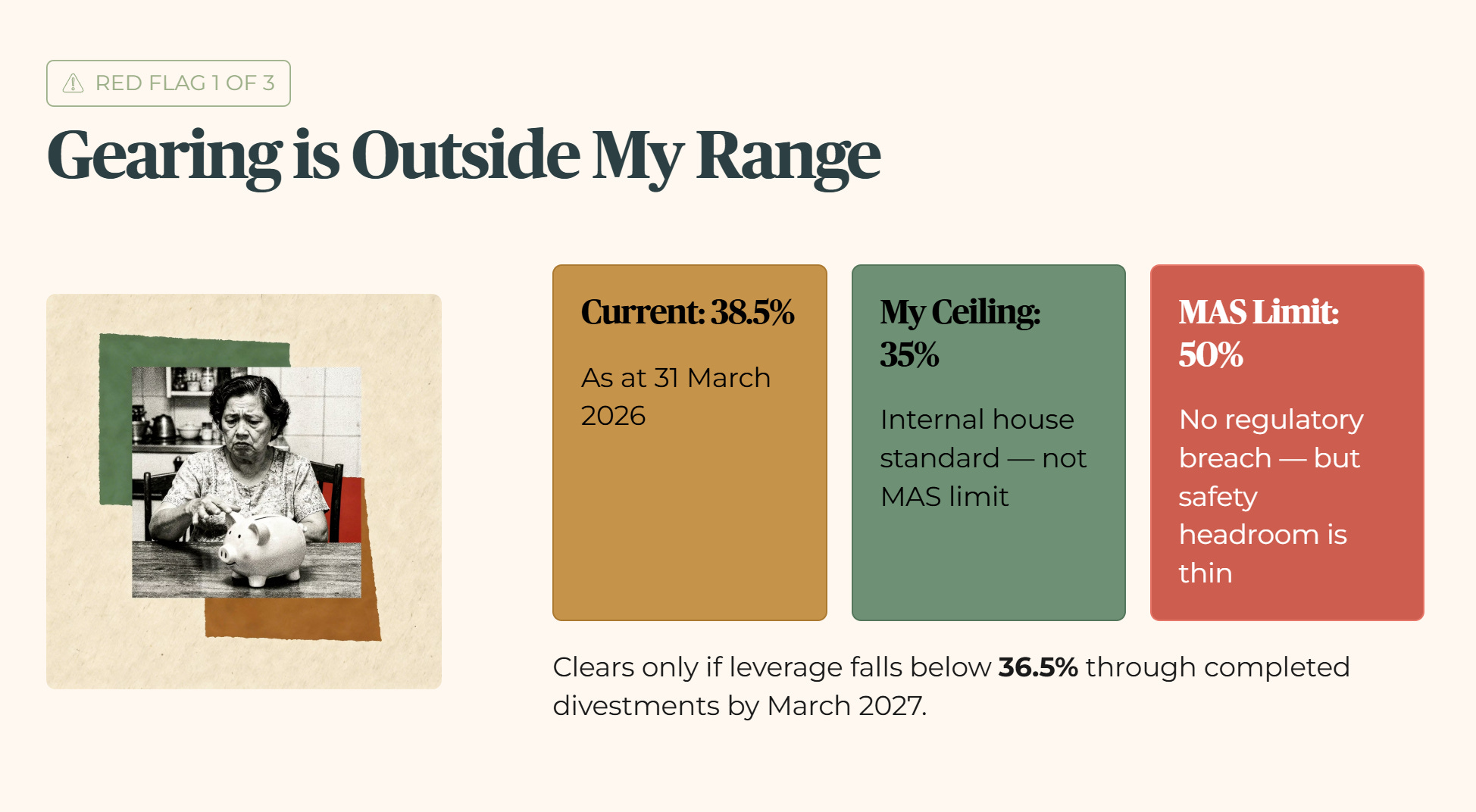

Red Flag 1: Gearing is Outside My Range

The aggregate leverage, the proportion of the trust’s assets funded by debt, stands at 38.5% as at 31 March 2026. My maximum allowable ceiling for a retirement income asset is 35%. To be clear, this is a breach of my internal house standard, not a regulatory violation. The MAS statutory limit sits at 50%, meaning the trust is completely safe from a regulatory standpoint.

But running leverage near 38.5% creates significant sequencing risk. If the Paragon acquisition closes and requires bridging funding before the Asia Square Tower 2 divestment proceeds are formally received, temporary leverage could push toward the post-transaction pro forma level of 38.7% before normalising. For a heartland retirement portfolio, running this high means any future asset devaluation or unexpected capital call leaves almost zero safety headroom. The aunty in Bedok drawing down her SRS account each month cannot afford to discover that the trust she is relying on has no buffer left when the property cycle turns.

This red flag clears only if aggregate leverage is brought back below 36.5% through completed asset divestments by March 2027.

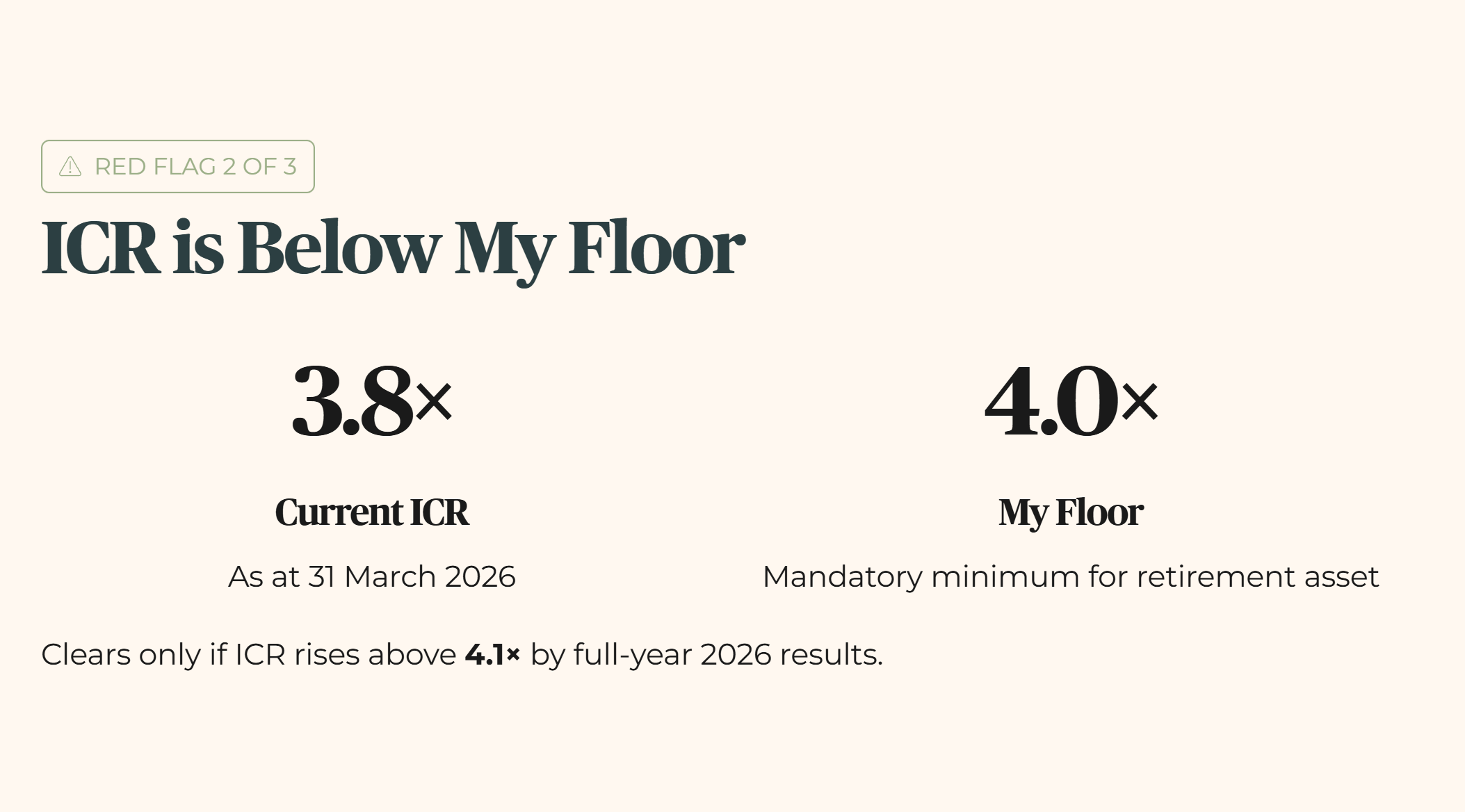

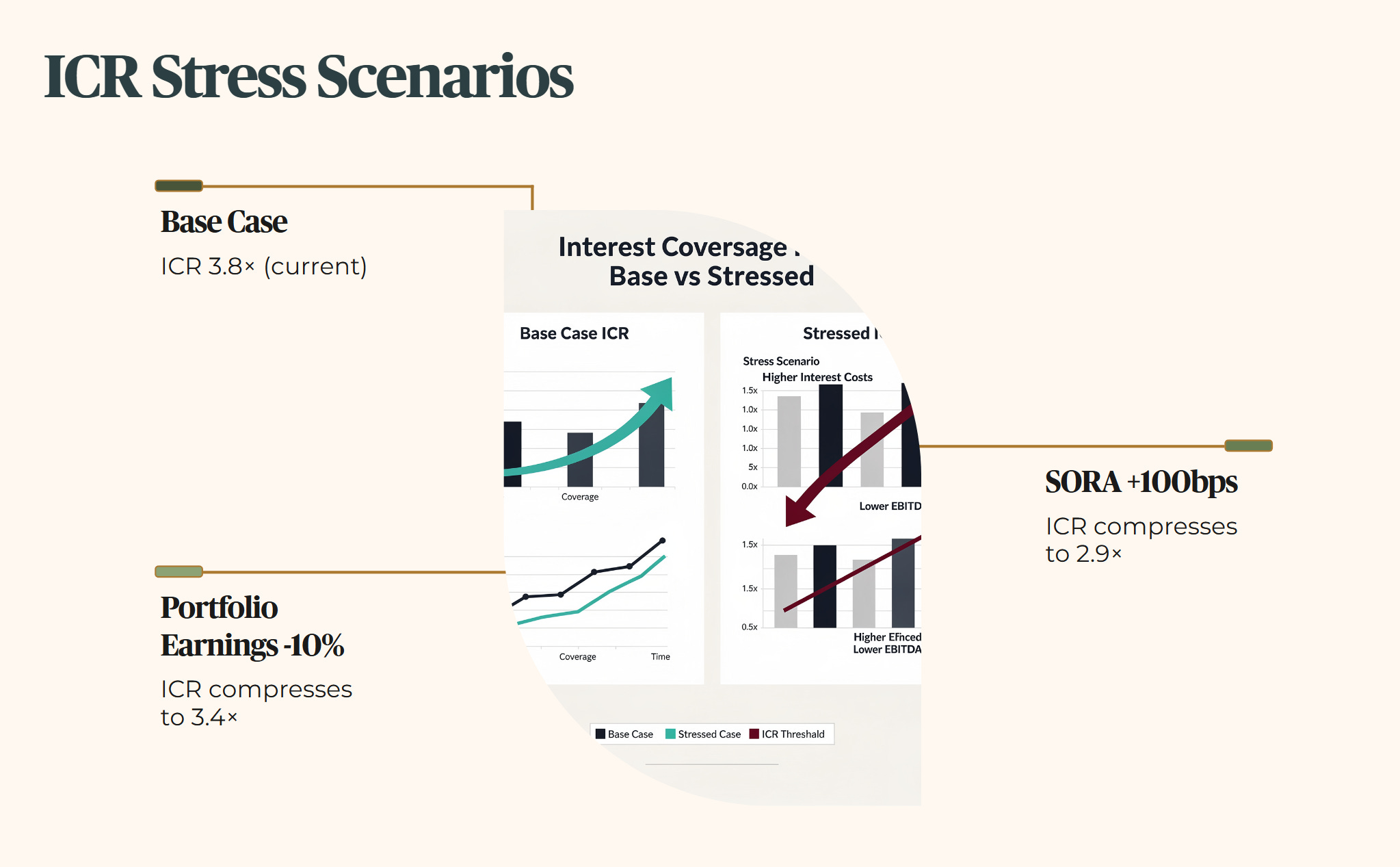

Red Flag 2: The Interest Coverage Ratio is Below My Floor

The more urgent concern is not the gearing level. It is the speed at which the interest coverage ratio can deteriorate under stress. The ICR sits at 3.8 times as at 31 March 2026, a direct failure of my mandatory 4.0 times floor. Put plainly, the trust’s earnings currently cover its interest bill by 3.8 times. My minimum for a sanctuary retirement asset is 4.0 times.

The stress scenarios in the company’s own disclosure make the risk concrete. If SORA, the floating rate benchmark that determines the cost of the trust’s unhedged borrowings, rises by 100 basis points from current levels, the ICR compresses to 2.9 times. If portfolio earnings fall by 10%, the ICR contracts to 3.4 times. Both scenarios are unlikely given that SORA is near cycle lows and occupancies are broadly stable. But the point is not the probability of the scenario. The point is the distance between the current 3.8 times and a level where the trust begins to face real income distribution pressure. For a retired investor using CICT’s quarterly payouts to cover the household’s monthly groceries at the NTUC FairPrice, a capital structure that degrades this rapidly under stress cannot be treated as a safe haven.

This red flag clears only if the ICR rises above 4.1 times by the release of the full-year 2026 financial results.

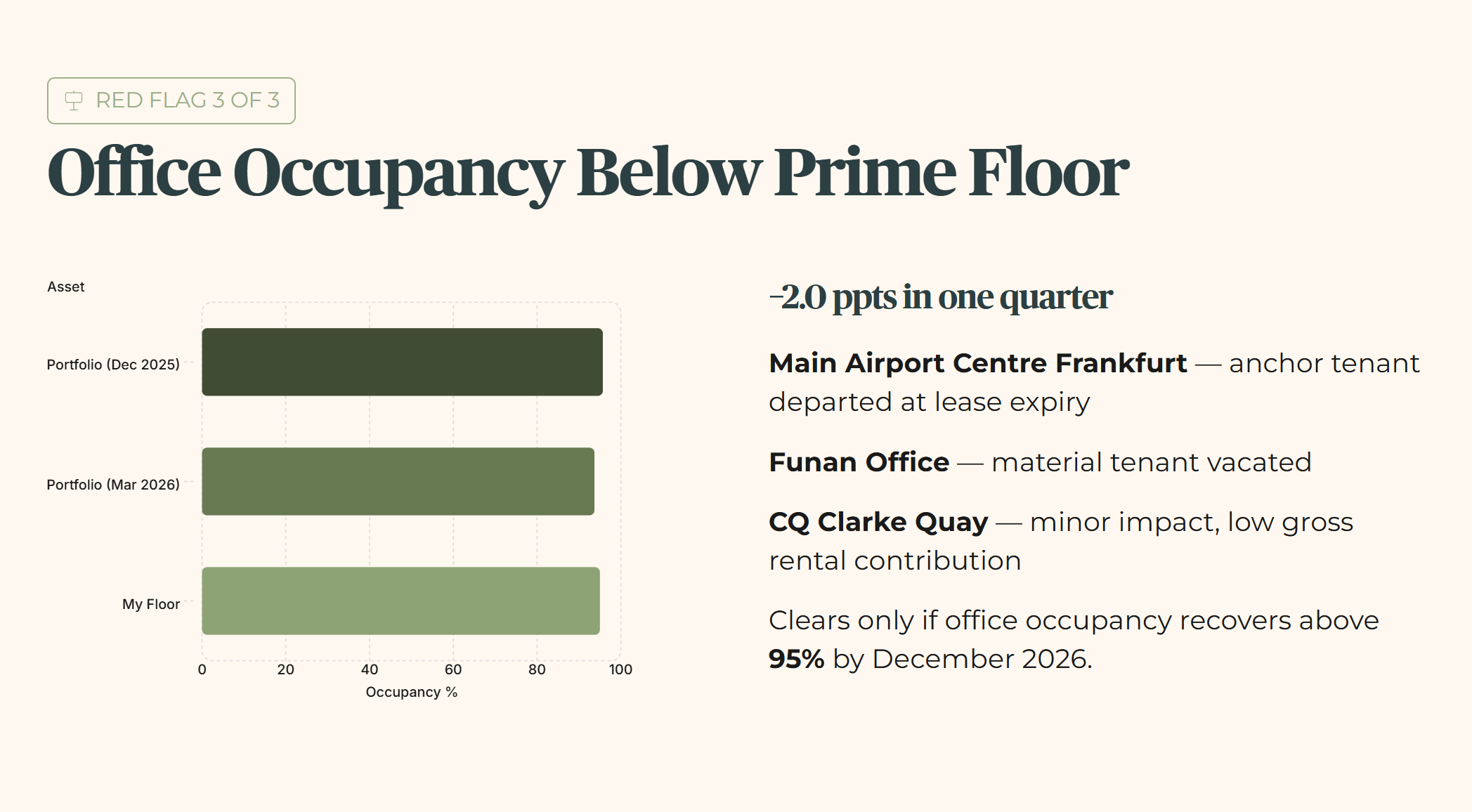

Red Flag 3: Office Occupancy Has Fallen Below the Prime Asset Floor

The commercial office segment has seen localised deterioration. Office portfolio occupancy dropped to 93.7% as at 31 March 2026, down from 95.7% at 31 December 2025. That is a 2.0 percentage point fall in a single quarter and pushes below my 95% threshold for prime commercial real estate.

Management has attributed this to three specific situations. The Main Airport Center in Frankfurt lost an anchor tenant at lease expiry, accounting for a significant portion of the consolidated portfolio drop. The Funan office development lost a tenant that occupied a material share of that building’s commercial footprint. The income disruption at CQ Clarke Quay was minor because the departing tenant was an event organiser with a low gross rental contribution. Active re-leasing is in progress across all three assets, with 1Q 2026 new and renewed office leases totalling 121,300 square feet at a retention rate of 68.9%. The pipeline of replacement tenants includes banking, insurance, financial services, and IT firms, which are higher-quality tenancy categories with longer lease commitments

This red flag clears only if commercial office occupancy recovers above 95% by December 2026.

The Window Is Already Open

The Window Closes Fast. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. By the time this analysis reaches you as a free subscriber, the entry window Iggy identified has already opened — and often closed.

Iggy’s Elite Investors don’t just get the report earlier. They get it when the numbers still matter — zero-day forensic breakdowns, the full “Red Zone” watchlist, and institutional-grade cheatsheets at the moment the setup is live, not after the market has already priced it in.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

The Singaporean Context

To evaluate the true value of this yield, we need to strip away the risk-free return available in local sovereign assets.

The current Singapore T-bill yield sits at 1.48% per annum (BS26111H, June 2026 auction). The CPF Special Account pays a guaranteed 4.0% per annum. Against the CPF SA floor, the trailing yield of 4.84% offers an equity risk premium of 84 basis points over a fully guaranteed government-backed return. That is a very thin margin of safety for an investor taking on the gearing risk, the ICR compression risk, and the office occupancy risk documented above.

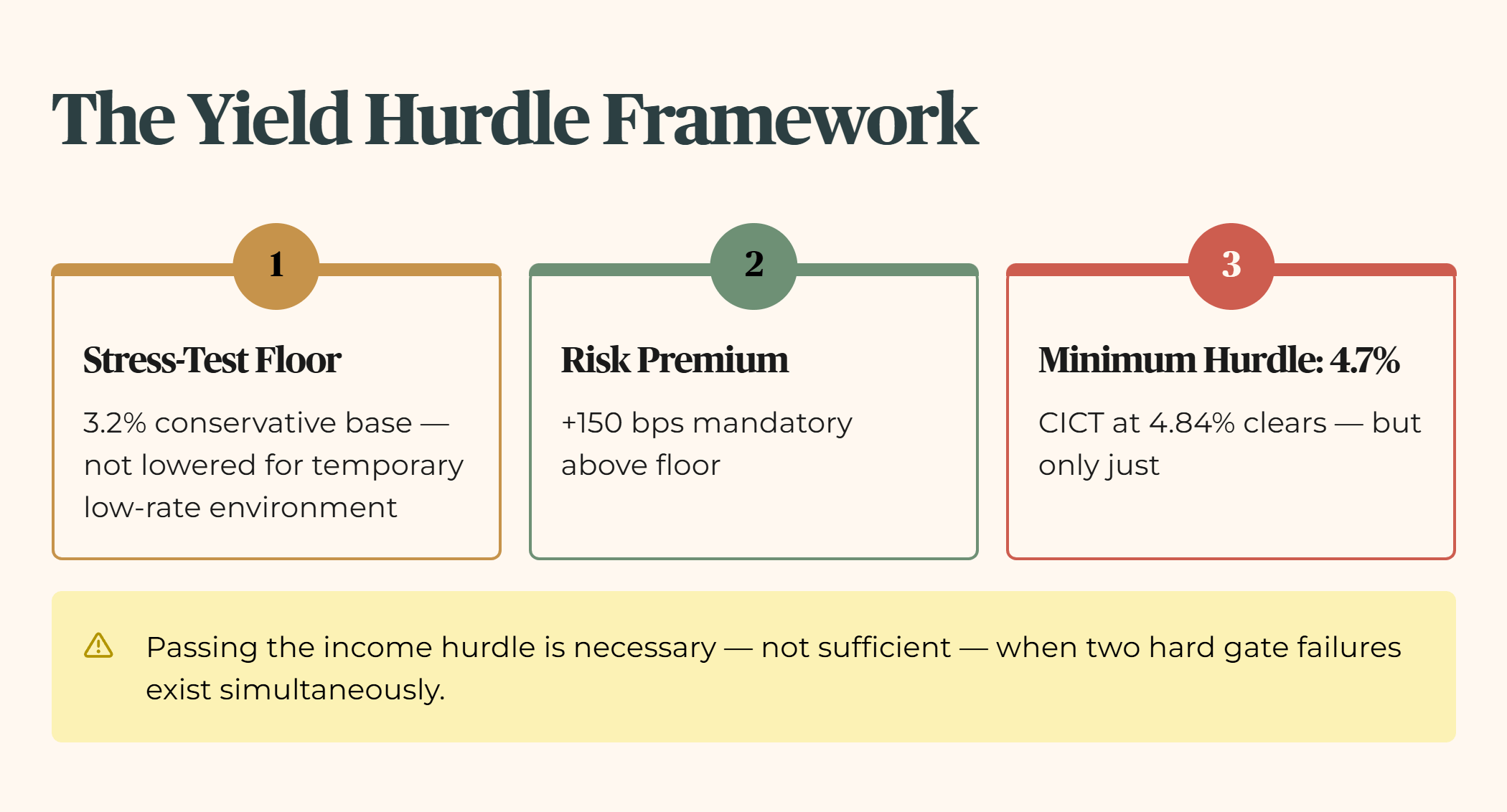

For this audit, I apply a conservative stress-test floor of 3.2%. I do not lower my standards to match a temporary low-rate environment. My minimum yield hurdle is 4.7%, which is the 3.2% floor plus 150 basis points of mandatory risk premium. CICT’s trailing yield of 4.84% clears this hurdle, but only just. Passing the income hurdle is a necessary baseline. It is not sufficient on its own for a retirement-grade classification when the balance sheet carries two simultaneous hard gate failures.

The Weighing Scale

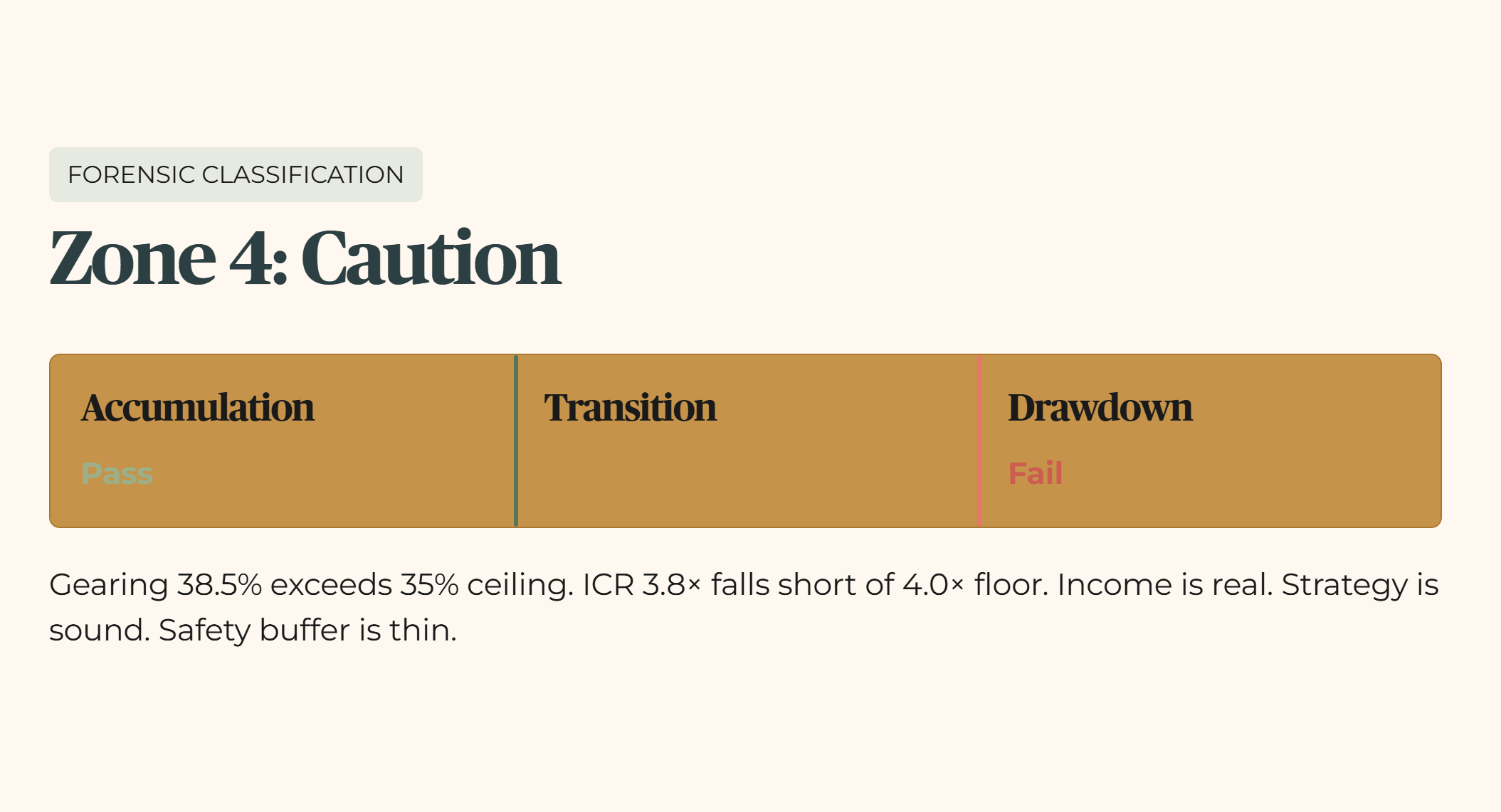

Forensic Classification: Income Core. Suitability, Accumulation: Pass. Transition: Conditional. Drawdown: Fail.

Iggy’s Forensic Zone: Zone 4, Caution.

This asset is currently flagged for caution because two balance sheet metrics sit outside the boundaries I require for a retirement sanctuary asset. The gearing at 38.5% exceeds my 35% ceiling. The ICR at 3.8 times falls short of my 4.0 times floor. The income is real and the strategy is sound, but the safety buffer is thin.

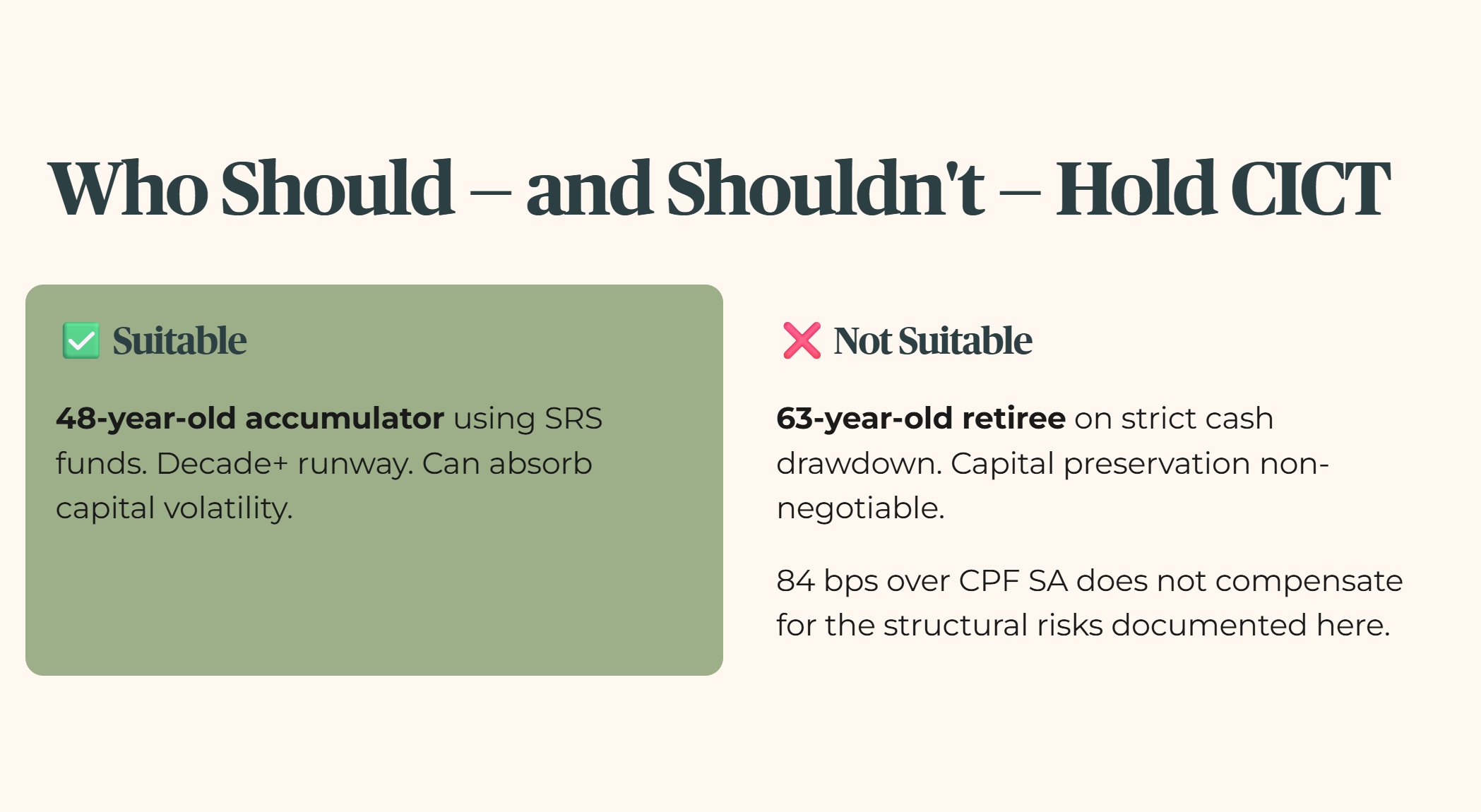

It fits a 48-year-old investor in the accumulation phase using SRS funds to build long-term dividend streams, someone who can absorb intermediate capital volatility and has a runway of more than a decade before they need to draw down. It is entirely unsuited for a 63-year-old retiree managing a strict cash drawdown portfolio where capital preservation and income stability are non-negotiable. For that retiree, the 84 basis point premium over CPF SA does not compensate adequately for the structural risks documented here.

The yield figure that clears the 4.7% hurdle by only 84 basis points is exactly where the forensic verdict tightens — and the next section runs the numbers on that margin of safety against CICT’s gearing and interest coverage so you can see whether this income stream truly earns a sanctuary-grade classification.