CICT Paragon Deal Fails Yield And Gearing Tests | SGX Daily Pulse 21 April 2026

When CICT swaps Asia Square at 3.0% exit to buy Paragon at 3.9% entry, your SRS dividend gets thinner while gearing jumps to 39.2%

IGGY’S DAILY DIGEST — EP1561 SGX Forensic Audit | 21 April 2026

Four names crossed my tracking board today. One is selling a fortress to buy a treadmill. One is running a gold machine on borrowed air. One is quietly tidying its balance sheet before anyone notices. And one is dressing up a flat year with an anniversary cheque. Not a bad Tuesday for forensic work. Let’s find out more.

In This Article:

CICT Dual Red Flag Yield Trap plus Gearing Breach

Aspial Lifestyle Gearing Alert

FCT Strategic Neutral and Redeployment Risk

Analyst Chatter Keppel REIT and Seatrium Signals

The Stress Test Buffer and Yield Hurdle

The Window Is Already Open

Iggys Take The Bottom Line

Iggys Forensic Disclaimer

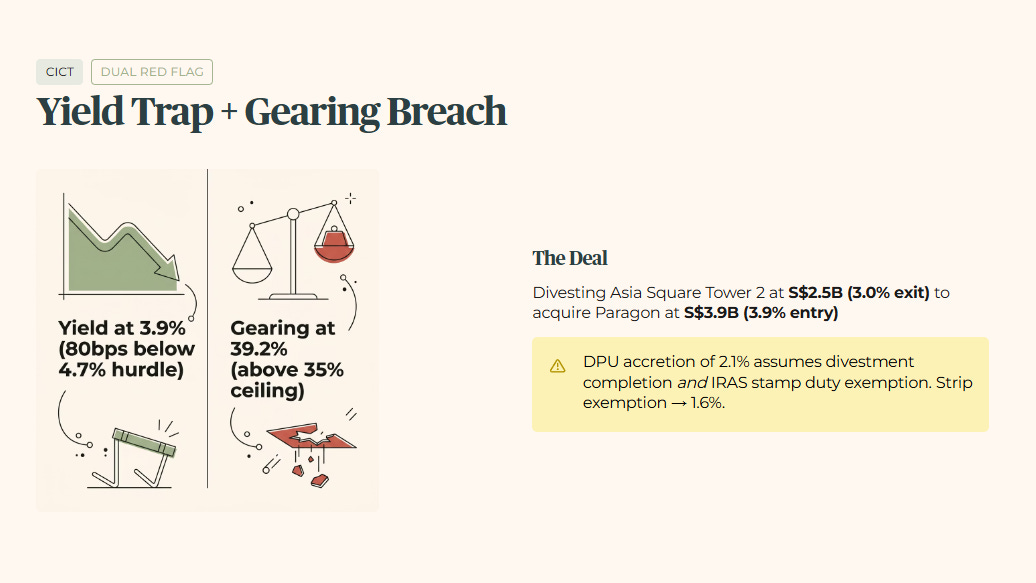

CICT - Dual Red Flag: Yield Trap + Gearing Breach

Forensic Verdict: The Paragon acquisition trades a fortress office asset for a sub-benchmark retail yield — and breaks the gearing ceiling in the process.

CICT is divesting Asia Square Tower 2 for S$2.5 billion and acquiring Paragon for S$3.9 billion at a 3.9% entry yield. Source: SGX Filing, 20 April 2026.

That 3.9% entry yield sits 80 basis points below Iggy’s 4.7% minimum hurdle. The management-stated 2.1% DPU accretion assumes both the Asia Square divestment completing and a stamp duty exemption from IRAS. Strip the exemption, and accretion falls to 1.6%. That is a thin margin built on two moving parts.

Pro-forma gearing lands at 39.2% post-transaction. That is a standalone forensic disqualifier. Iggy’s ceiling is 35%. This deal does not just fail the yield test — it fails the balance sheet test.

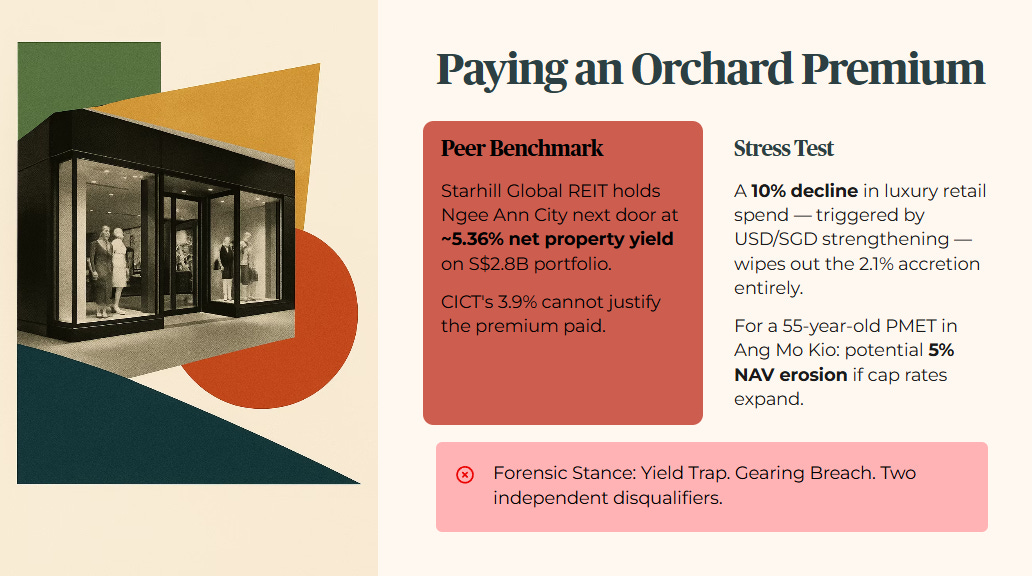

The peer context sharpens the picture. Starhill Global REIT holds a portion of Ngee Ann City next door and carries a derived net property yield of approximately 5.36% against a portfolio valuation of S$2.8 billion. CICT is paying an Orchard premium that its own yield cannot justify.

A 10% decline in luxury retail spend — triggered by USD/SGD strengthening — wipes out the 2.1% accretion entirely and makes the deal DPU-dilutive. For a 55-year-old PMET in Ang Mo Kio who treats CICT as a Sanctuary holding, the dollar consequence is potential 5% NAV erosion if cap rates expand.

Forensic Stance: Yield Trap. Gearing Breach. Two independent disqualifiers.

🦎 Iggy’s Insight

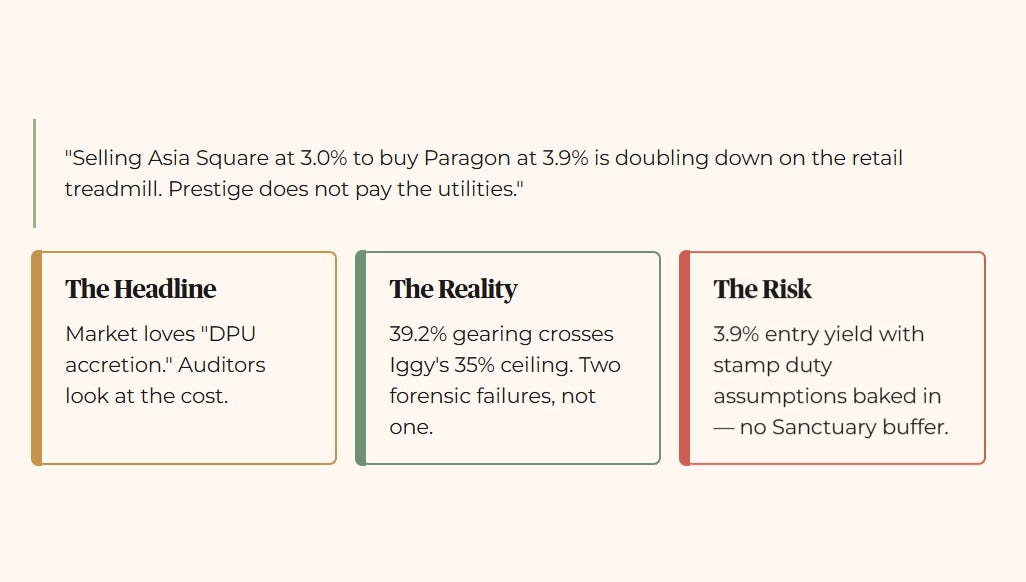

The market loves the “DPU accretion” headline. Auditors look at the cost. Selling Asia Square at a 3.0% exit yield to buy Paragon at 3.9% is doubling down on the retail treadmill while the STI trades at all-time highs. But the yield arithmetic is only half the problem. At 39.2% pro-forma gearing, CICT has crossed Iggy’s 35% ceiling — meaning this deal fails two forensic tests simultaneously, not one. In a high-inflation environment, a 3.9% entry yield with stamp duty assumptions baked in offers no Sanctuary buffer. You are buying Orchard prestige on a leveraged balance sheet. Prestige does not pay the utilities.

Aspial Lifestyle - Gearing Alert

Forensic Verdict: Refinancing at 5.1% on a 70.8% geared balance sheet is not a yield play. It is a leverage bet with a fixed coupon attached.

Aspial Lifestyle priced S$28 million in notes at 5.1% per annum, due October 2029. Source: FSMOne/SGX.

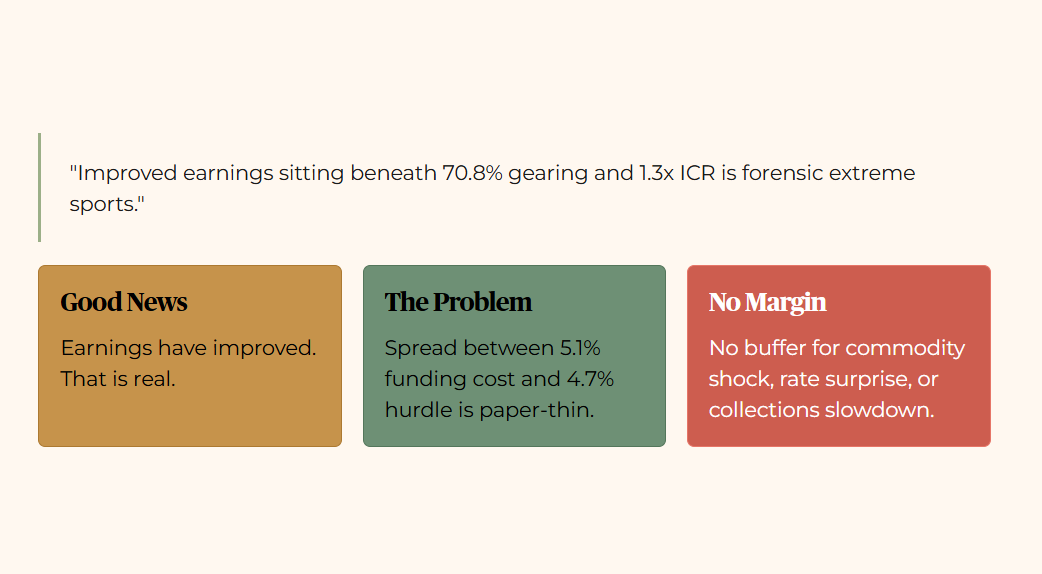

The 5.1% coupon clears Iggy’s 4.7% hurdle on paper. The balance sheet context makes that irrelevant. Gearing sits at 70.8%. ICR is 1.3x against Iggy’s 4x floor. The company is running a gold-backed lending operation funded by high-cost capital, and the debt wall is the primary narrative here — not the earnings recovery.

Hour Glass operates in the same luxury and lifestyle space with zero net debt. Aspial’s 70.8% gearing is a forensic outlier in the sector, not a temporary phase.

A 10% drop in gold prices squeezes the 1.3x ICR toward 1.0x. That is covenant breach territory. For a 45-year-old HDB owner in Punggol holding these notes for income, the risk-reward is misaligned: equity-level balance sheet exposure for a fixed 5.1% return.

Forensic Stance: Watchlist Trigger.

🦎 Iggy’s Insight

Earnings have improved. That is the good news, and it is real. But improved earnings sitting beneath a 70.8% gearing ratio and a 1.3x interest coverage is forensic extreme sports. Aspial is a gold-backed lending machine running on high-cost capital, and at 5.1% refinancing rate, the spread between funding cost and the 4.7% Iggy hurdle is paper-thin. When the ICR is already at 1.3x, there is no margin for a commodity shock, a rate surprise, or a collections slowdown. This is not a dividend play dressed up as a bond. It is a leveraged balance sheet with a coupon stapled to the front.

FCT - Strategic Neutral

Forensic Verdict: Selling White Sands at a 4.5% exit yield is a defensive balance sheet move, not a growth play.

FCT is in preliminary discussions to divest White Sands for above S$470 million at an approximate 4.5% exit yield. Source: Business Times, 20 April 2026. FCT’s SGX clarification confirms discussions are ongoing with no certainty of completion.

The 4.5% exit yield sits just below Iggy’s 4.7% hurdle. Management is not extracting a premium — this is a fair-value disposal to reduce gearing pressure. No official pro-forma gearing reduction or DPU impact has been published. Until the deal closes, any specific figure is analyst-derived, not management-stated.

What is clear directionally: if proceeds are redeployed below 5% yield, the divestment becomes DPU-dilutive despite improving the balance sheet. FCT’s suburban portfolio remains more resilient than peers facing similar divestment pressure, but the trade-off between balance sheet repair and income consistency is real.

For a 50-year-old in Tampines, this is a safer balance sheet but a thinner dividend check — and the arithmetic on the redeployment is not yet visible.

Forensic Stance: Strategic Neutral. Watch for redeployment yield disclosure.

Analyst Chatter

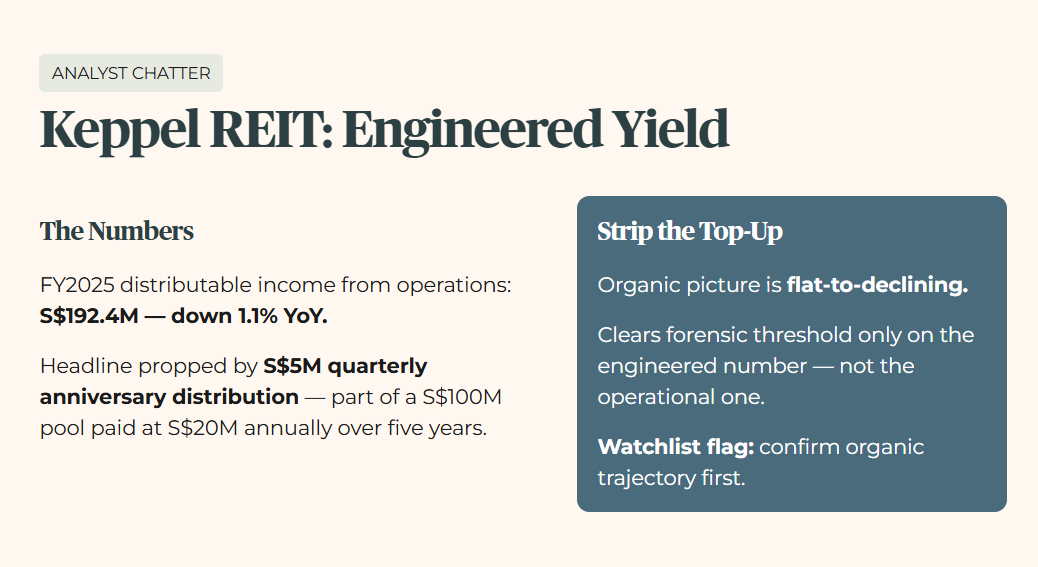

Keppel REIT: FY2025 distributable income from operations came in at S$192.4 million, down 1.1% year-on-year. The headline is framed around the S$5 million quarterly anniversary distribution — part of a S$100 million pool paid at S$20 million annually over five years. Strip that top-up, and the organic picture is flat-to-declining. Based on my personal tracking, this clears the forensic threshold only on the engineered number, not the operational one. Watchlist flag: confirm organic trajectory before treating this as a DPU recovery.

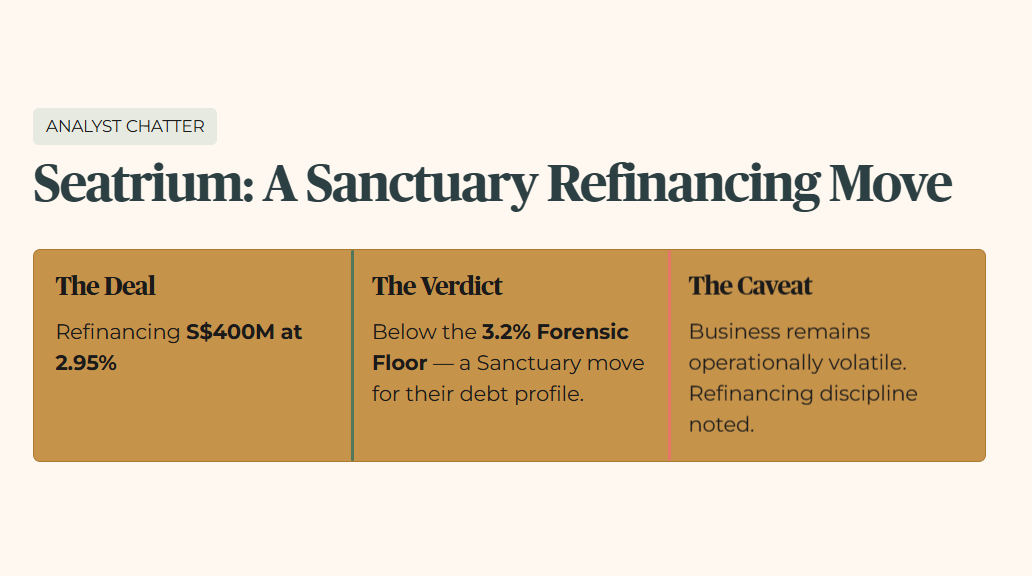

Seatrium: Refinancing S$400 million at 2.95% — below the 3.2% Forensic Floor. A Sanctuary move for their debt profile. The business remains operationally volatile, but the refinancing discipline is noted.

The Stress-Test Buffer

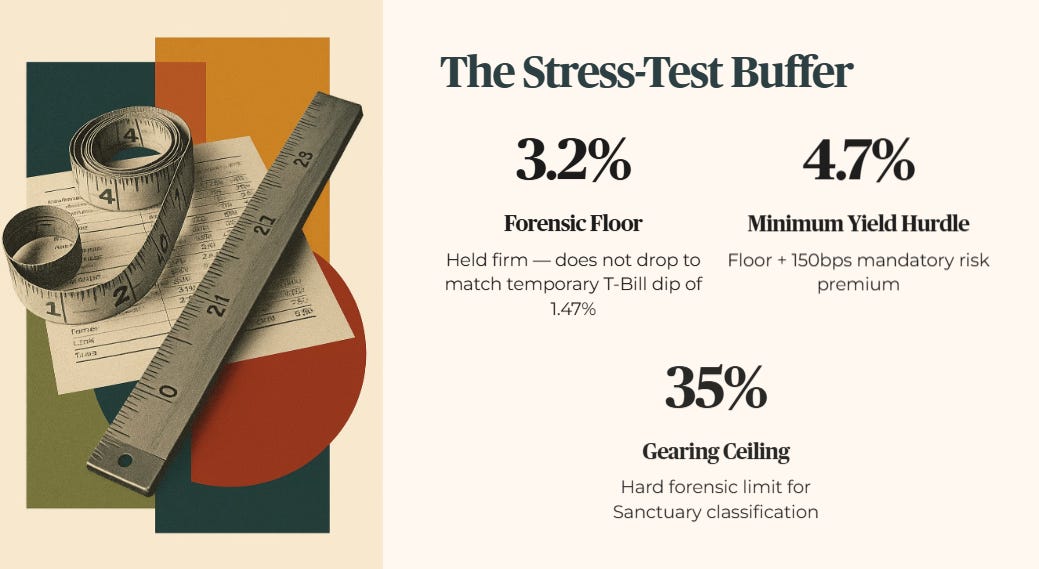

For this audit, I apply a conservative floor of 3.2%. The T-Bill sits at 1.47%, but I do not lower my standards to match a temporary market dip. My floor holds at 3.2% to ensure Sanctuary assets can withstand a return to long-term average rates. Minimum yield hurdle: 4.7% — the 3.2% floor plus 150 basis points of mandatory risk premium.

The Window Is Already Open

The Window Closes Fast. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. By the time this analysis reaches you as a free subscriber, the entry window Iggy identified has already opened — and often closed.

Iggy’s Elite Investors don’t just get the report earlier. They get it when the numbers still matter — zero-day forensic breakdowns, the full “Red Zone” watchlist, and institutional-grade cheatsheets at the moment the setup is live, not after the market has already priced it in.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

Iggy’s Take - The Bottom Line

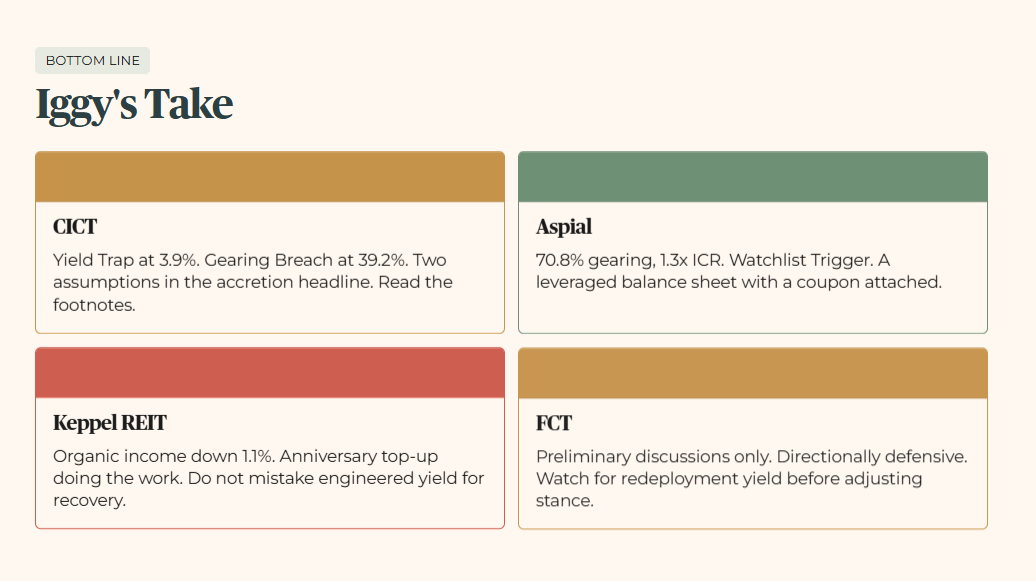

CICT: The Paragon deal fails two forensic tests independently. Yield Trap at 3.9%. Gearing Breach at 39.2%. The DPU accretion headline has two assumptions baked in. Read the footnotes.

Aspial: 70.8% gearing and 1.3x ICR. Watchlist Trigger. This is not a bond. It is a leveraged balance sheet with a coupon attached.

Keppel REIT: Organic distributable income is down 1.1%. The anniversary top-up is doing the work. Do not mistake engineered yield for operational recovery.

FCT: Preliminary divestment discussions only. Directionally defensive. Watch for redeployment yield before adjusting the forensic stance.

Accretion is what they tell you. The exit yield is what they are not saying.

Iggy’s Forensic Disclaimer

This content is produced for educational and informational purposes only. I am not a financial advisor — I am a retail investor who applies forensic analysis to my own portfolio and shares that process publicly. Nothing here constitutes a recommendation to buy, sell, or hold any security, and no specific target prices or personalised financial advice are offered. Stocks assessed under Iggy’s Forensic Yield Standard are benchmarked against a 4.7% minimum yield hurdle; stocks flagged as Growth Watch fall below this threshold but demonstrate clean balance sheet metrics and an identifiable growth catalyst — these carry a materially different risk profile and are not suitable as yield replacements for income-dependent investors. All data is sourced from public filings and verified sources; where data is unverified it is explicitly flagged. All investments carry risk, including the potential loss of principal, and past performance is not indicative of future results. If you are making investment decisions involving CPF, SRS, or personal capital, please conduct your own due diligence or consult a MAS-licensed financial adviser before committing funds.