CLINT FY 2025: The “Tax-Optimized” Dividend Machine or a Growth Slowdown in Disguise?

DPU reflects a 15% YoY increase as management utilizes the “Onshore Debt” lever, though occupancy trends and tenant concentration in data centres remain key variables.

Welcome back to the lab, folks. Today, we are dissecting the FY 2025 Financial Results for CapitaLand India Trust (CLINT). On the surface, the metrics show significant growth, but we’re going to peel back the layers to see if this dividend movement is fueled by operational expansion or some world-class “strategic financial plumbing.”

Download the Results Here:

In This Article:

The Slide-by-Slide Reality Check

Financial Highlights: The DPU Magic Trick

The “Onshoring” Gambit: Tax-Arbitrage Tetris

Operations & Portfolio: Sweating in Pune

Data Centres: The Billion-Dollar Pipeline

Iggy's Performance Scorecard

InvestingPro Reality Check

Iggy's Verdict🦎 About Iggy the Investing Iguana

Welcome to the Iguana Pit! If you’re new here, I’m Iggy: your guide through the dense jungle of the Singapore markets. My mission is simple: to spot the predators before they spot your portfolio.

We are now 5,800+ subscribers strong across YouTube and Substack, focusing purely on the data-driven alpha that mainstream media misses.

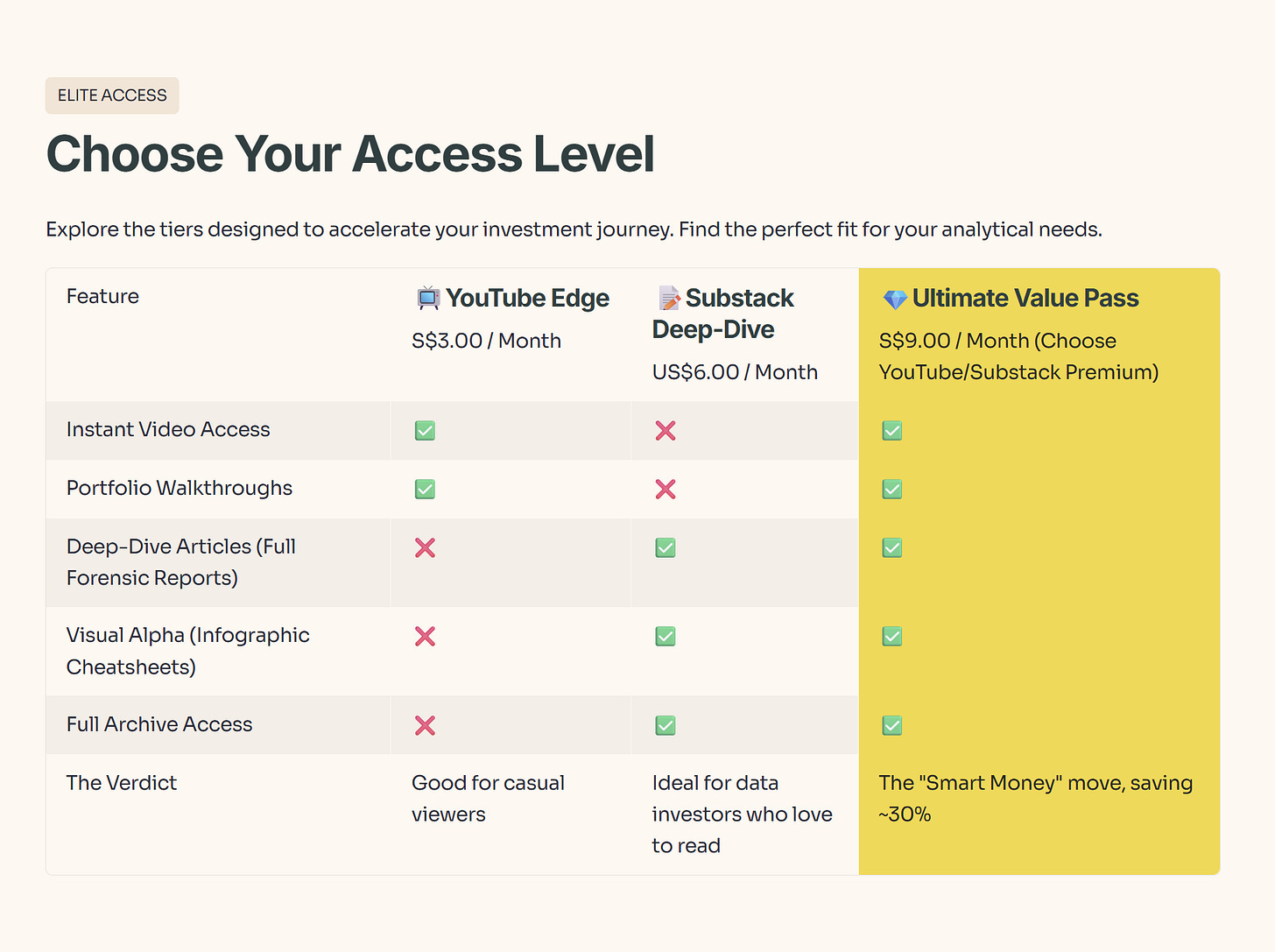

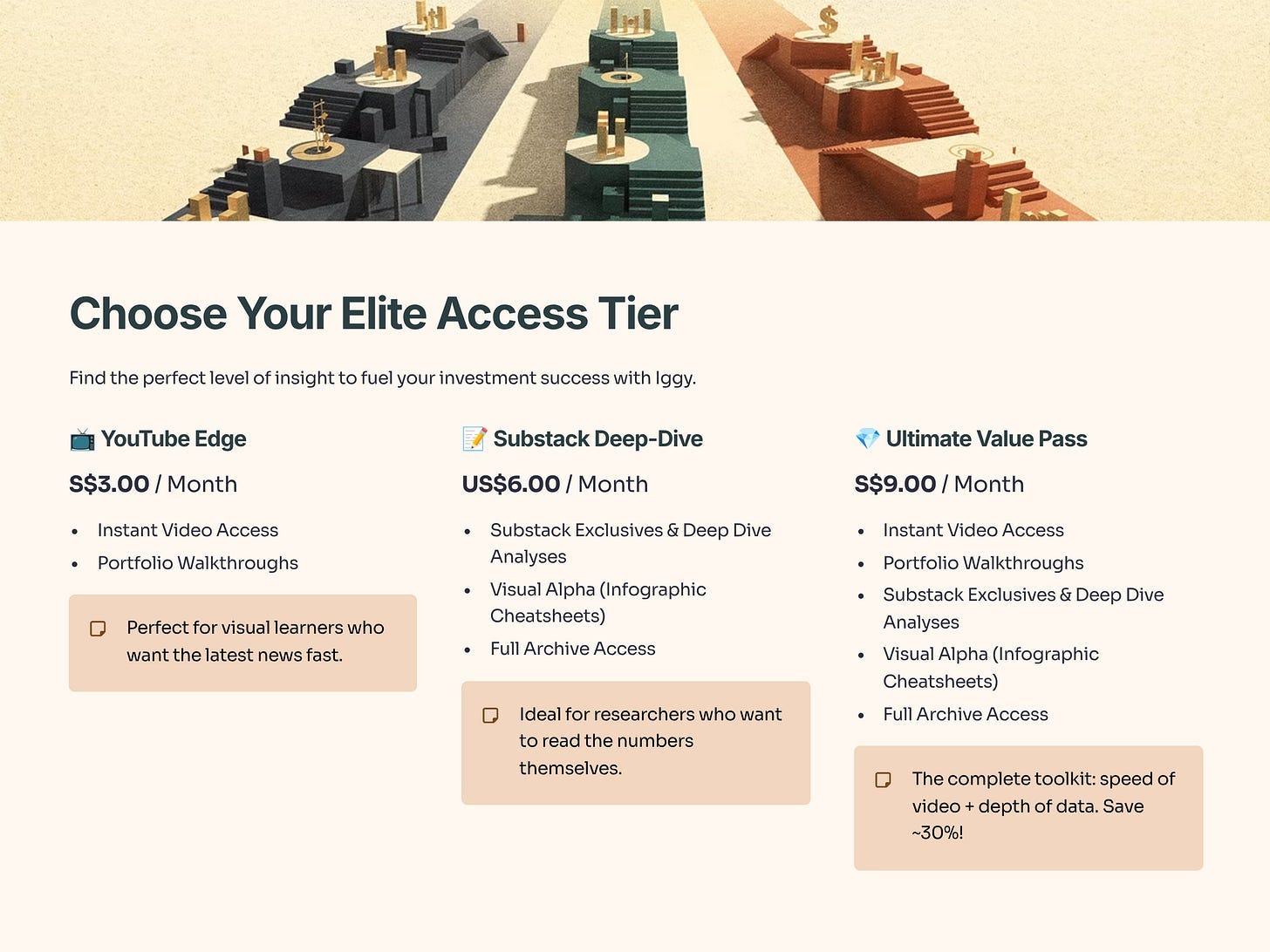

🚀 Join the “Elite 150” Inner Circle

Real alpha is found behind the velvet rope. Stop following the herd and start following the data with our 150+ paid members.

📺 The YouTube Edge (S$3/mo): Beat the Delay.

Instant Access: Watch new videos the moment they drop.

The Free Tier Trap: Free subscribers wait up to 14 days to see the same video. (By then, the news is old and the trade is gone).

📝 The Substack Deep-Dive (US$6/mo): Unlock the Vault.

Zero Paywalls: Read the full “Deep Dive” articles and “Substack Exclusive” articles found only on Substack.

Visual Alpha: Download exclusive Infographic Cheatsheets not available to free readers.

💎 The Ultimate Value Pass (S$9/mo): (BEST VALUE)

Get It All: Paid via YouTube, this bundle grants you Instant Video Access AND Full Substack Access.

The Math: You save ~30% compared to buying them separately. It’s the “Smart Money” move.

Why wait 2 weeks for old news? Get the data while it’s fresh. 👉 Join Here: https://www.youtube.com/@InvestingIguana/membership

The Slide-by-Slide Reality Check

Financial Highlights: The DPU Magic Trick

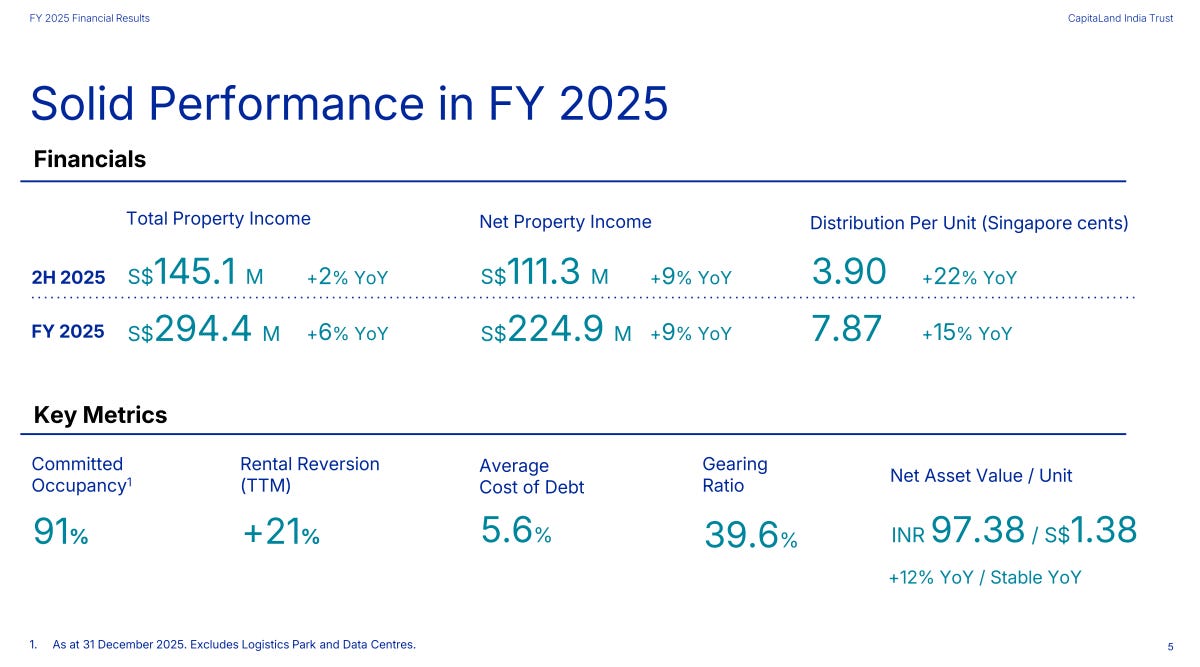

[Refer to Slide 5: Solid Performance in FY 2025 | Slide 11: FY 2025 vs FY 2024 Results]

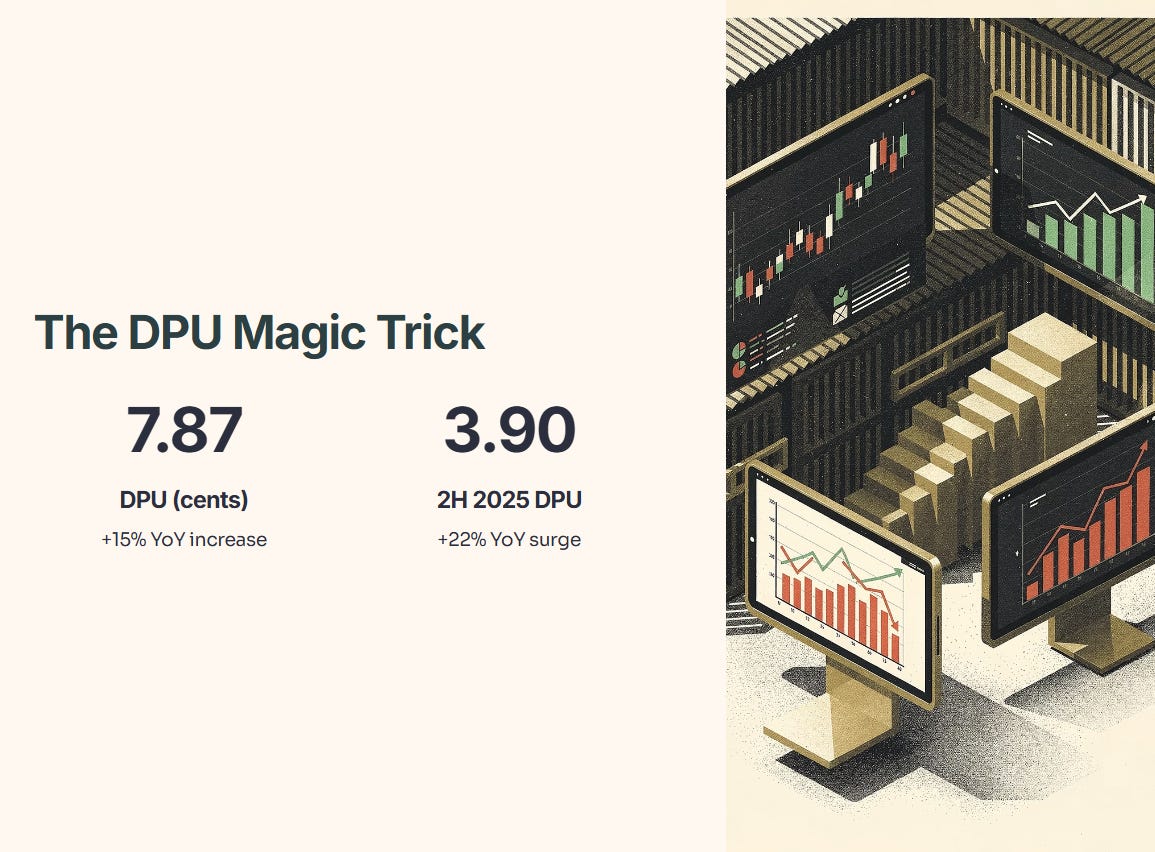

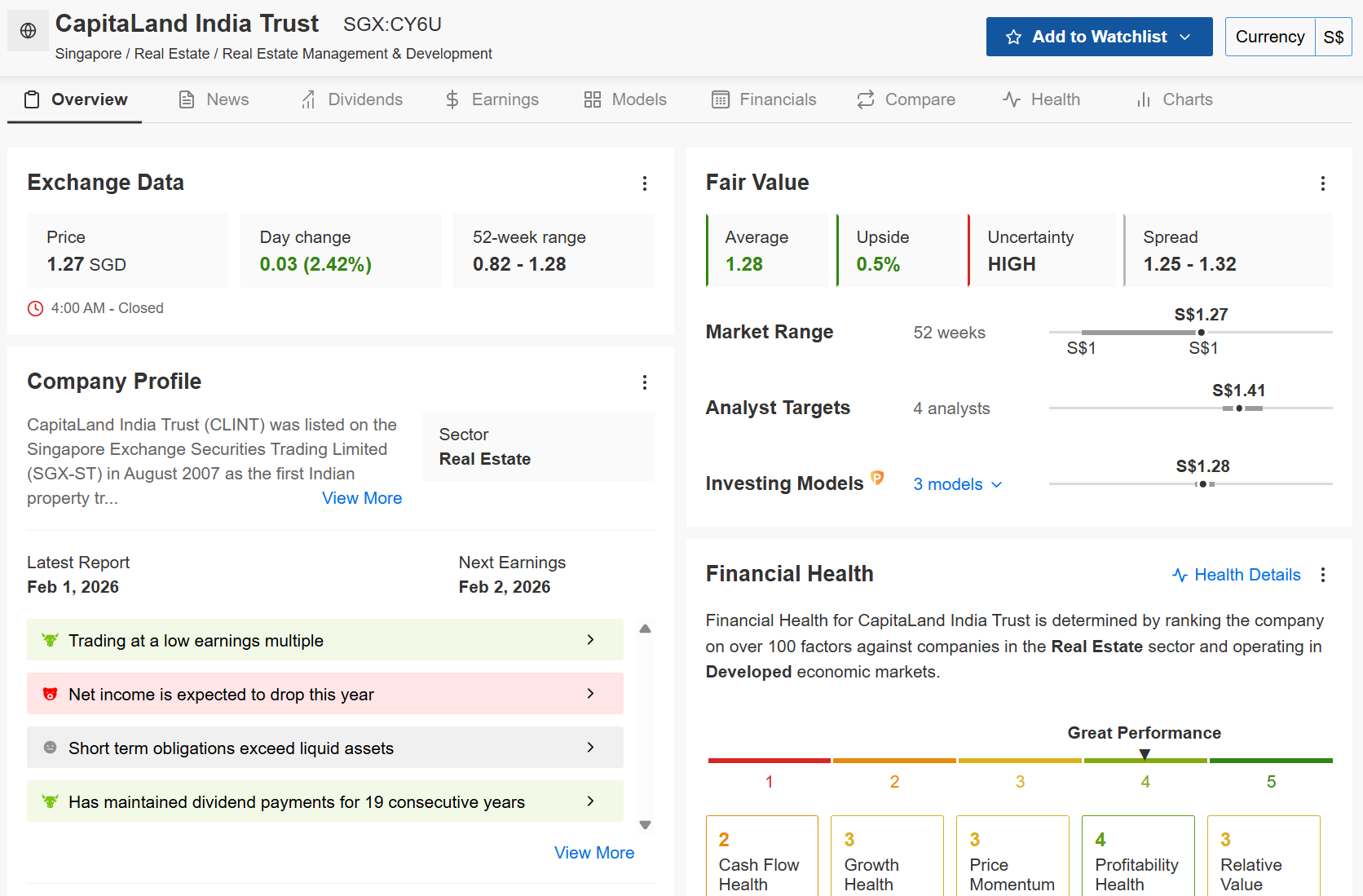

CLINT reported a Distribution Per Unit (DPU) of 7.87 Singapore cents for FY 2025—a solid +15% increase compared to last year. The momentum hit another gear in the second half, with 2H 2025 DPU reaching 3.90 cents, a +22% YoY surge.

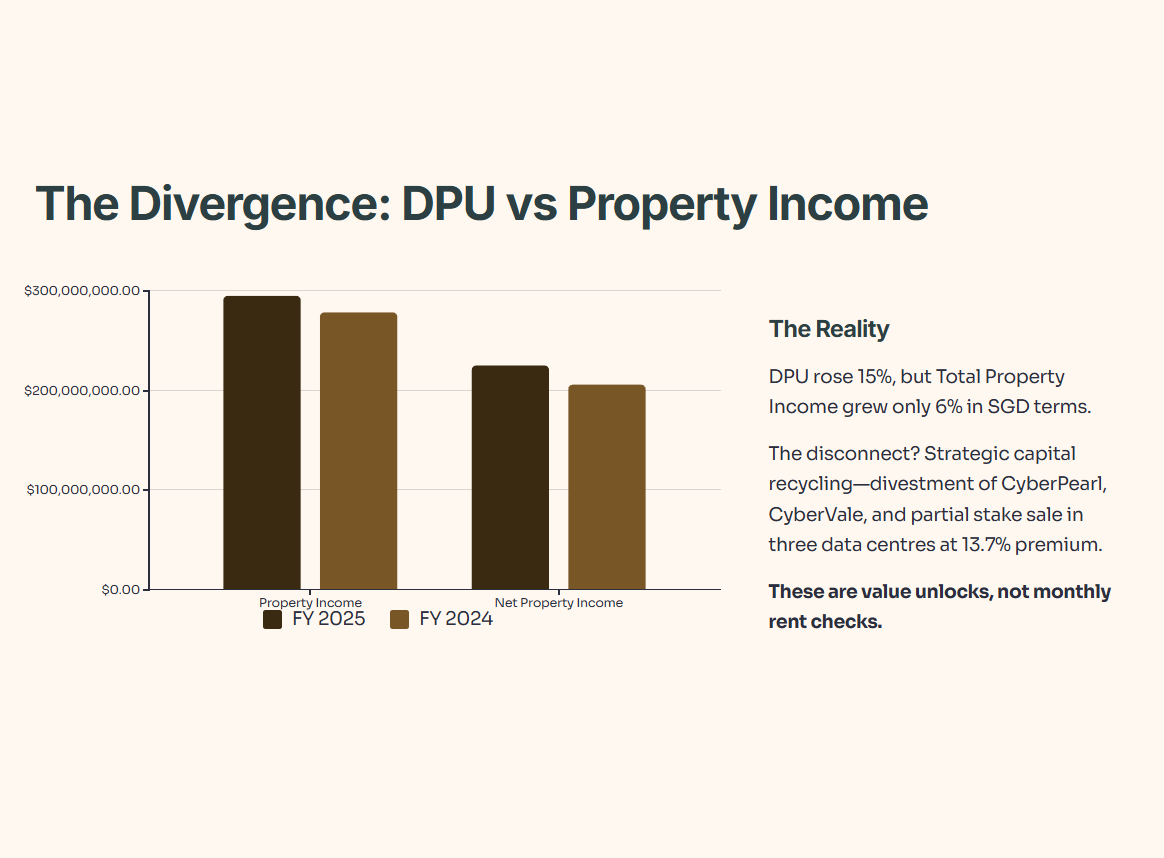

However, a closer look at the fundamentals reveals a divergence in growth rates. While DPU rose by 15%, Total Property Income grew by a more modest 6% in SGD terms. This disconnect is largely driven by strategic capital recycling rather than pure rental growth. The trust completed the divestment of CyberPearl and CyberVale and announced a partial stake sale in three data centres at a 13.7% premium to valuation. While these moves provide a headline boost to your distribution, they represent non-recurring capital events—essentially “value unlocks” rather than monthly rent checks.

The “Onshoring” Gambit: Tax-Arbitrage Tetris

[Refer to Slide 9: Optimising Capital Structure by Onshoring Debt]

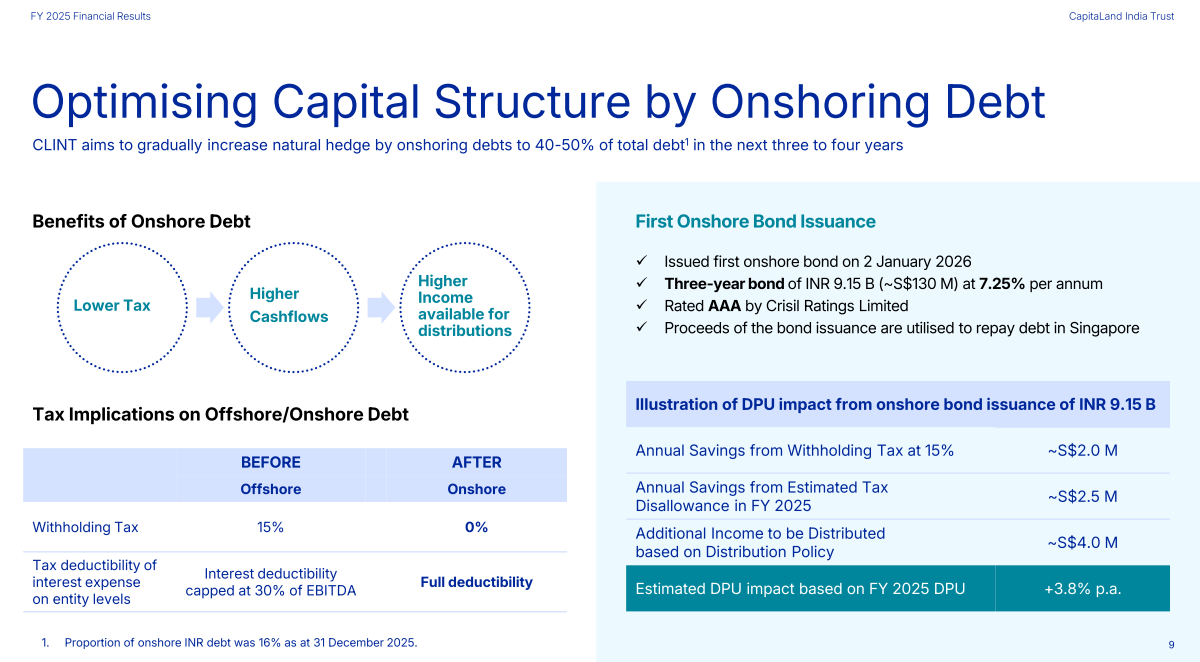

Management isn’t just building buildings; they are playing a high-stakes game of tax-arbitrage Tetris. A primary tactical lever used this year is the shift toward onshore INR debt, starting with a bond issuance of ~S$130 M at 7.25% p.a.

The logic? By moving debt to India, they eliminate the 15% withholding tax on interest payments and claw back full tax deductibility. Management estimates this specific move contributes a +3.8% p.a. impact to DPU. With a target to increase onshore debt to 40-50% of the portfolio (up from just 16%), this “tax alpha” strategy is going to be a multi-year focus. It’s a brilliant way to manufacture yield without needing to find a single new tenant.

Reality Check: The slides say the balance sheet is being optimized, but what do the institutional models say?

Here’s how the numbers look when we stress-test CLINT the same way institutional models do—and what that implies for your yield and downside risk.