Is the New CPF "Double Match" a Trap? (The Hidden Cost)

Your monthly cash flow is changing in January 2026. Here is the exact playbook to capture the new matching grants without hurting your liquidity.

If you thought you could coast into 2026 without touching your CPF settings, think again. The government is rolling out six major changes that will directly impact your take-home pay, your medical safety net, and—most importantly—how much “free money” you can extract from the system.

For many of you aged 45 to 65, this is a double-edged sword. You are facing a “Cash Flow Squeeze” (higher contribution rates and wage ceilings) but also a massive “Capital Opportunity” (new matching schemes). If you do nothing, you lose liquidity. If you optimize, you could lock in an extra S$3,000 per year in risk-free returns.

Let’s break down exactly what is happening and how to position your portfolio for January 1st.

In This Article:

• The “Senior Squeeze”: Why Your Take-Home Pay is Dropping

• The “Double Match” Opportunity: S$3,000 Risk-Free

• The “Opportunity Cost” Check: CPF vs. Popular REITs

• InvestingPro Reality Check

• The Wage Ceiling Hike: The S$8,000 Reality

• CareShield Life: Paying More, Getting More?

• The Verdict: Your January ChecklistWhy You Should Listen to Me

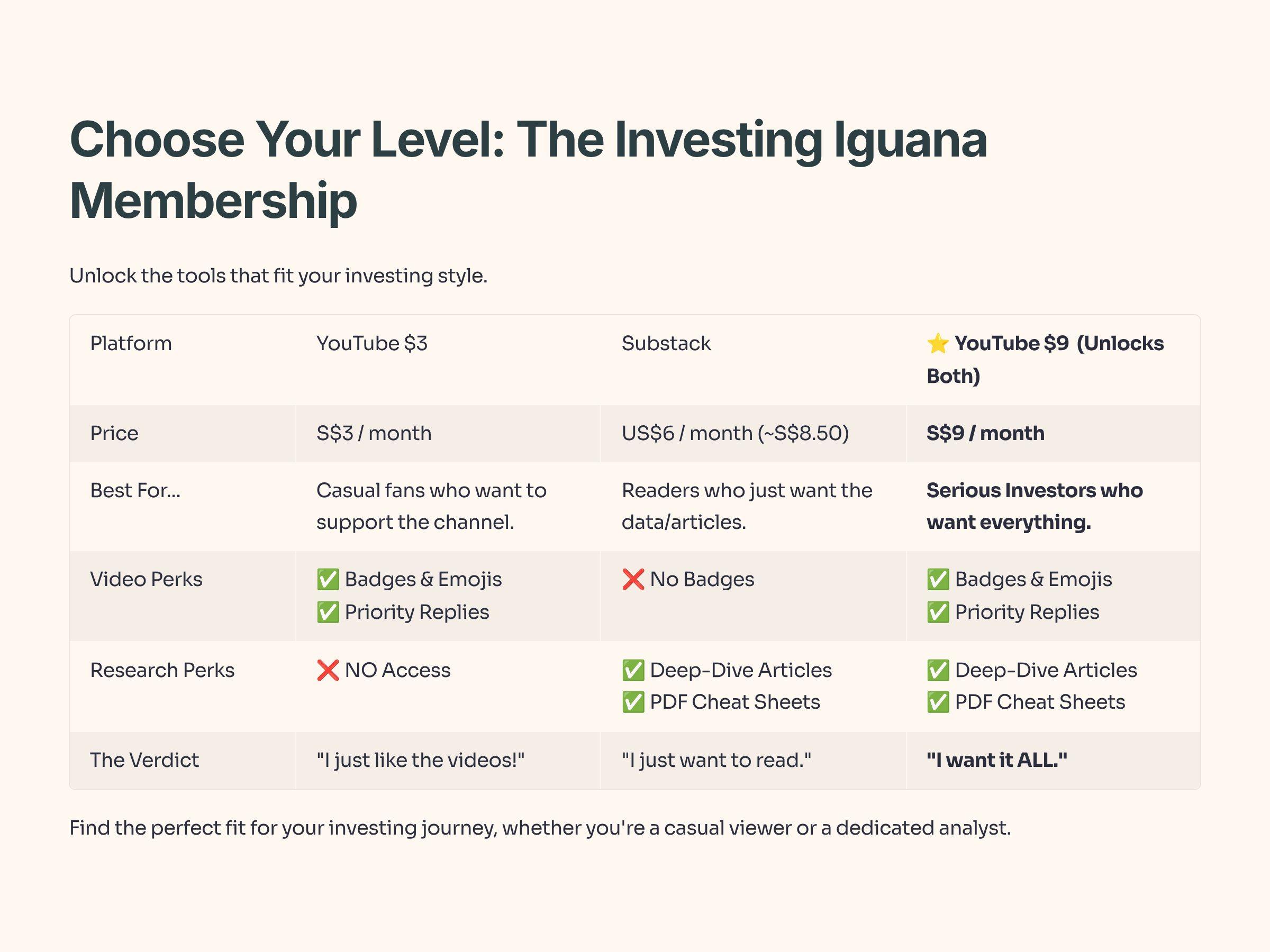

If you’re new here, welcome. I’m Iggy, your Singapore-based market analyst. Since October 2025, we’ve produced over 1,300 videos and 400 articles with 1.1 million watch hours. We are also home to a growing community of over 60 YouTube Premium subscribers and 30 paid Substack members who trust this data-driven approach.

Quick Housekeeping: If you want the best value, the YouTube Premium Membership (S$9/mth) bundles these deep-dive articles with the podcast videos. Substack alone is US$6, so the bundle is the ‘smart money’ move. Now, let’s get to the numbers.

1. The “Senior Squeeze”: Why Your Take-Home Pay is Dropping

The headline everyone ignores until they see their payslip: Contribution Rates are going up for workers aged 55 to 65.

From January 2026, the total CPF contribution rate for this age group rises by 1.5 percentage points.

0.5% comes from your employer (Great! Free money).

1.0% comes from YOU (Ouch. Less cash).

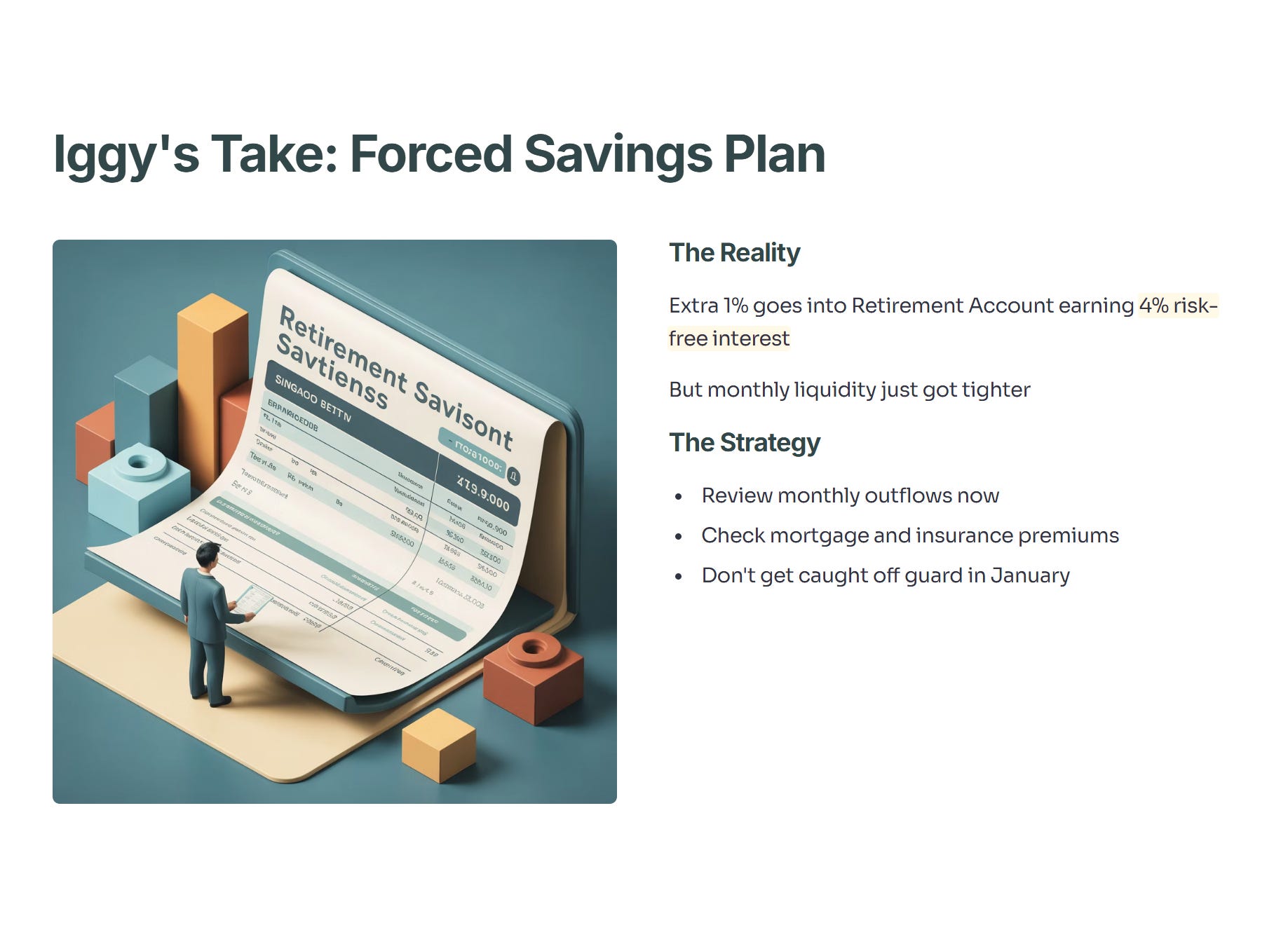

Iggy’s Take:

This is a forced savings plan, whether you like it or not. While the extra 1% goes into your Retirement Account (RA)—which earns that sweet 4% risk-free interest—it also means your monthly liquidity just got tighter.

The Strategy: Review your monthly outflows now. If you are servicing a mortgage with cash or have high insurance premiums, that 1% drop in disposable income might sting more than you think. Don’t get caught off guard in January.

2. The “Double Match” Opportunity: S$3,000 Risk-Free

This is the most important section of this article. If you ignore everything else, read this. The government is essentially handing out guaranteed returns to incentivize saving, and for 2026, they have doubled down.

We now have two matching schemes running simultaneously:

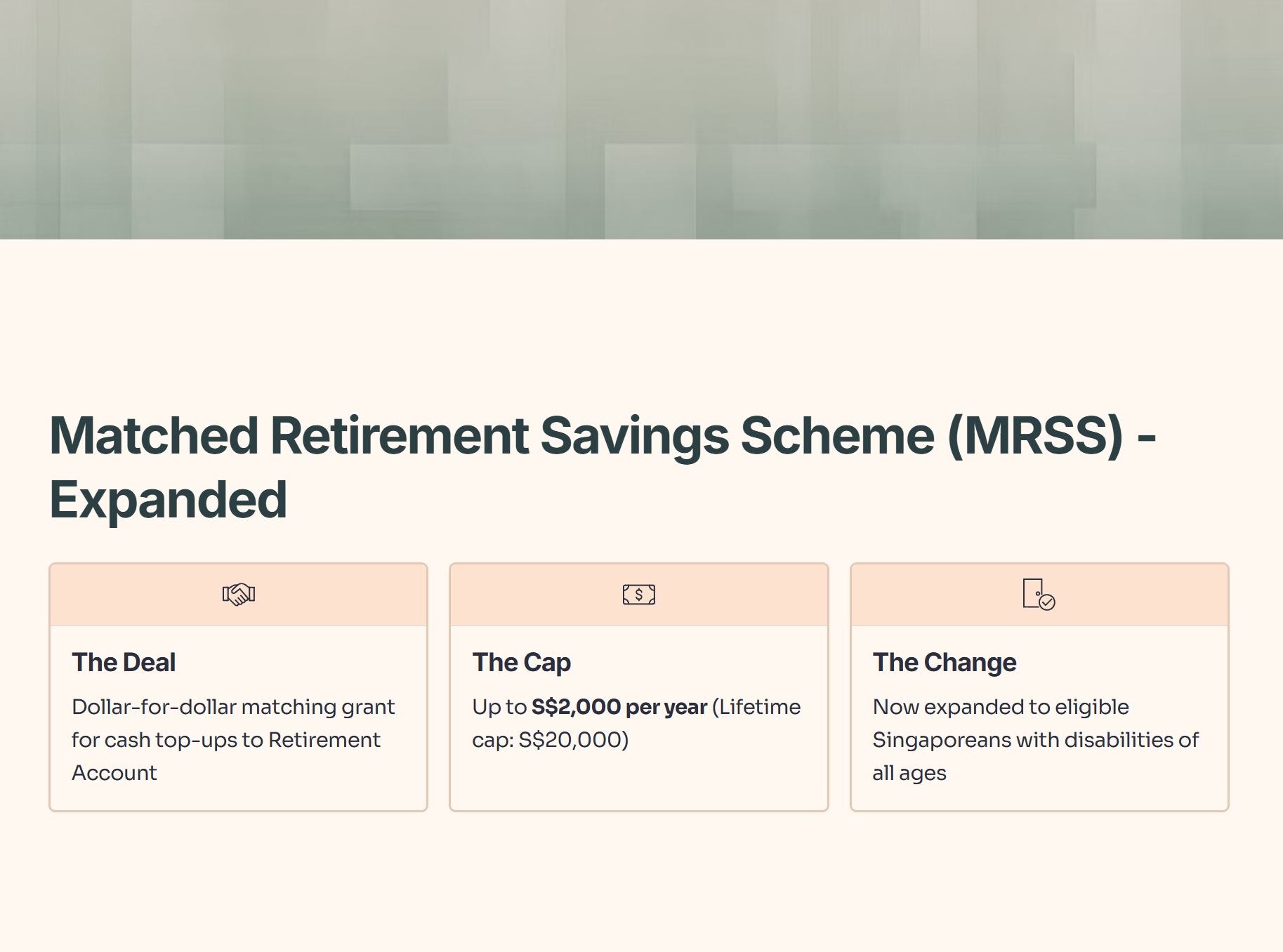

A. The Matched Retirement Savings Scheme (MRSS) - Expanded

The Deal: Dollar-for-dollar matching grant for cash top-ups to your Retirement Account (RA).3

The Cap: Up to S$2,000 per year (Lifetime cap: S$20,000).

The Change: Now expanded to eligible Singaporeans with disabilities of all ages.

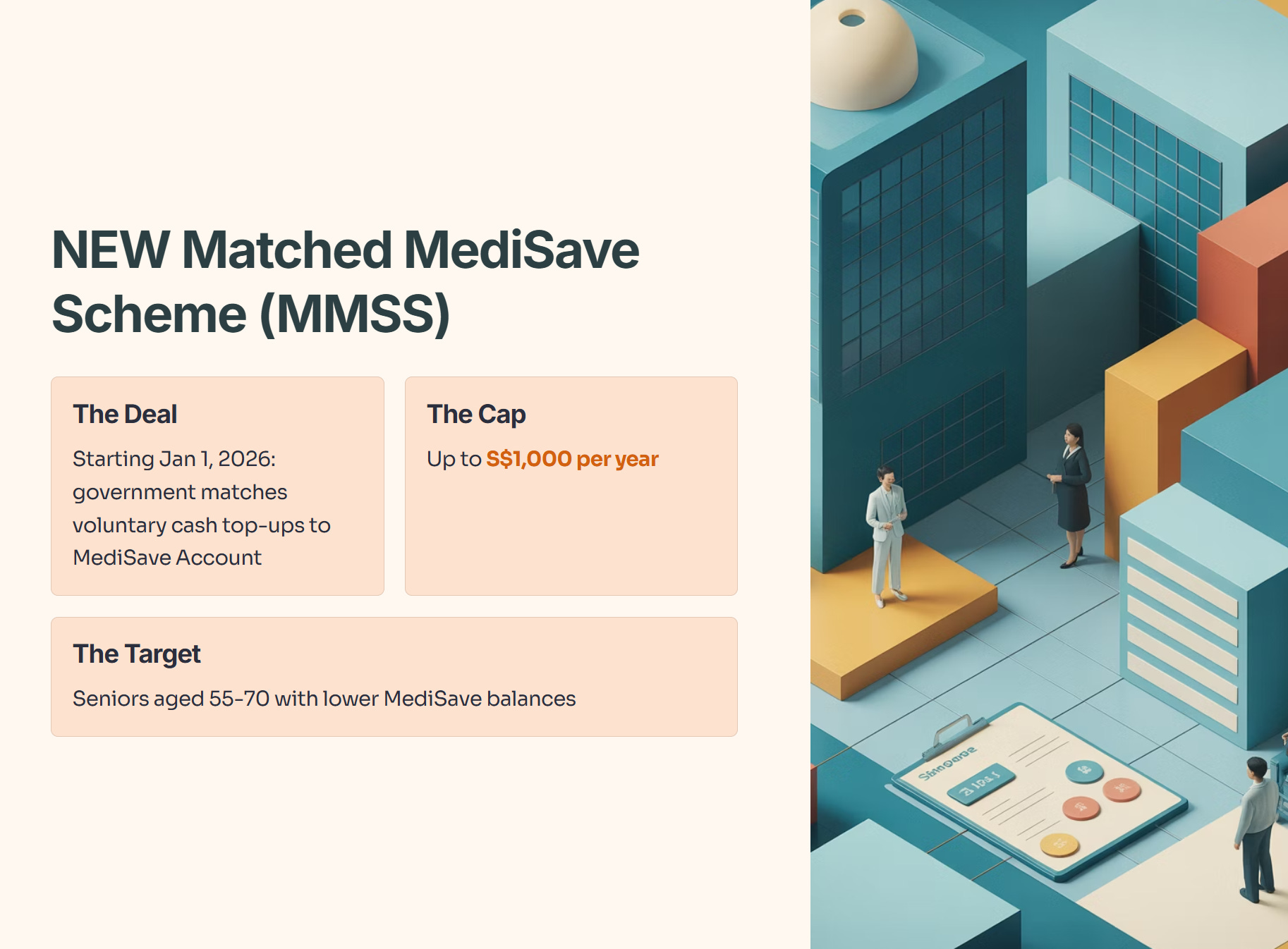

B. The NEW Matched MediSave Scheme (MMSS)

The Deal: Starting Jan 1, 2026, the government will match voluntary cash top-ups to your MediSave Account (MA).4

The Cap: Up to S$1,000 per year.

The Target: Seniors aged 55-70 with lower MediSave balances.

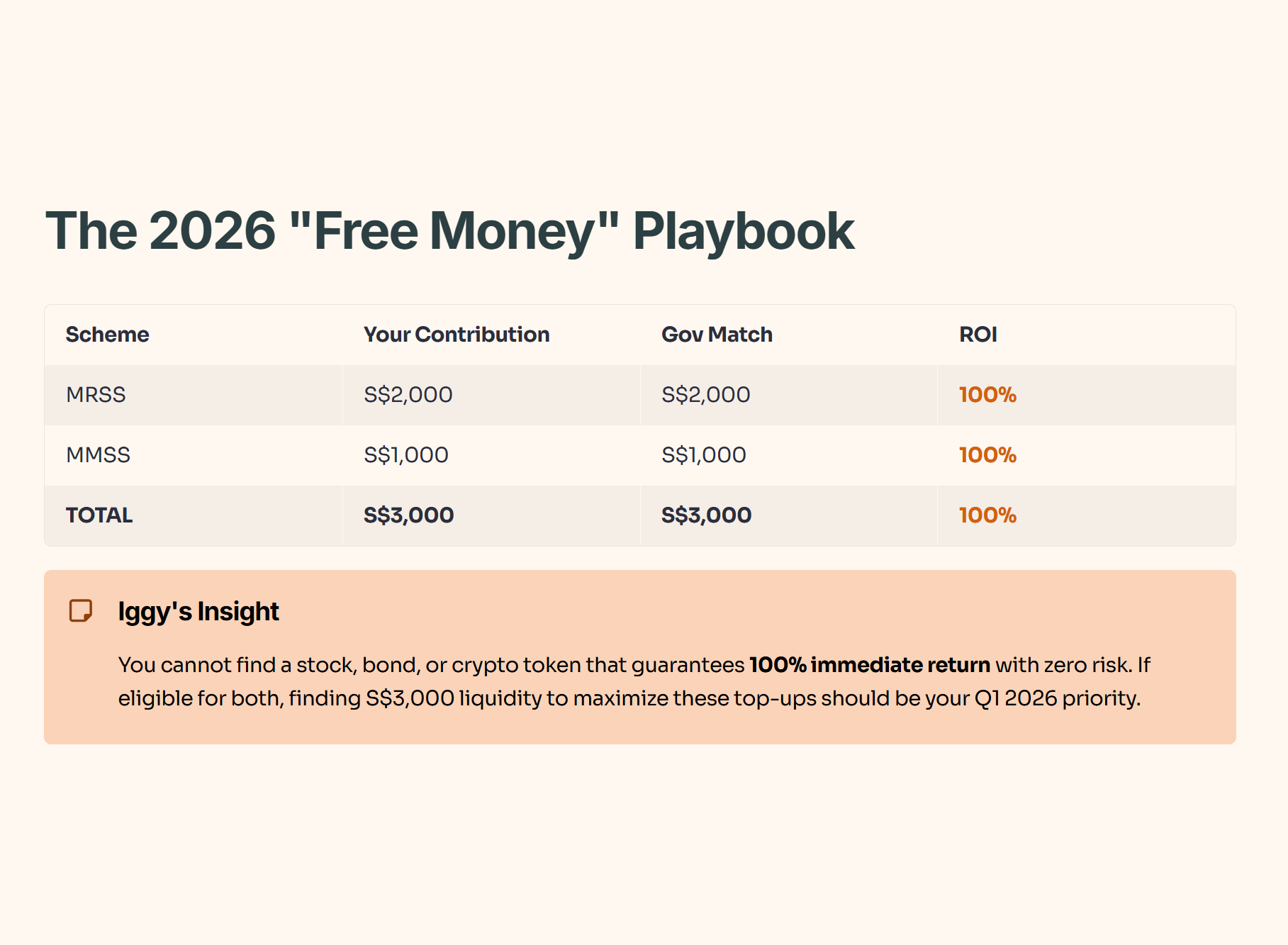

Table: The 2026 “Free Money” Playbook

Iggy’s Insight:

You cannot find a stock, a bond, or a crypto token that guarantees you a 100% immediate return with zero risk.

If you are eligible for both, finding S$3,000 of liquidity to maximize these top-ups should be your priority in Q1 2026. Yes, you can’t touch the money, but for retirement compounding, this beats DBS dividends any day of the week.

3. The “Opportunity Cost” Check: CPF vs. Popular REITs

With CPF offering 2.5% (OA) and over 4.0% (SA/RA/MA) risk-free, the bar for your stock investments is incredibly high.

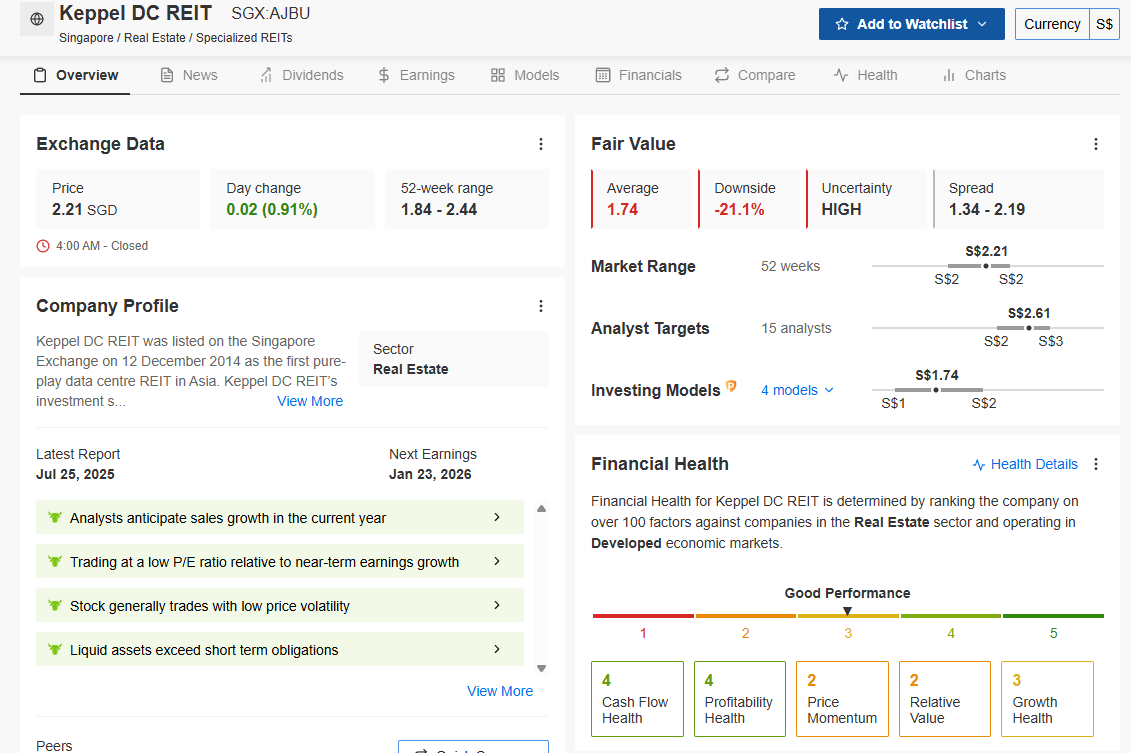

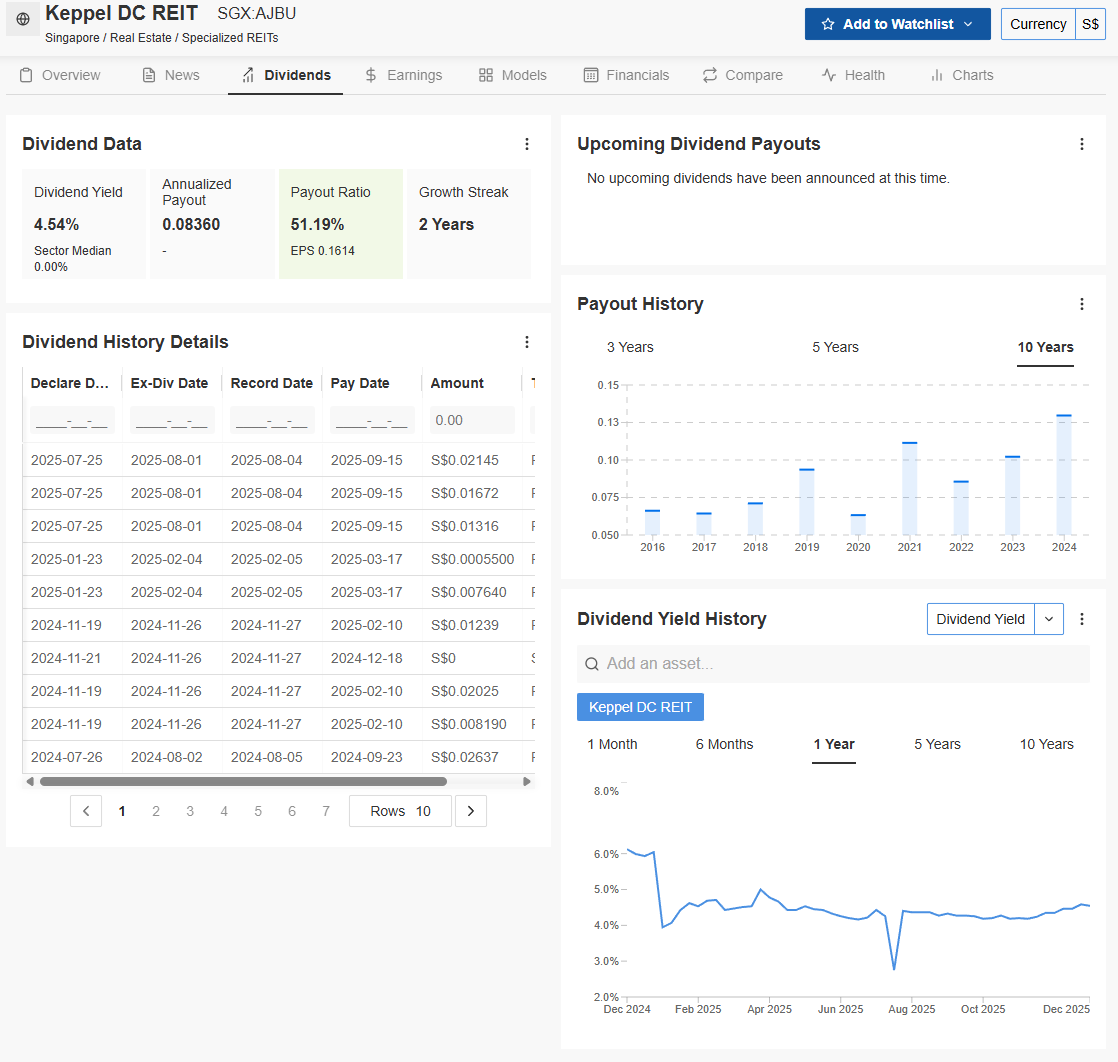

Let’s look at a crowd favorite: Keppel DC REIT (Data Centers). Everyone loves the “AI Data Center” narrative, but let’s look at the math.

I don’t just guess at safety. I check the institutional models.

Source: InvestingPro data. Unlock these institutional tools for yourself: Use code INVESTINGIGUANA for an exclusive 55% discount to kickstart 2026.

The Reality Check:

The Yield: 4.54%.

The Risk-Free Alternative (CPF SA/RA): ~4.08%.

The Spread: You are only getting an extra 0.46% for taking on equity risk.

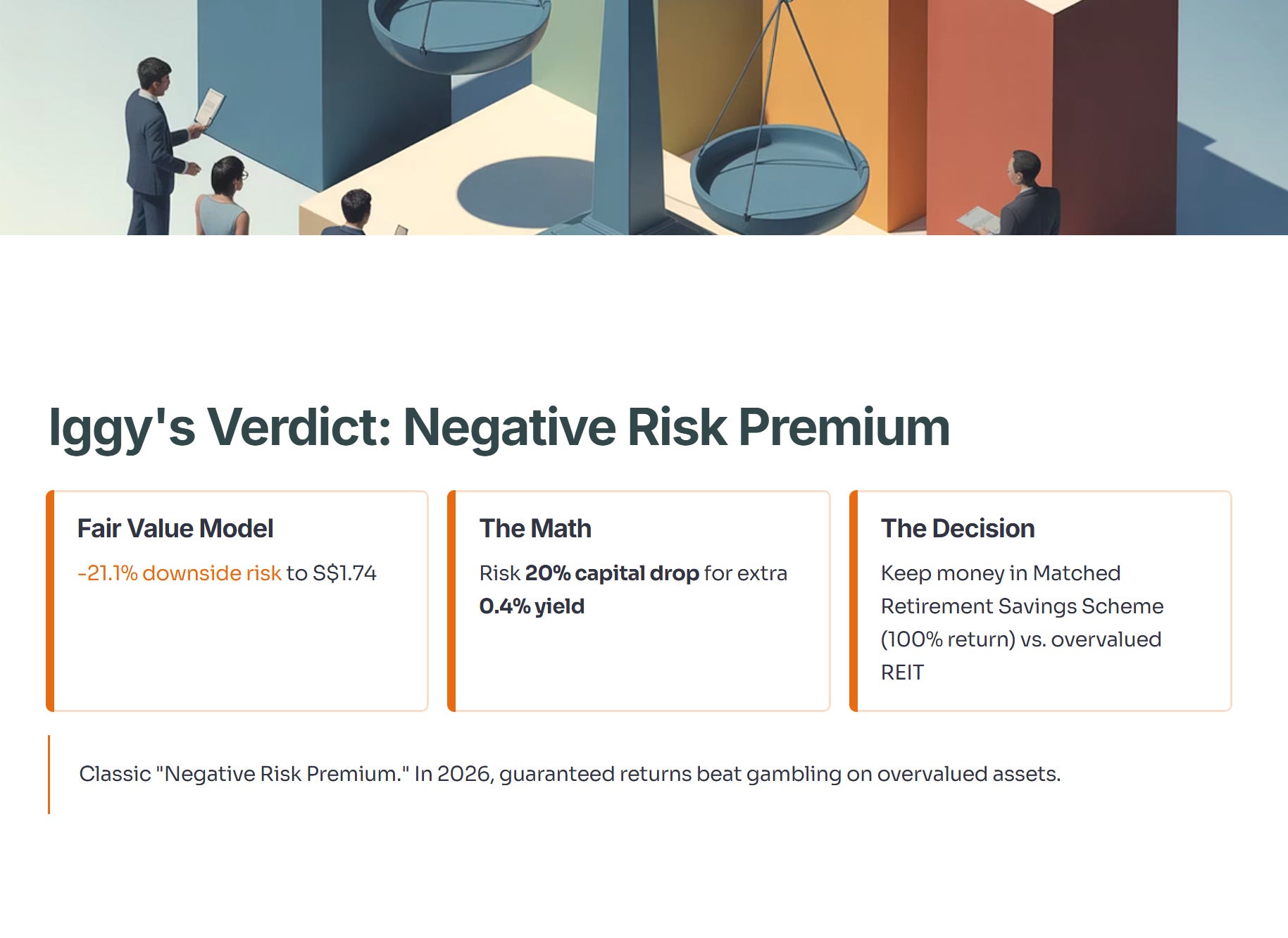

But here is the kicker: The Fair Value model suggests a -21.1% downside risk to S$1.74.

Iggy’s Verdict: This is a classic “Negative Risk Premium.” You are risking a potential 20% capital drop just to earn an extra 0.4% in yield. In 2026, I would rather keep that money in the Matched Retirement Savings Scheme (100% return) than gamble it on an overvalued REIT.

4. The Wage Ceiling Hike: The S$8,000 Reality