EPF 6.15% vs CPF 4%: The Ringgit Currency Trap

Chasing 6.30% across the Causeway ignores the 2.6% annual currency drag quietly eating your retirement.

We are looking at the Causeway not as a bridge for weekend trips, but as a pressure valve between two of the most sophisticated retirement engines in Asia.

Section 1: The Storm

Every major trade corridor in Southeast Asia eventually forces a choice between the speed of growth and the security of the vault. For decades, the Johor-Singapore Causeway has served as the physical manifestation of this tension — a strip of asphalt where capital, labour, and retirement dreams flow in opposite directions. On the northern end, the Employees Provident Fund (EPF) has long stood as a regional powerhouse, recently declaring a 6.30% dividend for 2024 that makes the Singaporean heartland look on with a mix of envy and confusion.

When that figure arrives from Kuala Lumpur, it creates a psychological ripple reaching all the way to the HDB blocks of Bedok and the coffee shops of Jurong East. The consensus narrative says Singaporeans are stuck in a low-yield trap, tethered to a 4% floor while their neighbours capture the upside of a more aggressive, equity-hungry investment mandate.

In This Article:

The Storm

The Wallet

The Evidence

The Scenario Matrix and SGX Sector Watch

The Singapore Investor Playbook

The Bottom Line

Iggy’s Forensic Compliance Standards — Standard Disclaimer

The Two Engines

The forensic gap lies in the structural architecture of these two engines and the invisible tax of currency volatility that most retail investors ignore until it is too late to pivot. On one side, a fund that operates like a global asset manager, chasing tech alpha and private equity gains to satisfy a domestic demand for high nominal returns. On the other, a Sanctuary model that prioritises the preservation of purchasing power in a Fortress currency.

For the Singaporean investor managing a CPF or SRS portfolio, the Storm is not a lack of yield. It is the potential for a total miscalculation of what real return actually looks like in a decade defined by regional currency shifts. The stakes for someone approaching age 55 in Queenstown are not theoretical. They are calculated in the difference between a retirement spent in a stable Sanctuary and one spent chasing a vanishing yield across a shifting border.

🦎 Iggy’s Insight

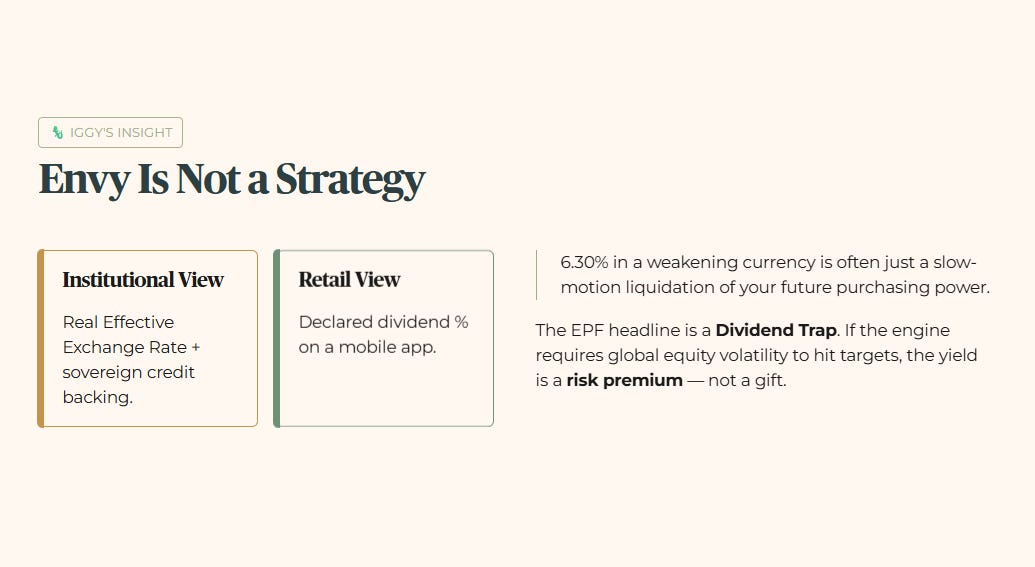

The psychological gap here is massive because institutional money treats the SGD/MYR corridor as a sophisticated carry trade, while the retail heartland treats it as a simple savings competition. Institutional players are looking at the Real Effective Exchange Rate and the sovereign credit backing of the underlying assets. The average investor is only looking at the declared dividend percentage on a mobile app.

The 6.30% EPF headline acts as a Dividend Trap for those who fail to account for the investment engine’s higher risk tilt. If the underlying engine requires global equity volatility to hit its targets, the yield is not a gift. It is a risk premium. Envy is not an investment strategy, and a 6.30% yield in a weakening currency is often just a slow-motion liquidation of your future purchasing power.

Section 2: The Wallet

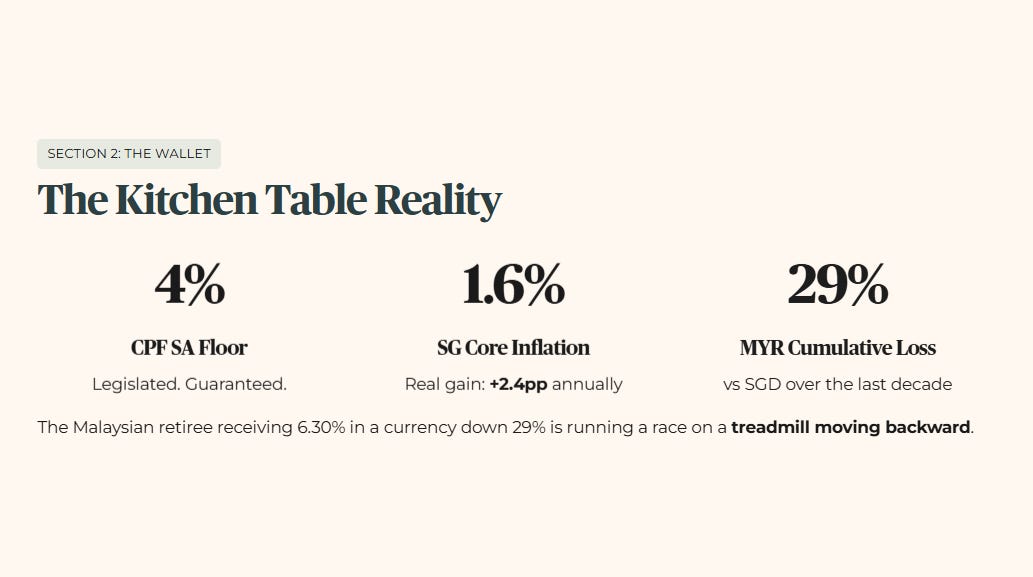

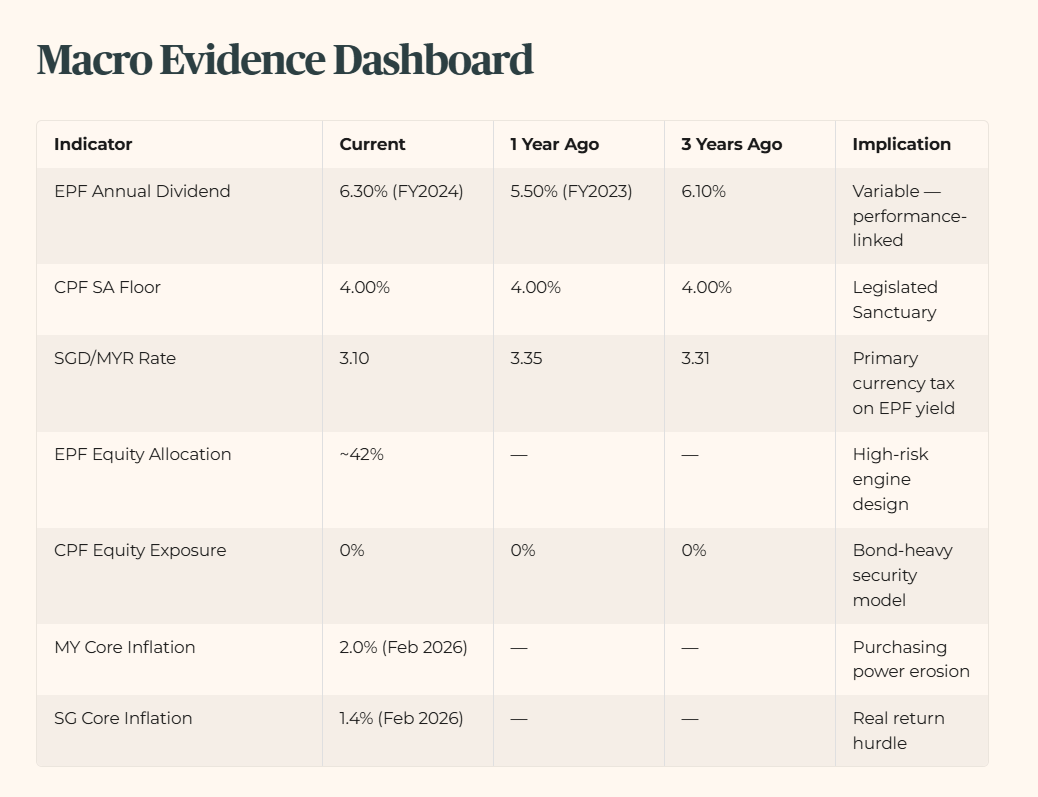

The reality of this regional yield gap hits the kitchen table the moment you look at the cost of living trajectory in a Fortress economy like Singapore. For a household in Toa Payoh or Woodlands, the 4% Special Account floor is not just a number in a ledger. It is a hedge against the relentless creep of imported inflation. Singapore’s core inflation sits at 1.6%. Your CPF SA is yielding 4%. That is a real gain of 2.4 percentage points annually, preserving your ability to buy the same basket of goods a decade from now. Conversely, the Malaysian retiree receiving 6.30% in a currency that has depreciated against the SGD by a cumulative 29% over the last decade finds themselves running a race on a treadmill that is moving backward.

For the investor managing SRS funds, the calculus is even more direct. The EPF’s heavy tilt into global tech, healthcare, and private equity means the fund is effectively running a high-conviction equity fund. If you are a 55-year-old in Singapore, the question is whether you want your retirement Sanctuary exposed to the same volatility as a Nasdaq-heavy portfolio, or whether you prefer the legislated guarantee of the CPF floor. You cannot spend a nominal percentage. You can only spend the value that remains after the currency market has taken its cut.

This regional dynamic is already repricing the way forensic investors look at SGX sectors, particularly the local banks and top-tier REITs. DBS, OCBC, and UOB essentially operate as the gatekeepers of Fortress capital. Their distributions are anchored in the same stability that supports the CPF floor. For the heartland investor, the wallet consequence of chasing regional yield is the potential neglect of these local yield generators that offer Sanctuary during periods of global rate shocks. If you shift capital out of a stable SGD environment to chase a nominal return across the Causeway, you are essentially shorting the Singapore Dollar. For a retiree whose expenses, medical, housing, and food, are all priced in SGD, that is a forensic gamble that rarely pays off when the math is stripped of its emotional headline.

🦎 Iggy’s Insight

There is a second-order effect retail investors are completely missing: the Legislated Floor versus Dividend Declaration models. The CPF 4% is a hard floor that has not moved in decades, providing a predictable Sanctuary benchmark for all other Singaporean assets. The EPF yield is a variable declaration based on annual performance. In a bad year for global equities, that number can shrink, and has, whereas the 4% CPF SA floor is a sovereign promise. The market is currently pricing in a stability premium for the SGD that makes the 4% floor functionally superior to a volatile 6% elsewhere. A guarantee you can bank on is always worth more than a maybe you have to chase.

Section 3: The Evidence

The evidence shows that the yield gap is a product of two entirely different mechanical designs, not a difference in management competence.

Forensic Verdict Beat: The 10-year currency depreciation math reveals that the 6.30% advantage is a statistical illusion for any investor who eventually needs to spend their capital in Singapore Dollars.

Table 1 — Macro Evidence Dashboard

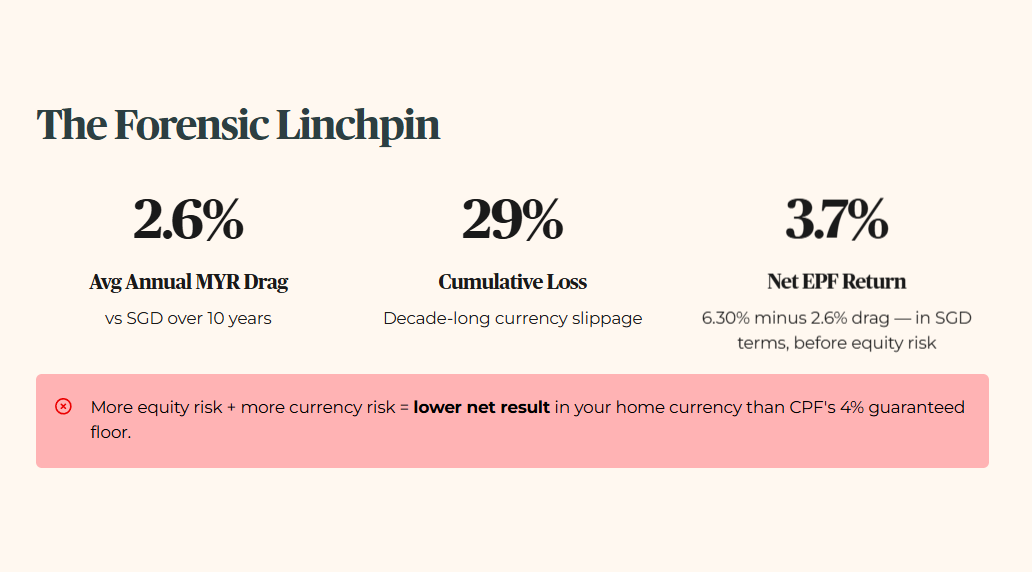

The forensic linchpin of this entire audit is the 2.6% average annual depreciation of the MYR against the SGD over the last ten years, compounding to a cumulative 29% currency loss over the decade. This single number makes the rest of the noise about which fund is better largely irrelevant for a Singapore-based retiree. If you start with S$100,000, convert it to MYR to capture the EPF yield, and convert it back a decade later, the currency slippage acts as a 29% cumulative drag on your capital.

The arithmetic is straightforward: 6.30% annual yield minus 2.6% average annual currency drag leaves approximately 3.7% net return in SGD terms before accounting for the equity risk premium the EPF engine requires to hit its target. When you compare that to the 4.0% risk-free, guaranteed, zero-volatility return of the CPF Special Account, the Regional Envy narrative collapses entirely. You are taking significantly more equity risk and currency risk for a lower net result in your home currency.

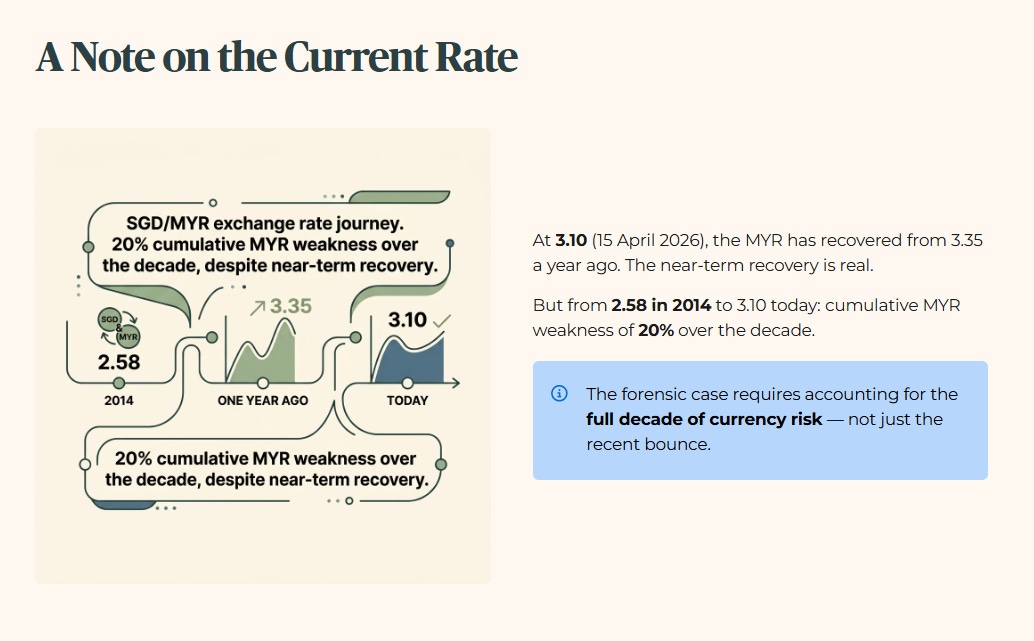

Note on the current SGD/MYR rate: at 3.10 as of 15 April 2026, the MYR has recovered from the 3.35 level of a year ago. That near-term recovery is real and worth acknowledging. The 10-year depreciation story from 2.58 in 2014 to 3.10 today still reflects cumulative MYR weakness of 20% against the SGD over the decade. The forensic case does not require the MYR to weaken every single year. It requires the retirement investor to account for the full decade of currency risk they are accepting when they lock capital into a non-SGD retirement vehicle.

nce you run the full 6.30% minus 2.6% annual drag against CPF’s legislated 4.0% floor over a decade in SGD terms, the “higher yield” story doesn’t just narrow — it inverts.