CPF LIFE Case Study: Engineering a $4,600 Monthly Payout (2026 Guide)

Because your retirement shouldn't depend on the price of Cai Fan staying at $4.00 forever.

Master the exact compounding mechanics to turn your mandatory savings into an iron bastion of tax-free retirement income.

You are 54 years old. You are sitting at the void deck of your Bedok / Marine Parade HDB block on a Sunday evening. You open your CPF statement on your phone. The number looks big. But you have no idea if it is enough. So you close the app and go back to watching the news. This is the precise moment when the anxiety hits.

It is the fear of outliving your CPF savings. It is the confusion about CPF LIFE payout options. It is the quiet, nagging uncertainty about whether you should be doing Special Account top-ups or SRS contributions. And let’s be honest, you are not alone.

Most Singaporeans carry this exact anxiety. But here is the uncomfortable truth. That anxiety exists purely because you are missing the forensic math.

By the end of this masterclass, you will understand exactly how much your CPF SA is earning every month, how to calculate your projected CPF LIFE payout, and which three actions available to you right now will have the greatest impact on your retirement income. You will know exactly how to turn this system into your personal fortress.

🦎 Iggy’s Insight:

Most Singaporeans treat their CPF like a locked drawer they cannot open. They see the monthly deduction on their payslip and feel an immediate sense of loss. But here is the uncomfortable truth about that mindset. It blinds you to the most powerful risk-free compounding engine available in Asia. While retail investors chase volatile dividend stocks hoping for a temporary yield, they completely ignore the guaranteed structural returns sitting right in front of them. It is like queuing for an hour at a hyped kopitiam stall while the Michelin-starred chicken rice uncle next door has no line. The math is clear. Your CPF is not a tax. It is your ultimate financial fortress.

In This Article:

The Life Stage Framework (The Core)

Stage 1: The Accumulation Phase (Age 30-54)

Stage 2: The Pre-Retirement Transition (Age 55-64)

Stage 3: The Drawdown Phase (Age 65+)

Stage 4: The Estate and Legacy Consideration

The Policy Change Radar

The Worked Example (The Live Case Study)

InvestingPro Reality Check

The VerdictAbout Iggy & the Elite 170

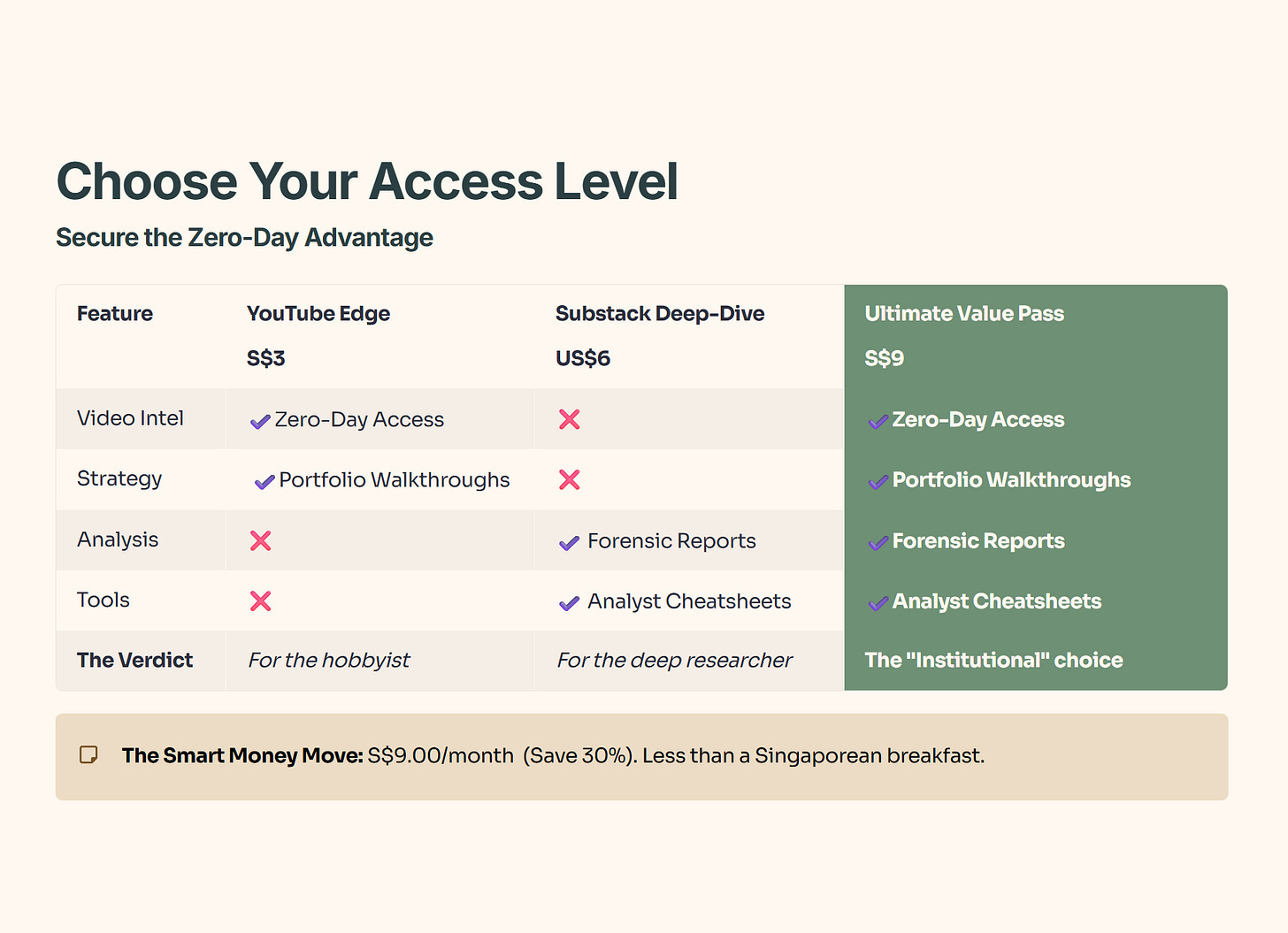

In the Singapore market, the gap between a smart entry and becoming someone else’s exit liquidity can be as little as 48 hours. That’s the cost of informational lag.

Free subscribers get my analysis up to 14 days later. The Elite 170 get it the moment it’s ready.

Your Edge:

The S$9 Ultimate Value Pass bundles zero-day video intel, forensic reports, and analyst cheatsheets into one institutional-grade feed — for less than a Singaporean breakfast.

The Life Stage Framework (The Core)

Stage 1: The Accumulation Phase (Age 30-54)

The primary objective in this phase is entirely mathematical. You are maximising CPF Special Account compound growth before the withdrawal age. The policy fact here is straightforward. The CPF Special Account currently generates a baseline 4.0% per annum. Historically, this 4.0% floor has been maintained through massive macroeconomic shifts. When global interest rates were near zero five years ago, this floor held firm.

Compared to the Australian Superannuation system, which fluctuates wildly with market equity cycles, Singapore’s SA is structurally superior for capital preservation. If global rates drop by 10% in the coming years, this 4.0% floor acts as an absolute shield. For a 45-year-old Singaporean, the wallet impact is immense. Every dollar inside the SA doubles roughly every eighteen years without you lifting a finger.

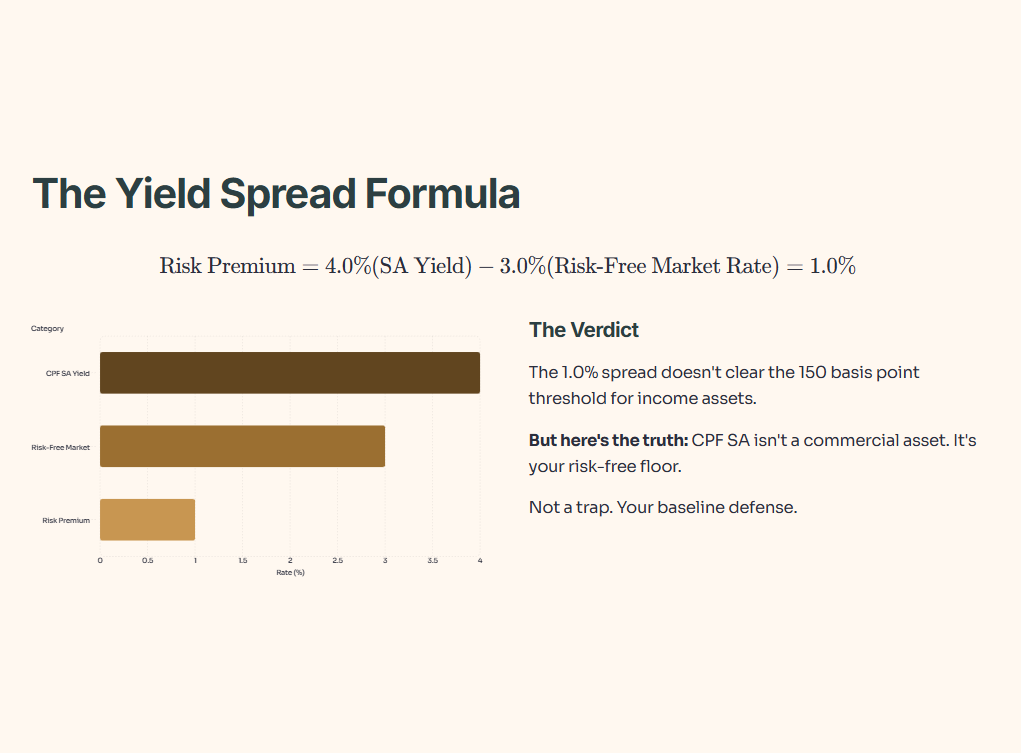

Let’s apply the Yield Spread formula to the CPF SA:

Risk Premium=4.0%(SA Yield)−3.0%(Risk-Free Market Rate)=1.0%

The calculated spread is 1.0%. And let’s be honest, this does not clear the 150 basis point minimum threshold we usually demand for income assets. But here is the uncomfortable truth. The CPF SA is not a commercial asset. It is the Iron Bastion. It is the risk-free floor of your entire portfolio.

So, is this a trap? No. It is your baseline defense. The key mechanism here is the voluntary SA top-up to hit the Full Retirement Sum of $220,400. You can also transfer funds from your Ordinary Account to your SA to capture that higher yield. This builds your runway to eventually hit the Enhanced Retirement Sum of $440,800.

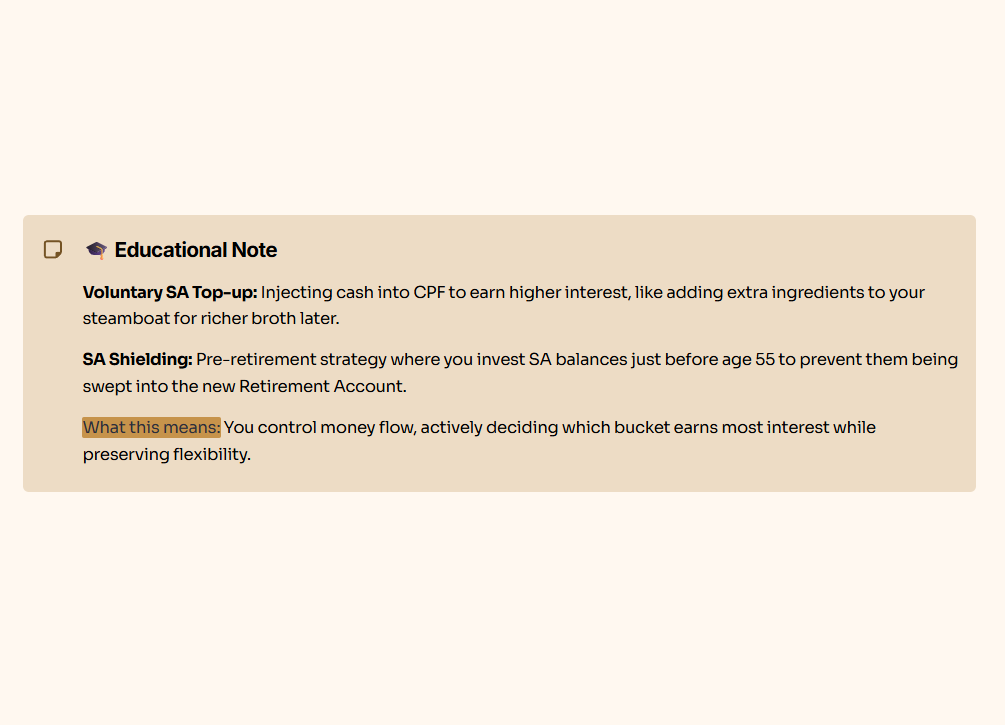

🎓 Educational Note: Let’s define that term. A Voluntary SA Top-up is simply injecting your own cash into the CPF system to earn higher interest, much like putting extra ingredients into your steamboat to make the broth richer later. SA Shielding is a pre-retirement strategy where you invest your SA balances just before age 55 to prevent them from being swept into the new Retirement Account. So what does this mean for you in practice? It means you control the flow of your money, actively deciding which bucket earns the most interest while preserving your flexibility.

🦎 Iggy’s Insight:

The single most underutilised strategy in the Accumulation Phase is the early-year voluntary top-up. Most Singaporeans wait until December to inject cash for tax relief. But here is the uncomfortable truth. CPF interest is calculated monthly based on the lowest balance.

By topping up in December, you forfeit eleven months of compounding. Doing this in January instead is like getting free rent at your hawker stall for a whole year. Over a twenty-year accumulation phase, this simple timing shift generates tens of thousands of dollars in pure, unearned passive income. The math rewards the decisive.

“You’ve seen how the Accumulation Phase works. Next, we’ll step into the danger zone from 55–64 — where one wrong CPF move can permanently shrink your lifetime payout (and one right move can lock in an extra four-figure income stream).”