CPF LIFE vs Age 95 Inflation Math Analysis

Defaulting to Standard Plan payouts structurally guarantees you lose purchasing power to medical inflation before your 80th birthday.

CPF LIFE Standard Plan Risks Poverty At Age 95

Most Singaporeans turning 55 this year will leave over S$60,000 in compounding purchasing power on the table by defaulting to the standard payout structure.

If you are fifty-five this year and you default to the CPF LIFE Standard Plan without calculating your personal crossover age, you are structurally guaranteeing a permanent erosion of your purchasing power by your eightieth birthday.

The terminal wealth gap between an escalating and flat payout over a thirty-year horizon often exceeds S$60,000 for a fully funded account, stripping your specific retirement income of its ability to absorb medical inflation. Here is exactly how to calculate the mathematical break-even point and position your CPF LIFE and SRS architecture to outlive your baseline expenses.

In This Article:

Stage 1 The Compounding Window Age 30–54

Stage 2 The Pivot Point Age 55–64

Stage 3 The Drawdown Architecture Age 65+

Stage 4 The Legacy Layer Estate Planning

The Policy Change Radar

The Live Case Study The Marine Parade Household

Strategic Considerations

CPF Disclaimer Addendum

Standard Forensic Disclaimer

About Iggy & the Elite Investors

The Crash Wasn’t a Surprise. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided before the opening bell — not after the damage is done. The red flags are always there. The question is whether you had the forensic framework to read them in time.

Iggy’s Elite Investors didn’t chase the headline yield. They had the full forensic breakdown — the gearing ratios, the occupancy gaps, the debt overhang — before the market opened and before the price moved. Zero-day reports, the complete “Red Zone” watchlist, and institutional-grade cheatsheets that flag the landmines disguised as opportunities.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

Stage 1: The Compounding Window (Age 30–54)

Before we can calculate the longevity risk of your CPF LIFE payout, we must address how you build the capital base in your accumulation years. The years between thirty and fifty-four represent the definitive compounding window. During this phase, your Special Account (SA) is the primary engine of your retirement architecture.

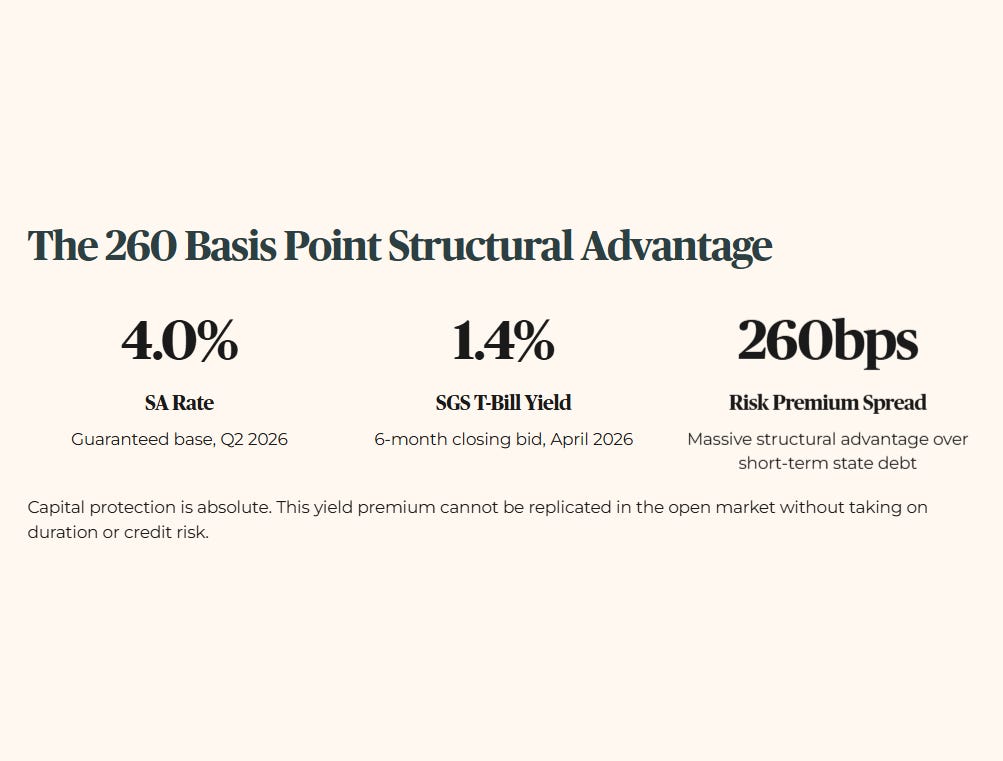

The baseline mechanic is straightforward: the Special Account currently pays a guaranteed base rate of 4.0% per annum for Q2 2026, unchanged from the Savings Mortgage Rate (SMRA) floor. When we look at the historical context, this 4.0% floor has remained a static sanctuary through both zero-interest-rate environments and recent inflationary spikes.

From a global comparison perspective, this risk-free yield vastly outperforms the fixed-income allocations of UK pension schemes or Australian Superannuation funds, which are forced to take on duration risk to chase similar returns. In a forward scenario, if global interest rates were to collapse by 10% over the next decade due to a macro recession, this policy floor mathematically shields your retirement baseline from the volatility. The wallet impact is absolute: for a forty-year-old heartland earner with S$120,000 in their SA, this mechanism guarantees S$4,800 of annual compound interest, entirely immune to Straits Times Index fluctuations.

We evaluate this using a strict risk premium framework. The risk premium is your SA rate minus the current risk-free market alternative. Today, that means taking the SA rate of 4.0% and subtracting the current six-month SGS T-Bill closing bid yield of approximately 1.4% per annum as at early April 2026. That spread — 260 basis points — represents a massive structural advantage over short-term state debt. The capital protection is absolute, and the yield premium is not something you replicate in the open market without taking on duration or credit risk.

Iggy’s Insight: Think of your Special Account like an HDB lift upgrading programme. It is slow, highly structured, and entirely outside your daily control, but it guarantees that the value of your property is elevated permanently. Voluntary top-ups during this window act as an accelerant. The opportunity cost of early liquidity is the single greatest threat here.

When you use excess cash to chase higher yields in the private market, you are abandoning a guaranteed structural floor. Unless your private portfolio consistently clears the minimum yield hurdle of 4.7% — that is the Iggy Forensic Floor of 3.2% plus 150 basis points of mandatory risk premium — across a full market cycle, the forensic picture suggests that maxing out your CPF limit is the superior capital allocation.

Stage 2: The Pivot Point (Age 55–64)

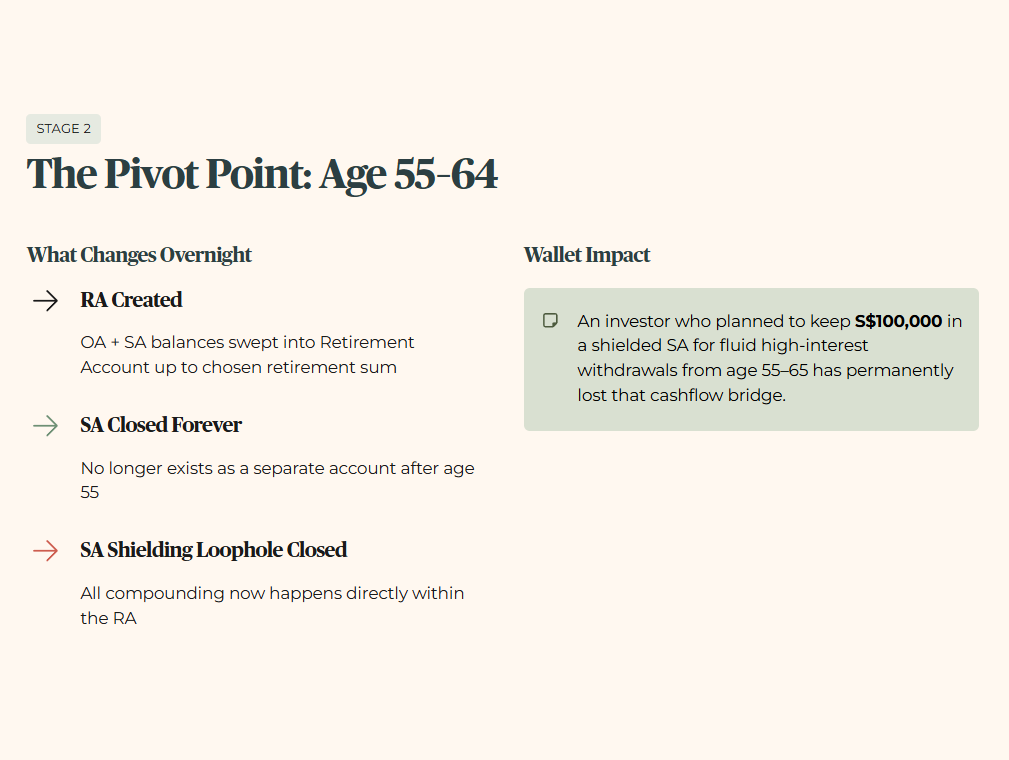

At age fifty-five, the structural rules of your retirement change overnight. This is the pivot point. The mechanics of the Retirement Account (RA) creation are activated. Your Ordinary Account (OA) and Special Account balances are swept to form your RA, up to your chosen retirement sum limit.

This brings us to the most critical, yet widely misunderstood, mechanic for our core readership: the closure of the Special Account at age 55. The SA no longer exists as a separate account after this point. All balances are swept into the RA up to your applicable retirement sum, with any excess remaining in the OA.

Historically, savvy retail investors used the SA shielding loophole to manually park OA funds into high-yield instruments, forcing the RA to draw from the lower-yielding OA.

Globally, very few pension systems allow such granular arbitrage, which is exactly why the policy was tightened. In a forward scenario, this forces all compounding to happen directly within the RA, removing the secondary 4.0% liquidity pool. The wallet impact is profound: an investor who planned to keep S$100,000 in a shielded SA for fluid, high-interest withdrawals from age 55 to 65 has permanently lost that specific cashflow bridge.

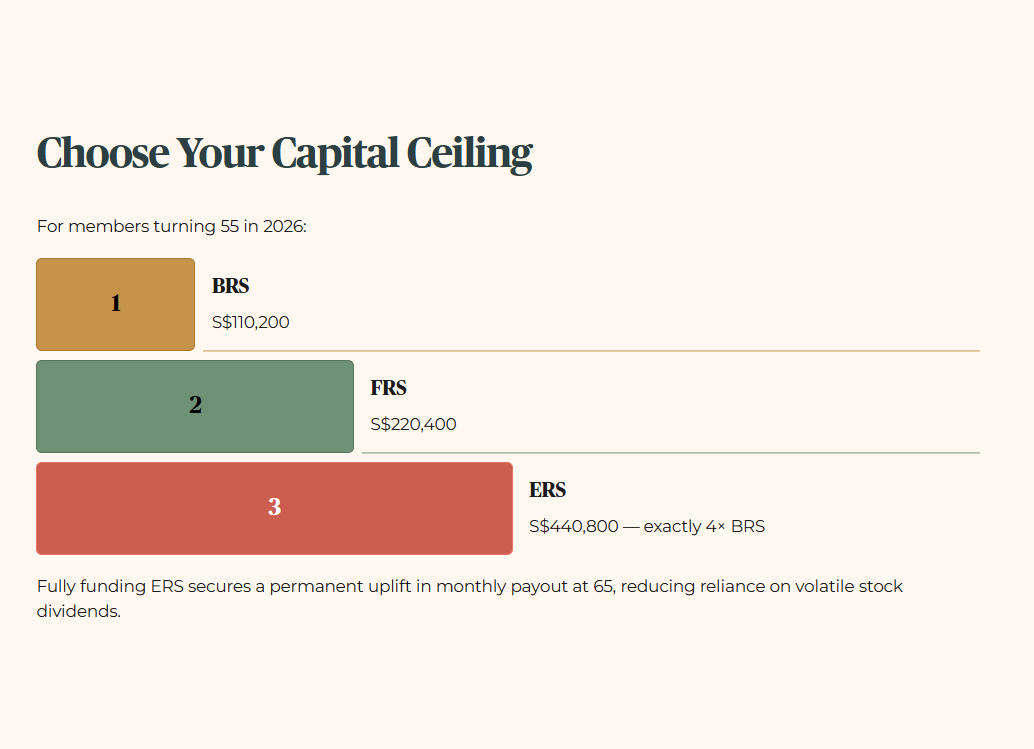

During this decade, you must actively define your capital ceiling. You have three paths: the Basic Retirement Sum (BRS), the Full Retirement Sum (FRS), or the Enhanced Retirement Sum (ERS). For members turning 55 in 2026, the figures are as follows: the BRS stands at S$110,200, the FRS at S$220,400, and the ERS at S$440,800 — which in 2026 happens to be exactly four times the BRS. These sums increment annually to pace core inflation. In a forward scenario, a 10% upward revision in these policy sums requires immediate top-ups from your SGX dividend portfolio to maintain the highest payout bracket. The wallet impact is decisive. A household that fully funds the ERS at S$440,800 rather than stopping at the FRS secures a permanent uplift in their baseline monthly payout at age 65, mathematically reducing their reliance on volatile stock dividends.

But once you lay the ERS decision alongside the actual CPF LIFE Standard versus Escalating payout projections, the break-even age calculation rewrites how much risk your portfolio can afford to carry past 80.