CPF Special Account Closure 2025: What’s Next for Your Retirement Plan?

The CPF Special Account has closed for those aged 55 and above from January 2025. What should you do with your savings, and where can you find safe, steady growth now?

Why This Matters to You Right Now

Earlier this year (on January 19, 2025), the CPF Special Account closed for all members aged 55 and above. This is not a small tweak. It affects tens of thousands of Singaporeans every year who turn 55 and suddenly need to rethink where their retirement savings sit.

If you counted on the Special Account’s 4% guaranteed interest to grow your nest egg risk-free, that chapter is done. Your SA balance has already moved to your Retirement Account up to the Full Retirement Sum, and any excess landed in your Ordinary Account, where it earns just 2.5% per year. That is a big drop in returns if you do nothing about it.

The good news? You have choices. Safe ones. Income-generating ones. And you do not need to be a market wizard to make them work. But you do need to plan, and you need to start now before inflation eats into your purchasing power.

In This Article:

• The Special Account: What It Was and Why It’S Gone

• Post-SA Closure: Where Your Money Goes

• CPF Retirement Sums 2025 Comparison

• Your Options After the Special Account Closure

• Option 1: Transfer OA Savings Back to RA

• Option 2: Singapore Savings Bonds

• Option 3: Fixed Deposits

• Option 4: Supplementary Retirement Scheme (SRS)

• Safe Investment Alternatives Comparison (October 2025)

• Chasing Income: Dividend Stocks and REITs

• Singapore Banks

• Singapore REITs

• Building a Balanced Portfolio: ETFs and Unit Trusts

• Straits Times Index ETFs

• Unit Trusts

• CPFIS Investment Options for Your CPF Funds

• Three Investor Profiles: Which One Are You?

• Profile 1: Ultra-Cautious Saver

• Profile 2: Income-Seeker

• Profile 3: Balanced Investor

• Three Investor Profiles: Action Plan Summary

• Final Thoughts: Change Can Be Scary, But Also an OpportunityThe Special Account: What It Was and Why It’s Gone

The CPF Special Account was always about retirement. It earned higher interest than the Ordinary Account, compounded quietly over the years, and gave peace of mind to those who wanted to keep things simple. Many relied on it as a steady, hands-off way to grow their retirement funds without market risk.

But from January 19, 2025, that account closed for everyone aged 55 and above. The reason? The government wanted to streamline the system. Now, only savings committed for long-term retirement get the higher interest rate of 4%. Savings you can withdraw should earn the short-term rate.

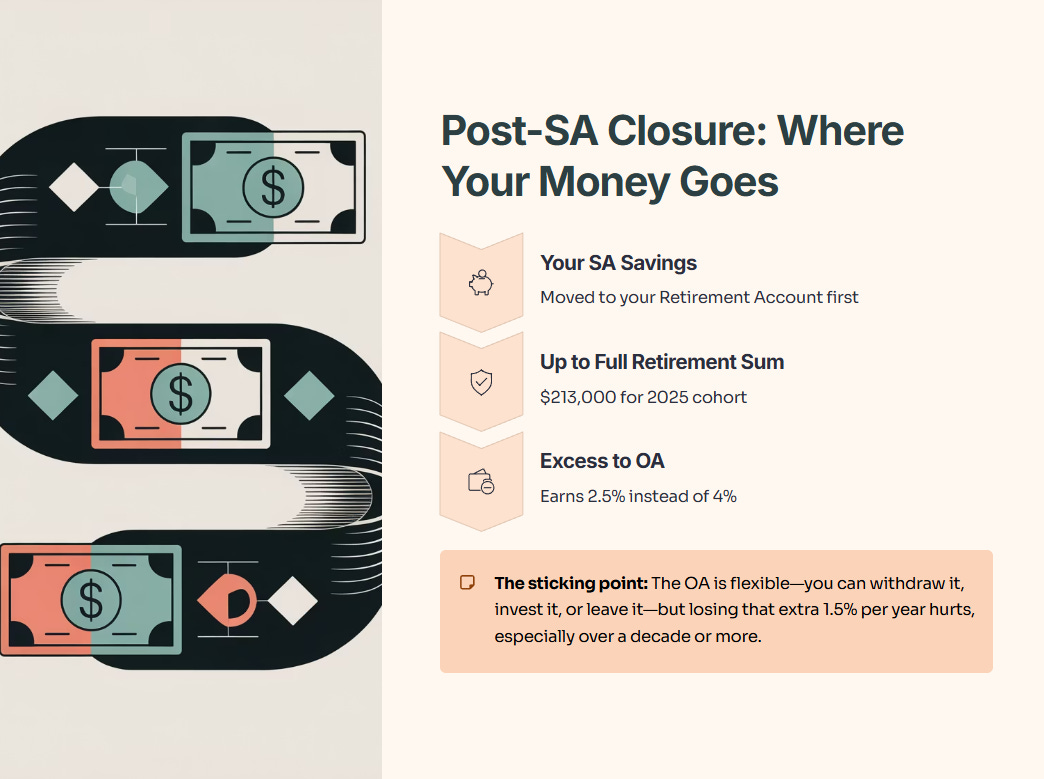

Post-SA Closure: Where Your Money Goes

Here is what happened. Your SA savings moved to your Retirement Account first, up to the Full Retirement Sum for your cohort. In 2025, that Full Retirement Sum is $213,000. If you had more than that in your SA, the rest went to your OA. Once in the OA, that money earns 2.5% instead of 4%.

That is the sticking point. The OA is flexible—you can withdraw it, invest it, or leave it—but the interest rate is lower. For many retirees, losing that extra 1.5% per year hurts, especially over a decade or more.

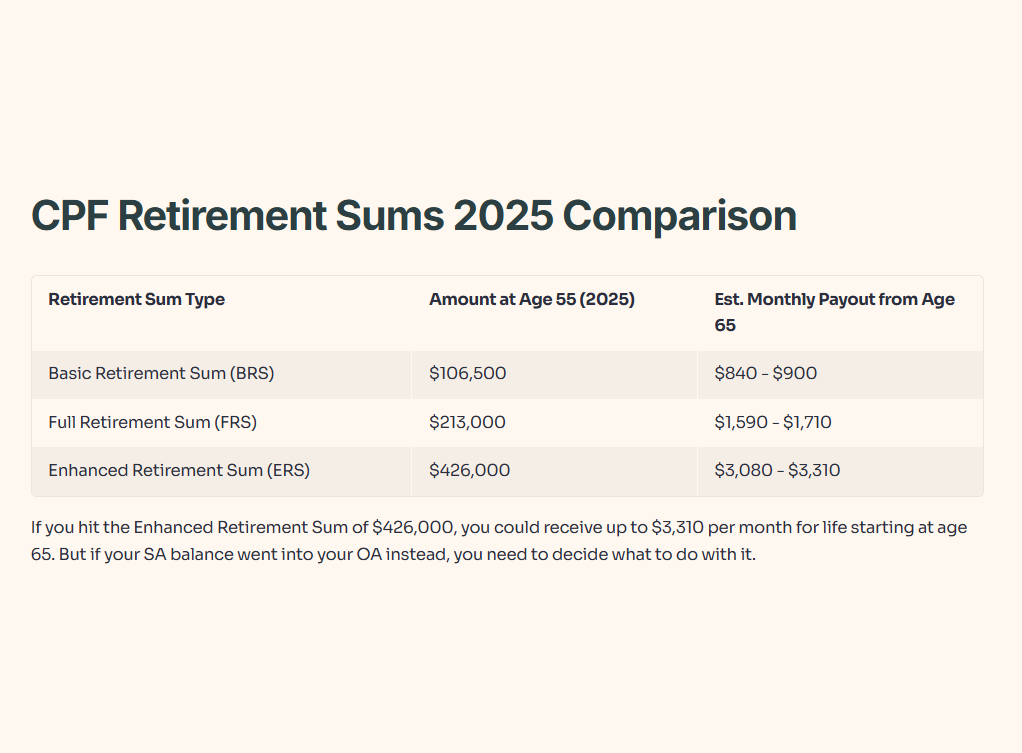

CPF Retirement Sums 2025 Comparison

The table above shows what you can expect depending on how much you set aside in your Retirement Account by age 55. If you hit the Enhanced Retirement Sum of $426,000, you could receive up to $3,310 per month for life starting at age 65. That is a solid baseline. But if your SA balance went into your OA instead, you need to decide what to do with it.

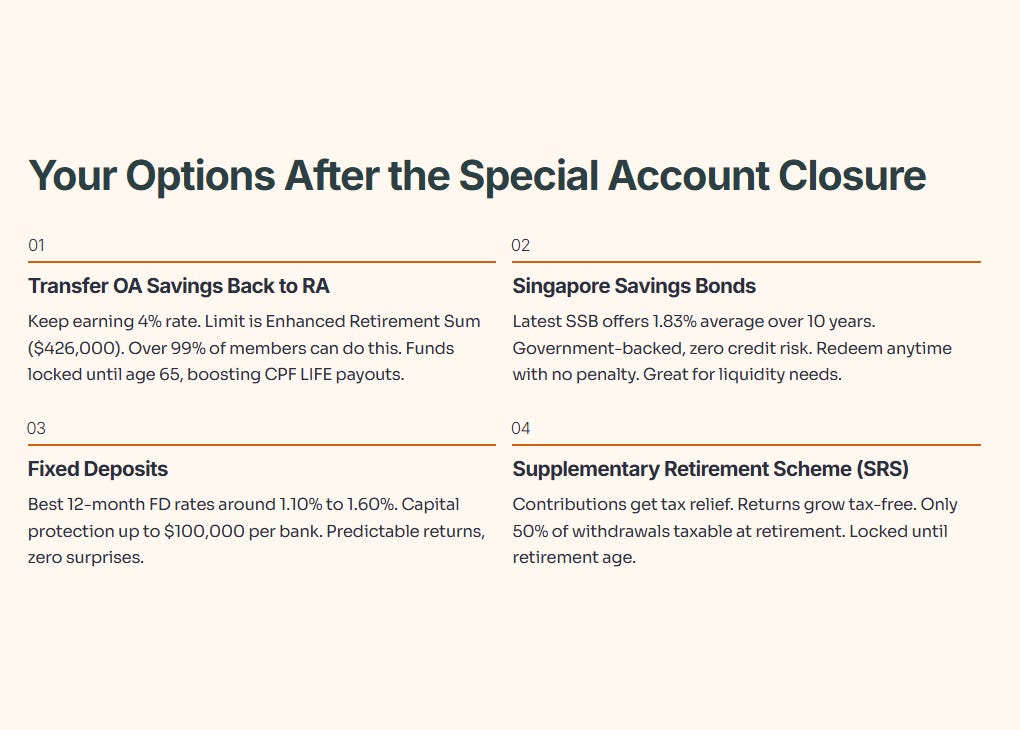

Your Options After the Special Account Closure

Once your SA closed, your money split between the RA and the OA. The RA portion is locked until age 65, where it streams out as CPF LIFE payouts. But the OA portion? That is yours to manage.

You have a few paths forward.

Option 1: Transfer OA Savings Back to RA

If you want to keep earning the 4% rate, you can transfer those OA savings back into your Retirement Account. The limit is the Enhanced Retirement Sum, which in 2025 is $426,000. Over 99% of members can do this transfer. Once moved, those funds are locked in and will boost your monthly CPF LIFE payouts from age 65.

This option suits people who do not need the cash now and prefer the guaranteed 4% over any market-based investment. You get higher payouts, no volatility, and peace of mind.

Option 2: Singapore Savings Bonds

If you want safety but also liquidity, Singapore Savings Bonds are a solid choice. The latest SSB for November 2025 offers an average return of 1.83% over 10 years, starting at 1.39% in the first year. Yes, that is lower than CPF’s 4%, but you can redeem anytime with no penalty.

SSBs are government-backed, so there is zero credit risk. They suit retirees who want to keep their options open or who might need the cash for emergencies or opportunities down the road.

Option 3: Fixed Deposits

Fixed deposits are another low-risk option. As of October 2025, the best 12-month FD rates hover around 1.10% to 1.60%. Banks like DBS, OCBC, CIMB, and RHB offer competitive rates for deposits starting from $1,000 to $20,000.

FDs give you predictable returns and capital protection up to $100,000 per bank under the deposit insurance scheme. But rates are low compared to CPF, and your money is locked for the tenure. Still, if you want zero surprises and a known outcome, FDs work.

Option 4: Supplementary Retirement Scheme (SRS)

The SRS is a voluntary scheme where contributions get tax relief. Each dollar you put in reduces your taxable income by a dollar. Investment returns inside SRS grow tax-free, and only 50% of withdrawals are taxable at retirement.

For higher earners still working past 55, SRS top-ups can cut your tax bill while building a second retirement pot. You can invest SRS funds in stocks, bonds, unit trusts, or ETFs. But remember, SRS is locked until your retirement age, and early withdrawals trigger penalties.

Safe Investment Alternatives Comparison (October 2025)

The table above sums up the safest paths. Each has trade-offs. CPF gives the best rate but no access. SSBs give flexibility but lower returns. FDs give security but modest yields. SRS gives tax breaks but requires discipline and a longer time horizon.

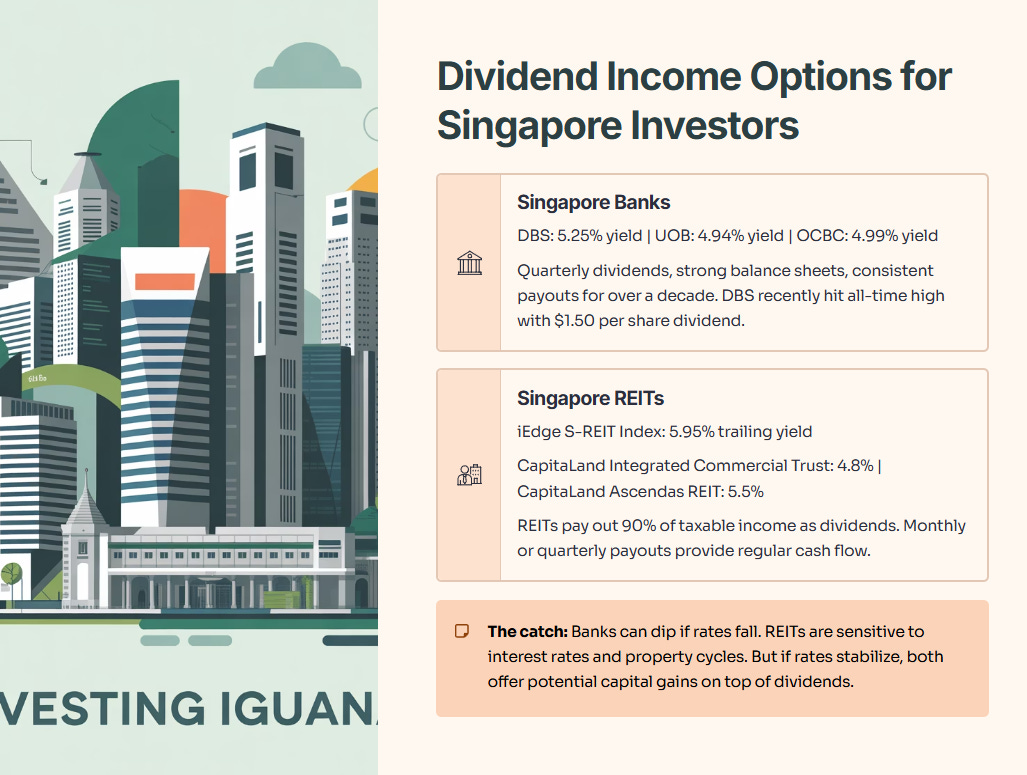

Chasing Income: Dividend Stocks and REITs

If you can handle a bit more risk and want regular payouts, dividend stocks and REITs are worth a look. Singapore’s market is full of income-generating assets, and many trade at attractive valuations heading into 2025.

Singapore Banks

DBS, UOB, and OCBC are the big three. DBS offers a dividend yield around 5.25%, UOB around 4.94%, and OCBC around 4.99%. These banks pay quarterly dividends, have strong balance sheets, and have delivered consistent payouts for over a decade.

DBS recently hit a new all-time high and declared a total dividend of $1.50 per share for the first half of 2025, translating to an annualized yield of about 5.5%. That is higher than the CPF OA rate and comes with potential capital gains if the stock price appreciates.

But banks are not risk-free. Earnings can dip if interest rates fall or if loan growth slows. Still, for income-seekers who want to balance safety and yield, the big three banks are a good starting point.

Singapore REITs

REITs are designed to pay out at least 90% of taxable income as dividends, making them natural income generators. The iEdge S-REIT Index has a trailing 12-month dividend yield of 5.95% as of mid-2025. Some REITs offer even higher yields, above 6%.

Popular picks include CapitaLand Integrated Commercial Trust (CICT) with a 4.8% yield, and CapitaLand Ascendas REIT with a 5.5% yield. REITs like Parkway Life REIT and data center REITs offer monthly or quarterly payouts, giving you regular cash flow.

The catch? REITs are sensitive to interest rates and property market cycles. Occupancy rates, rental reversions, and debt levels all matter. But if rates stabilize or fall, REITs could see price appreciation on top of dividends. That makes them a solid choice for income-seekers willing to ride out some volatility.

Building a Balanced Portfolio: ETFs and Unit Trusts

Not everyone wants to pick individual stocks. If you prefer a hands-off approach, ETFs and unit trusts give you instant diversification.

Straits Times Index ETFs

The two main STI ETFs are the SPDR Straits Times Index ETF (ES3) and the Nikko AM Singapore STI ETF (G3B). Both track the STI, which hit record highs in 2025. Combined, they have over $2.8 billion in assets.

These ETFs give you exposure to Singapore’s 30 largest blue chips in one trade. The SPDR STI ETF charges 0.28% per year, making it one of the cheapest ways to own the local market. You can buy it with cash or through your CPF Ordinary Account under CPFIS.

Unit Trusts

If you want broader diversification or exposure to Asia or global markets, unit trusts are an option. Funds like the Eastspring Investments Asian Balanced Fund invest in a mix of Asian equities and US bonds, targeting medium to long-term total returns. The LionGlobal Singapore Balanced Fund mixes local equities with fixed income and has delivered solid year-to-date performance.

Unit trusts charge higher fees than ETFs, often 1.25% to 1.5% per year. But they offer active management and can access markets that ETFs do not cover well. You can buy them with CPF OA funds under CPFIS, making them a popular choice for CPF investors.

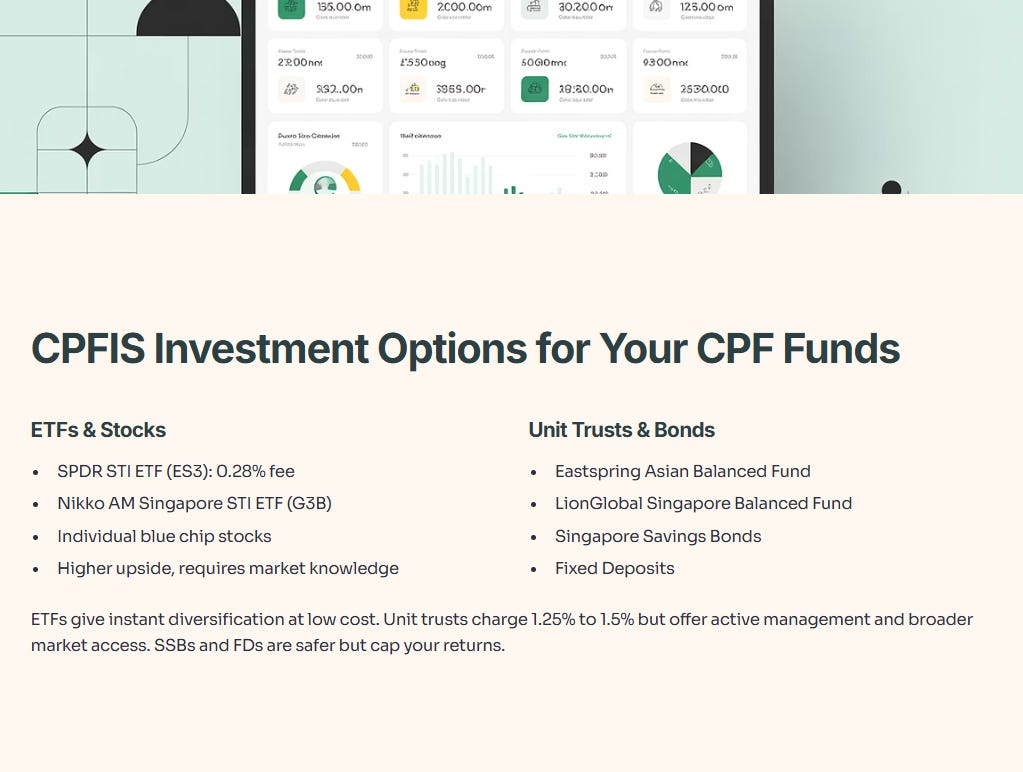

CPFIS Investment Options for Your CPF Funds

The table above shows what you can invest using your CPF funds. ETFs and stocks require more market knowledge, but they offer higher upside. SSBs and FDs are safer but cap your returns.

Three Investor Profiles: Which One Are You?

Everyone’s retirement journey is different. Some people just want to sleep well at night. Others want higher payouts and are okay with a bit of risk. Here are three profiles to help you figure out your next move.