CPF vs Cash: The Hidden Opportunity Cost That’s Costing You Thousands

Unlock an extra 1–2% a year on your cash by choosing the right mix of CPF, REITs, and T-bills—here’s the simple, data-driven playbook by age, risk, and time horizon to stop leaving money on the table.

CPF vs Cash: The Hidden Opportunity Cost That’s Costing You Thousands

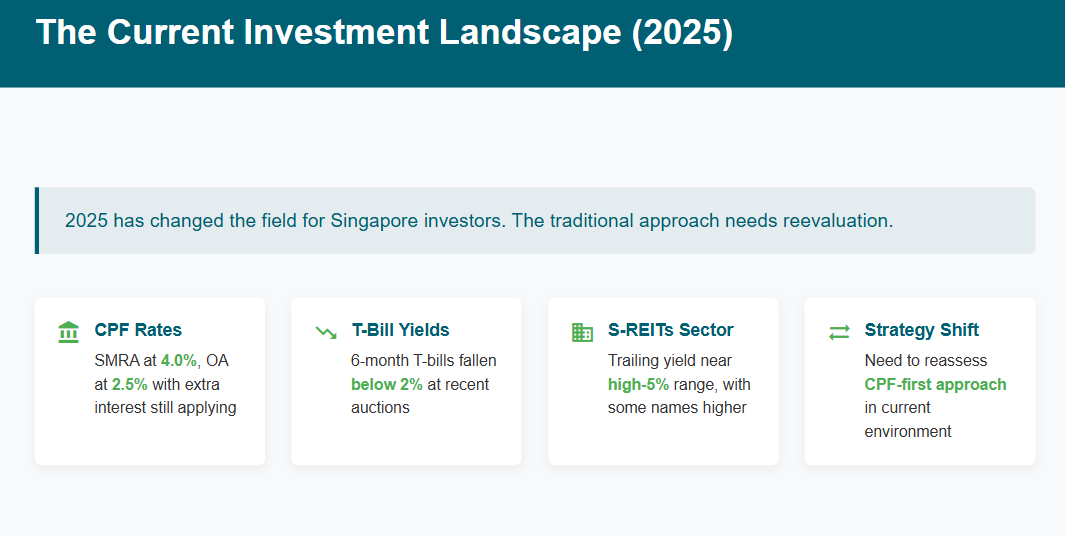

Most investors still follow a simple rule: top up CPF first, then think about markets. That worked when T-bills were juicy and the Special Account felt endless. But 2025 changed the field. The Special, MediSave, and Retirement Accounts pay 4.0% in Q3 2025, while the Ordinary Account pays 2.5%. Extra interest rules still apply. Six-month T-bill yields have fallen below 2% at recent auctions.

The broad S-REITs sector offers a trailing yield near the high-5% range, with some names higher. In this deep dive, I’ll show who should prioritize CPF top-ups, who should tilt toward REITs, and when T-bills still make sense. We’ll cover yields, real returns, taxes, risk, and time horizon so you leave with a simple plan you can act on.

Comparison of investment yields available to Singaporean investors, showing CPF accounts versus market alternatives with risk level coding

The Core Insight

The math is sobering. If you're under 55, your effective CPF return with bonus interest is about 3.5% on the first $60,000. But if you're over 55 and your Special Account is closed, you're stuck with 2.5% on your Ordinary Account balance.

This creates a massive opportunity cost. A 35-year-old professional earning the enhanced CPF rate of 3.5% is missing out on 2.4% annually by not investing in REITs averaging 5.9%. Over 20 years, that's the difference between $100,000 growing to $197,000 in CPF versus $314,000 in REITs.

For those over 55, the opportunity cost is even steeper. With SA closure forcing money into the 2.5% OA, the gap widens to 3.4% annually compared to REIT investments.