CSE Global: 3 Good and 3 Red Flags

Can CSE Global’s steady dividends and data centre bets outshine currency risks for Singapore investors?

Should Singapore investors buy, hold, or sell CSE Global now? This perennial question returns to the spotlight as the SGX-listed systems integrator posts steady growth and maintains its dividend, but faces margin and currency headwinds. With big moves in the data centre space, local CPF and SRS investors must weigh both promise and risk.

Investors are often left puzzled by CSE: It looks solid on paper, yet remains volatile, and sometimes feels like a “value trap.” Confusion makes sense—revenue is rising, order books look full, but cost inflation and volatile exchange rates muddy the earnings picture. This piece breaks down three positives, three red flags, and ends with Iggy’s latest verdict, tailored for Singapore (and Malaysia) readers.

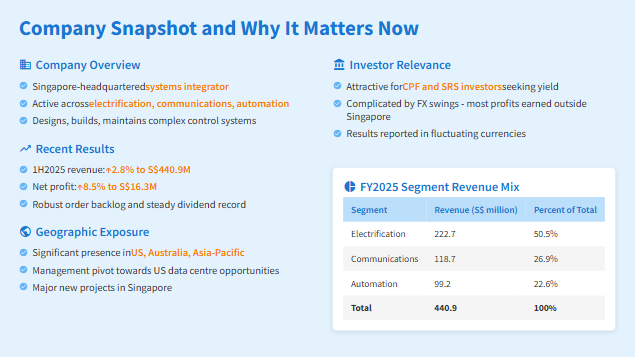

Company Snapshot and Why It Matters Now

CSE Global (SGX: 544) is a Singapore-headquartered systems integrator, active across electrification, communications, and automation. Its core business is designing, building, and maintaining complex control and communications systems for industries from energy to infrastructure. The firm has significant exposure in the US, Australia, and across Asia-Pacific. Management pivots towards US data centre opportunities and major new projects in Singapore position CSE for growth.

Recent results surprised on the upside: For 1H2025, revenue rose 2.8% to S$440.9 million and net profit jumped 8.5% to S$16.3 million. With a robust order backlog and a steady dividend record, CSE stands out for local investors who prize cash flow and resilience. CPF and SRS suitability, however, is complicated by FX swings—most of its profits are earned outside Singapore and reported in fluctuating currencies.

Table: FY2025 Segment Revenue Mix

SegmentRevenue (S$ million)Percent of TotalElectrification222.750.5%Communications118.726.9%Automation99.222.6%Total440.9100%

This table breaks down CSE’s 1H2025 revenue mix by segment. Electrification remains the largest contributor, but communications is growing fast due to US data centre project wins, underlining strategic exposure to global infrastructure themes.

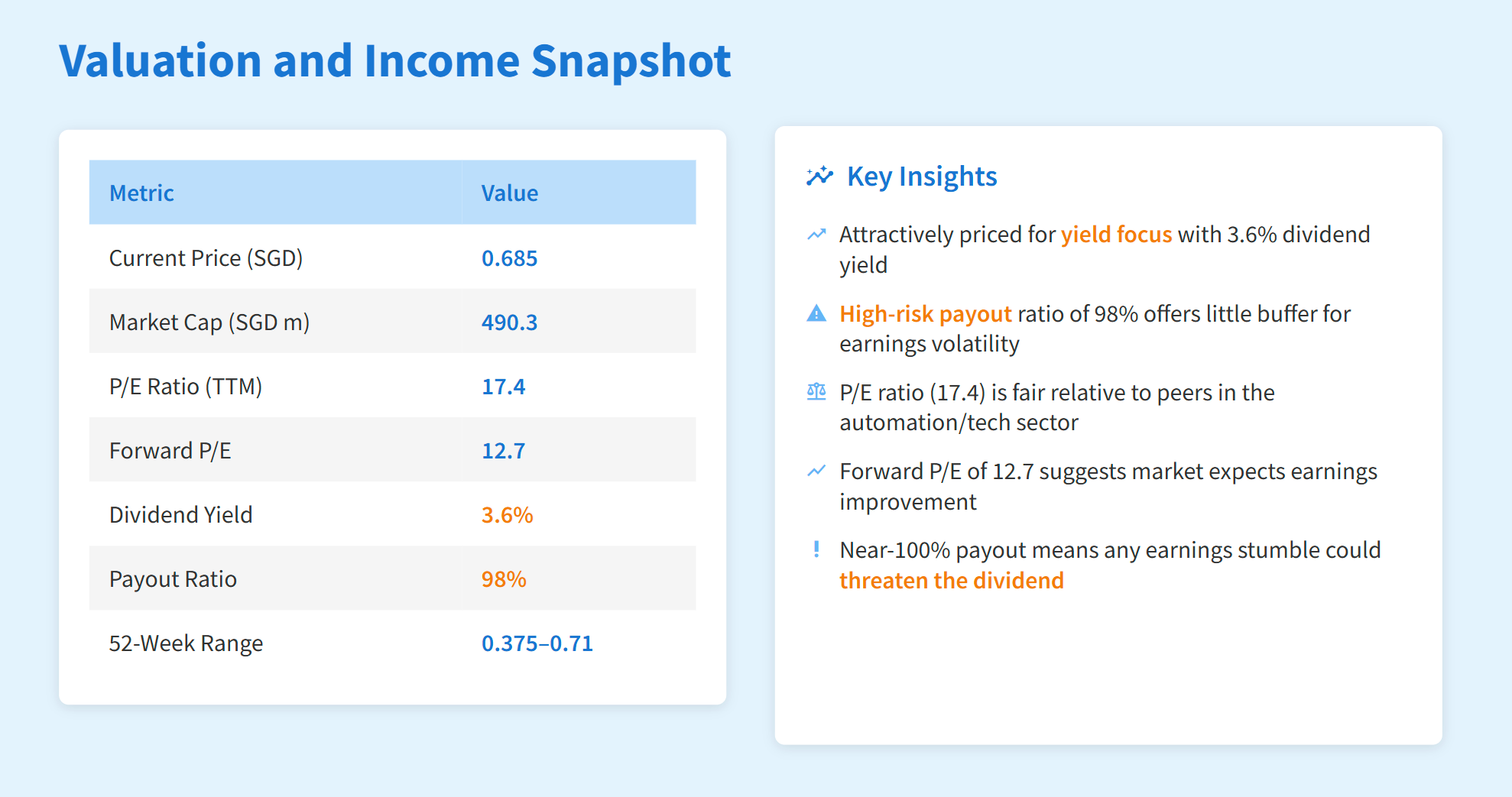

This snapshot shows CSE Global is attractively priced for yield, with a generous but high-risk payout. While its P/E is fair relative to peers, the near-100% payout means any earnings stumble could threaten the dividend.

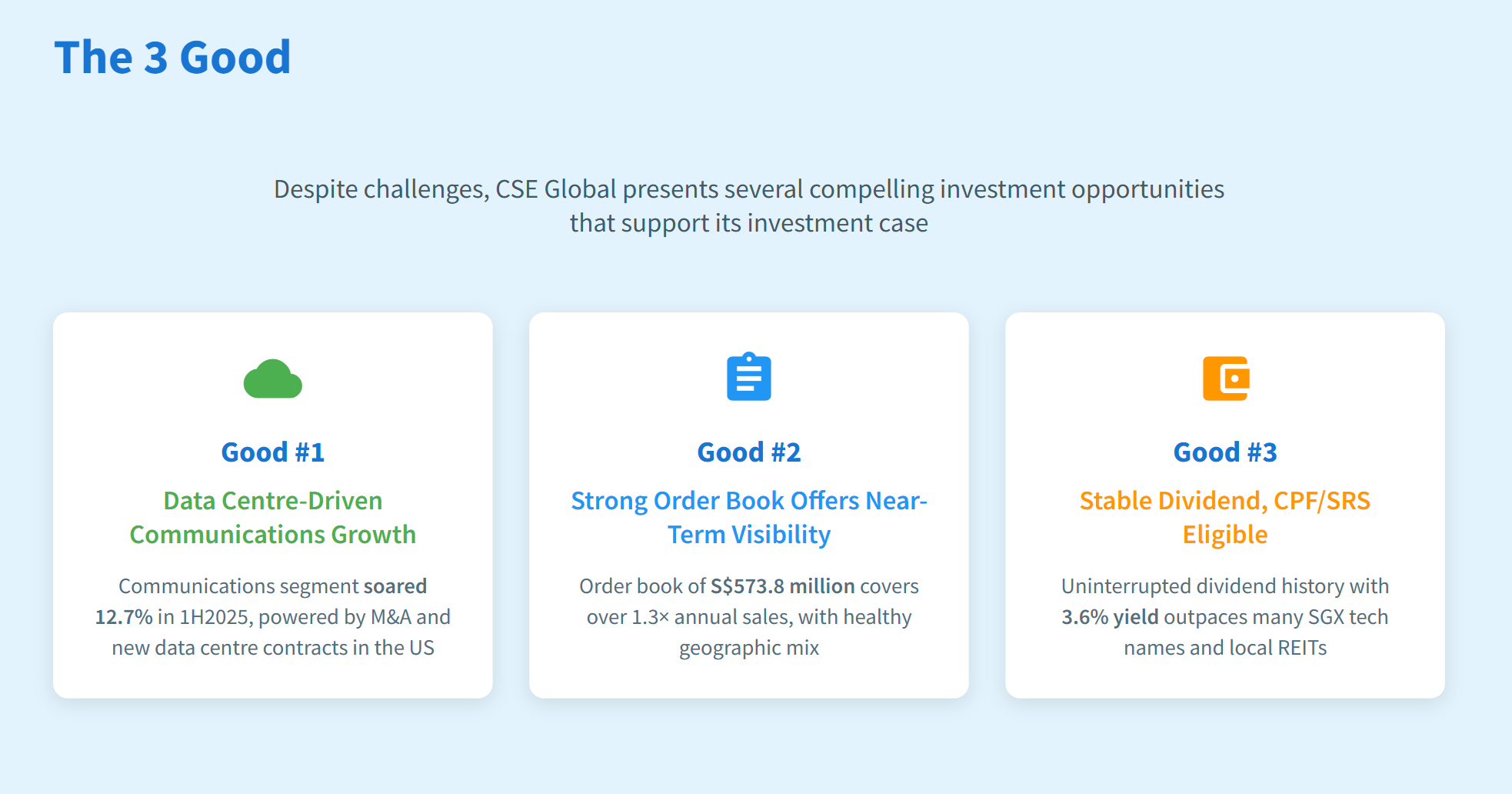

The 3 Good

Good #1: Data Centre-Driven Communications Growth

CSE’s communications segment soared 12.7% in 1H2025 to S$118.7 million, powered by M&A and new data centre contracts in the US. The strategic acquisition of Chicago Communications boosts its US presence—opening up four states and direct access to the booming data centre sector. Local investors should note Singapore’s own data centre sector is growing rapidly, with capex expected to scale as new government policies support digital investments.

Quick tip: Watch for fresh contract wins in US and Asia data centres each quarter; rising exposure can support earnings even if Singapore slows.