🦎 Daily Pulse: SGX Digest, 9 April 2026

The STI brushes the 5,000 ceiling as T-bill yields melt, forcing a forensic rotation into equity risk premiums.

The index hit 4,996.05 today. The real forensic tension is not the rally. It is the collapse of the T-bill sanctuary to 1.46% (26 March auction; 9 April result pending), which mathematically reboots the yield spread for every income seeker in Singapore.

In This Article:

Market Snapshot

Seatrium

AMTD Idea Group

SIA Engineering

Link REIT

Analyst Chatter

Watchlist and Yield Spread

Iggy’s Take: The Bottom Line

About Iggy & the Elite Investors

The Window Closes Fast. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. By the time this analysis reaches you as a free subscriber, the entry window Iggy identified has already opened — and often closed.

Iggy’s Elite Investors don’t just get the report earlier. They get it when the numbers still matter — zero-day forensic breakdowns, the full “Red Zone” watchlist, and institutional-grade cheatsheets at the moment the setup is live, not after the market has already priced it in.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

📊 Market Snapshot

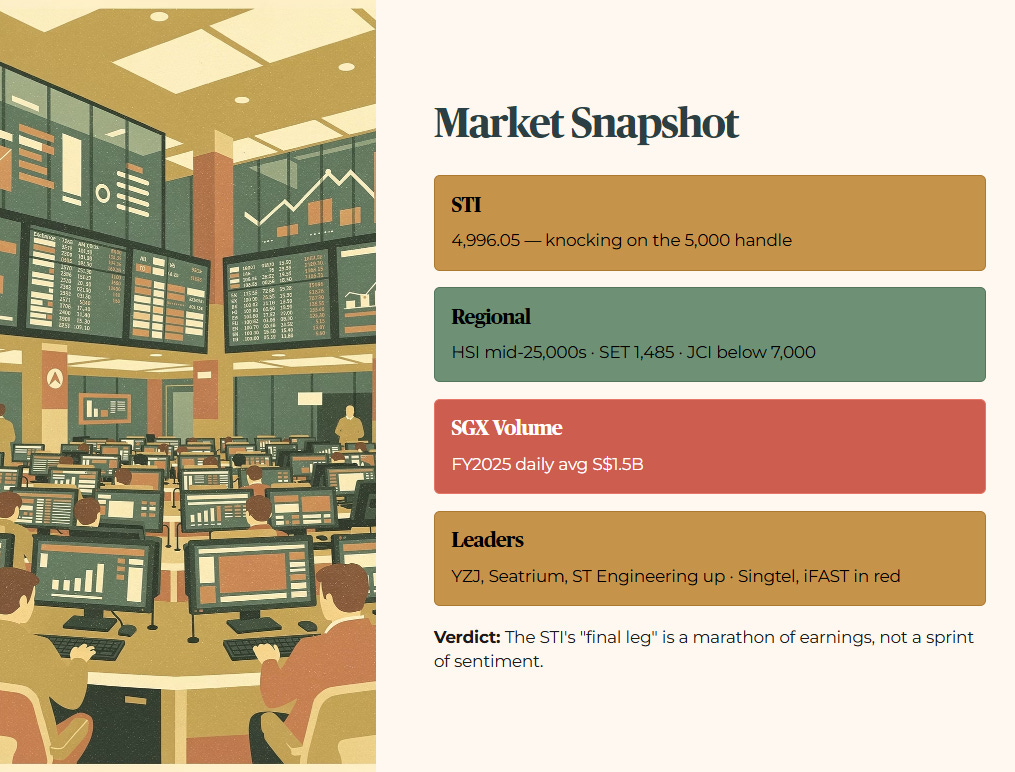

Verdict Beat: The STI is flirting with history, but the “final leg” is a marathon of earnings, not a sprint of sentiment.

STI closed at 4,996.05 on 8 April, currently knocking on the 5,000 handle. Regional context: HSI trading in the mid-25,000s range; SET closed at 1,485.03 on 8 April; JCI has broken below 7,000. SGX FY2025 daily average value stands at S$1.5 billion; intraday comparison is not available at time of publication. Dominant sector: marine and engineering, with YZJ, Seatrium, and ST Engineering leading. Singtel and iFAST in the red.

🔍 The Audit

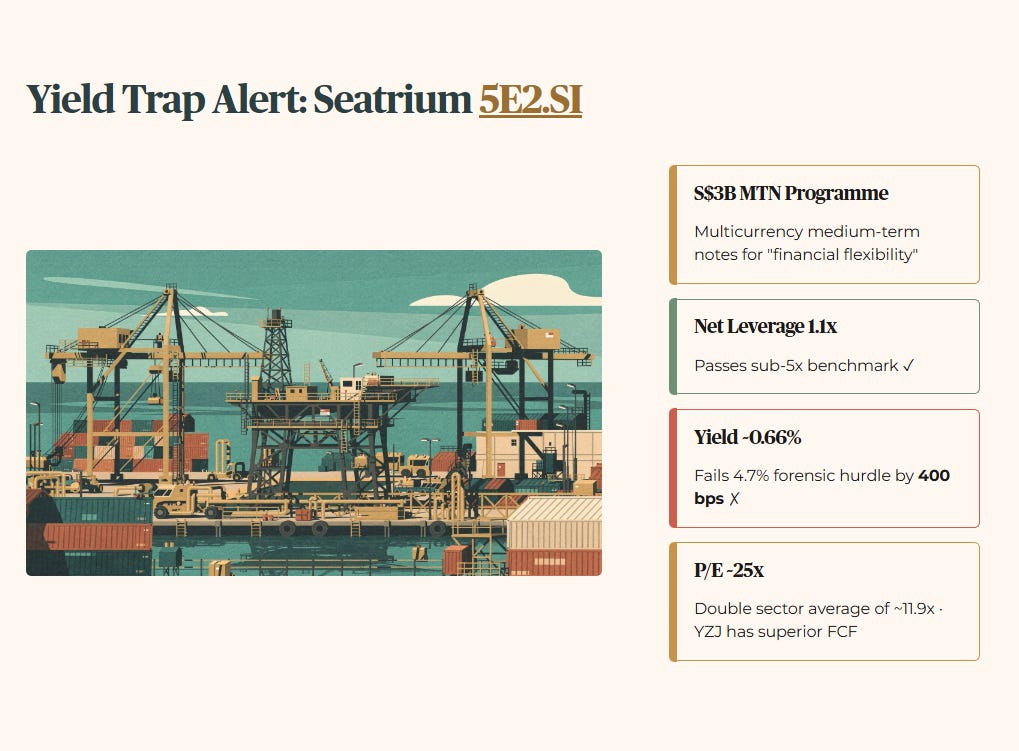

Yield Trap Alert: Seatrium (5E2.SI)

Verdict Beat: The balance sheet is cleaner, but the S$3 billion debt programme is the “MRT Door Paradox” — the door is open for growth, but leaning too hard on it stalls the dividend recovery.

Layer 1 — Raw Fact: Seatrium has established a S$3.0 billion multicurrency medium-term note programme to increase financial flexibility.

Layer 2 — Benchmark: Net leverage at 1.1x passes the sub-5x benchmark. Forward yield of approximately 0.66% fails the 4.7% forensic hurdle by a full 400 basis points.

Layer 3 — Peer Context: Peer Yangzijiang Shipbuilding maintains superior free cash flow. Seatrium trades at approximately 25x P/E, double the sector average of approximately 11.9x.

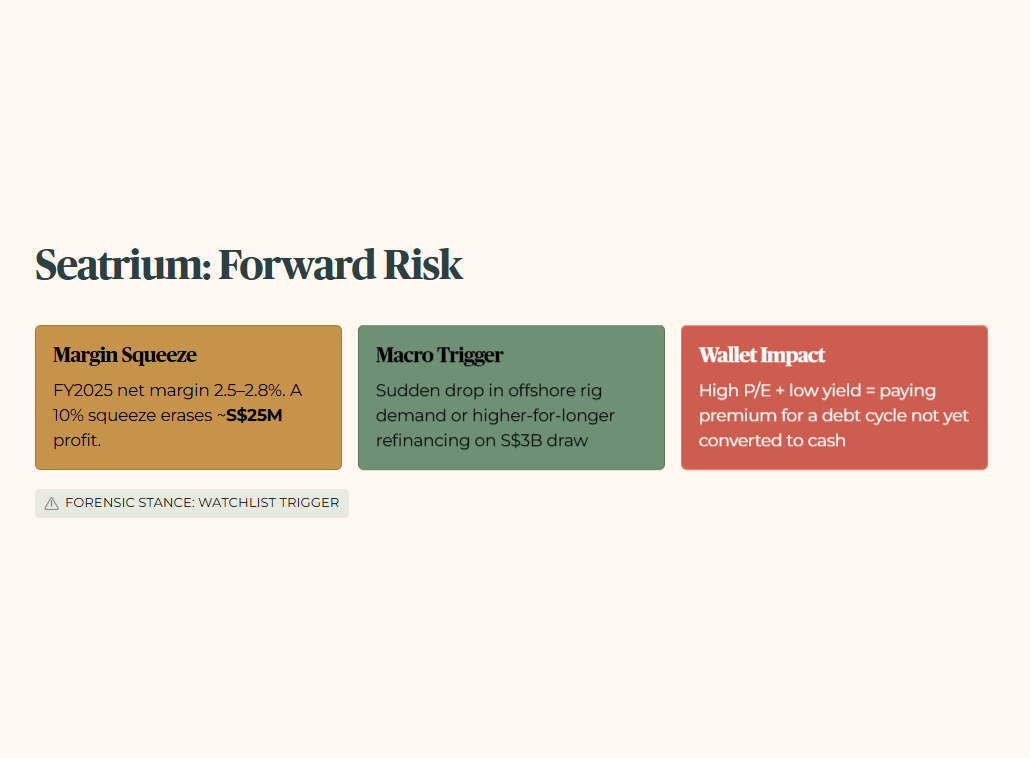

Layer 4 — Forward Scenario: At a confirmed FY2025 net margin of 2.5 to 2.8%, a 10% margin squeeze would erase roughly S$25 million in profit. The named macro trigger: a sudden downturn in global offshore rig demand or higher-for-longer refinancing costs on the S$3 billion draw.

Layer 5 — Wallet Impact: For a 45-year-old HDB owner in Bedok supplementing salary, this is a Watchlist Trigger. The high P/E and low yield mean you are paying a premium for a debt cycle that has not converted to cash yet. Forensic Stance: Watchlist Trigger.

🦎 Iggy’s Insight: The Debt Cycle Tax

Seatrium’s S$3 billion note programme is not inherently dangerous — it is the price of operating at scale in offshore marine. The forensic problem is the sequencing. You are being asked to pay 25x earnings today for a yield of 0.66%, on the promise that the debt cycle will eventually convert into distributions. That is not investing. That is speculating on a management execution timeline you cannot audit.

Yangzijiang has already done the hard work of converting its order book into free cash flow. Until Seatrium shows the same conversion, the S$3 billion is a liability before it is an asset. The door is open — but the cash has not walked through it yet.