Daily Pulse: SGX Digest — March 30, 2026

The Oil Shock Stress Test: Is Your Dividend Fuel-Injected?

If you are standing outside the SGX Centre on Shenton Way this morning, watching the live ticker scroll across the building’s facade, the numbers are telling a story that the weekend headlines did not prepare you for. Brent crude has surged past US$115 a barrel on Middle East tensions, and the STI is down 20 points in early trade toward the 4,870 level. For a retail investor holding local blue chips, this is not just a global news headline. It is a direct tax on the corporate margins that fund your dividends. When oil spikes, the Fortress Balance Sheet is not just a buzzword — it is the only thing standing between your retirement payouts and a margin call.

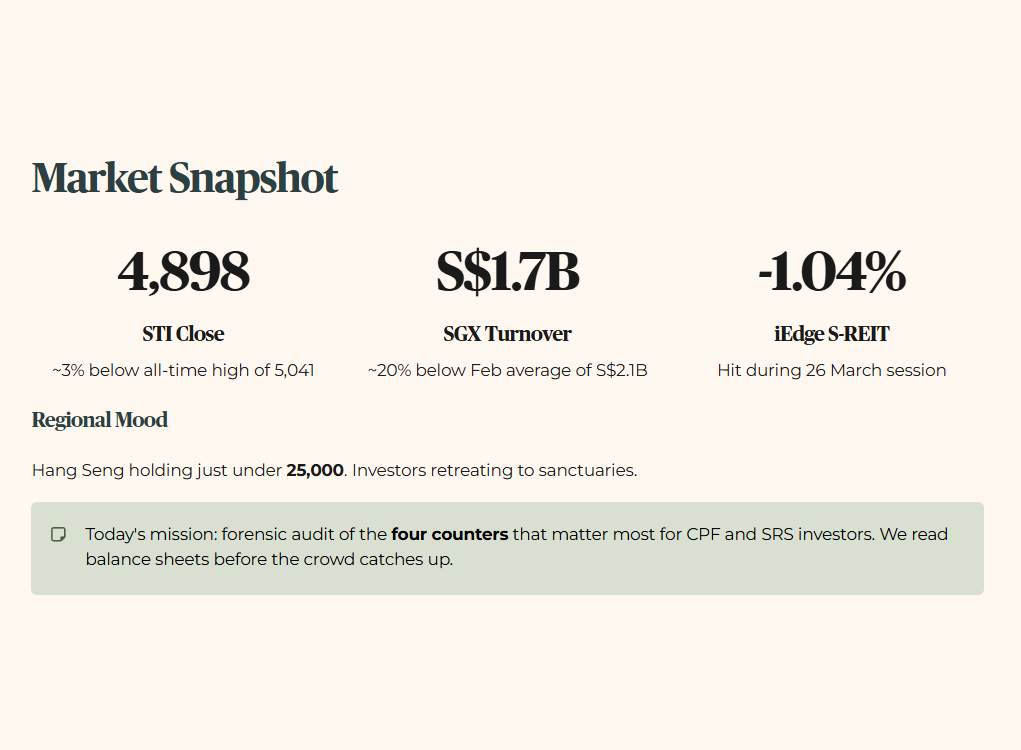

The STI last closed around 4,898, roughly 3% below its recent all-time high of 5,041. In Kopitiam Logic, this is like the price of condensed milk going up overnight — it does not just affect your kopi; it changes the math for every stall in the centre. Regionally, the mood is mixed. The Hang Seng is holding just under 25,000, while SGX securities turnover has slowed to S$1.7 billion, approximately 20% below the February average of S$2.1 billion. Investors are retreating to Sanctuaries as the iEdge S-REIT index took a 1.04% hit during the March 26 session.

Today’s forensic mission is to cut through the oil shock noise and audit the four counters that matter most for the Singapore retail investor managing CPF and SRS capital. We are not chasing momentum. We are reading the balance sheets before the crowd catches up.

In This Article:

The Audit Forensic Triage

Manulife US REIT BTOU Yield Trap Alert

CapitaLand Ascendas REIT A17U Core Monitoring

Sembcorp Industries U96 Transition Watchlist

Jardine Cycle and Carriage C07 Satellite Monitoring

Iggys Insight The Figueroa Funeral

Analyst Chatter The Suit Filter

Watchlist and Yield Spread

Iggys Take The Bottom Line

Iggys Forensic Compliance Standards Standard Disclaimer

About Iggy & the Elite Investors

The Window Closes Fast. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. By the time this analysis reaches you as a free subscriber, the entry window Iggy identified has already opened — and often closed.

Iggy’s Elite Investors don’t just get the report earlier. They get it when the numbers still matter — zero-day forensic breakdowns, the full “Red Zone” watchlist, and institutional-grade cheatsheets at the moment the setup is live, not after the market has already priced it in.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

The Audit: Forensic Triage

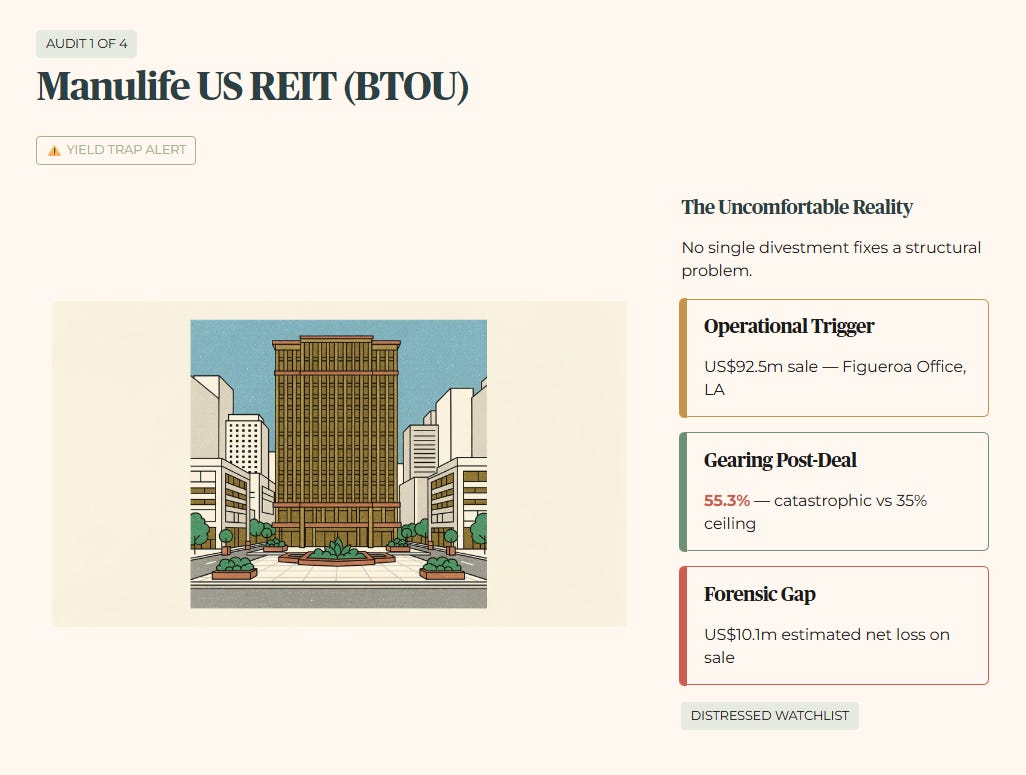

1. Manulife US REIT (BTOU) — Yield Trap Alert

The uncomfortable reality of BTOU is that no single divestment fixes a structural problem. Selling the Figueroa building in Los Angeles for US$92.5 million sounds decisive until you look at what remains after the transaction costs, the net loss, and the gearing level that the sale is supposed to rescue.

The Five-Layer Audit:

Layer 1 — Raw Fact: MUST is divesting its 35-storey Figueroa building — currently only 45.6% occupied — to the City of Los Angeles for US$92.5 million. Net proceeds are estimated at US$82.4 million after transaction costs and credits.

Layer 2 — Historical Benchmark: Post-sale gearing of 55.3% remains a catastrophic breach of Iggy’s 35% gearing ceiling. This is nearly 20 percentage points above the Fortress standard. NAV per unit has already eroded from US$0.23 to US$0.19 as of end-2025. The trust is not recovering — it is contracting.

Layer 3 — Peer Context: While industrial peers like CLAR are deploying the equity lever to acquire data centres and logistics assets, MUST is selling assets just to meet a Minimum Sale Target under its Master Restructuring Agreement (MRA) to avoid default. These are two entirely different capital allocation strategies. One is building; the other is surviving.

Layer 4 — Forward Scenario: Stress-testing a further 10% drop in US office valuations would likely wipe out the remaining equity cushion. The US office market has not found its floor. Remote work structurally changed the demand profile for Class B and Class C office space, and a 45.6% occupancy rate on a tower you are selling to a city government is not a sign that the worst is behind you. It is a sign that the private market would not take it.

Layer 5 — Wallet Impact: For a CPF or SRS holder, your capital is currently being used to fund bank covenant relief. There is zero Organic NPI flowing to your pocket, and distributions remain halted until specific MRA hurdles are cleared. Every dollar you have in BTOU is a dollar working for the lenders, not for your retirement. This is the definition of a Yield Trap that has already snapped shut.

Forensic Verdict Beat: This is survival by amputation — the patient is losing blood faster than the bandage can be applied.

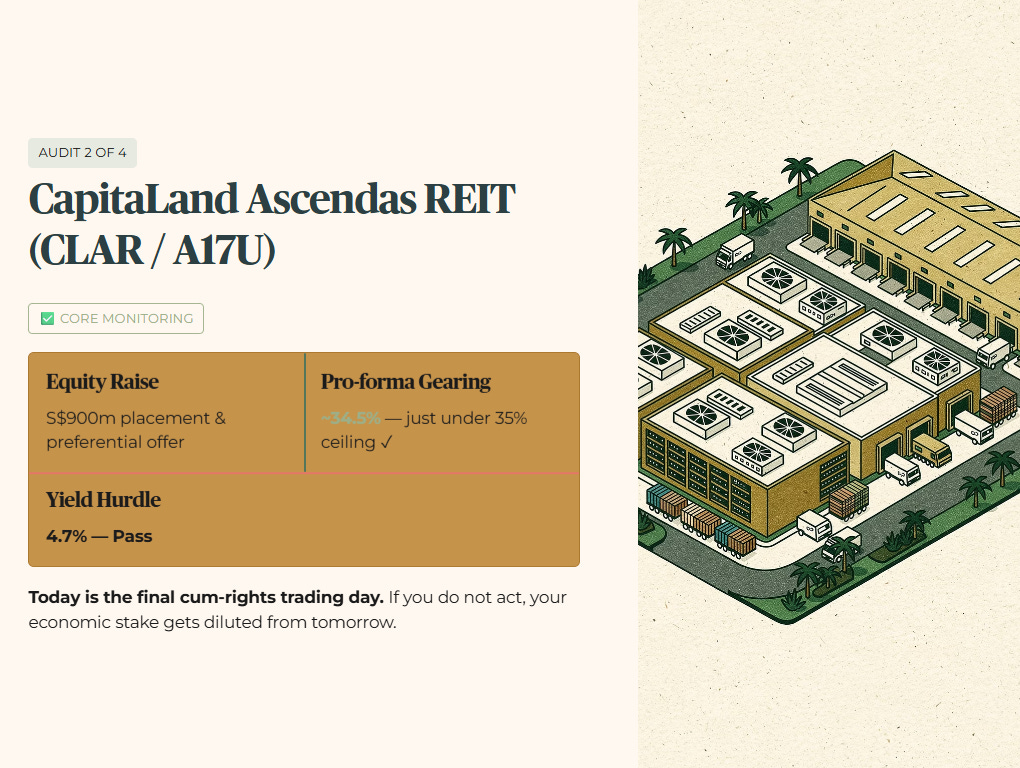

2. CapitaLand Ascendas REIT (A17U) — Core Monitoring

CLAR is doing what a well-run industrial REIT should do in a cycle like this: deploying capital into structural growth assets while managing the balance sheet tightly enough to stay inside the gearing ceiling. Today is the final cum-rights trading day, and the mechanics of this equity raise matter for every unitholder.

The Five-Layer Audit:

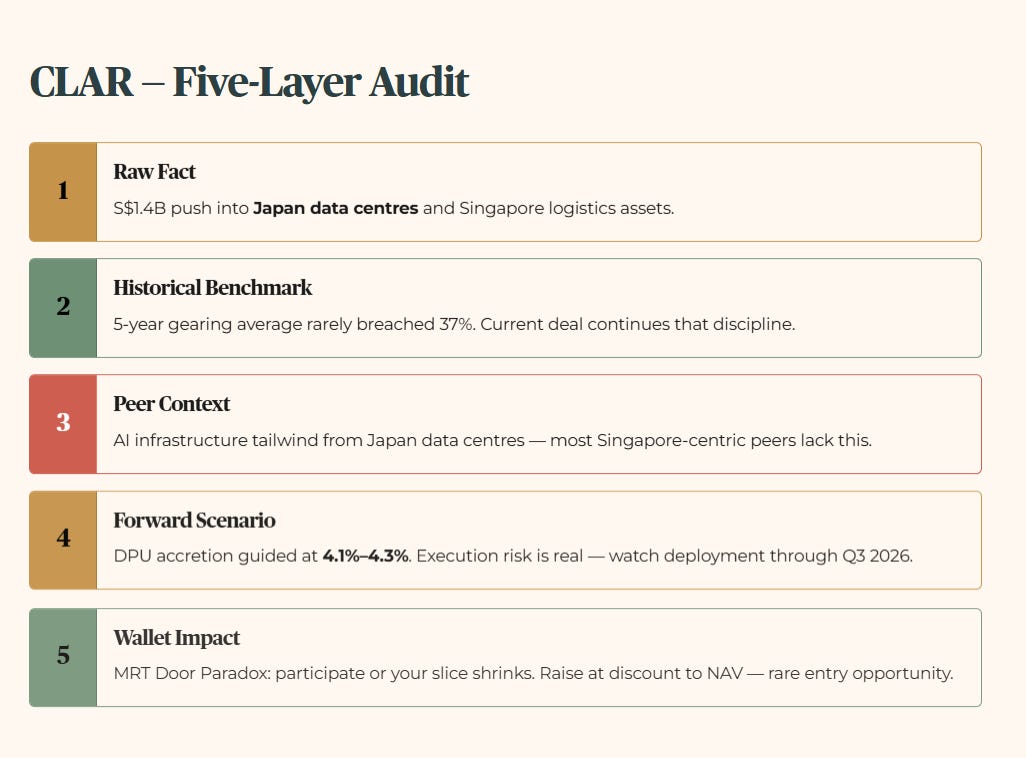

Layer 1 — Raw Fact: CLAR is raising S$900 million via placement and preferential offer to fund a S$1.4 billion push into Japan data centres and Singapore logistics assets. Today is the final cum-rights trading day, which means if you are a current unitholder and you do not act, your economic stake gets diluted from tomorrow.

Layer 2 — Historical Benchmark: This transaction pulls pro-forma gearing down to approximately 34.5%, successfully landing just under our 35% ceiling. CLAR has consistently managed its balance sheet with discipline — the 5-year gearing average has rarely breached 37%, even during the aggressive post-COVID acquisition phase. The current deal continues that pattern rather than breaking it.

Layer 3 — Peer Context: CLAR is effectively becoming an industrial growth platform rather than a defensive bond proxy. It is trading near-term yield for long-term scale — a strategic luxury that MUST can no longer afford and that pure-play logistics REITs with declining DPU trajectories cannot execute without triggering gearing alarms. The Japan data centre exposure in particular gives CLAR a structural tailwind from AI infrastructure spending that most Singapore-centric industrial landlords simply do not have.

Layer 4 — Forward Scenario: A 10% shift in global cap rates would put pressure on the DPU accretion targets, which are currently guided at 4.1% to 4.3%. If the Japan deployments are delayed by permitting or construction friction, the growth premium embedded in the current unit price becomes expensive dilution rather than accretive expansion. The risk is execution, not balance sheet. For a REIT this size, with a Temasek-linked sponsor and institutional backing, execution risk is manageable — but it is not zero. Watch the deployment timeline through Q3 2026.

Layer 5 — Wallet Impact: For an SRS investor, this is the MRT Door Paradox in reverse. You must participate in the preferential offer or your slice of the pie gets smaller. You are paying a subscription fee just to maintain your current yield level. That is the structural cost of holding a growth-oriented REIT through an equity raising cycle. For investors who cannot or do not wish to participate, the dilution is real and must be factored into the yield calculation going forward. For those who can participate, the S$900 million raise at a discount to NAV represents a rare opportunity to add to a core position at a price that the open market has not offered in recent months.

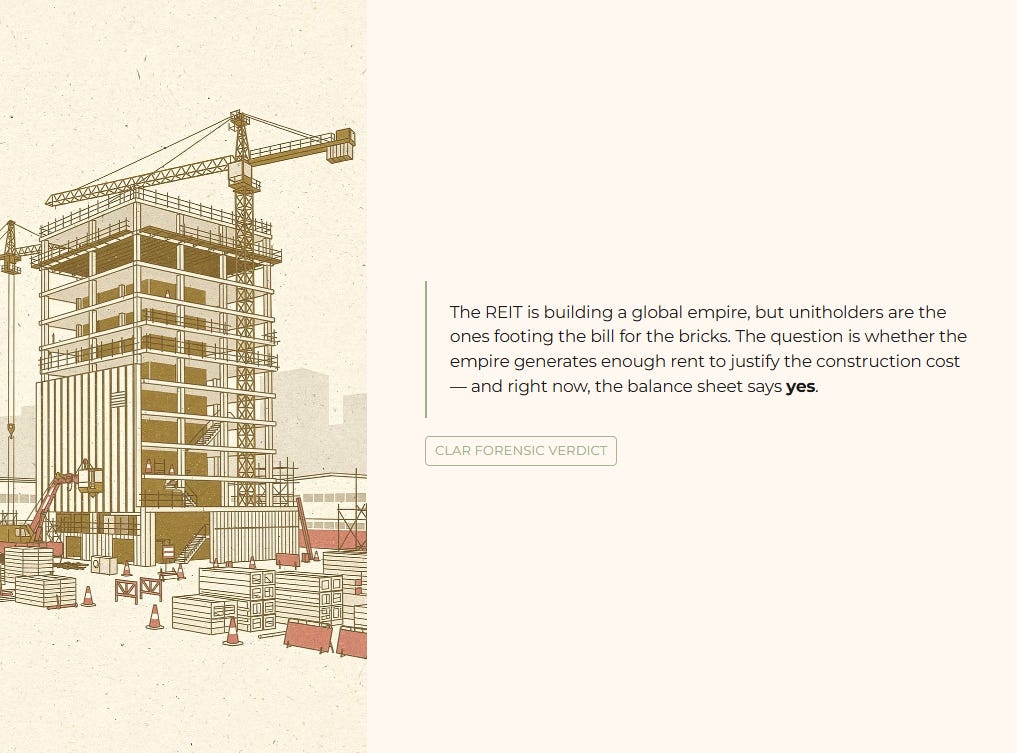

Forensic Verdict Beat: The REIT is building a global empire, but unitholders are the ones footing the bill for the bricks. The question is whether the empire generates enough rent to justify the construction cost — and right now, the balance sheet says yes.

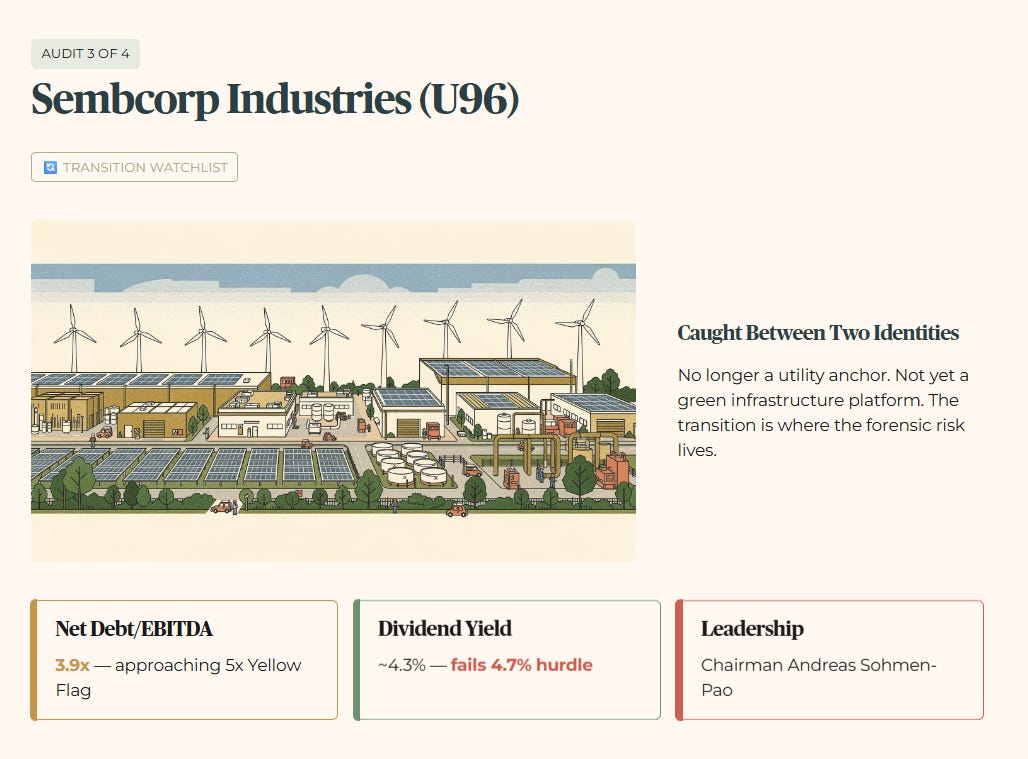

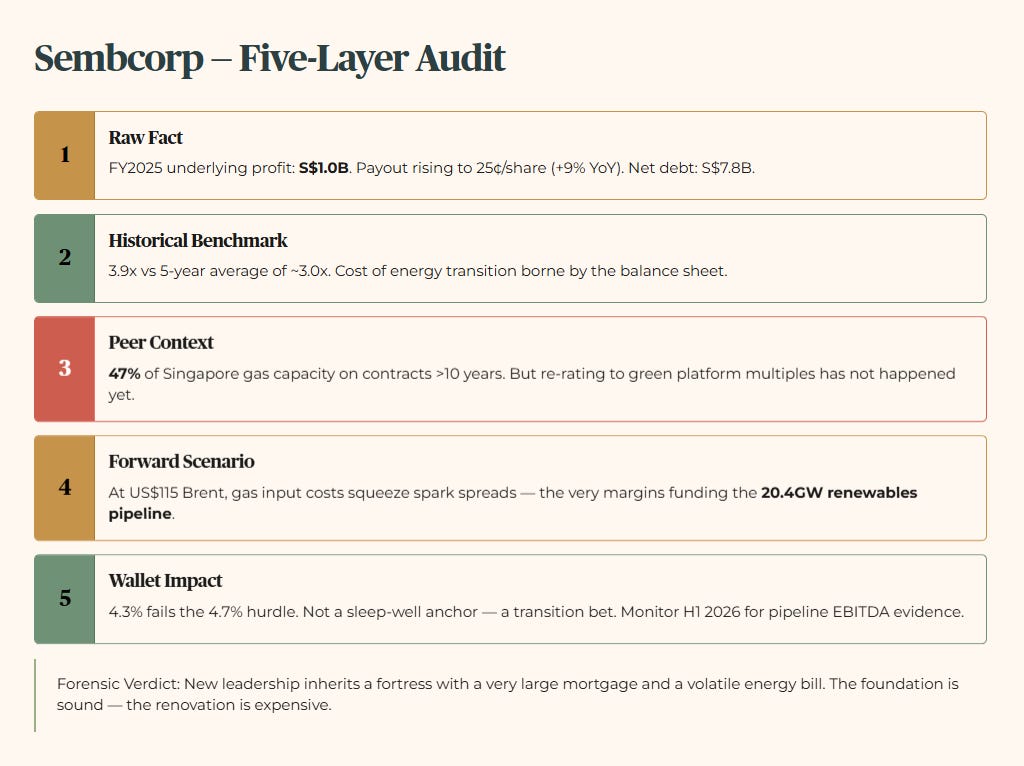

3. Sembcorp Industries (U96) — Transition Watchlist

Sembcorp is one of the most structurally interesting companies on the SGX right now because it is caught between two identities. It is no longer the utility anchor it was five years ago, and it has not yet fully become the green infrastructure platform it is trying to become. That transition is exactly where the forensic risk lives.

The Five-Layer Audit:

Layer 1 — Raw Fact: Sembcorp delivered S$1.0 billion in underlying profit for FY2025, and the payout is rising to 25 Singapore cents per share, up 9% year on year. Net debt remains elevated at S$7.8 billion.

Layer 2 — Historical Benchmark: Net Debt/EBITDA at 3.9x is approaching the 5x Yellow Flag zone. The company is not in distress — 3.9x is manageable — but the trajectory matters. If the 20.4GW renewables pipeline requires continued capital deployment without proportional EBITDA growth, this ratio moves in the wrong direction. The 5-year average was closer to 3.0x. The current premium to that average reflects the cost of the energy transition, and that cost is being borne by the balance sheet.

Layer 3 — Peer Context: Unlike traditional utilities, Sembcorp’s profile is shifting toward a capital-intensive green independent power producer model. 47% of its Singapore gas-fired generation capacity is now on contracts longer than 10 years, providing a meaningful revenue buffer. But the comparison set is no longer SP Group or Keppel Infrastructure — it is increasingly global green energy platforms that trade on project pipeline multiples rather than utility yield multiples. That re-rating has not fully happened yet, and until it does, the stock sits in an awkward middle ground.

Layer 4 — Forward Scenario: If Brent crude stays at US$115, input costs for gas could squeeze the spark spreads needed to fund the massive renewables pipeline. The irony of Sembcorp’s transition thesis is that it is partially funded by gas generation profits — and a sustained oil shock that drives up gas input costs without a proportional increase in power tariffs compresses exactly the margin that is funding the green pivot. A 10% sustained increase in gas input costs would put meaningful pressure on near-term EBITDA and could slow the deployment timeline on the renewables pipeline.

Layer 5 — Wallet Impact: At 4.3%, U96 fails the 4.7% absolute minimum yield hurdle at current pricing. For a retiree in Marine Parade managing SRS funds, this is not a sleep-well utility anchor anymore. It is a transition bet where the yield does not yet justify the execution risk of a 20.4GW renewables pipeline. The 9% dividend increase is a positive signal from management, but a single year of payout growth does not offset a yield that sits below our minimum threshold and a debt load that is trending in the wrong direction. Monitor the H1 2026 results for evidence that the pipeline is generating EBITDA rather than consuming it.

Forensic Verdict Beat: New leadership is inheriting a fortress with a very large mortgage and a volatile energy bill. The foundation is sound — the renovation is expensive.

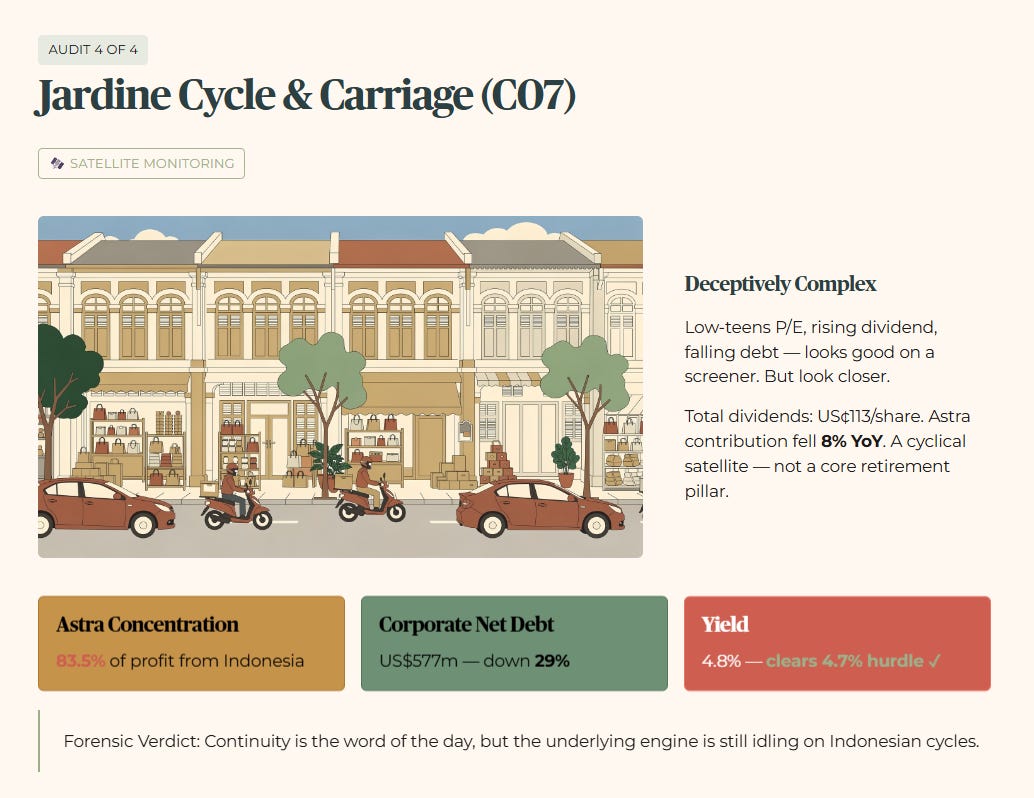

4. Jardine Cycle & Carriage (C07) — Satellite Monitoring

JC&C is the most deceptively complex counter on today’s watchlist. A low-teens P/E, a rising dividend, and a falling debt load all look good on a screener. But 83.5% of the underlying profit comes from a single Indonesian exposure, and that concentration is the forensic risk that the headline numbers consistently obscure.

The Triage: JC&C is cleaning house. Corporate net debt fell 29% to US$577 million, and total dividends hit US¢113 per share. However, Astra Indonesia still contributes US$927 million — roughly 83.5% of the total US$1.11 billion underlying profit. For the SRS investor, JC&C is a bet on the Indonesian consumer disguised as a Singapore blue chip. The 4.8% one-year yield is respectable and clears our 4.7% minimum hurdle, but Astra’s contribution fell 8% year on year. It is a cyclical satellite position — useful for diversification, not appropriate as a core retirement pillar.

Forensic Verdict Beat: Continuity is the word of the day, but the underlying engine is still idling on Indonesian cycles.

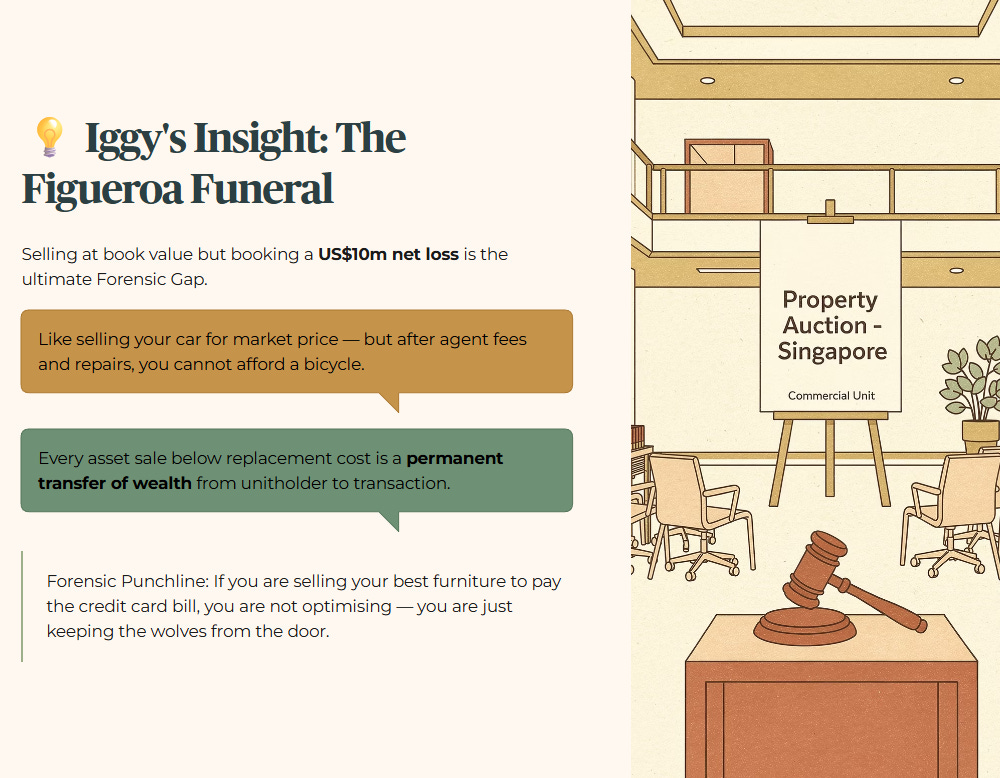

💡 Iggy’s Insight: The Figueroa Funeral

Selling an office tower at book value but booking a US$10 million net loss is the ultimate Forensic Gap. It is like selling your car for the market price but realising after the agent fees and repair costs, you cannot even afford a bicycle. MUST is deleveraging, yes — but at the cost of the very NAV unitholders are clinging to. Every asset sale below replacement cost is a permanent transfer of wealth from the unitholder to the transaction. When a REIT’s strategy is to sell its way to solvency, the finish line is not a Fortress Balance Sheet — it is an empty portfolio.

Forensic Punchline: If you are selling your best furniture to pay the credit card bill, you are not optimising — you are just keeping the wolves from the door.

Analyst Chatter (The Suit Filter)

Institutional desks are highlighting the STI dip as a potential entry window, citing a resilient 4.8% GDP forecast. However, the latest 6-month T-Bill yield confirmed at 1.46% on March 26. When we run this through the Iggy Forensic Floor of 3.2%, the minimum yield hurdle sits at 4.7%. Any watchlist trigger on a REIT or blue chip yielding less than that — without a verified, material growth kicker — is padding, not analysis.

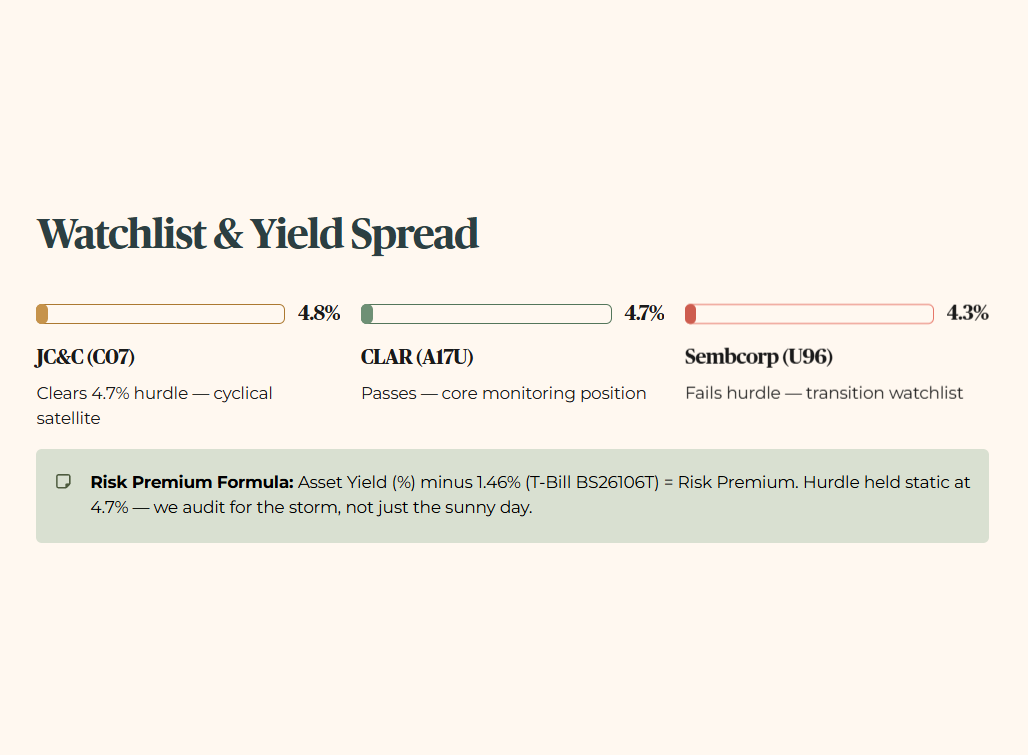

Watchlist & Yield Spread

The Calculation: Asset Yield (%) minus 1.46% (Latest T-Bill, BS26106T) = Risk Premium.

Note on the Stress-Test Buffer: I apply a conservative floor of 3.2% for all forensic comparisons. We audit for the storm, not just the sunny day. While the T-Bill has moved, my hurdle remains static at 4.7% (3.2% + 150 basis points) to ensure we do not chase yield down into the gutter during a temporary rate dip.

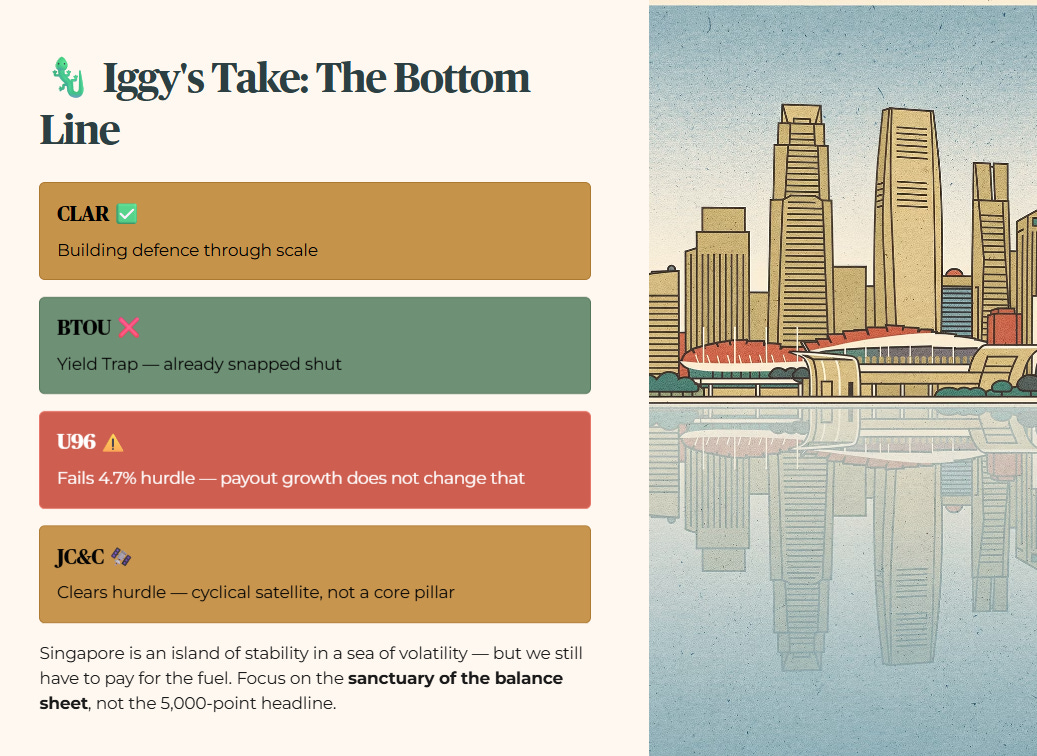

🦎 Iggy’s Take: The Bottom Line

Today’s STI drop is a reminder that Singapore is an island of stability in a sea of volatility — but we still have to pay for the fuel. For a retiree in Marine Parade managing SRS funds, the focus should not be on the 5,000-point headline. It should be on the sanctuary of the balance sheet.

CLAR is building defence through scale, while BTOU is a warning of what happens when a Yield Trap snaps shut. Sembcorp and JC&C are clearing their decks, but they carry operational weights that require active monitoring. U96 fails the 4.7% minimum yield hurdle at current pricing — a fact the payout growth headline does not change. JC&C clears the hurdle but remains a cyclical satellite, not a core pillar.

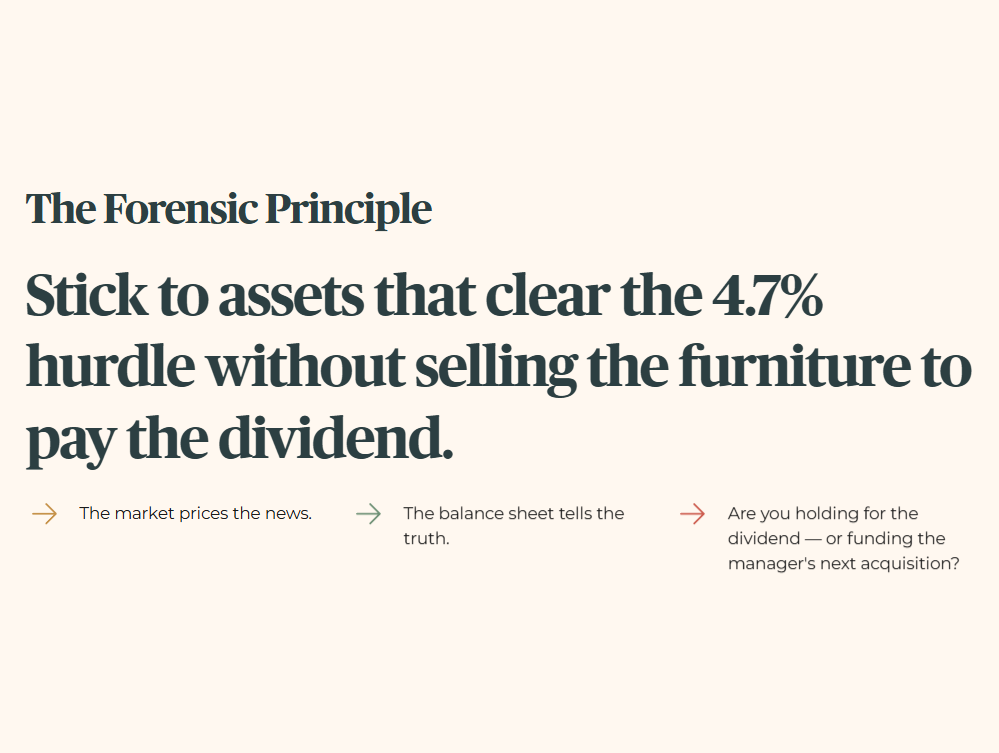

Stick to the assets that clear the 4.7% minimum yield hurdle without needing to sell the furniture to pay the dividend.

Are you holding for the dividend, or are you just funding the manager’s next acquisition? The market prices the news. The balance sheet tells the truth.

Iggy’s Forensic Compliance Standards — Standard Disclaimer

This content is produced for educational and informational purposes only. I am not a financial advisor — I am a retail investor who applies forensic analysis to my own portfolio and shares that process publicly. Nothing here constitutes a recommendation to buy, sell, or hold any security, and no specific target prices or personalised financial advice are offered. All data is sourced from public filings and verified sources; where data is unverified it is explicitly flagged. All investments carry risk, including the potential loss of principal, and past performance is not indicative of future results. If you are making investment decisions involving CPF, SRS, or personal capital, please conduct your own due diligence or consult a MAS-licensed financial adviser before committing funds.