DBS at $57.63 and 4.59% Yield | SGX Daily Pulse 07 Apr 2026

Forensic tracking shows DBS yields hitting 4.59%. Here is why the 2026 institutional data differs from retail sentiment.

Gearing ceilings are cracking under higher-for-longer rates while hidden associate losses drag down blue-chip darlings.

The STI might be holding above water, but look under the hood and you will find blue chips bleeding associate losses and REITs flirting with dangerous MAS aggregate leverage limits.

In This Article:

Market snapshot

Singapore Airlines associate losses and dividend risk

Keppel Infrastructure Trust yield versus gearing ceiling

Prime US REIT aggregate leverage and MAS limit stress test

Del Monte Pacific red zone insolvency risk

Analyst chatter the suit filter

Watchlist and yield spread framework

Iggys take the bottom line

Iggys forensic compliance standards standard disclaimer

About Iggy & the Elite Investors

The Window Closes Fast. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. By the time this analysis reaches you as a free subscriber, the entry window Iggy identified has already opened — and often closed.

Iggy’s Elite Investors don’t just get the report earlier. They get it when the numbers still matter — zero-day forensic breakdowns, the full “Red Zone” watchlist, and institutional-grade cheatsheets at the moment the setup is live, not after the market has already priced it in.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

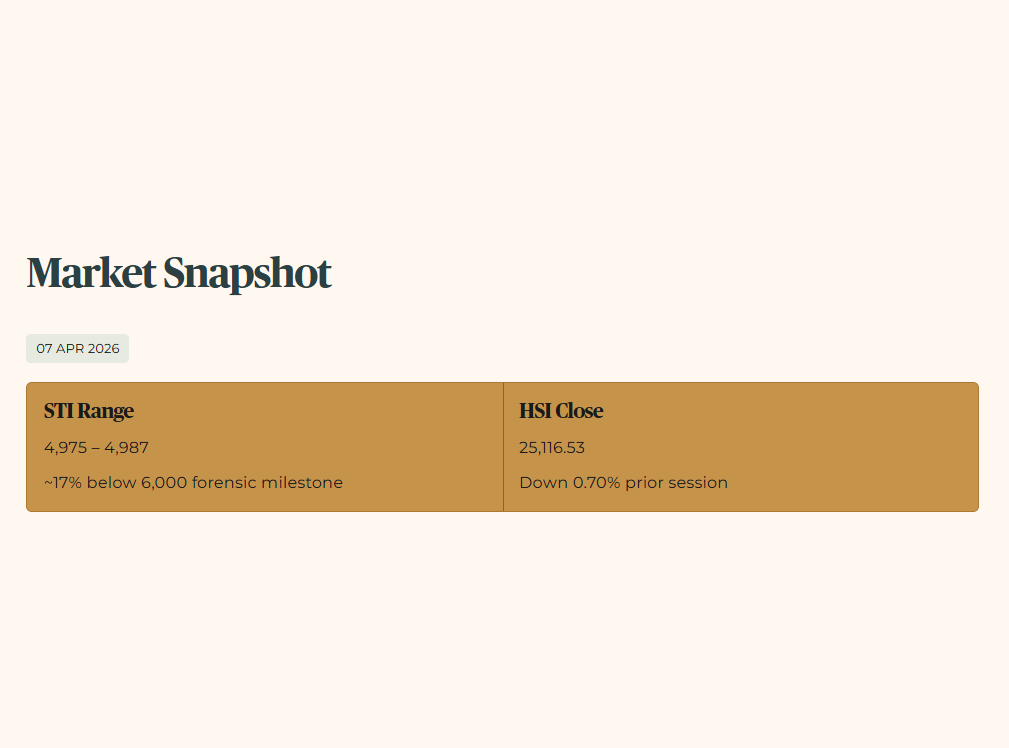

MARKET SNAPSHOT

The STI is trading in the 4,975–4,987 range in the morning session on April 7, sitting approximately 17% below the 6,000 forensic milestone. The HSI closed down 0.70% at 25,116.53 on the prior session.

THE AUDIT

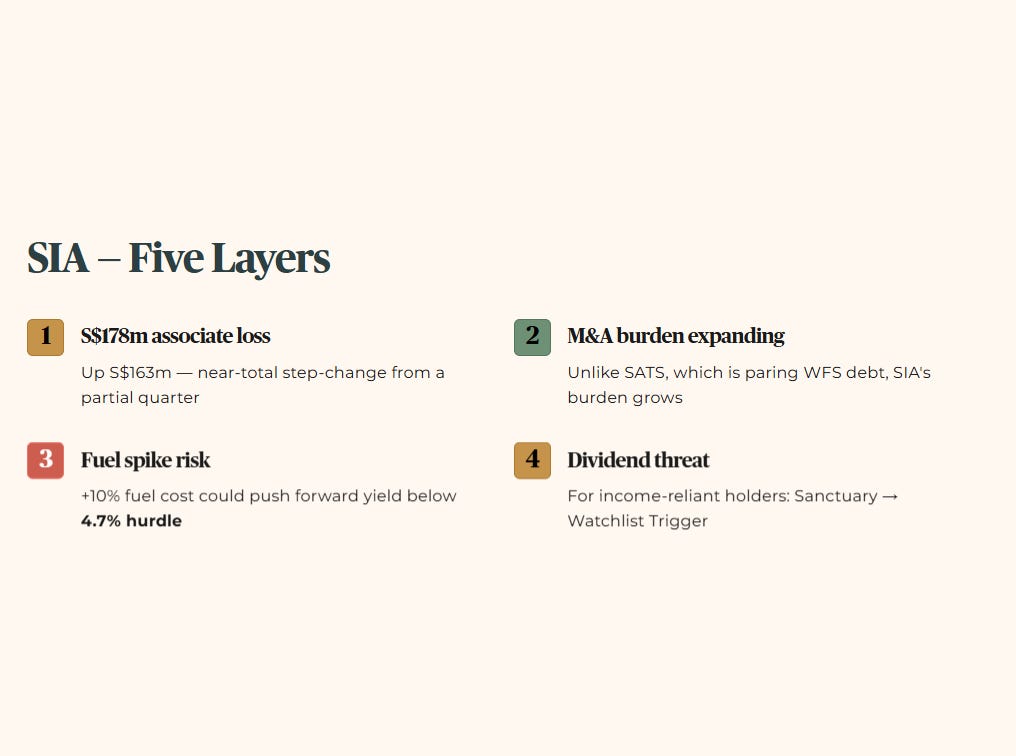

1. SINGAPORE AIRLINES (C6L)

This is a classic case where operational excellence masks a bleeding balance sheet at the associate level.

Layer 1: SIA’s share of associate losses from Air India increased by S$163 million, reaching S$178 million for Q3 FY2026.

Layer 2: This loss represents a near-total step-change from a partial quarter, aggressively breaching the historical average of its associate drag.

Layer 3: Unlike SATS, which is aggressively paring down its WFS acquisition debt and turning the corner, SIA is seeing its M&A burden expand.

Layer 4: If aviation fuel costs spike by 10% in the upcoming quarter, the combined pressure of core margin compression and this associate loss could push SIA’s forward dividend yield well below our 4.7% absolute minimum hurdle.

Layer 5: For a 55-year-old in Tampines relying on C6L dividends for passive income, this earnings hole translates to a direct percentage cut in your expected payout, shifting this stock from a perceived Sanctuary to a strict Watchlist Trigger.

Iggy’s Insight: The market loves to price Singapore Airlines purely on passenger load factors and post-pandemic travel momentum. But when you carry a 25.1% stake in an asset that wipes S$178 million from your bottom line in a single quarter, you are no longer just an airline — you are a holding company subsidising a turnaround project.

SATS learned this the hard way with WFS and took years to climb out. SIA is flying straight into that same M&A headwind just as core margins compress. You cannot pay dividends with load factors. You pay them with retained earnings — and right now, Air India is drinking your yield straight from the firehose.

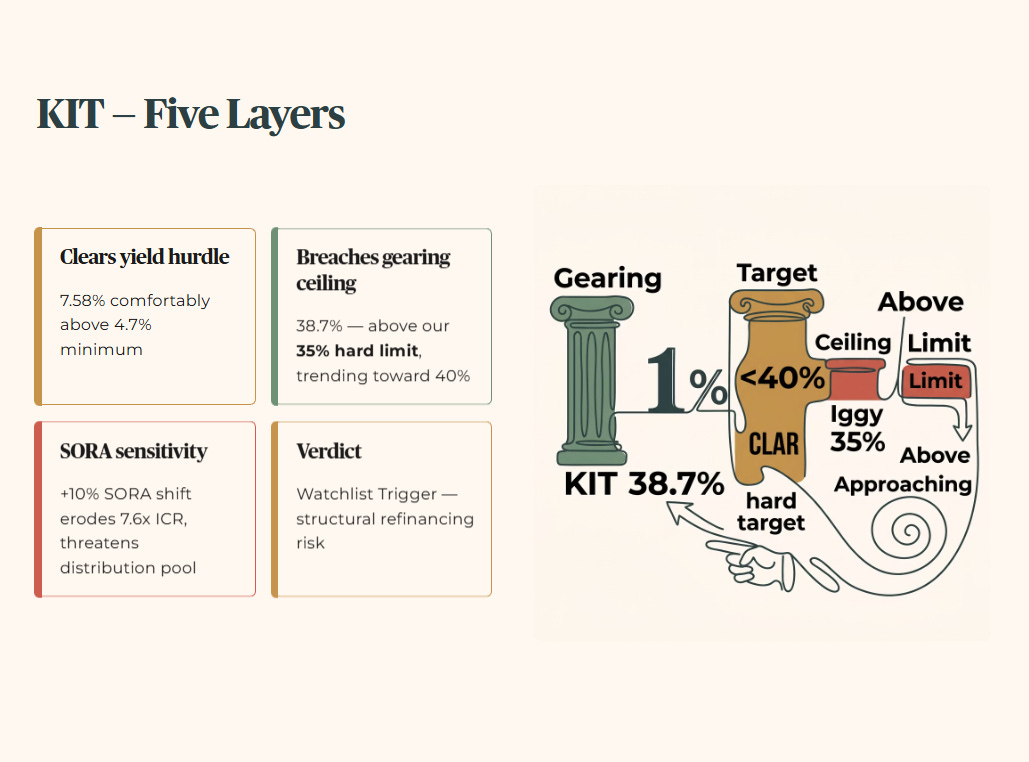

2. KEPPEL INFRASTRUCTURE TRUST (A7RU) — Gearing Alert

The headline yield looks fat, but the debt load driving it breaches our forensic ceiling.

Layer 1: Keppel Infrastructure Trust carries a confirmed FY2025 net gearing of 38.7% alongside a solid ICR of 7.6x, offering a 7.58% TTM yield backed by an approximate 4.51% weighted average debt cost.

Layer 2: While the distribution comfortably clears our 4.7% yield hurdle, the 38.7% leverage sits stubbornly above our 35% Gearing Ceiling.

Layer 3: Compare this to an industrial peer like CLAR, which aggressively defends its Fortress Balance Sheet with a hard target to keep gearing below 40%. KIT is already at 38.7% and trending toward that ceiling, not away from it.

Layer 4: A 10% upward shift in the SORA curve over the next refinancing window would erode that 7.6x ICR, instantly narrowing the spread and directly threatening the cash distribution pool.

Layer 5: For an income investor in Ang Mo Kio managing a high-yield portfolio, that yield comes with structural refinancing risk that could shave hundreds of dollars off your quarterly payout. This classifies as a Watchlist Trigger.

Iggy’s Insight: Everyone loves a 7.58% yield until they see the scaffolding holding it up. Keppel Infrastructure Trust is hovering at 38.7% net gearing — close enough to the 40% ceiling that there is no comfortable margin for error. When you are pushing that hard against the limit, you are not buying infrastructure stability; you are buying interest rate sensitivity. A 7.6x ICR looks comfortable today, but that buffer evaporates the moment debt rollover meets a higher-for-longer SORA environment. This is not a defensive infrastructure play. It is a leveraged bet on interest rates, dressed up in a distribution statement.

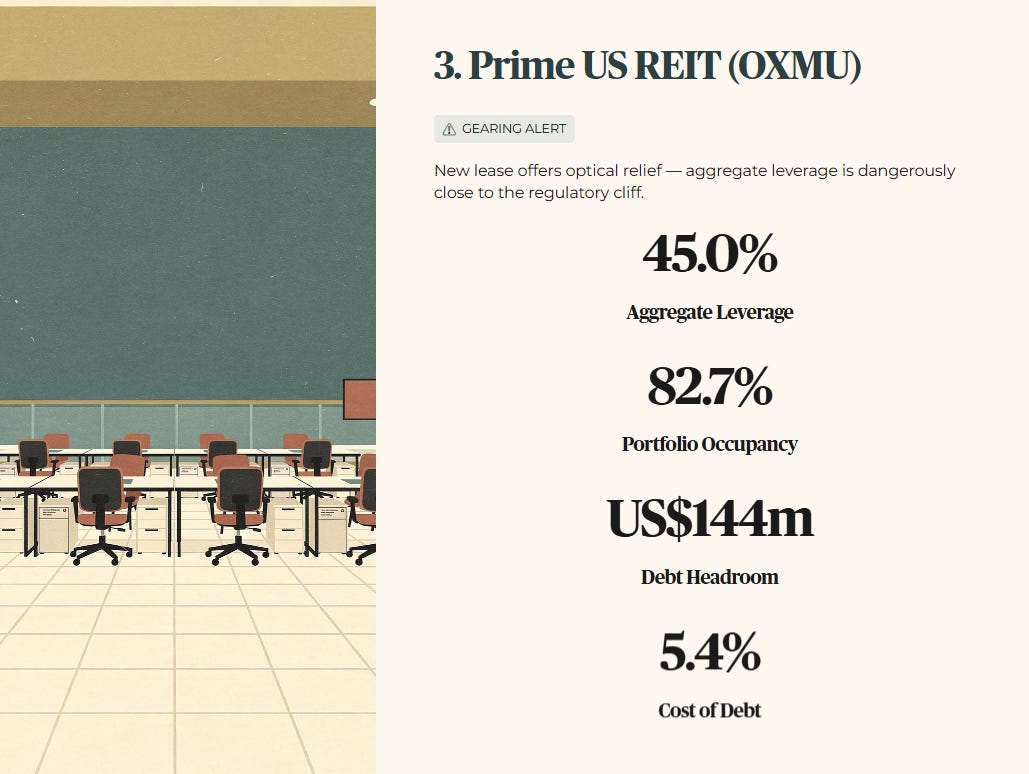

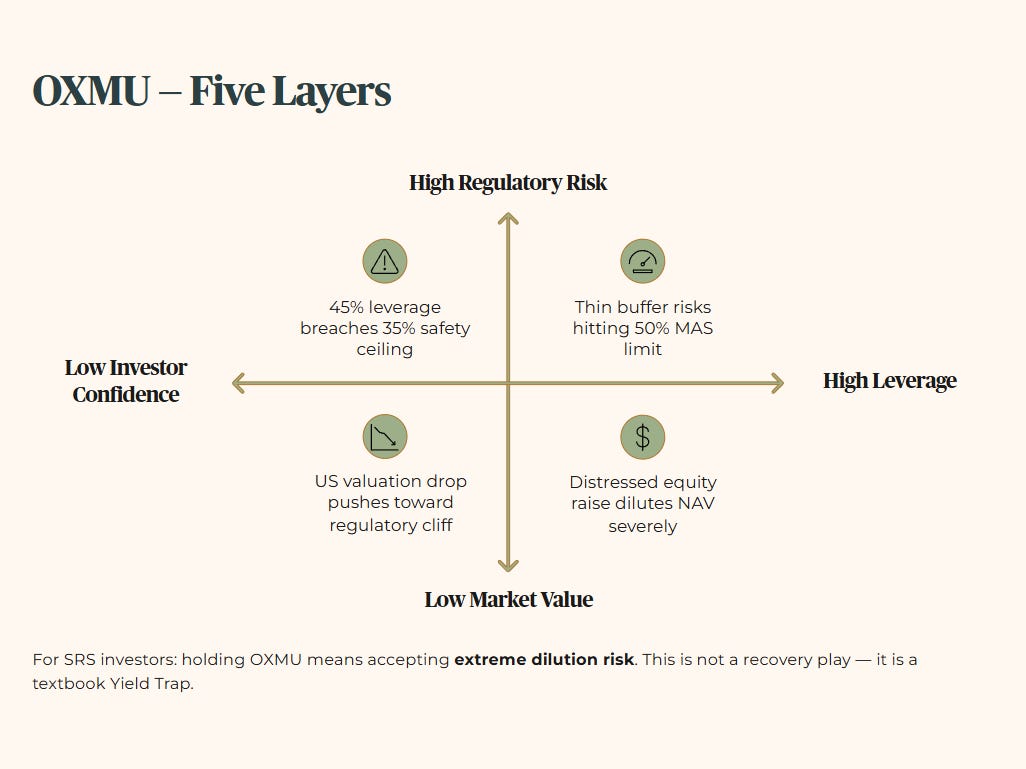

3. PRIME US REIT (OXMU) — Gearing Alert

A new lease offers optical relief, but the aggregate leverage is dangerously close to the regulatory cliff.

Layer 1: Despite securing a new 40,000 sq ft lease that lifted portfolio committed occupancy to 82.7%, the trust’s confirmed FY2025 aggregate leverage sits at 45.0%.

Layer 2: This leverage completely shatters our 35% ceiling and leaves very little buffer before hitting the 50% MAS regulatory limit.

Layer 3: While local heavyweights like MLT maintain ample debt headroom, OXMU is staring squarely at The Debt Wall with limited liquidity options.

Layer 4: If US commercial valuations drop by another 10% in the upcoming appraisal cycle, that leverage will be pushed toward the 50% MAS ceiling, forcing a distressed equity fund-raising that will instantly dilute NAV.

Layer 5: For an SRS investor in Jurong East, holding this means accepting extreme dilution risk to your capital base. This is not a recovery play — it is a textbook Yield Trap.

Iggy’s Insight: Getting excited about a new lease when aggregate leverage sits at 45.0% is like squeezing through the closing doors of a train that has already left the tracks. Prime US REIT is mathematically cornered. The 50% MAS limit is not a target — it is a cliff edge.

With US commercial valuations still facing appraisal pressure, they are one bad cycle away from a distressed equity raising. Retail investors holding on for a recovery are missing the forensic math entirely. When the capital structure is this fragile, every new lease is a temporary stay of execution, not a turnaround signal.

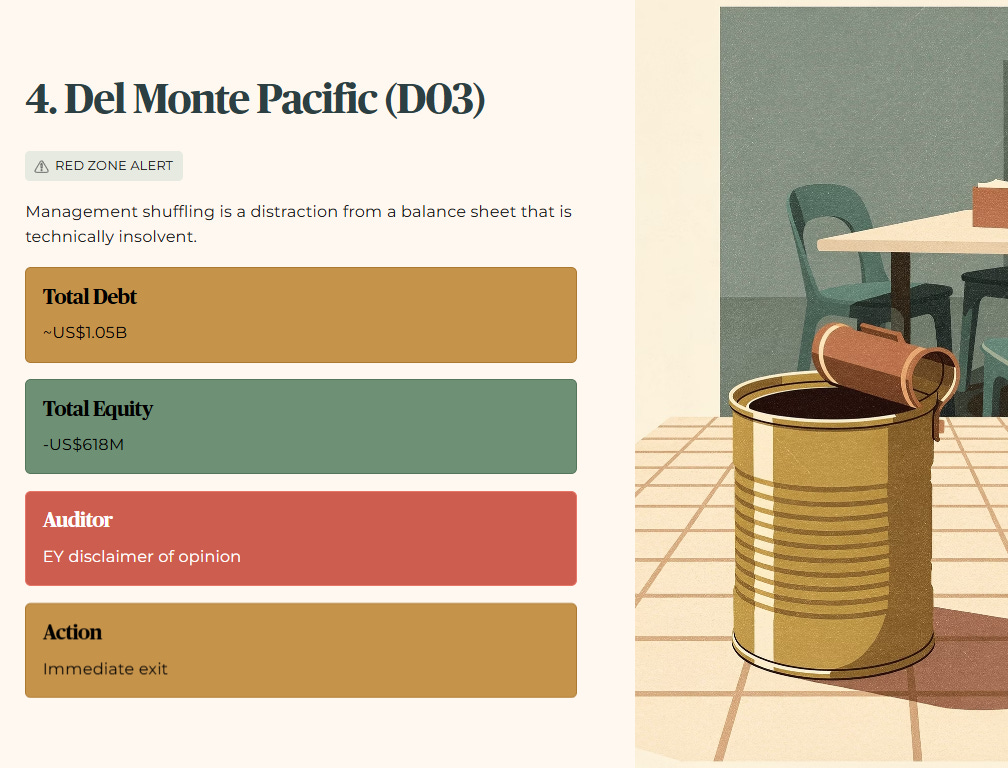

4. DEL MONTE PACIFIC (D03) — Red Zone Alert

Management shuffling is a distraction from a balance sheet that is technically insolvent at the equity level.

Layer 1: Alongside a formal SGX filing regarding a COO transition, the audited FY2025 balance sheet reveals total equity starkly negative at -US$618 million, with an EY disclaimer of opinion on the accounts.

Layer 2: This structural reality obliterates any historical benchmark, shifting the narrative from high leverage directly into technical insolvency.

Layer 3: You cannot even benchmark this against standard SGX consumer peers. It fails the basic mathematical test of a going concern.

Layer 4: If lending conditions tighten by 10% in the next quarter, the inability to roll over its US$565 million in pre-restructuring short-term borrowings for its Asia and Philippines continuing operations will force immediate liquidations and an equity wipeout.

Layer 5: For anyone holding this in their CPF investment account, based on my forensic framework, this registers as a Red Zone Watchlist Trigger for immediate capital preservation rather than waiting for a turnaround.

Iggy’s Insight: Corporate reshuffles mean nothing when the balance sheet is mathematically broken. Del Monte is operating with negative US$618 million in equity and carrying an EY disclaimer of opinion. That is not a turnaround narrative — that is technical insolvency dressed up in a press release.

When liabilities exceed assets to this degree, the equity tranche is effectively worthless. Retail investors holding this are not investing; they are providing exit liquidity for creditors. You do not buy a company that fails the basic test of a going concern. It is like buying a FairPrice house brand tin of beans and finding out the tin is empty — and you still owe the cashier money.

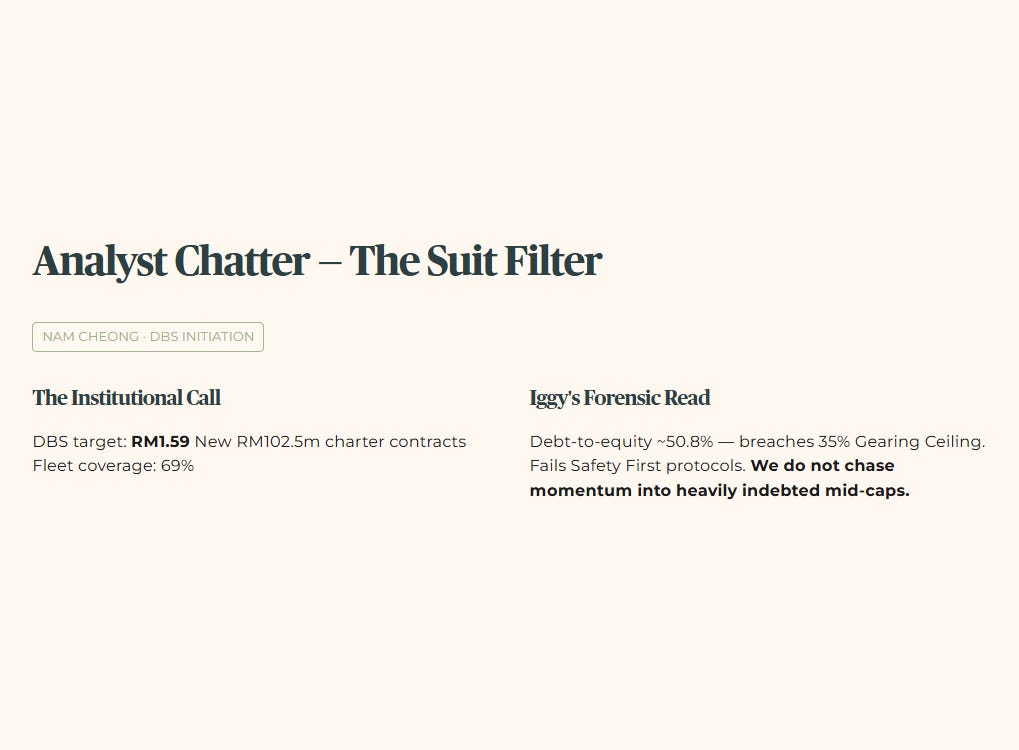

ANALYST CHATTER — The Suit Filter

DBS initiated coverage on Nam Cheong with a target of RM1.59, based on restructured debt and new RM102.5 million charter contracts. The fleet coverage looks solid at 69%, but our forensic logic applies here regardless.

The SGX filing indicates a debt-to-equity ratio of approximately 50.8%. This breaches the Iggy 35% Gearing Ceiling. The institutional call rests on debt repayment prioritisation clauses, but structural leverage of that magnitude means it fails our Safety First protocols. We do not chase momentum into heavily indebted mid-caps.

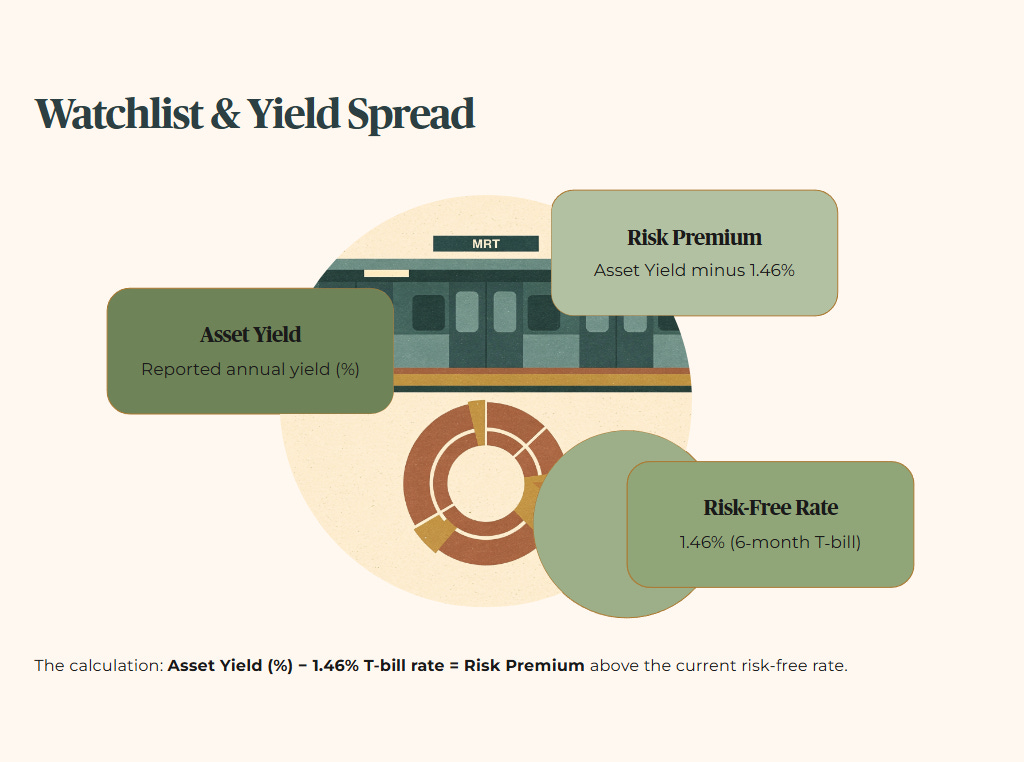

WATCHLIST & YIELD SPREAD

The calculation: Asset Yield (%) minus 1.46% (6-month T-bill, Mar 31, 2026 auction) = Risk Premium above the current risk-free rate.

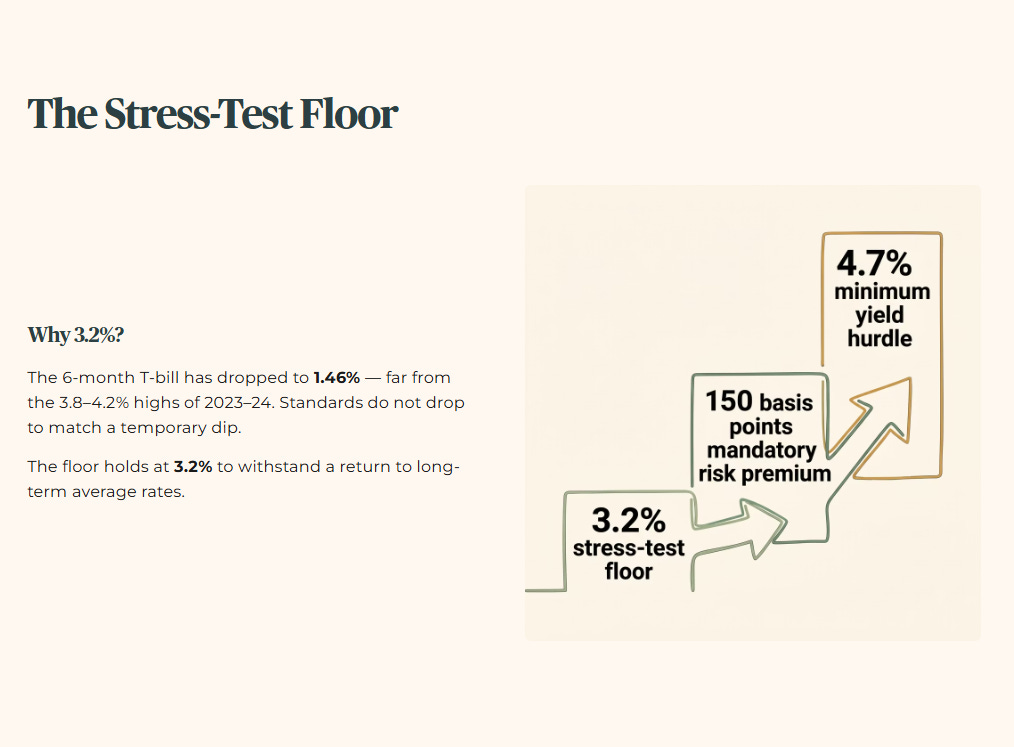

A note on the Stress-Test Buffer: For this audit, I apply a conservative floor of 3.2%. We audit for the storm, not just the sunny day. The 6-month T-bill has dropped to 1.46% — a long way from the 3.8–4.2% highs of 2023 and 2024. I do not lower my standards to match a temporary market dip. The floor holds at 3.2% to ensure sanctuary assets can withstand a return to long-term average rates. The minimum yield hurdle remains 4.7% — that is the 3.2% floor plus 150 basis points of mandatory risk premium.

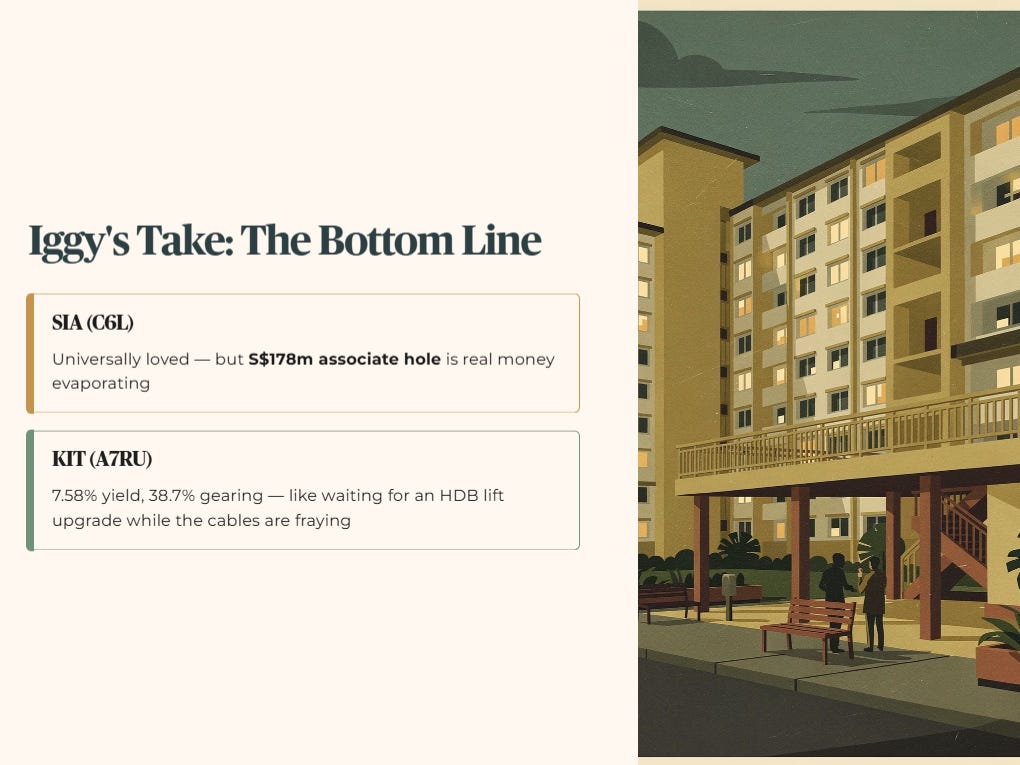

🦎 IGGY’S TAKE: THE BOTTOM LINE

The market is throwing a lot of optical illusions at us today. Singapore Airlines is universally loved, but that S$178 million associate hole is real money evaporating from the bottom line. Over at the REITs, we are seeing the classic tension between headline yields and balance sheet realities. Keppel Infrastructure Trust is offering an attractive 7.58%, but holding 38.7% net gearing while doing so is like waiting for an HDB lift upgrade while the cables are already fraying. It works until it abruptly stops working.

And let’s be honest, the true danger lies in the offshore spaces. Prime US REIT’s 45.0% leverage is a blinking red light for an impending equity cash call. Del Monte is operating with confirmed negative equity and an auditor disclaimer.

For a retiree in Choa Chu Kang managing SRS funds, you cannot afford to finance these corporate debt walls. The numbers must be cold and they must be clean. Are you buying genuine cash flow, or are you just providing liquidity to a sponsor’s balance sheet problem?

Capital preservation starts where the illusions end.

Iggy’s Forensic Compliance Standards — Standard Disclaimer

This content is produced for educational and informational purposes only. I am not a financial advisor — I am a retail investor who applies forensic analysis to my own portfolio and shares that process publicly. Nothing here constitutes a recommendation to buy, sell, or hold any security, and no specific target prices or personalised financial advice are offered. All data is sourced from public filings and verified sources; where data is unverified it is explicitly flagged. All investments carry risk, including the potential loss of principal, and past performance is not indicative of future results. If you are making investment decisions involving CPF, SRS, or personal capital, please conduct your own due diligence or consult a MAS-licensed financial adviser before committing funds.