DBS Group Holdings: A world-class giant at the crossroads

DBS Group Holdings (SGX: D05) just posted steady H1 2025 results in a falling-rate world. For Singapore investors, the question is simple: is quality now priced for perfection, or is there still.....

DBS Group Holdings: A world-class giant at the crossroads

DBS Group Holdings (SGX: D05) just posted steady H1 2025 results in a falling-rate world. For Singapore investors, the question is simple: is quality now priced for perfection, or is there still a margin of safety?

Rates are easing, fee income is rising, and the stock sits near record highs. In this note, I lay out 3 good, 3 red flags, and Iggy’s verdict so you can frame a clear decision without the noise.

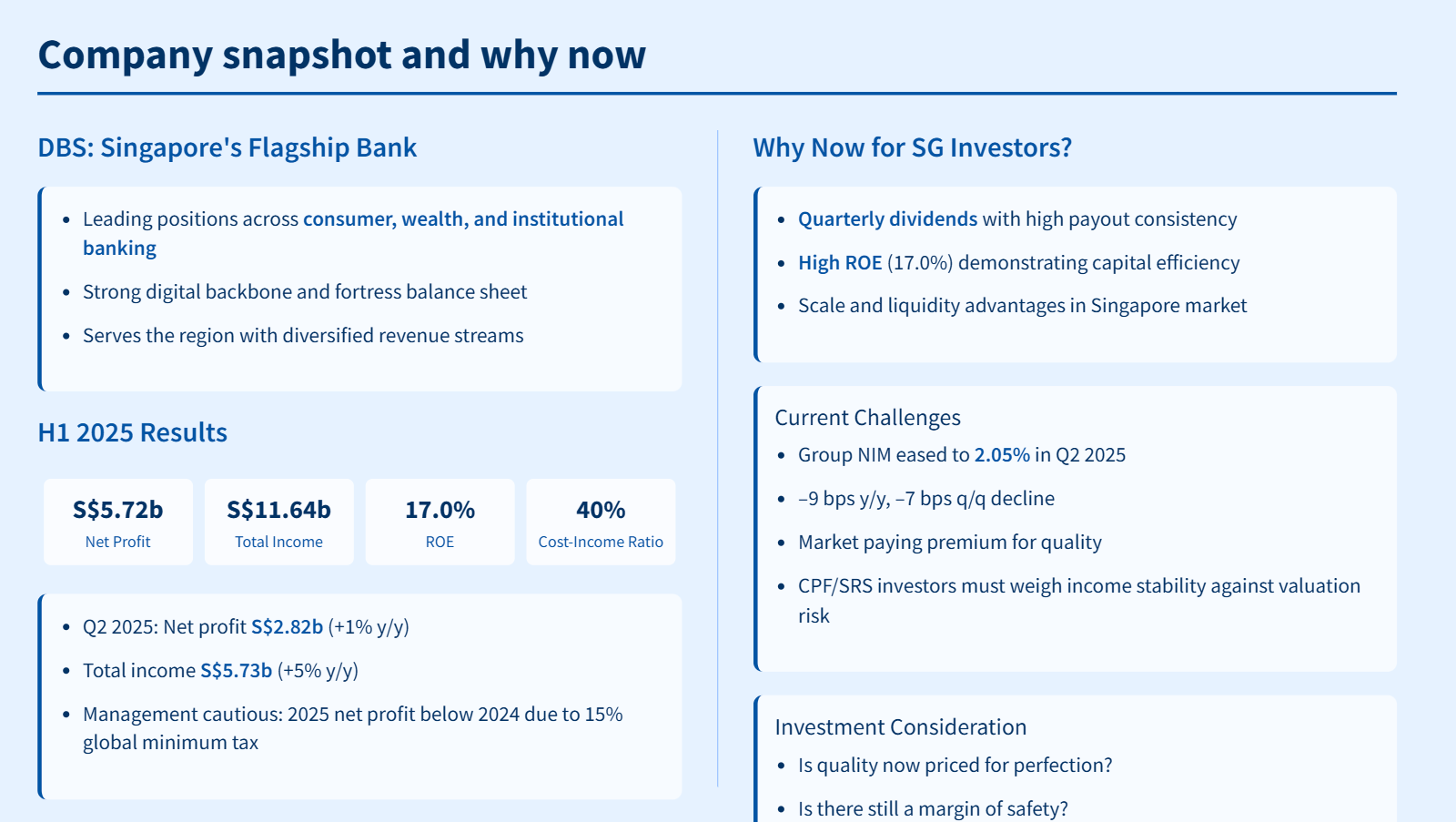

Company snapshot and why now

DBS is Singapore’s flagship bank with leading positions across consumer, wealth, and institutional banking. It serves the region with a strong digital backbone and a fortress balance sheet. H1 2025 results show resilience: net profit S$5.72b (flat y/y), total income S$11.64b (+5% y/y), ROE 17.0%, and cost-income ratio 40%. Q2 2025 delivered net profit S$2.82b (+1% y/y), with total income S$5.73b (+5% y/y). Management kept a cautious stance for 2025, noting net profit will be below 2024 levels due to the 15% global minimum tax even as net interest income holds slightly above 2024.

Why now for SG investors? DBS offers quarterly dividends, high ROE, and scale. But the setup is tricky. Group NIM eased to 2.05% in Q2 2025 (–9 bps y/y, –7 bps q/q). The market still pays up for quality. CPF/SRS investors must weigh income stability against valuation risk and the path of rates.

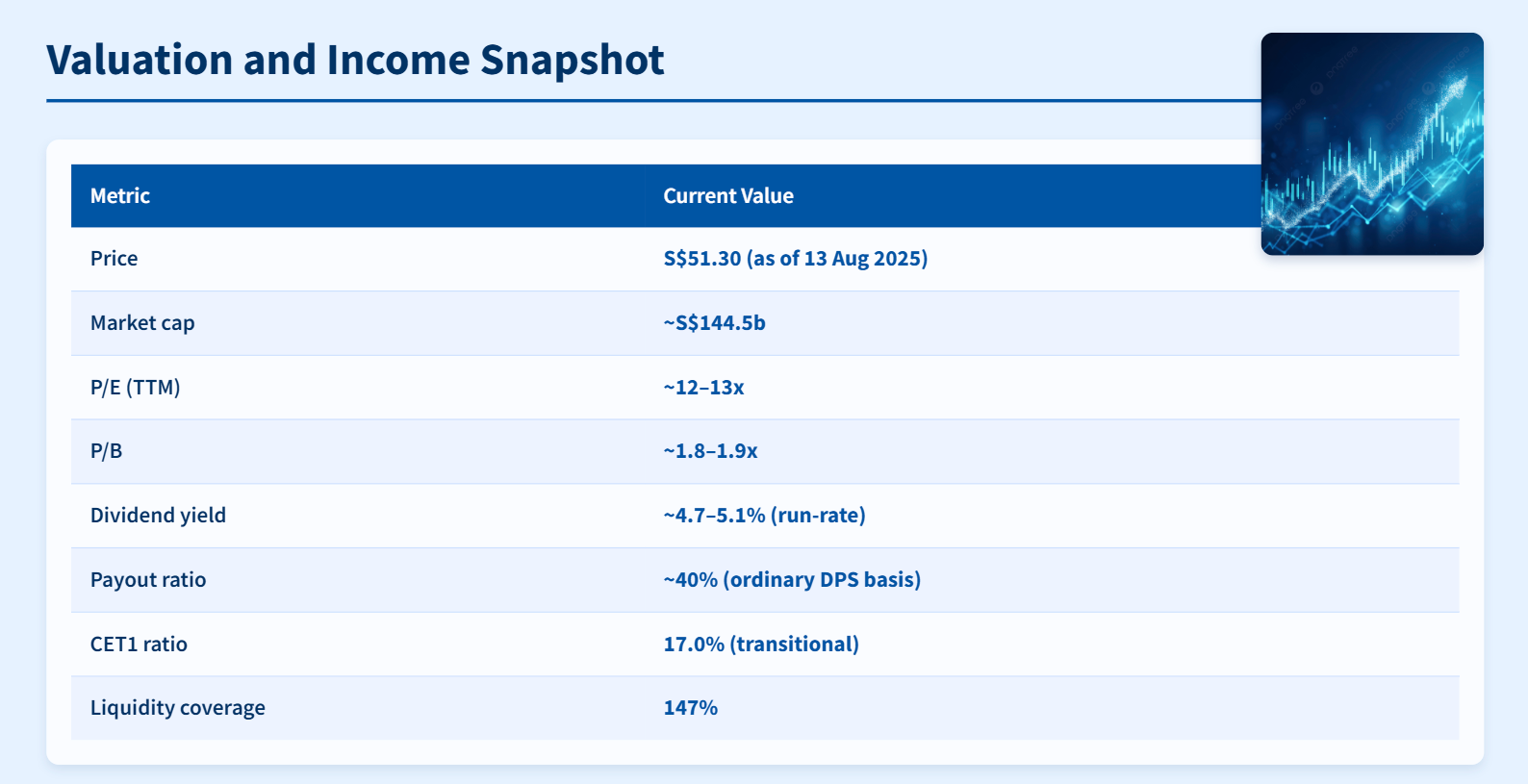

Table: Valuation and income snapshot (Current)

DBS trades at a premium P/B to local peers due to high ROE, digital scale, and balance sheet strength. For income-focused SG investors, a near-5% yield with quarterly payouts compares well to SGS yields. The premium implies the market is pricing steady execution even as margins compress and tax headwinds bite.