DBS Hits All-Time Highs: Is This Banking Giant Still Worth Your Investment?

With DBS shares soaring past S$54 and market cap crossing S$150 billion, Singapore’s banking leader faces a critical question—can it justify these stratospheric valuations?

The banking giant just achieved another milestone, pushing its stock price to unprecedented heights while leaving rivals OCBC and UOB in the dust. But as any seasoned Singapore investor knows, record highs often trigger the age-old debate: opportunity or trap?

The numbers tell a compelling story, yet they also reveal the complexity facing investors today. With interest rates shifting, wealth management booming, and valuations stretching to new extremes, DBS presents both tremendous strengths and legitimate concerns that every portfolio decision must weigh carefully.

In This Article:

• The Unstoppable Rise of Southeast Asia’s Banking Titan

• Record-Breaking Financial Performance Drives Investor Confidence

• The Wealth Management Gold Mine Fuels Growth

• Navigating the Interest Rate Headwinds

• Valuation Reality Check: Premium or Justified?

• Strategic Capital Allocation Rewards Shareholders

• The Verdict: Quality Commands Its PriceThe Unstoppable Rise of Southeast Asia’s Banking Titan

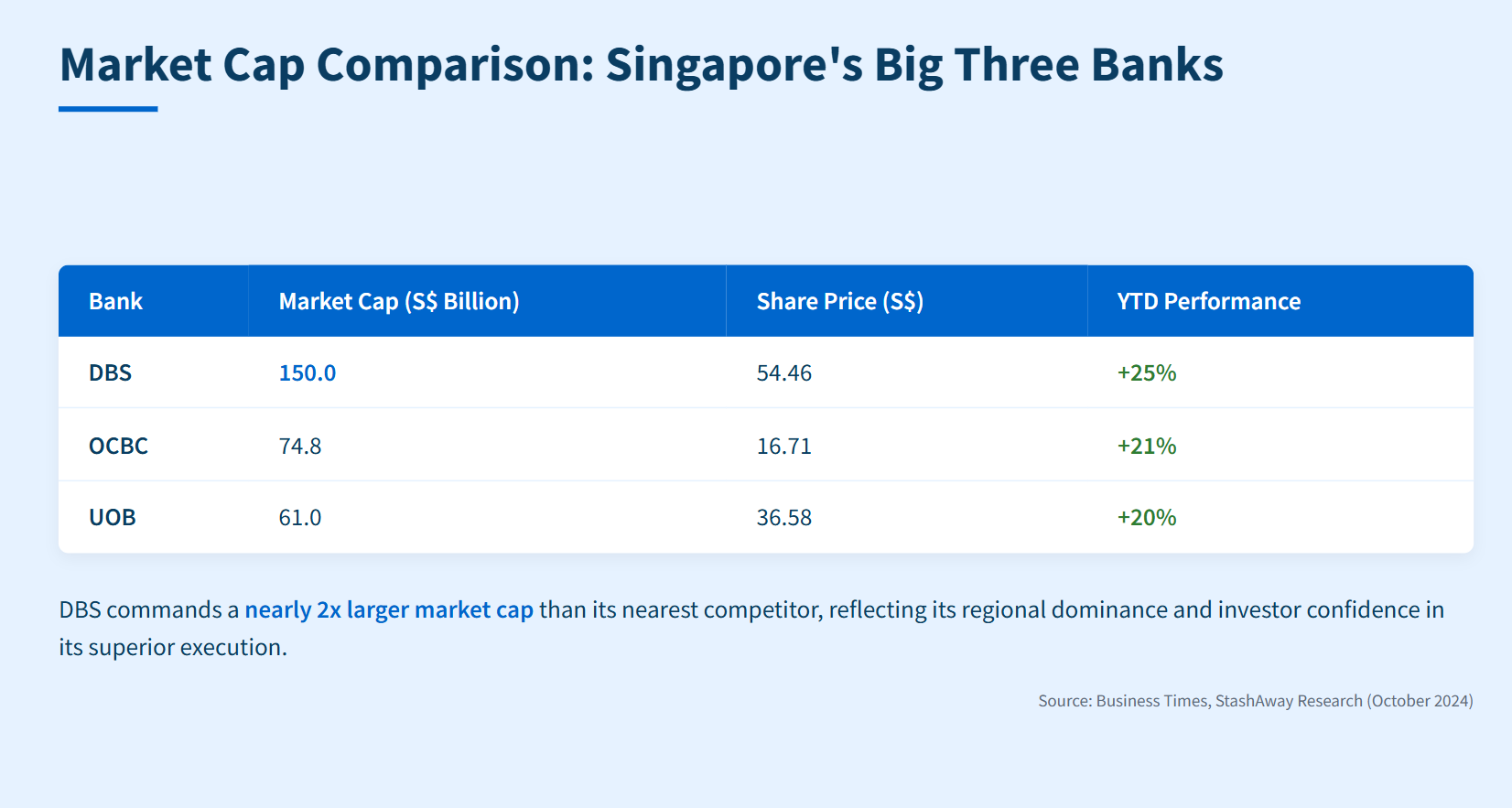

DBS has become the undisputed heavyweight champion of Southeast Asian banking. The bank’s journey to S$54.46 per share represents a remarkable 25% climb year-to-date, pushing its market capitalization beyond S$150 billion. This achievement makes DBS nearly twice the size of its nearest competitor OCBC, whose market cap sits at approximately S$75 billion.

The bank’s dominance extends beyond mere size. DBS became the first Singapore-listed company to cross the US$100 billion market cap threshold, a milestone that underscores its regional significance. This wasn’t a fluke—it reflects sustained operational excellence and strategic positioning that continues to attract premium valuations from investors.

Market Cap Comparison Table: Singapore’s Big Three Banks

Source: Business Times, StashAway Research (October 2024)

This table reveals the substantial gap between DBS and its competitors, highlighting why the bank commands such attention from institutional and retail investors alike. The market has consistently rewarded DBS’s superior execution with a valuation premium that shows no signs of diminishing.

Record-Breaking Financial Performance Drives Investor Confidence

The third quarter of 2024 delivered exceptional results that justify much of the market’s enthusiasm. DBS reported record quarterly net profit of S$3.03 billion, representing a 15% year-over-year increase and 8% sequential growth. This marked the first time the bank surpassed the S$3 billion quarterly profit threshold, setting a new benchmark for Singapore’s banking sector.asianbankingandfinance+1

Total income surged 11% to S$5.75 billion, driven by broad-based growth across multiple business lines. The bank’s diversified revenue streams proved their worth, with record fee income leading the charge alongside stronger treasury customer sales and the highest markets trading income in ten quarters.dbs+1

DBS Q3 2024 Performance Breakdown

Source: DBS Q3 2024 Results Presentation

The nine-month performance tells an equally impressive story, with net profit reaching a record S$8.79 billion and return on equity maintaining a robust 18.8%. These metrics demonstrate DBS’s ability to generate superior returns on shareholder capital, a key factor driving the premium valuation multiple investors willingly pay.

The Wealth Management Gold Mine Fuels Growth

The standout performer in DBS’s portfolio has been wealth management, which generated record fee income and represents a structural shift in the bank’s business model. Wealth management fees surged 45% in 2024 to reach S$2.18 billion, driven by broad-based growth in investment products and bancassurance.

This phenomenal growth reflects Singapore’s emergence as a regional wealth hub, attracting affluent clients seeking stability and sophisticated financial services. DBS has positioned itself at the center of this trend, with assets under management reaching a record S$396 billion. The bank’s digital capabilities and regional presence make it particularly attractive to high-net-worth individuals diversifying across Asia.

The wealth management surge isn’t just about fees—it represents a fundamental transformation toward more stable, recurring revenue streams. Unlike traditional lending, wealth management generates income through asset-based fees that prove more resilient during economic downturns and interest rate cycles.

This shift toward fee-based income provides DBS with greater earnings stability and justifies higher valuation multiples typically reserved for asset management companies rather than traditional banks.

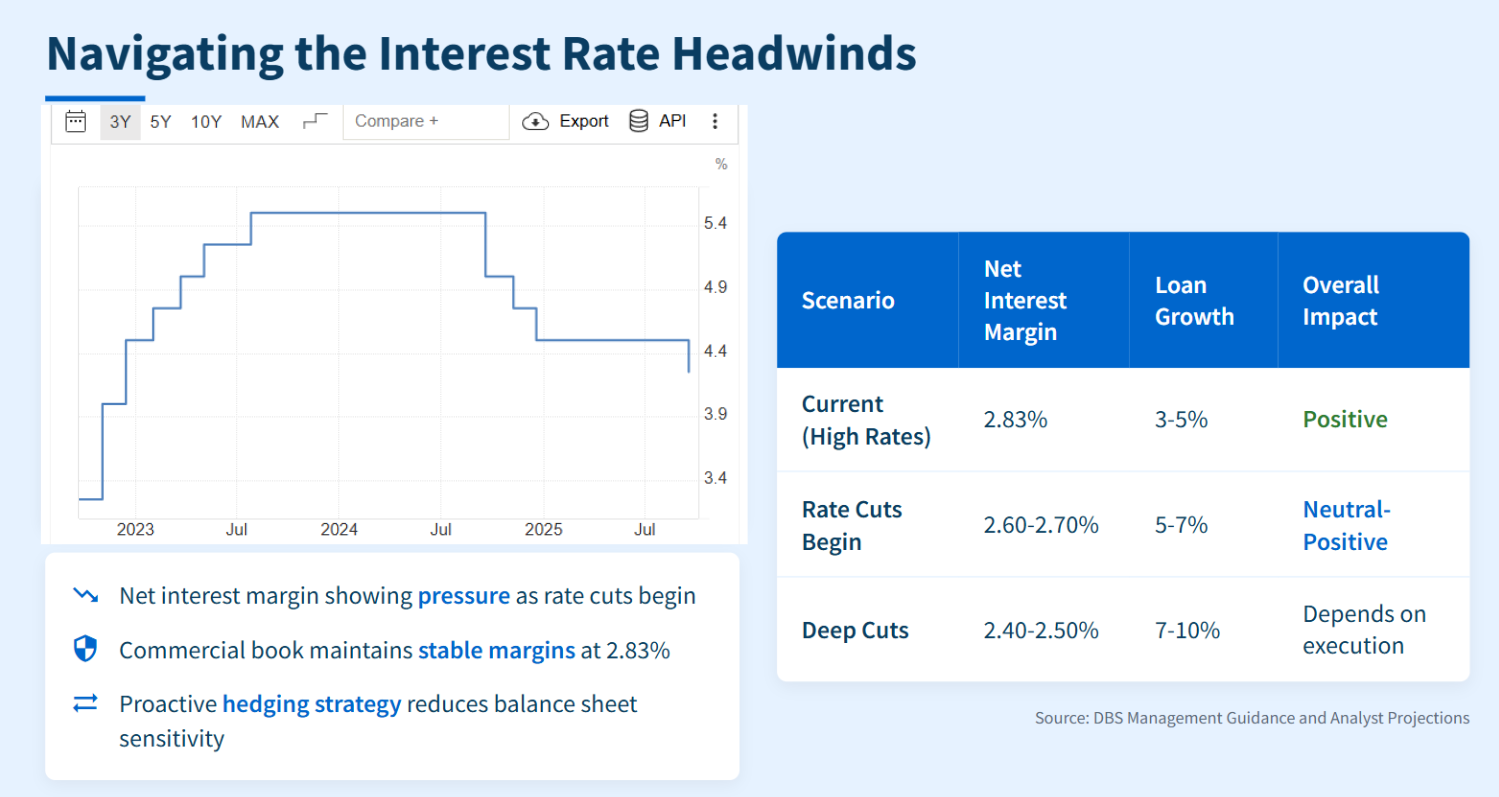

Navigating the Interest Rate Headwinds

The elephant in the room remains interest rate sensitivity, particularly as central banks globally pivot toward cutting rates. DBS faces the same fundamental challenge as all banks: falling rates compress net interest margins while potentially stimulating loan growth. The bank’s net interest margin has already shown signs of pressure, declining from previous peaks as rate cuts begin to filter through the system.

The bank’s commercial book maintained stable net interest margins of 2.83% in Q3 2024, while management has strategically reduced balance sheet sensitivity to rate changes. This proactive hedging approach, combined with continued balance sheet growth, has helped offset margin pressure through volume expansion.

The Federal Reserve’s recent rate cuts and projected future reductions create both challenges and opportunities. Lower rates should stimulate loan demand, potentially driving growth that compensates for margin compression. DBS management expects exactly this dynamic, projecting that rate decreases will boost lending activity while the bank’s diversified fee income provides additional stability.

Interest Rate Impact Analysis

Source: DBS Management Guidance and Analyst Projections

This analysis suggests DBS is well-positioned to weather the rate transition, particularly given its strong fee income growth and operational efficiency initiatives.

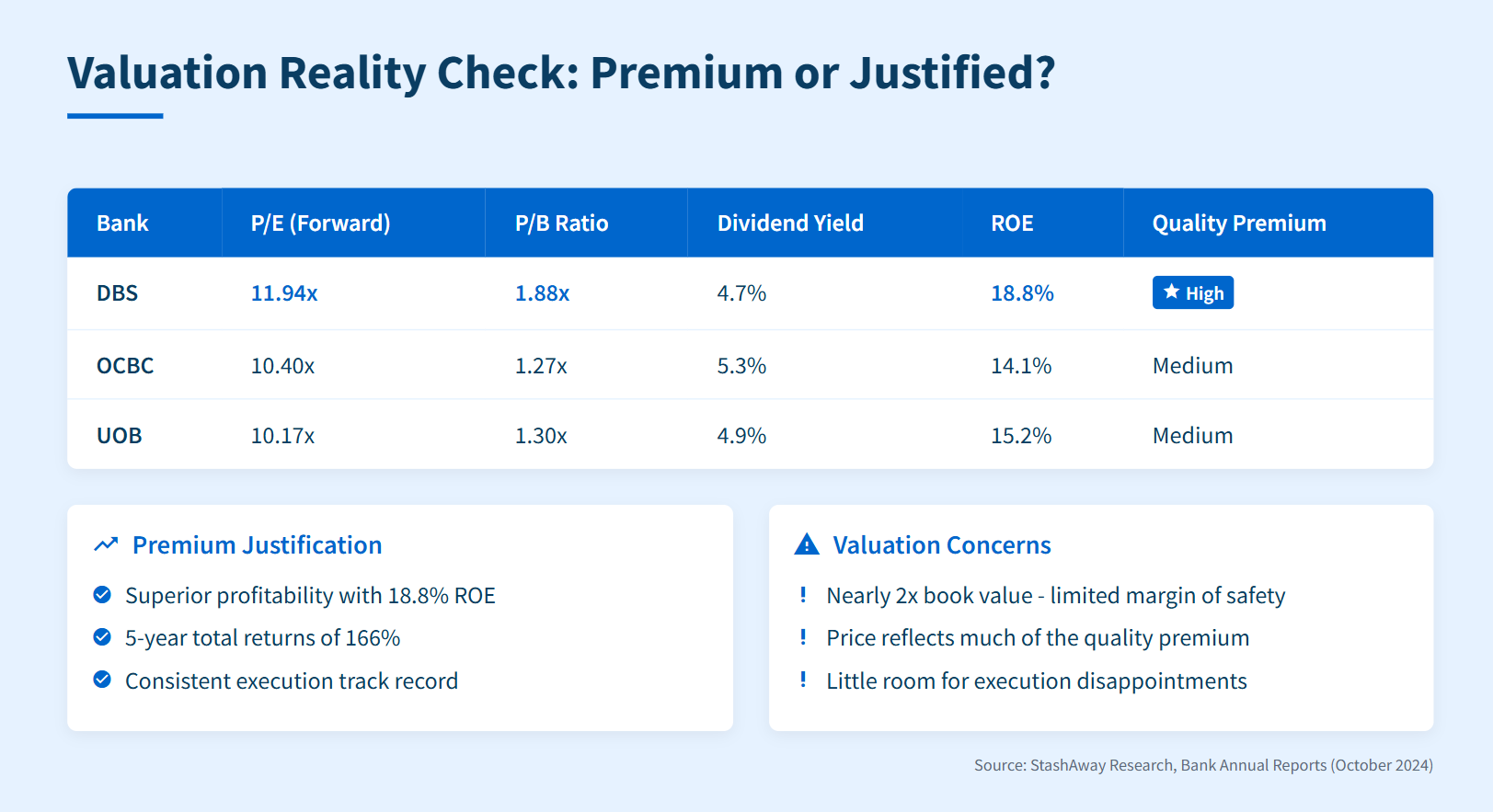

Valuation Reality Check: Premium or Justified?

At current levels, DBS trades at compelling yet expensive metrics that demand careful consideration. The bank’s price-to-book ratio of 1.88 significantly exceeds OCBC’s 1.27 and UOB’s 1.30, reflecting the market’s willingness to pay up for DBS’s superior performance. Forward price-to-earnings ratios around 11.94 also command a premium to local peers, though this remains reasonable for a bank generating 18%+ returns on equity.

The question becomes whether these valuations reflect fair value or speculative excess. DBS’s track record suggests the premium is largely justified—the bank has consistently delivered superior profitability, growth, and shareholder returns compared to regional peers. Five-year total returns of 166% dwarf the broader market and demonstrate the bank’s ability to compound shareholder wealth effectively.

Yet valuations matter, particularly for new investors considering entry points. At nearly 2x book value, DBS offers limited margin of safety compared to its historically cheaper peers. Investors must weigh the bank’s quality and growth prospects against the price being demanded by the market.

Comparative Valuation Metrics

Source: StashAway Research, Bank Annual Reports (October 2024)

This comparison reveals DBS’s premium positioning while highlighting the value proposition offered by its competitors, giving investors choice based on their risk-return preferences.

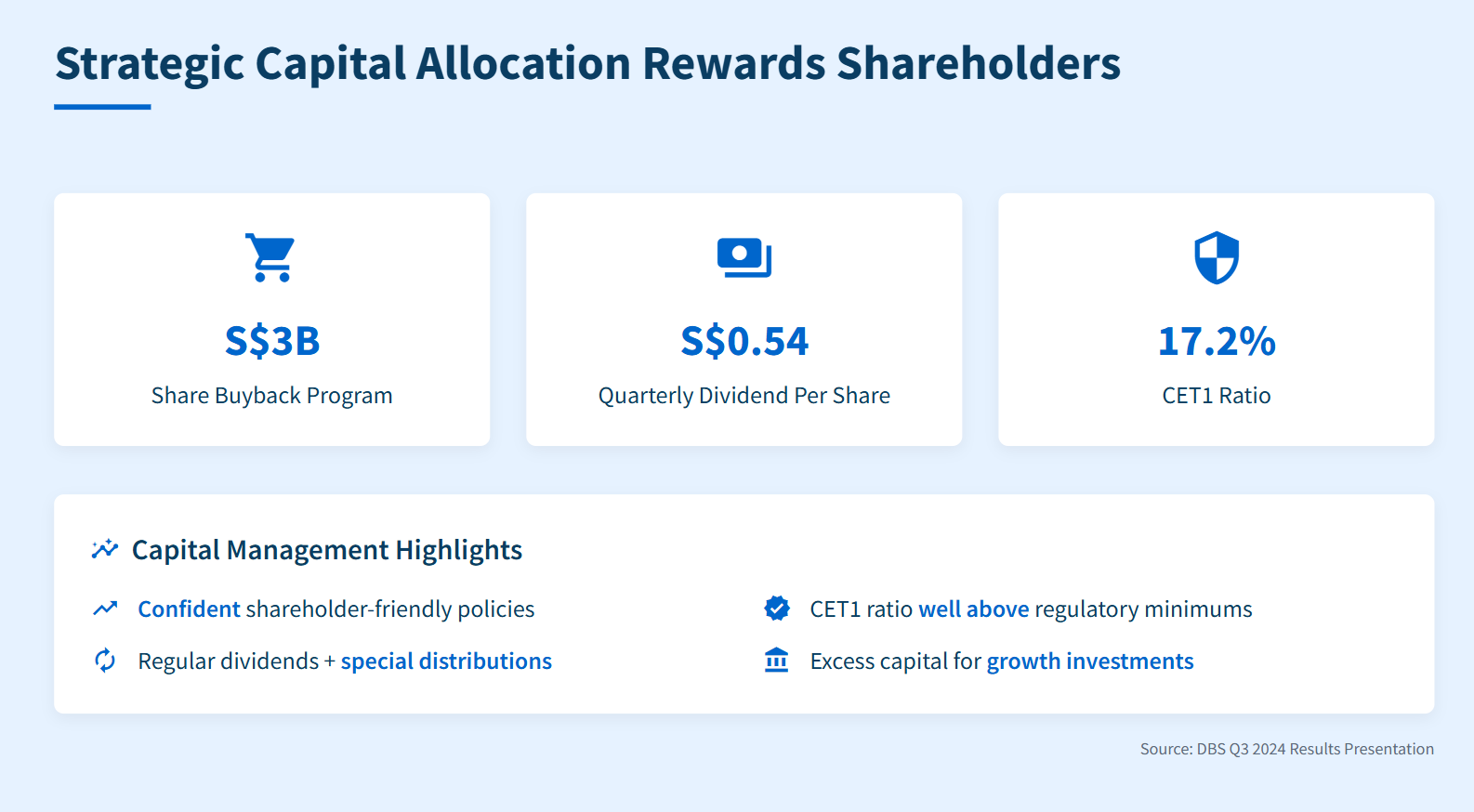

Strategic Capital Allocation Rewards Shareholders

DBS’s approach to capital management demonstrates confident, shareholder-friendly policies that support the investment thesis. The bank announced a new S$3 billion share buyback program alongside its Q3 results, adding to regular dividend payments and special distributions. This aggressive capital return strategy reflects management’s confidence in future earnings and commitment to returning excess capital to shareholders.

The dividend policy remains attractive, with the board declaring a quarterly dividend of S$0.54 per share for Q3, bringing the year-to-date total to S$1.62 per share. Combined with the ongoing buyback program and announced capital return dividends, DBS offers multiple ways for shareholders to benefit from the bank’s cash generation capabilities.

This capital allocation strategy becomes particularly important as banking regulations require stronger capital buffers. DBS maintains a robust CET1 ratio of 17.2% on a transitional basis, well above regulatory minimums. This excess capital provides flexibility for both growth investments and shareholder returns, supporting the bank’s premium valuation.

The Verdict: Quality Commands Its Price