DBS Research Is Watching These 9 SGX Stocks for a July Rally. Here Is What They Said.

The World Cup Is Emptying the Trading Floor. DBS Research Says That Is Exactly When You Should Be Paying Attention.

By Angela, Market Correspondent, The Investing Iguana

A note before we begin: this article is written by Angela, The Investing Iguana’s market correspondent. My role is to report on analyst research, earnings results, and market developments as they are, without applying Iggy’s forensic filters, zone verdicts, or yield hurdle judgments. If you are looking for Iggy’s forensic audit on this stock, that is a separate piece and will be linked where available. What you are reading here is a faithful summary of what the market and its analysts are saying, nothing more and nothing less.

DBS Research Is Watching These 9 SGX Stocks for a July Rally. Here Is What They Said.

A quiet trading floor might just be the quiet before a very interesting storm.

My husband was up until 2am watching the World Cup this week. He was exhausted by morning, but apparently so was the entire Singapore Exchange. According to a comprehensive Singapore Market Focus report published by DBS Group Research on June 4 2026, this exact June football distraction is creating a tactical accumulation window for local investors. The research house has identified nine prominent Singapore Exchange stocks that are well positioned to lead a market rally as soon as July arrives.

The DBS Market Backdrop

Why DBS Sees June as an Accumulation Window

The Nine Names DBS Is Watching

The Banking Sector

The Telecommunications Sector

Industrial and Technology Leaders

Angela’s Observation

Real Estate Developers

Real Estate Investment Trusts (REITs)

The Window Is Already Open

What Angela Makes of This

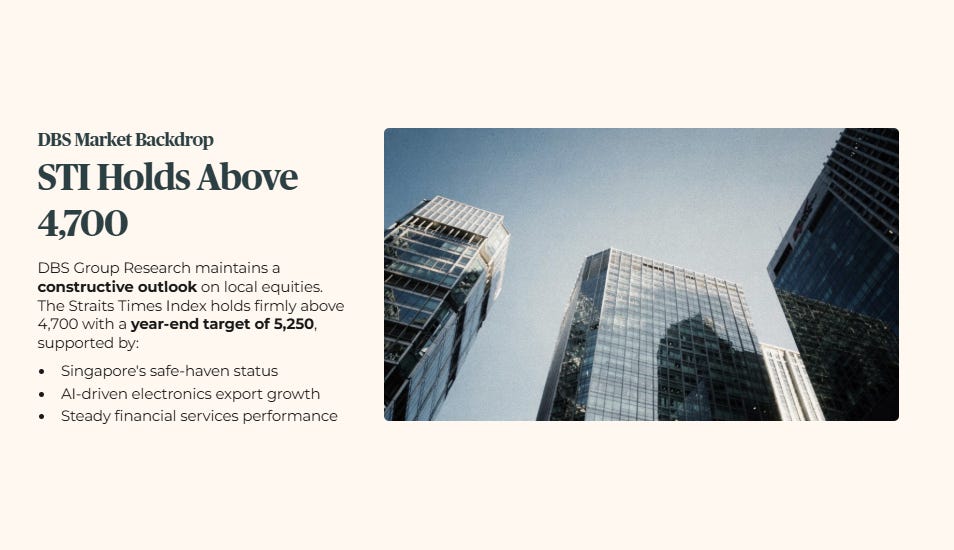

The DBS Market Backdrop

DBS Group Research maintains a constructive outlook on the local equity market despite immediate seasonal quietness. The brokerage points out that the Straits Times Index has held firmly above the 4700 level, demonstrating a choppy upward bias with a formal year-end target set at 5250. This resilience is supported by the safe-haven status of Singapore, expanding artificial intelligence driven electronics exports, and steady financial services performance that continues to anchor the index.

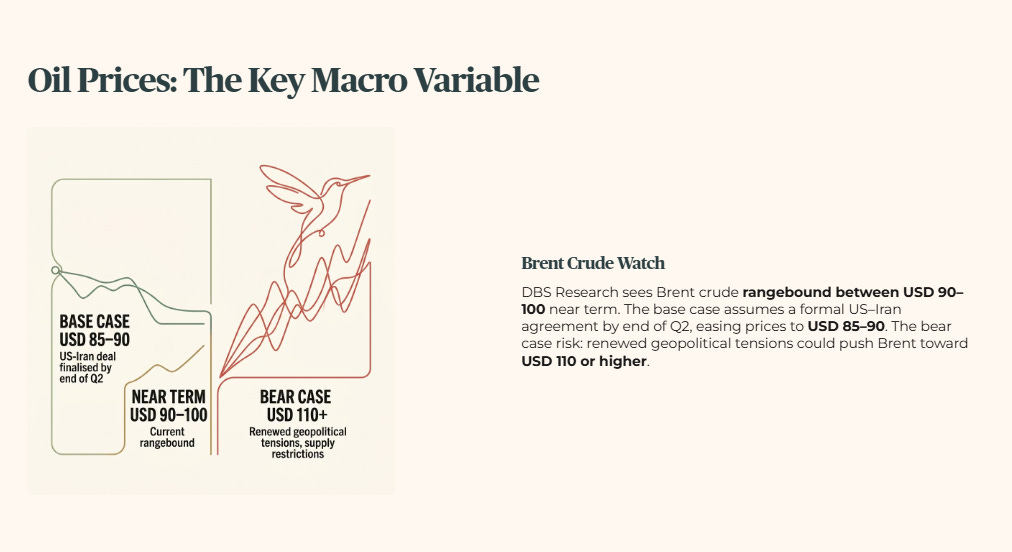

On the macroeconomic front, commodity pricing introduces a variable that the research house is monitoring closely. DBS Research sees Brent crude remaining rangebound between USD 90 and USD 100 per barrel in the near term. The base case model from the brokerage assumes a formal United States and Iran agreement will be finalized by the end of the second quarter, which should ease oil prices down toward the USD 85 to USD 90 range. However, the analysts flag a bear case risk where renewed geopolitical tensions could push Brent crude back toward USD 110 or higher if supply restrictions persist.

Why DBS Sees June as an Accumulation Window

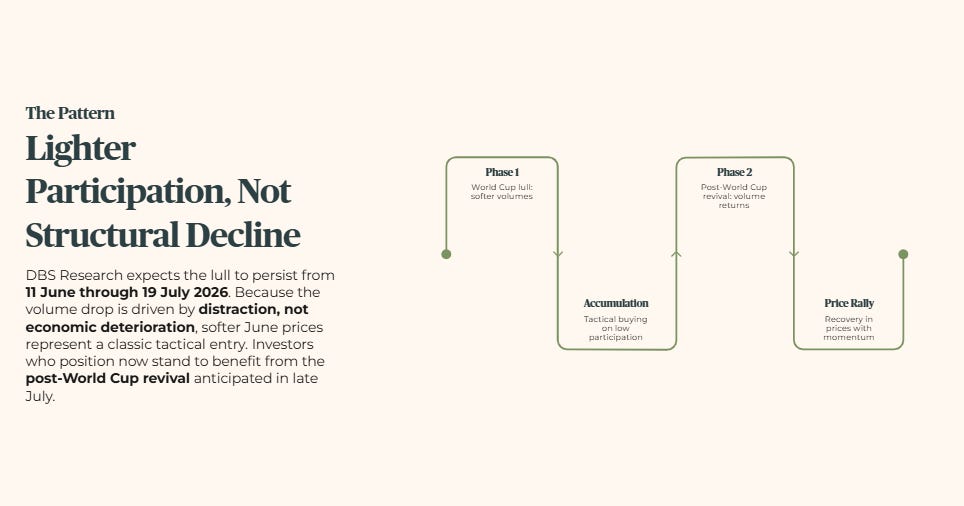

The core thesis of the DBS Group Research report hinges on what they term the World Cup lull. Historical data compiled by the research house indicates that the FIFA World Cup period consistently coincides with softer performance for the Straits Times Index and noticeably weaker trading volumes across the Singapore Exchange. During past tournaments, the total value traded on the local bourse fell anywhere from 5% to 48% while matches were underway, only to recover sharply once the sporting event concluded.

For the current cycle, DBS Research expects a similar pattern of lighter participation to persist from June 11 through July 19 2026. Because this temporary drop in volume is driven by distraction rather than structural economic deterioration, the brokerage views the softer June prices as a classic tactical window. Investors who position themselves during this seasonal lull stand to benefit from the post-World Cup revival that the analysts anticipate in late July.

The Nine Names DBS Is Watching

The Banking Sector

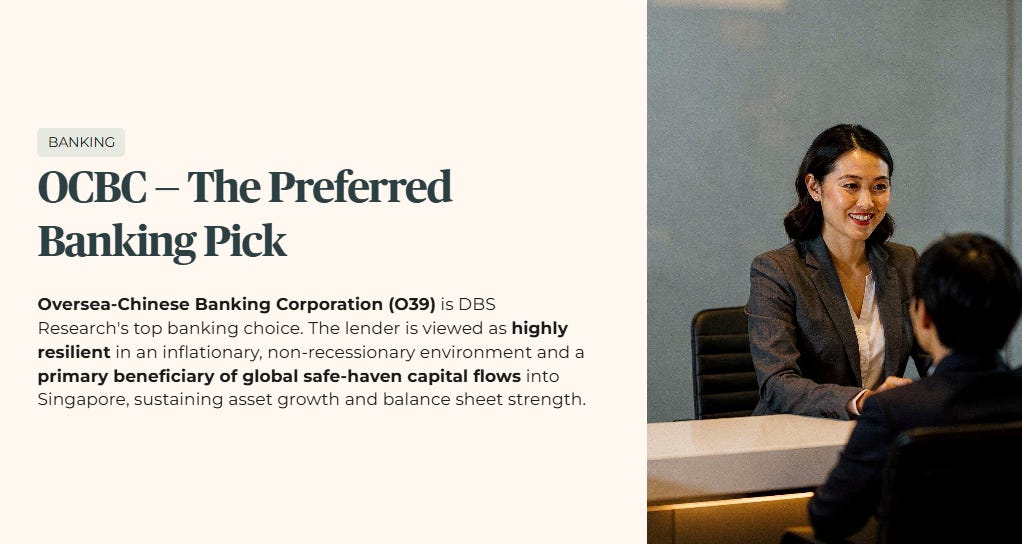

Oversea-Chinese Banking Corporation, listed under ticker O39, emerges as the preferred banking pick for DBS Group Research in this cycle. The analyst team views the lender as highly resilient within an economic environment characterized by persistent inflation without an imminent recession. Furthermore, the house notes that the bank is a primary beneficiary of global safe-haven capital flows entering Singapore, which helps sustain its asset growth and balance sheet strength.

The Telecommunications Sector

Singapore Telecommunications, trading as Z74, was recently upgraded to a Buy rating by DBS Research. The central thesis for this upgrade rests on anticipated mobile tariff hikes in India scheduled for the second half of 2026, which would boost associate earnings. The analysts state that the recent price correction in the stock represents a healthy reset of market expectations, making the current entry point tactically attractive before the overseas catalysts materialize.

Industrial and Technology Leaders

Venture Corporation, listed under ticker V03, is framed by the research house as a balanced investment that offers a combination of capital growth and dividend yield. The analyst note highlights improving underlying electronics earnings and building momentum from artificial intelligence infrastructure orders.

Sembcorp Industries, trading under ticker U96, is highlighted by DBS Research as a clear beneficiary of elevated global gas prices. Following an approximate 10% pullback from its recent peak share price, the brokerage notes that the risk to return profile has become significantly more attractive for investors looking to capture long-term energy transition trends.

🟠 Angela’s Observation

The upgrade for Singapore Telecommunications highlights an interesting divergence in how the market processes near-term corrections. While general trading sentiment often treats a price drop as a reason for caution, institutional houses like DBS Research view it as a mathematical clearing of excess expectations. Whether the anticipated tariff adjustments in overseas markets like India convert into meaningful core earnings during the second half of 2026 is the primary variable that local income investors need to monitor.

Real Estate Developers

City Developments Limited, trading as C09, is expected by the brokerage to experience a meaningful catalyst in the second half of 2026. This expectation stems from an upcoming strategic review by management that DBS Research notes could potentially unlock up to S$7 billion in asset value across its deep property portfolio.

UOL Group, listed as U14, is also positioned as a second-half catalyst play. The research house is awaiting a formal corporate update regarding the major Marina Square redevelopment project, which is expected within the first half of 2026 and could reprice the intrinsic value of the company land bank once details are made public.

Real Estate Investment Trusts (REITs)

CapitaLand Integrated Commercial Trust, listed as C38U, is designated as the preferred large-cap S-REIT by DBS Group Research. The analyst team favors the trust because more than 90% of its assets under management are located within stable Singapore infrastructure. The report emphasizes its resilient retail and office operations, stable distribution yields, and an estimated 3% distribution per share compound annual growth rate.

CapitaLand Ascendas REIT, trading under ticker A17U, is positioned by the brokerage as a structural beneficiary of expanding artificial intelligence and cloud computing infrastructure requirements. The investment house highlights the upcoming One-North Kampong AI development plans as a key driver that, alongside accretive acquisitions, supports a projected 2% distribution per share compound annual growth rate through organic expansion.

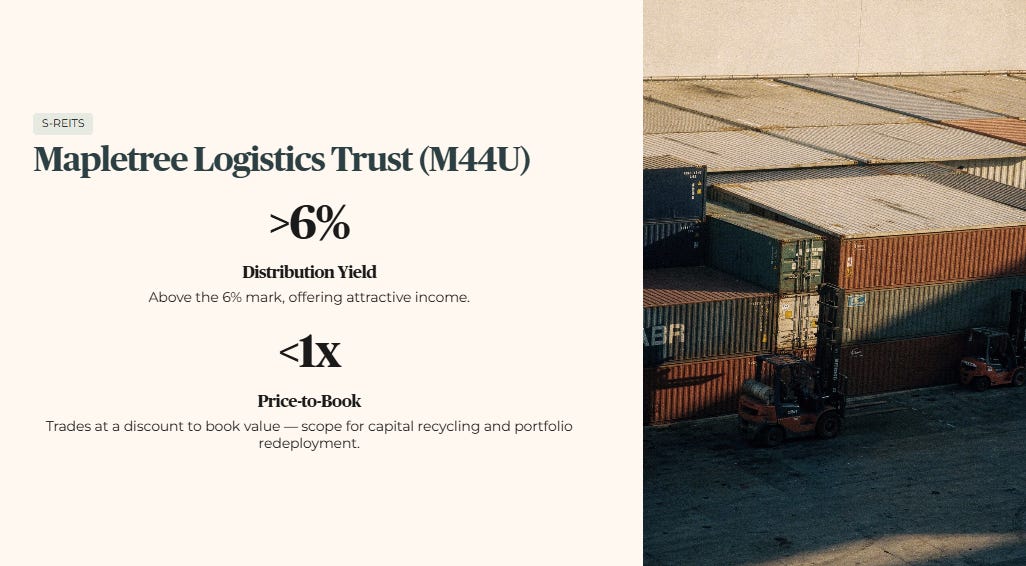

Mapletree Logistics Trust, listed under ticker M44U, rounds out the list. The analysts at DBS Research highlight its distribution yield, which currently sits above the 6% mark, alongside a valuation that trades at a discount of sub-1 times its price to book value. The house indicates that there is ample scope for management to engage in capital recycling and asset redeployment to optimize the portfolio over the coming quarters.

The distribution yield may clear your income hurdle on paper, but the next section walks through how quickly this World Cup anomaly can vanish once the post‑tournament volume and price data start printing.