DBS Says BUY on OUE REIT’s 8% Yield. Our Forensic Screen Found a 2.34x Problem.

When a Headline Yield Hides a Balance Sheet Problem

A single accounting entry of 2.34 tells you everything you need to know about the thin line between nominal cash flow and structural asset erosion.

When a major financial institution issues a resounding BUY call on a real estate investment trust based on future rental upside, retail investors frequently overlook the balance sheet scaffolding holding the entire asset class together.

This forensic audit will break down exactly why a headline yield can mask severe structural vulnerabilities when the underlying interest coverage cracks beneath a high interest rate environment.

Reviewing institutional research requires a clear head and a complete separation of operational performance from balance sheet stability.

As the Singapore market consolidates around record highs, the temptation to reach for high-yielding real estate counters becomes incredibly strong for capital focused entirely on monthly or quarterly distribution checks.

It is precisely during these moments of market optimism that a strict, rule-based forensic screen becomes your most valuable defensive tool.

Section 1 — The Analyst’s Case

Section 2 — Iggy’s Forensic Screen

Financial Health Checklist

Section 3 — The Dividend Trajectory

Section 4 — The Forensic Gap

Iggy’s Insight Box 1

Section 5 — What To Watch Next

Iggy’s Insight Box 2

Closing — The Forensic Stance

Section 1 — The Analyst’s Case

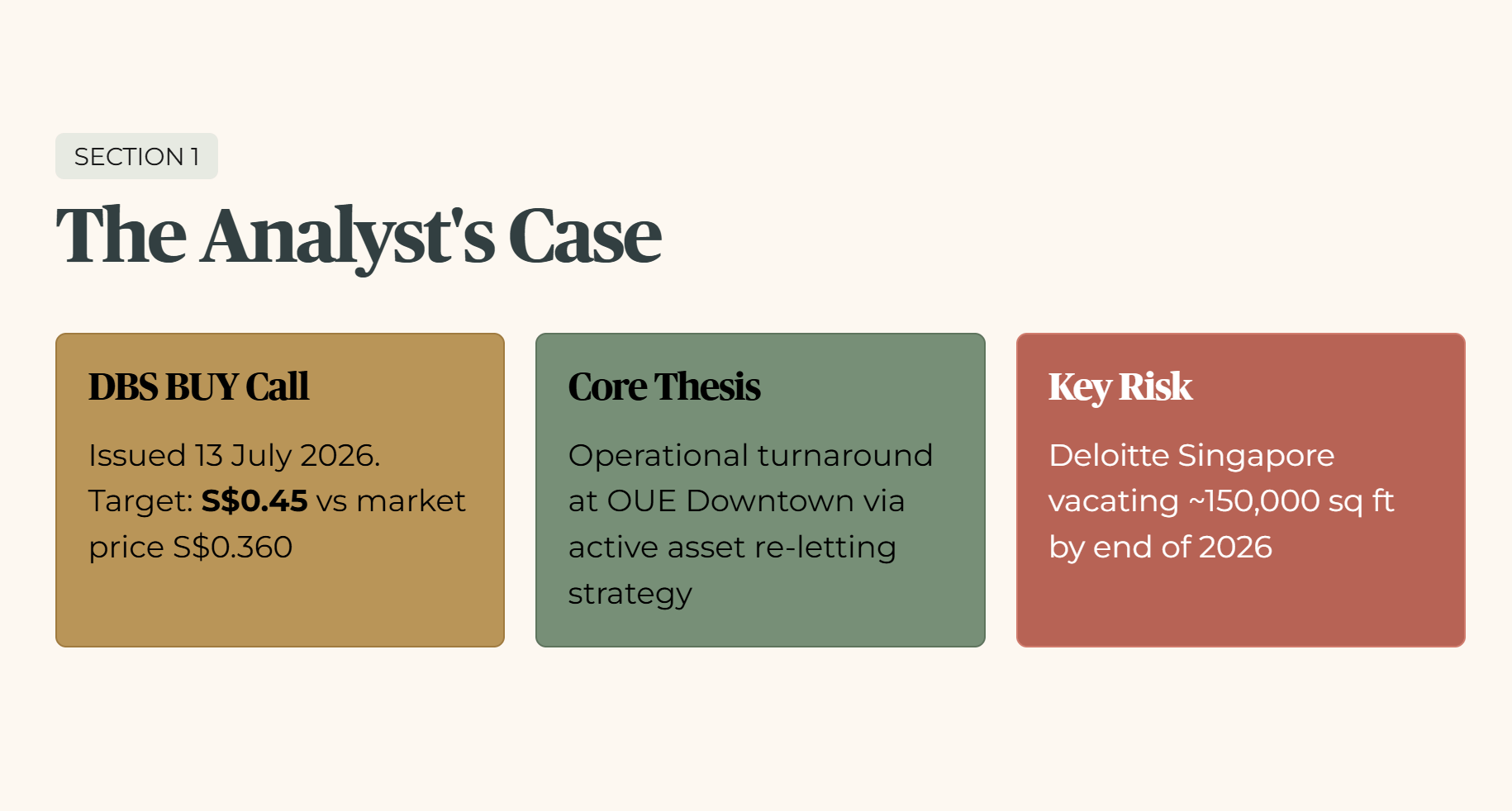

The institutional thesis issued by DBS on 13 July 2026 maintains a highly constructive outlook on OUE REIT (TS0U), reiterating a BUY recommendation with a target price of S$0.45 against a market price of S$0.360, confirmed via Longbridge real-time quote as at 17 July 2026.

The core of the analyst’s case rests on an operational turnaround and an active asset re-letting strategy at OUE Downtown. The building is facing a major near-term transition as its third-largest tenant, Deloitte Singapore, prepares to vacate approximately 150,000 square feet of space by the end of 2026 to relocate to Orchard Central, following a brief interim transition to co-working spaces.

Because Deloitte currently contributes approximately 4.9% of total portfolio revenues and roughly 7% of commercial rental income based on FY2025 metrics, this departure introduces an undeniable short-term income overhang. If the entire 150,000 square feet were to remain completely vacant throughout FY2027, the analyst estimates a maximum theoretical downside risk of a 7% drop in full-year DPU. However, the institutional research frames this material event not as an existential threat, but as a long-term commercial opportunity.

The structural justification for the BUY call hinges on a significant rental reversion gap. Deloitte’s historical lease was signed at an estimated historical rate below S$8 per square foot, which sits comfortably underneath prevailing market asking rents of approximately S$10 per square foot for comparable properties in the area. Even with core Grade A office rents in the Central Business District averaging S$12.50 per square foot as of the second quarter of 2026, the analyst argues that OUE Downtown, despite its older vintage and slightly lower competitive stance, will successfully capture sub-divided leasing demand due to a lack of new prime CBD office supply.

Beyond the office portfolio, the institutional thesis incorporates secondary operational elements. The planned divestment of Crowne Plaza Changi Airport is expected to result in a minor ~2% contraction in FY2027F DPU, which management intends to offset through capital recycling strategies. The report highlights potential growth vectors, including the acquisition of an expanded stake in the Salesforce Tower in Sydney, where certain minority owners are reportedly open to exiting their positions, alongside potential asset optimization strategies involving One Raffles Place.

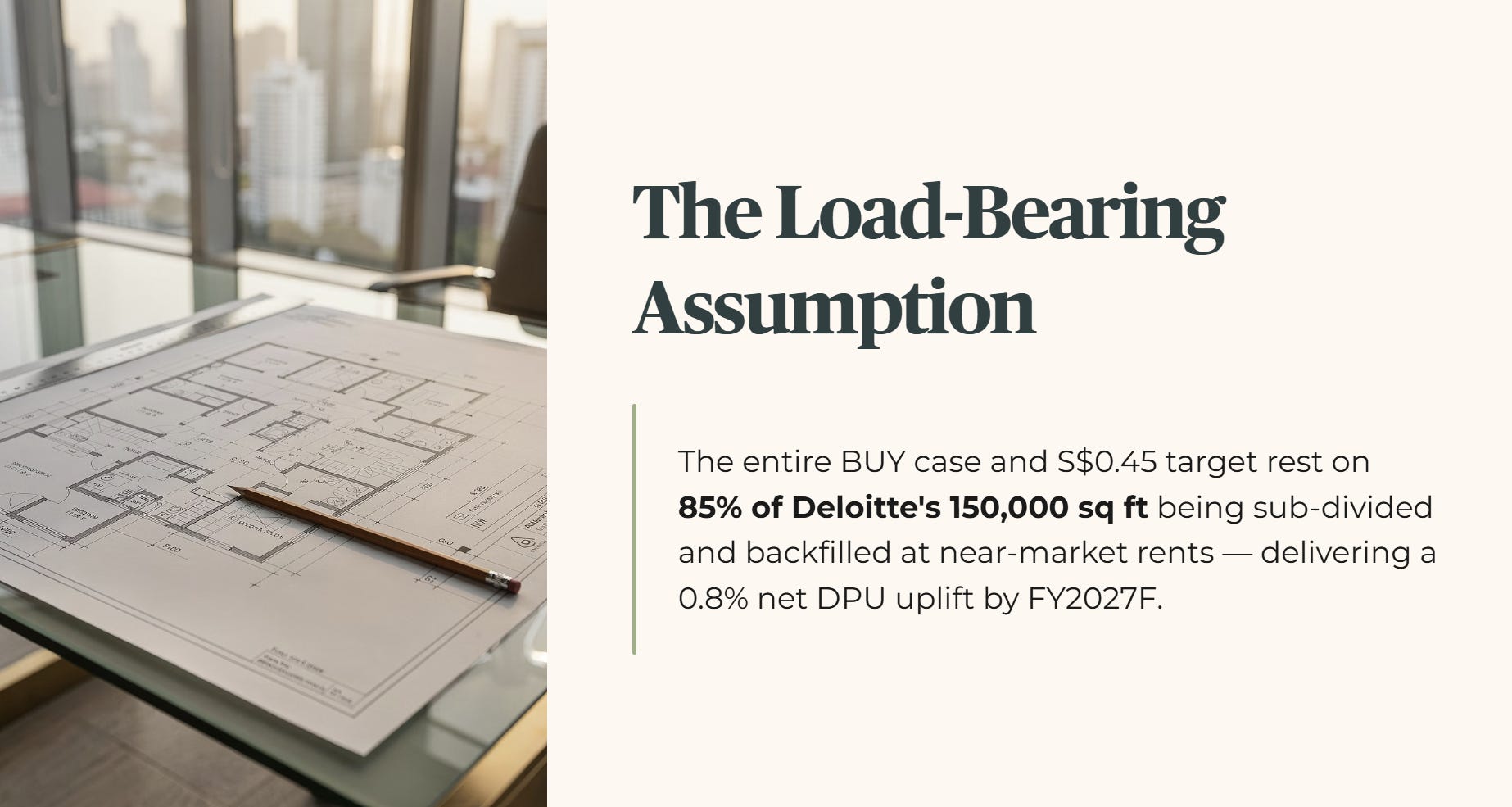

THE LOAD-BEARING ASSUMPTION: The entire institutional BUY case and the S$0.45 valuation target rest entirely on the operational projection that approximately 85% of Deloitte’s vacated 150,000 square feet will be successfully sub-divided and backfilled at near-market rents, delivering a 0.8% net DPU uplift by FY2027F.

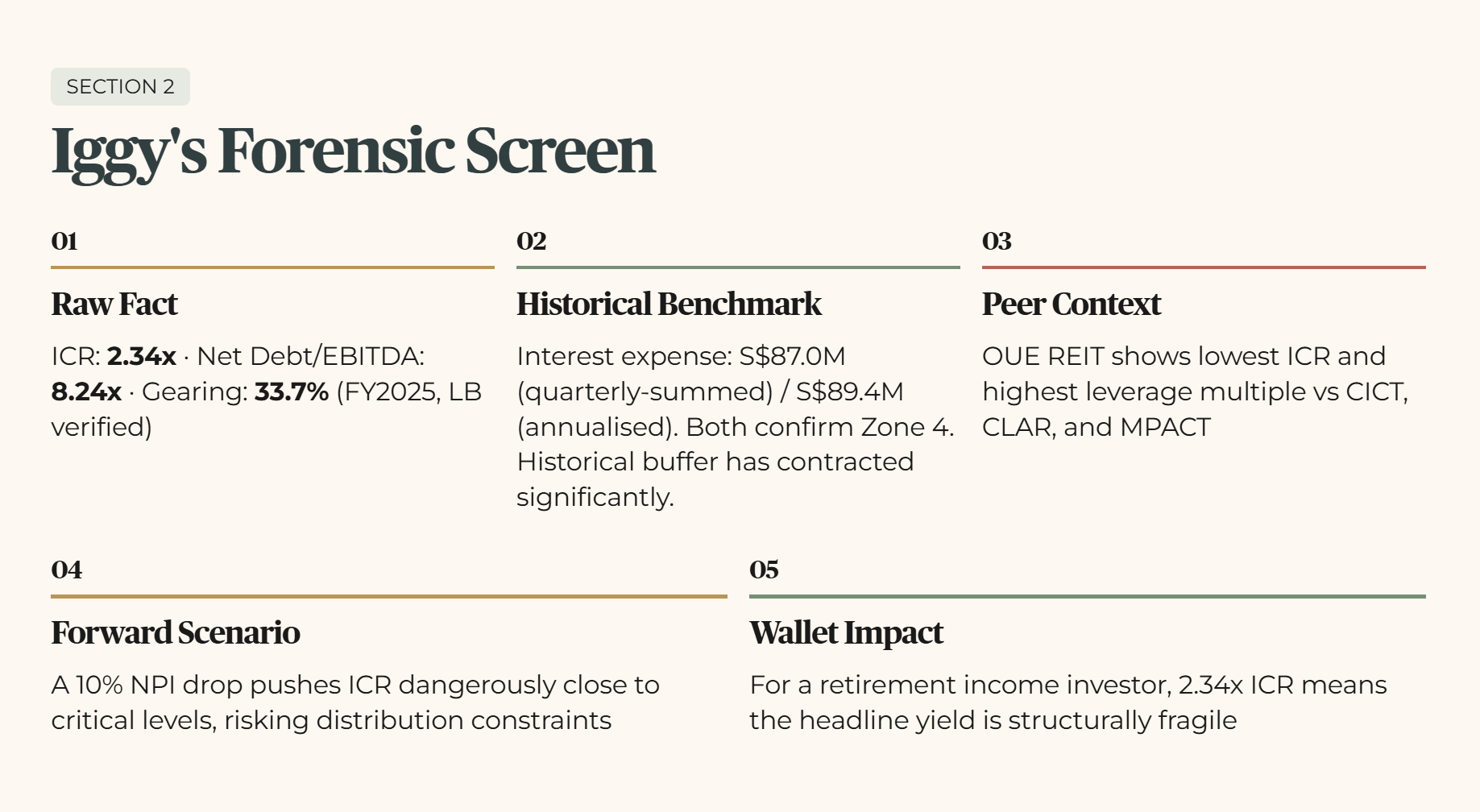

Section 2 — Iggy’s Forensic Screen

Our forensic framework does not evaluate real estate assets based on what a leasing manager hopes to achieve eighteen months from now; it audits the structural reality of the balance sheet today.

Applying the five-layer audit to OUE REIT using verified data as of 17 July 2026 reveals a severe divergence between operational optimism and balance sheet resilience.

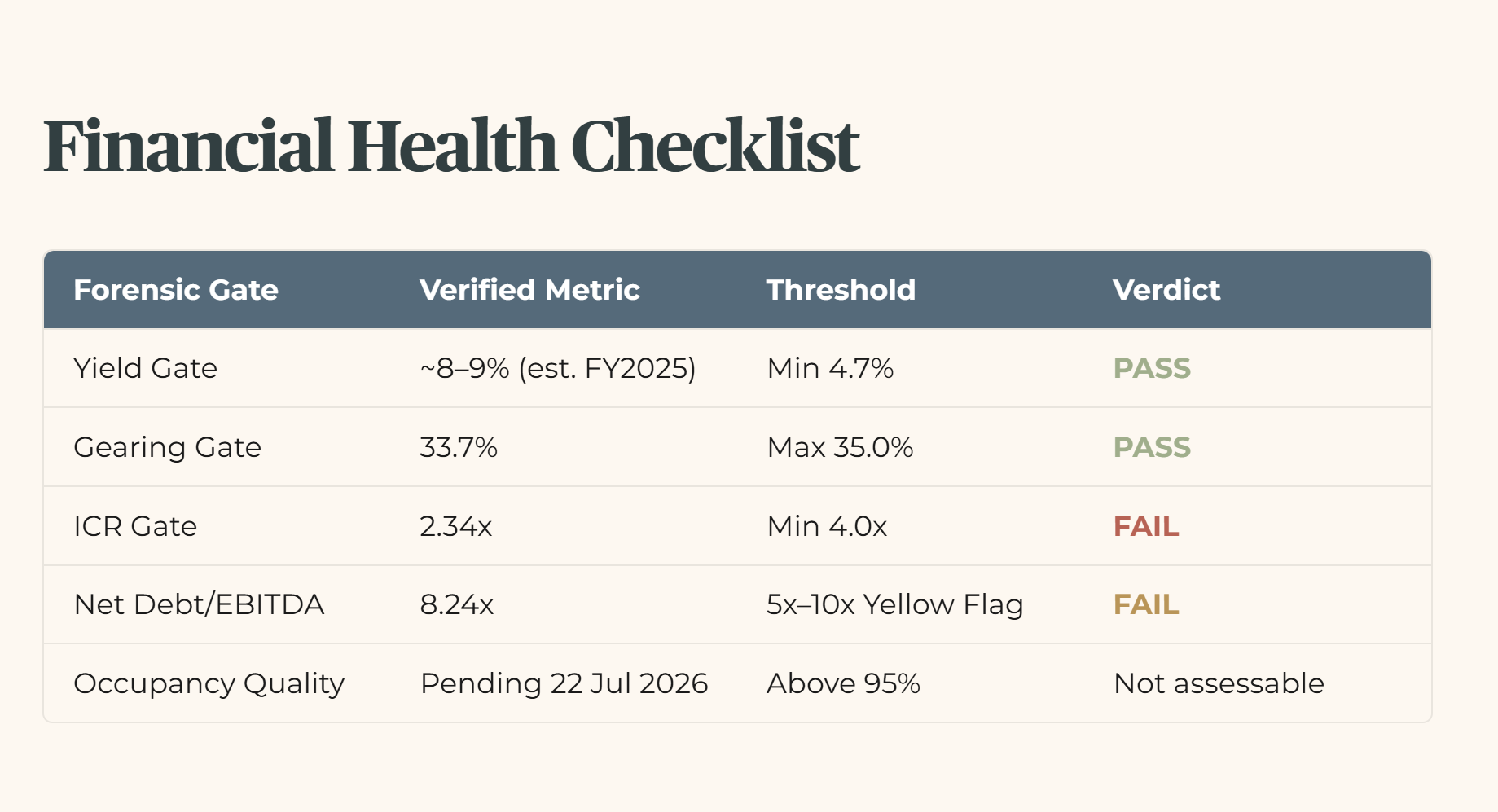

Layer 1 — Raw Fact: The verified Interest Coverage Ratio (ICR) stands at 2.34x, confirmed via Longbridge structured data as at 17 July 2026 and based on FY2025 filings, the most recent full-year figures available ahead of the 22 July 2026 H1 2026 release. The Net Debt to EBITDA ratio is 8.24x, and aggregate gearing sits at 33.7%, both confirmed on the same basis, against a current market price of S$0.360.

Layer 2 — Historical Benchmark: Looking across a multi-year horizon, the financing costs of the REIT have adjusted dramatically to the prevailing interest rate environment. A review of the interest expense line shows two closely aligned figures: a quarterly-summed total of S$87.0 million and an annualised headline figure of S$89.4 million. Both produce an interest coverage ratio within the same Zone 4 range, so the small variance does not change the forensic verdict. The historical buffer that protected distributions has contracted significantly as debt has rolled over.

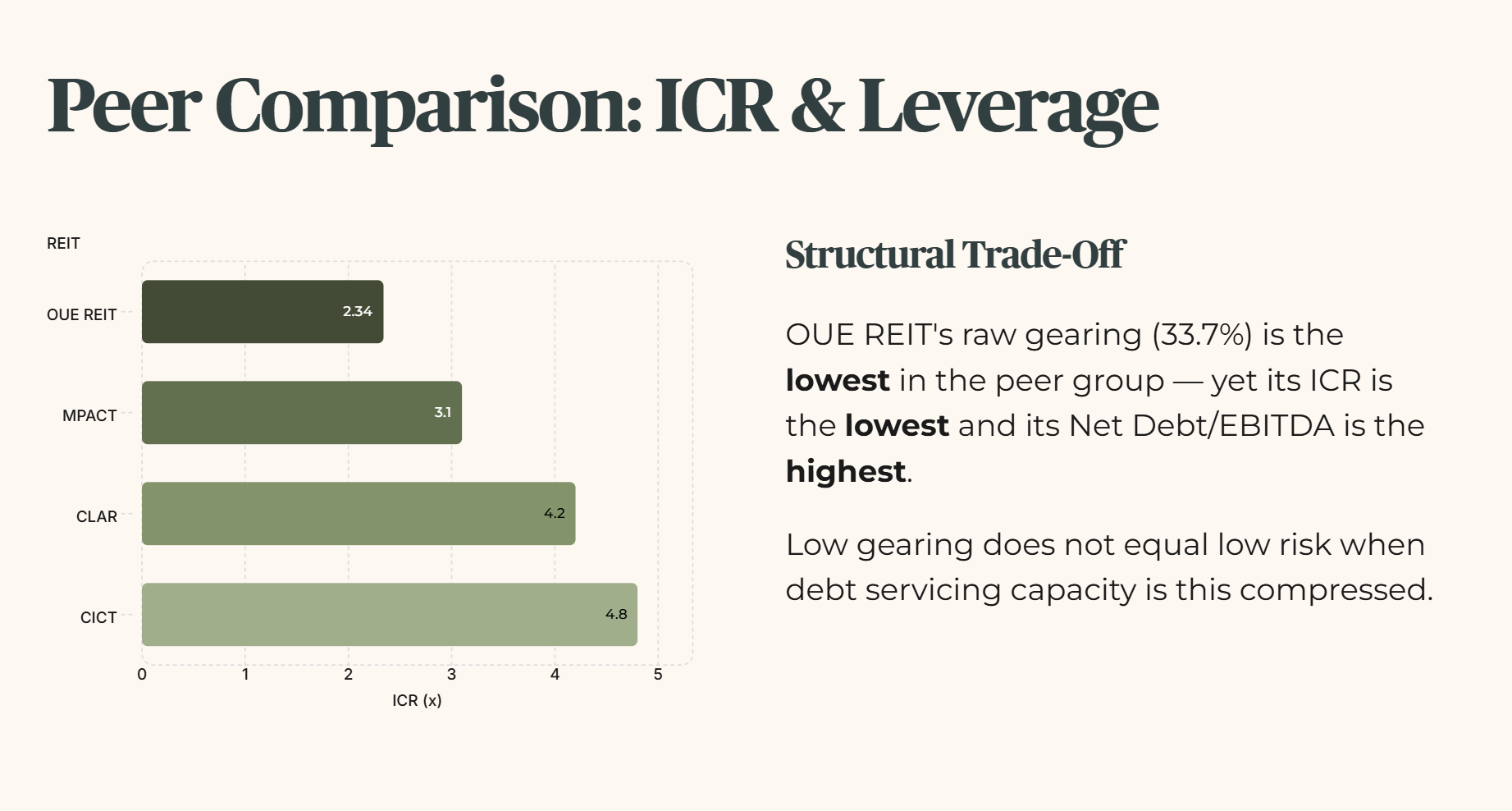

Layer 3 — Peer Context: When placed directly alongside prime SGX commercial and industrial peers like CapitaLand Integrated Commercial Trust (CICT), CapitaLand Ascendas REIT (CLAR), and Mapletree Pan Asia Commercial Trust (MPACT), a clear structural trade-off emerges. OUE REIT displays the lowest interest coverage and the highest leverage multiple among the group, even though its raw gearing ratio remains the lowest.

Layer 4 — Forward Scenario: If macro conditions shift and net property income drops by 10% due to prolonged vacancy during the sub-division process, an ICR of 2.34x leaves almost no operational insulation. Any further increase in refinancing costs would push the coverage ratio dangerously close to critical levels, risking structural capital distribution constraints.

Layer 5 — Wallet Impact: For a 55-year-old Singaporean investor relying on predictable quarterly distributions to fund personal cost-of-living requirements, an asset with restricted interest coverage means the headline income stream is inherently fragile. The balance sheet lacks the structural equity buffer required to safeguard the dividend if the operational turnaround faces delays.

Financial Health Checklist

Weighted Soft Flag Assessment

ICR Trending Downward Toward Floor: Present. The structural compression of interest coverage underneath prevailing refinancing rates constitutes a severe operational headwind. MAJOR, 1.0.

Trading Above InvestingPro Fair Value: Not yet assessable. An independent fair value benchmark is not available through current data sources pending further disclosure.

Sponsor Top-Ups Present in NPI: Absent. Gross rental income streams do not indicate artificial net property income engineering or transient sponsor income support mechanisms. 0.0.

Gearing Trending Upward Quarter-on-Quarter: Absent. Total aggregate debt relative to deposited property value remains stabilized within standard operating parameters. 0.0.

Single-Market Concentration Above 70%: Not yet assessable. A comprehensive geographical breakdown across global asset stakes awaits updated disclosures.

Weighted Soft Flag Total: 1.0

Section 3 — The Dividend Trajectory

Evaluating the forward durability of OUE REIT distributions requires analyzing the relationship between current cash flows and upcoming leasing vacancies. Because the H1 2026 financial statement publication is scheduled for 22 July 2026, the trailing metrics must be treated as estimates anchored to the verified historical base.

Dividend Trajectory

The core challenge facing the distribution trajectory is a timing mismatch between capital outflows and income collection. Even if the analyst’s base case proves entirely correct and management eventually achieves an annualized rental rate of S$10 per square foot on the components of the sub-divided Deloitte space, the physical execution of dividing 150,000 square feet requires material capital expenditure.

During the multi-month period dedicated to configuration changes, marketing initiatives, and tenant fit-outs, the asset generates no organic revenue from those floors. When this vacancy phase is combined with the structural loss of income resulting from the Crowne Plaza Changi Airport divestment, the cushion protecting the dividend narrows significantly. If net property income falls temporarily during the asset turnaround, the compressed interest coverage ratio means cash must be retained to service debt obligations, creating immediate downward pressure on the distribution run-rate.

The compressed interest coverage ratio of 2.34x and the capital outlay required to reconfigure 150,000 square feet set up the next section’s forensic step, where we quantify how this stresses the retirement-grade dividend safety under Iggy’s 4.7% yield and 4.0x ICR standards.