DCA vs Lump Sum: What's Smarter for Singapore Investors?

Stop DCA on autopilot—use seven clear triggers to go faster, cut cash drag, and maximise CPF/SRS compounding without taking dumb risk

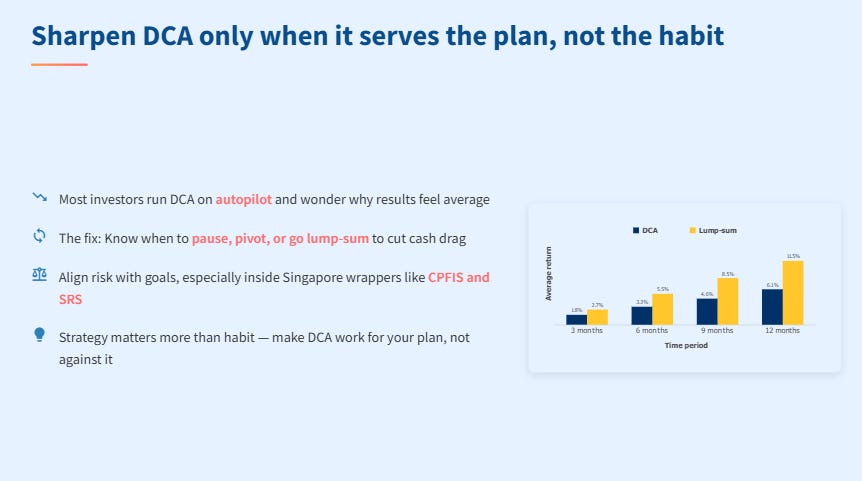

Most investors stick to dollar-cost averaging (DCA) without thinking about whether it still fits their situation. It’s easy to fall into autopilot, adding the same amount each month, hoping slow and steady wins the race. But following a routine just for the sake of it can hold you back—especially if your plan, life, or the market has changed. This guide shows you how to make DCA work smarter. You’ll learn when to speed up, go all-in, or pause your investing based on your goals and Singapore-specific options like CPFIS and SRS. The real goal is matching your approach to your needs—not just copying a habit—so your strategy serves you, not the other way around.

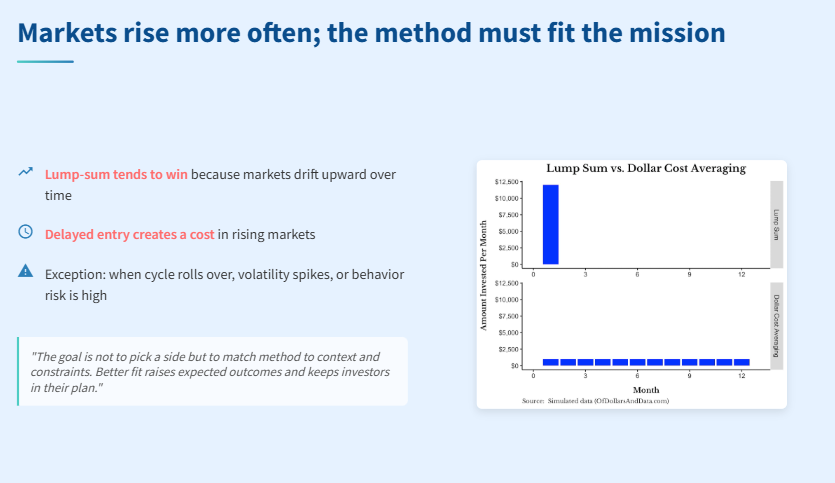

Markets rise more often; the method must fit the mission

Most days, the market quietly crawls upwards, a bit like an iguana chilling in the sun. If you sit on your pile of cash, waiting for the “perfect” time to jump in, you might wait forever—like a lizard hoping for rain on a hot Orchard Road afternoon.

Dropping a lump sum into the market gets your money growing faster. Compounding kicks in straight away, which is like planting your seeds at the start of the rainy season—lots of time for things to grow! But sometimes, dark clouds gather—markets turn choppy, or you feel uneasy. When that happens, slowing down with dollar-cost averaging (DCA) can help you avoid big bites from the storm.

Just remember: don’t pick a style because the crowd is doing it. Ask yourself—what’s the financial weather in your own life? Think about your goals, how you’re investing (your wrappers, like SRS or CPF), and how much risk you can take without losing sleep.

The whole point? Find what fits you. That way, you stay cool when the market heats up, your returns look better in the long run, and you don’t end up running for cover at the wrong time.