Mapletree DPU Crisis: 3 Yield Traps vs. 1 "Fortress" Buy

REIT dividends are hitting your account this month, but DPU is shrinking. Here’s how to tell if you should buy more or stay away.

December is here. That means holiday shopping, year-end planning, and for Singapore REIT investors, dividend payouts landing in your CDP account. The Mapletree trio and Frasers Logistics are all writing cheques this month.

But there is a catch. Distribution per Unit (DPU) is under pressure. Interest costs are eating into your payouts faster than rental reversions can make up for them.

If you have been watching your REIT portfolio, you might feel frustrated. You see the share prices down significantly from their 2021 highs. You see the DPU numbers flat or dropping. You wonder if you should cut losses or double down to lower your average price.

I get it. I have been analyzing Singapore REITs through three rate cycles. The signals are mixed—prices are cheap, but debt is expensive. But mixed signals do not mean no signals. Let me walk you through what the numbers really tell us about the checks you are receiving this month.

In This Article:

• The Mapletree Trio vs. Frasers: The Tale of the Tape

• The Interest Rate Squeeze

• Valuation: Value Trap or Bargain Bin?

• The Verdict: Iggy’s Action Plan

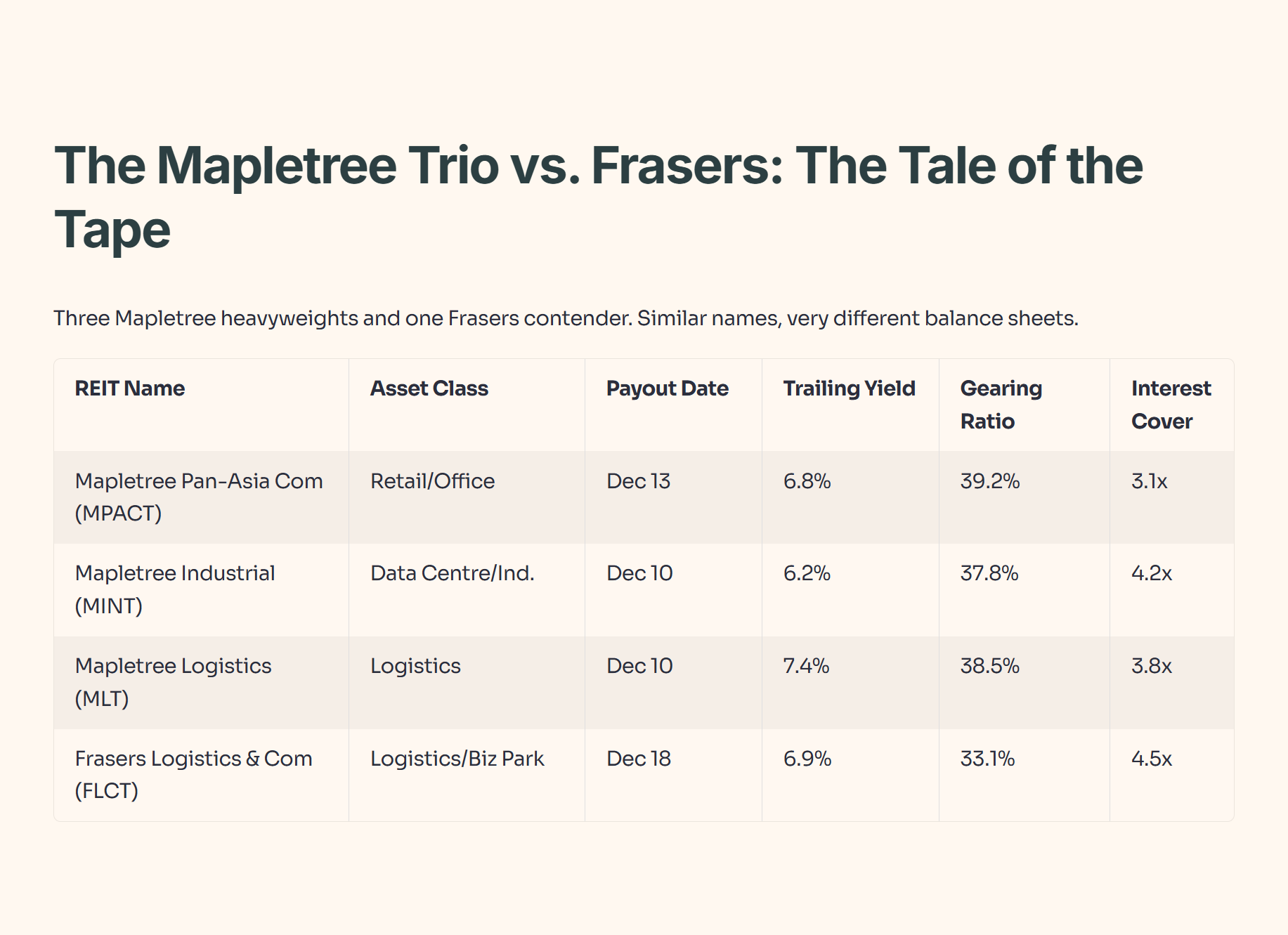

• The Bottom Line: Don’t Compound a MistakeThe Mapletree Trio vs. Frasers: The Tale of the Tape

Let us start with the raw data. We have three Mapletree heavyweights and one Frasers contender paying out this month. They sound similar, but their balance sheets tell very different stories.

Table 1: December 2025 Payout & Financial Health Snapshot

Iggy’s Insight:

Do not let the “Mapletree” brand name lull you into a false sense of security. While the sponsor is strong, the debt profiles are deteriorating. Notice the Interest Cover for MPACT is down to 3.1x. That is dangerously close to the comfort line. Conversely, FLCT has a gearing of just 33.1%. In a “higher-for-longer” environment, low gearing isn’t just a safety buffer; it is ammunition for acquisitions. FLCT can buy distressed assets; MPACT is busy trying to fix its own balance sheet.

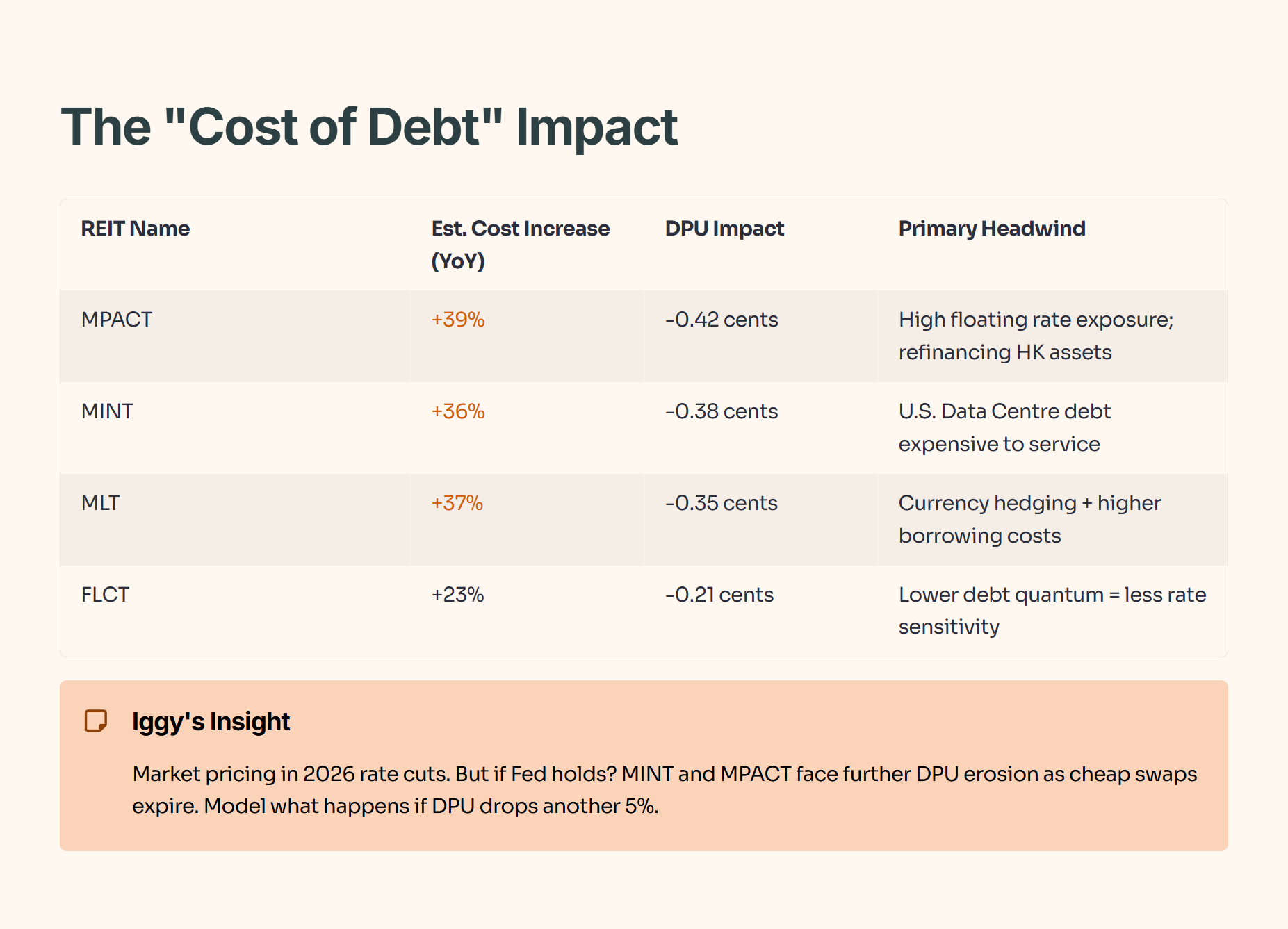

The Interest Rate Squeeze

Why is your DPU shrinking? It is simple math. REITs borrow money to buy properties. When rates go up, interest expense goes up.

The REITs that hedged poorly—or those with hedges rolling off right now—are feeling the pain. Below is the estimated impact of rising interest costs on the DPU for this quarter compared to last year.

Table 2: The “Cost of Debt” Impact

Iggy’s Insight:

The market is currently pricing in rate cuts for 2026. But what if the Fed holds? If rates stay at current levels for another 12 months, MINT and MPACT will see further DPU erosion as cheap swaps expire. You cannot just look at the trailing yield of 6.8%; you have to model what happens if the DPU drops another 5%.

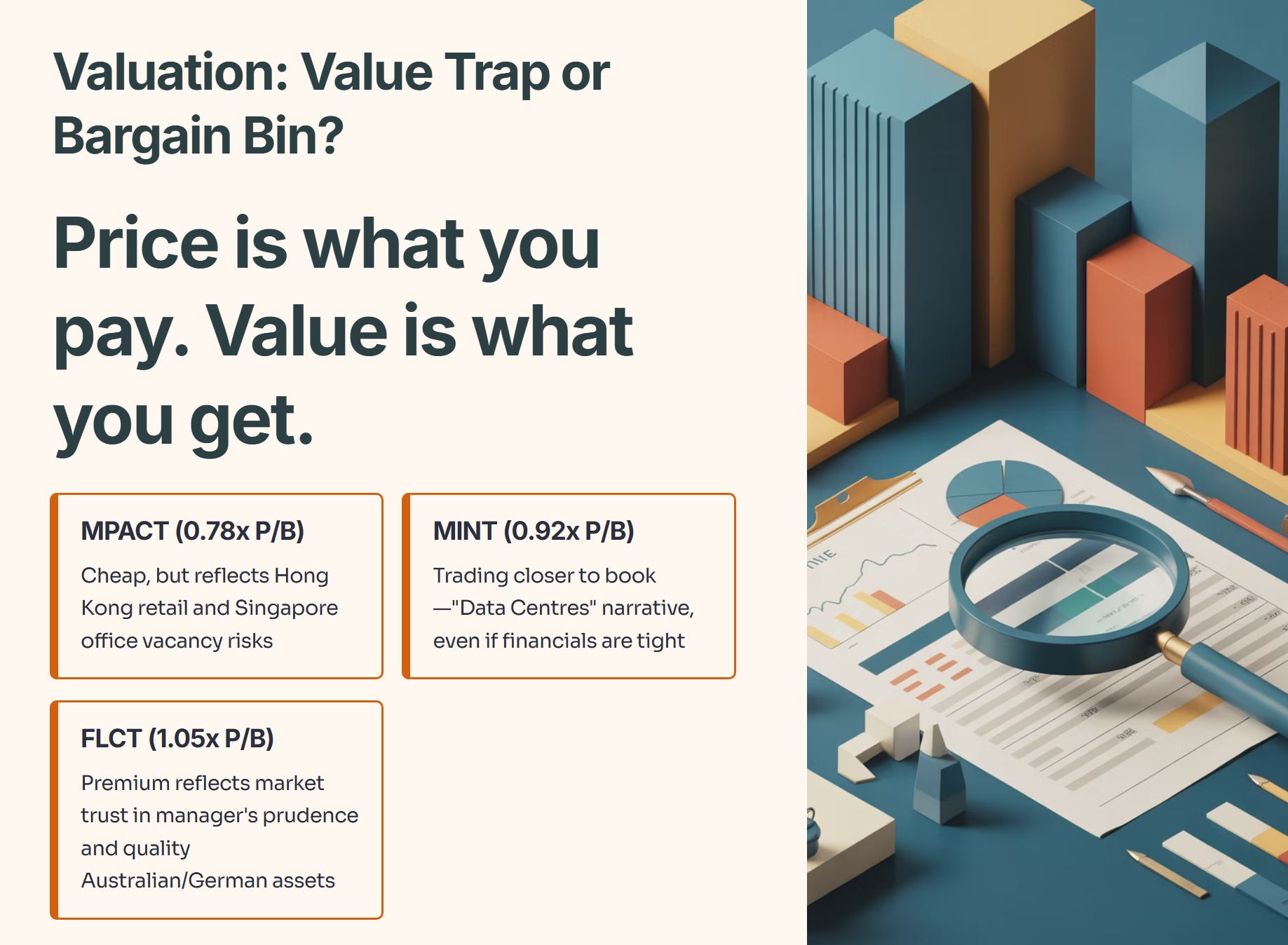

Valuation: Value Trap or Bargain Bin?

Price is what you pay. Value is what you get.

Currently, the Mapletree trio is trading at discounts to book value (P/B < 1.0), while Frasers is trading at a slight premium or par. New investors often make the mistake of buying the biggest discount.

MPACT (0.78x P/B): Cheap, but reflects the risk of Hong Kong retail and Singapore office vacancies.

MINT (0.92x P/B): Trading closer to book because “Data Centres” are a sexy narrative, even if the financials are tight.

FLCT (1.05x P/B): The premium exists because the market trusts the manager’s prudence and the quality of the Australian/German assets.

But don’t just take my word for it. Let’s look at the institutional models.

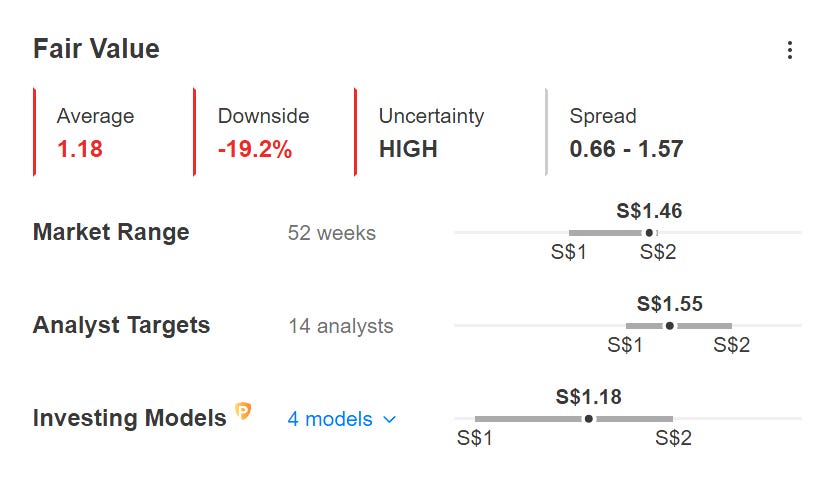

Here is the Fair Value analysis from InvestingPro for Mapletree Pan Asia Commercial Trust (MPACT).

Chart: MPACT’s Fair Value Estimate. Source: InvestingPro (I use this tool to fact-check my REITs. Get up to 50% off with code INVESTINGIGUANA).

According to InvestingPro’s Fair Value model (which averages 4 financial models), the intrinsic value is only S$1.18.

Compare that to the current market price of S$1.46, and the model suggests a significant 19.2% downside risk.

This confirms my fear: The stock isn’t just facing headwinds; it is potentially overpriced relative to its fundamentals. The market hasn’t fully priced in the risks yet.

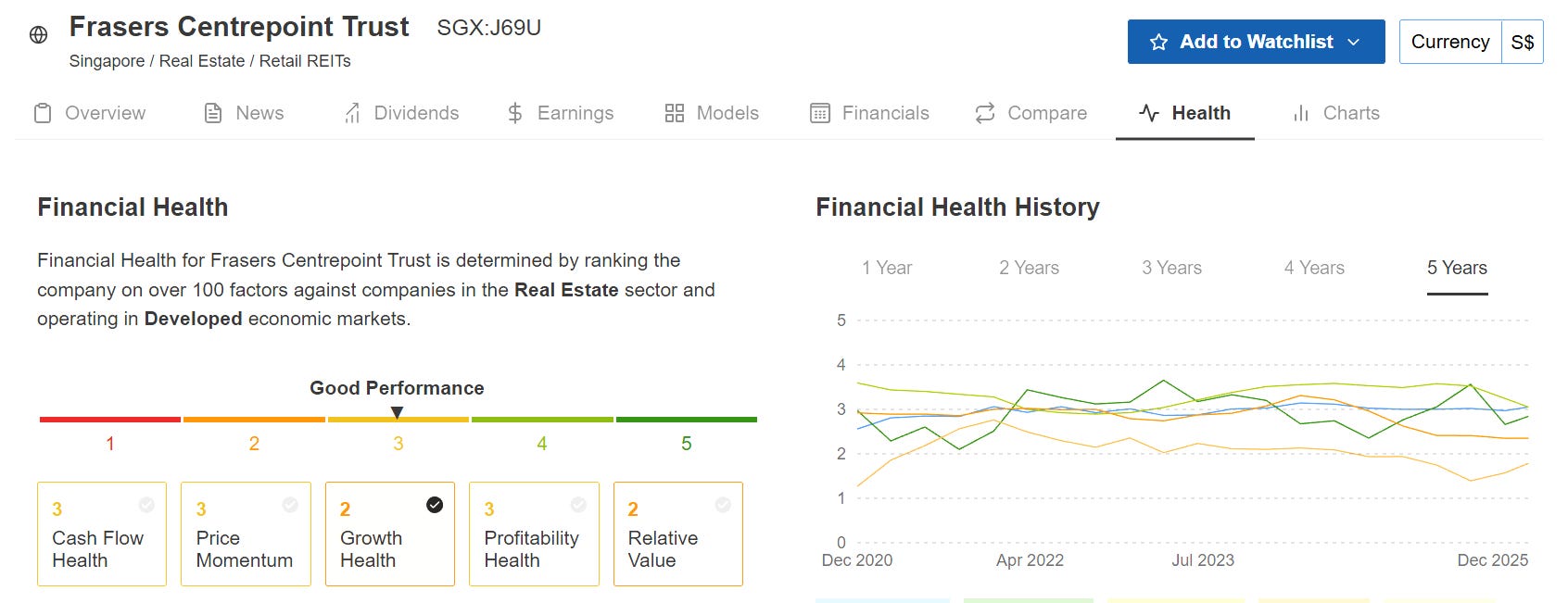

I call FLCT a ‘Core’ holding for a reason. Look at this Financial Health history from InvestingPro.

Source: InvestingPro Financial Health Score. (Data as of Dec 2025. Premium members can use code INVESTINGIGUANA for up to 50% off).

See that steady Green line? That represents Profitability Health. For 5 years, through COVID and interest rate hikes, FLCT has maintained strong profitability scores. While other REITs are seeing their health scores degrade, FLCT remains a fortress. That consistency is what lets me sleep at night.”*

Iggy’s Insight:

I view MPACT as a potential “Value Trap” for the impatient investor. A discount to book value only matters if the book value is accurate. With Hong Kong capitalization rates expanding (meaning property values are falling), MPACT’s book value is likely to be written down further. You aren’t buying a dollar for 78 cents; you are buying a shrinking dollar.

The Verdict: Iggy’s Action Plan

You want clear calls? Here is how I am positioning my own portfolio and what I suggest for your SRS and Cash holdings.