UOB: Why I Changed My Mind (And My New $32 Buy Zone)

The Kitchen-Sink Quarter: Decoding the 72% Profit Crash and Why the ‘Smart Money’ is Moving to the Sidelines

Decoding UOB’s Fair Value Flip: Why My Target Changed in 72 Hours

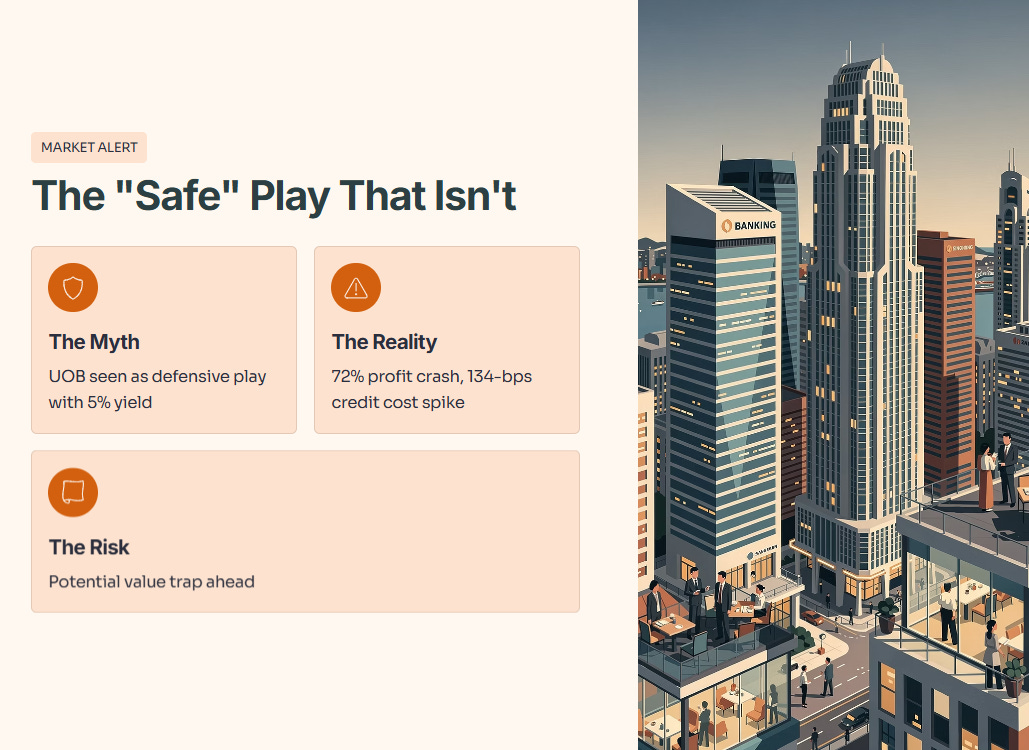

Everyone thinks UOB is the “safe” defensive play among Singapore’s Big Three. They look at the 5% yield and the bank’s historic resilience and sleep soundly. They’re wrong. The market just performed a violent recalibration of UOB’s fair value, and if you aren’t looking at the 72% profit crash and the 134-basis-point credit cost spike, you’re flying blind into a potential “value trap”.

Personal Note: If you’ve followed my portfolio for a while, you know I used to be heavily optimized toward UOB for its ASEAN growth story. But lately, I’ve become much more cautious. I’m not here to be a cheerleader for any stock; I’m here to protect capital. When the data changes—like it did this past quarter—my recommendation must change. This isn’t inconsistency; it’s risk management.

In This Article:

• About Iggy the Investing Iguana channel

• The Iggy Audit: The Post-Earnings Recalibration

• The Three Structural Headwinds for 2026

• The InvestingPro Data Check: Removing the Bias

• Peer Comparison: Why UOB Looks the "Weakest"

• The Verdict: The 2026 Action Plan

• Why I Changed My Mind: From Optimist to SkepticAbout Iggy the Investing Iguana channel

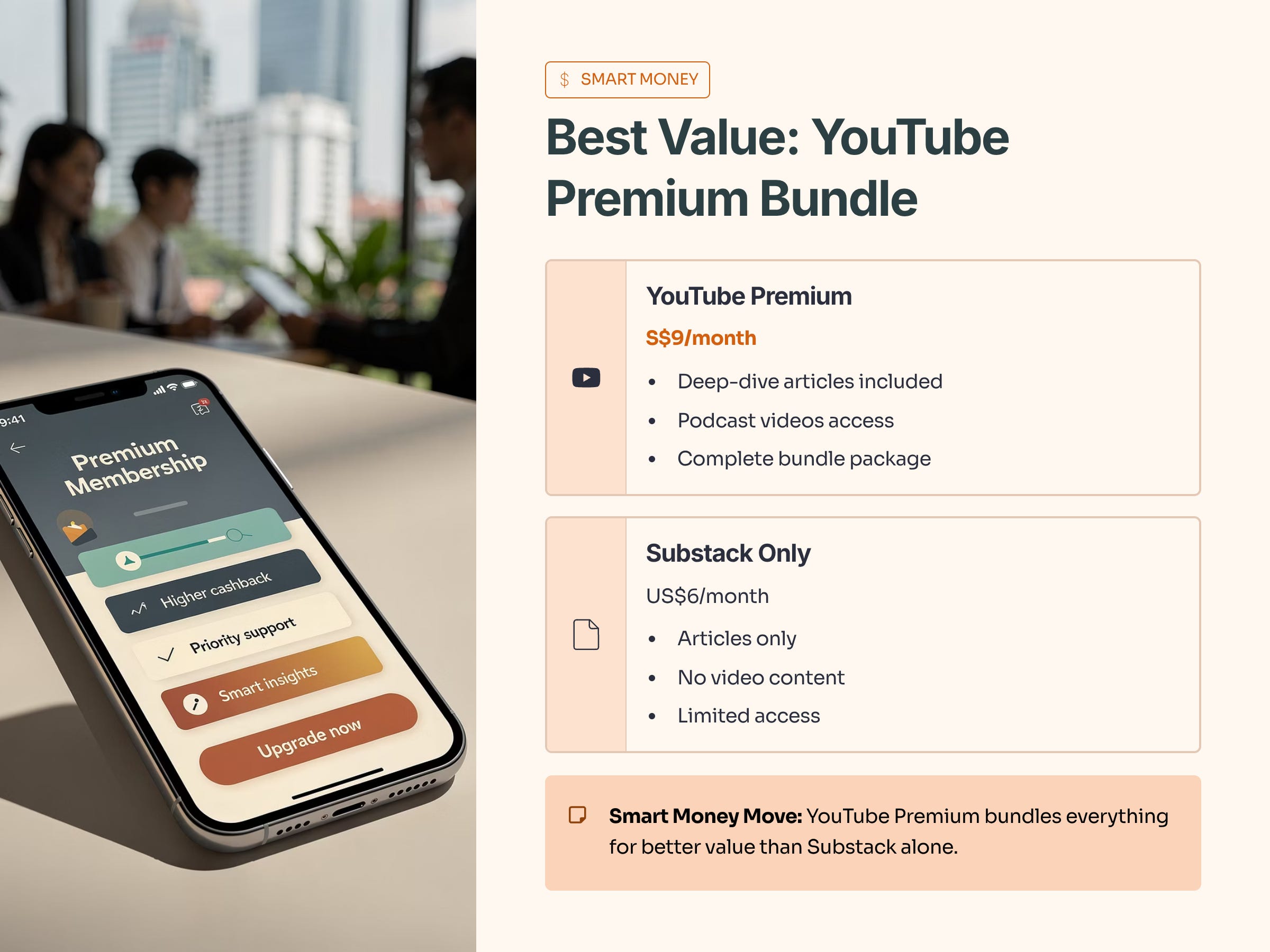

If you’re new here, welcome. I’m Iggy, your Singapore-based market analyst. Since October 2025, we’ve produced over 1,300 videos and 400 articles with 1.1 million watch hours. We are also home to a growing community of over 5,300 subscribers and an ‘Inner Circle’ of 100+ paid members across YouTube and Substack.

Quick Housekeeping: If you want the best value, the YouTube Premium Membership (S$9/mth) bundles these deep-dive articles with the podcast videos. Substack alone is US$6, so the bundle is the ‘smart money’ move. Now, let’s get to the numbers.

The Iggy Audit: The Post-Earnings Recalibration

The recent shift in UOB’s target price wasn’t a sudden mood swing; it was a mathematical necessity after the bank’s Q3 2025 results revealed a balance sheet under significant pressure compared to its record-breaking peers.

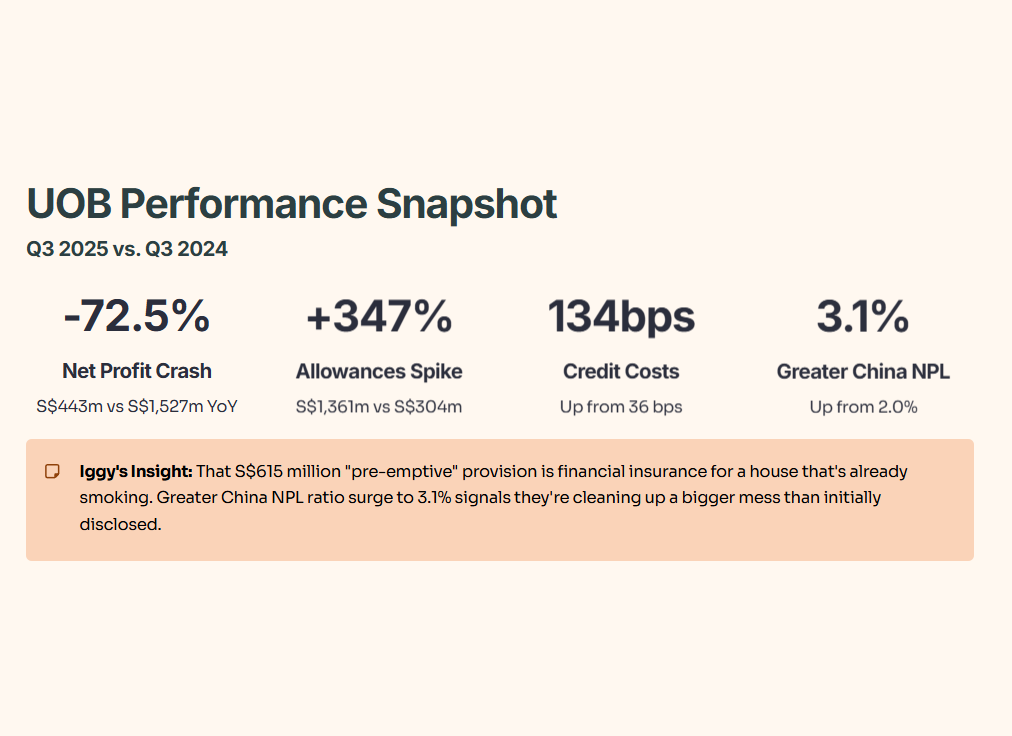

UOB Performance Snapshot (Q3 2025 vs. Q3 2024)

💡 Iggy’s Insight: That S$615 million “pre-emptive” provision is what I call “financial insurance” for a house that’s already smoking. While management claims they are “strengthening resilience”, the fact is their Greater China non-performing loan (NPL) ratio has surged to 3.1%. They aren’t just being cautious; they are cleaning up a mess that’s bigger than initially disclosed.

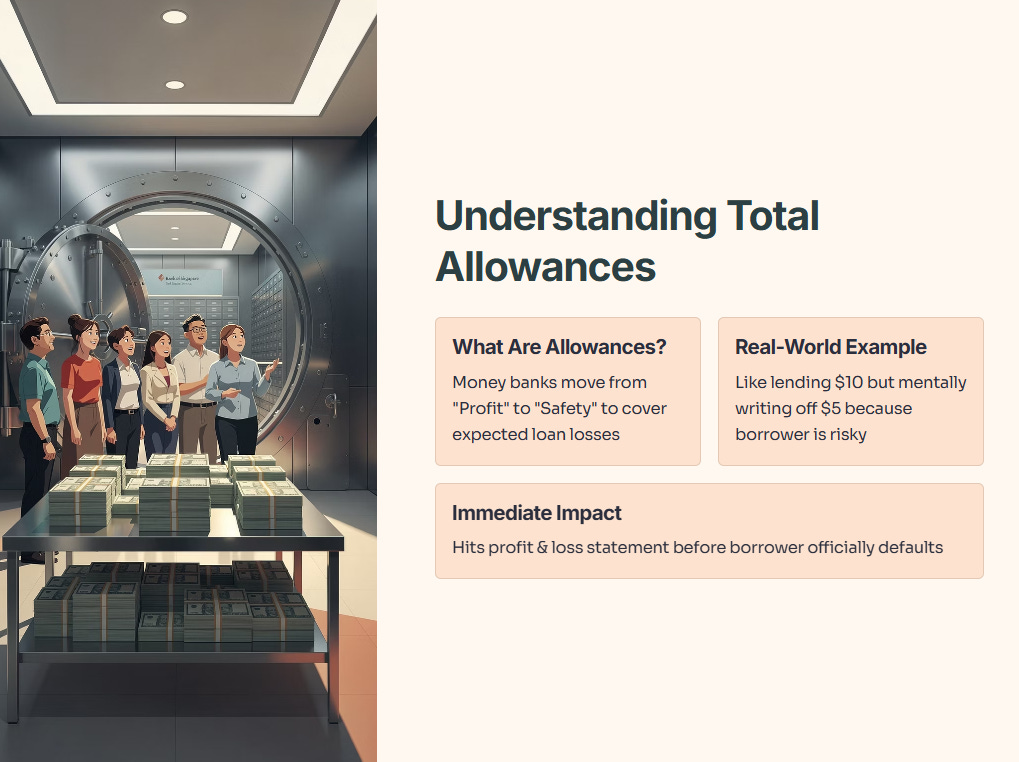

Understanding “Total Allowances” and Credit Costs

Before going further, it helps to slow down on one critical term that appears in every bank result: Total Allowances or Provisions. When a bank lends money, it expects to get the principal and interest back, but some borrowers will struggle or fail, so the bank moves part of its profit into a “safety” bucket to prepare for those losses. This is like lending a friend ten dollars while already assuming in your head that five dollars is gone because you know he is bad with money; that five dollars is the provision, and it hits the profit and loss statement today even if he has not officially defaulted yet.

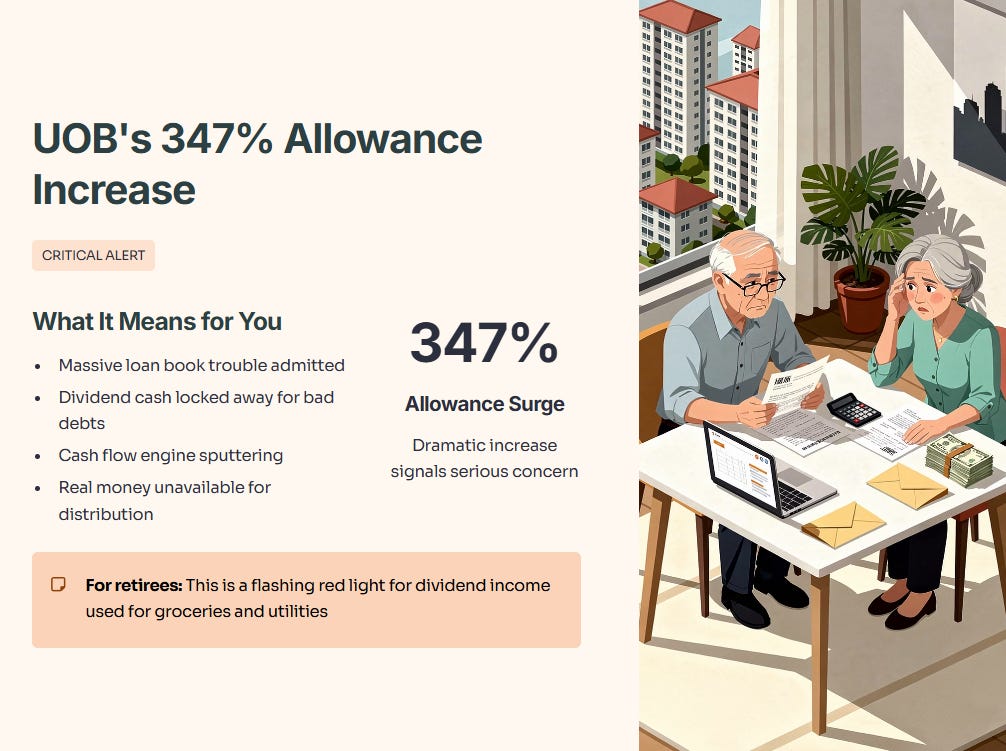

So when UOB increases its allowances by 347%, it is not just shifting numbers between lines on an accounting spreadsheet. It is the bank admitting that a much larger slice of its loan book is now at risk, and cash that could have supported dividends or reinvestment is being locked away to cover bad debts. For a Singaporean retiree using bank dividends to fund groceries or utility bills, this is a flashing red light, because it means the cash flow engine of the bank is sputtering and less real cash is available for distribution.

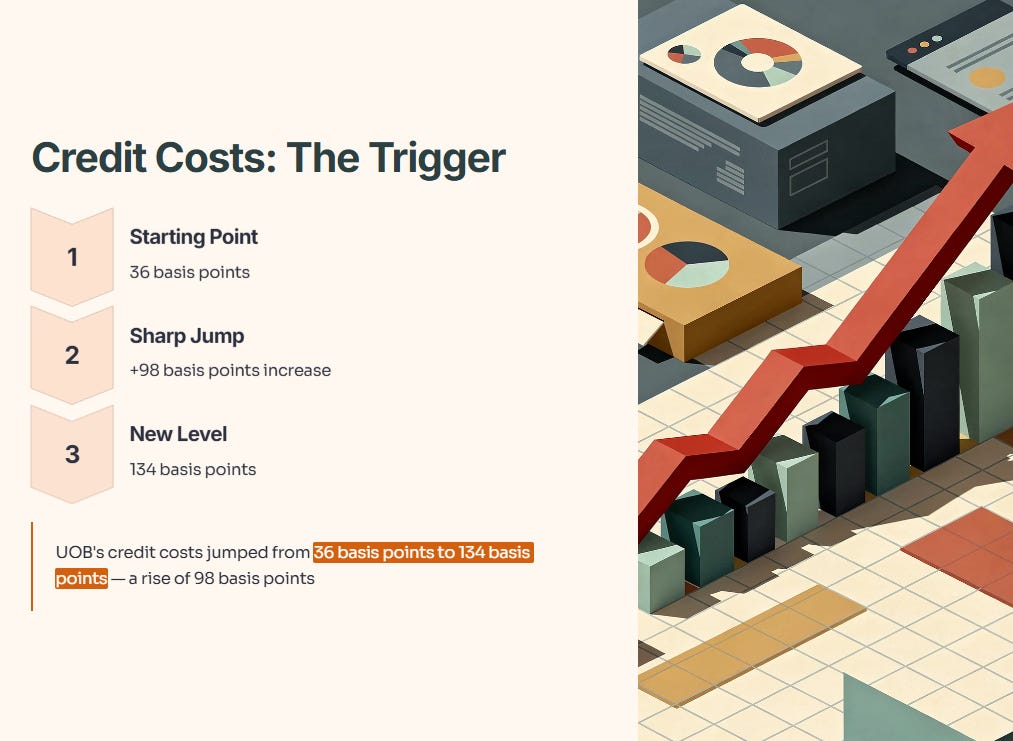

The technical label for this pain is Credit Costs. UOB’s credit costs jumped from 36 basis points to 134 basis points, which is a rise of 98 basis points in a single year and a clear sign that the bank is paying much more to insure against bad loans. In simple terms, every extra basis point of credit cost is money that used to flow cleanly to shareholders but is now being rerouted into a buffer against future defaults.

The Three Structural Headwinds for 2026

The China Property Albatross: According to regulatory filings, UOB’s Hong Kong branch had over HK$69.2 billion (S$11.5 billion) in property-related loans as of June 2025, representing 43% of the branch’s gross loans. As real estate prices in the region sink—with office units down 50% from peaks—these assets are becoming lead weights.

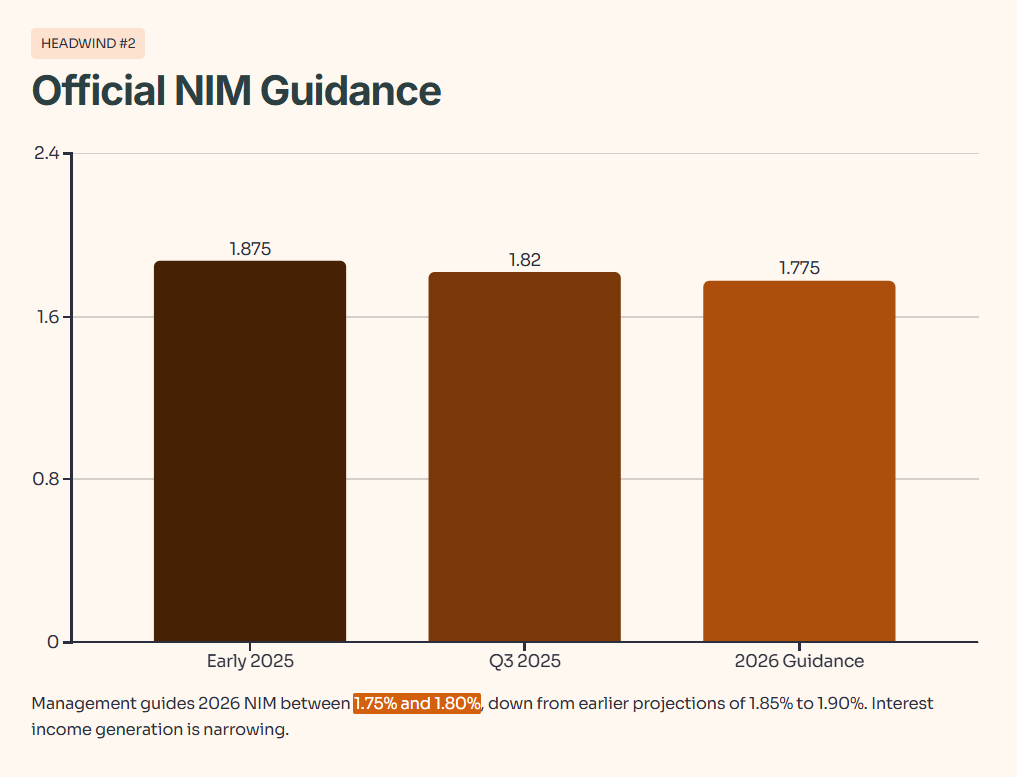

Official NIM Guidance: Management has officially guided that 2026 NIM will likely range between 1.75% and 1.80%, down from earlier 2025 projections of 1.85% to 1.90%. As global rates ease, UOB’s ability to generate interest income is narrowing.

Credit Cost “Normalisation”: While UOB expects credit costs to fall back to 25-30 basis points in 2026, this assumes no further deterioration in US or China commercial real estate. If the property market doesn’t floor, these “normalised” targets could be overly optimistic.

The InvestingPro Data Check: Removing the Bias

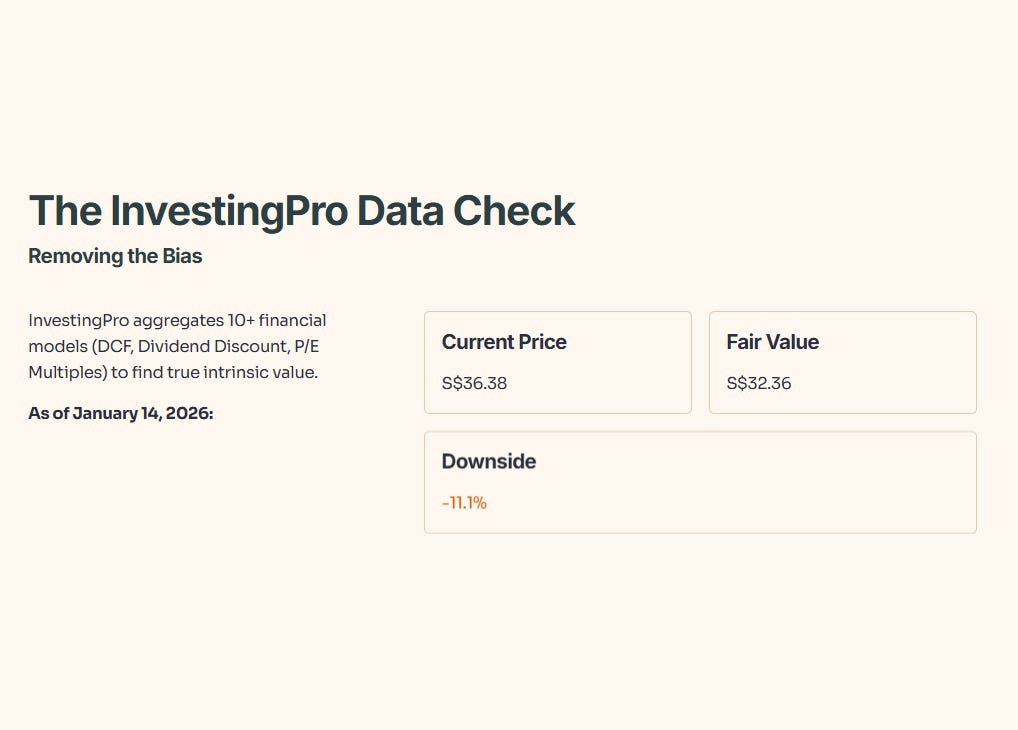

I don’t guess at valuations using a napkin calculation. I check the InvestingPro Fair Value Model. Why is this powerful? Because it doesn’t rely on one opinion; it aggregates 10+ distinct financial models (DCF, Dividend Discount, P/E Multiples) to remove human bias and find the true intrinsic value.

As of January 14, 2026, the InvestingPro data for UOB (SGX:U11) shows:

Current Price: S$36.38

InvestingPro Fair Value: S$32.36

Downside Potential: -11.1%

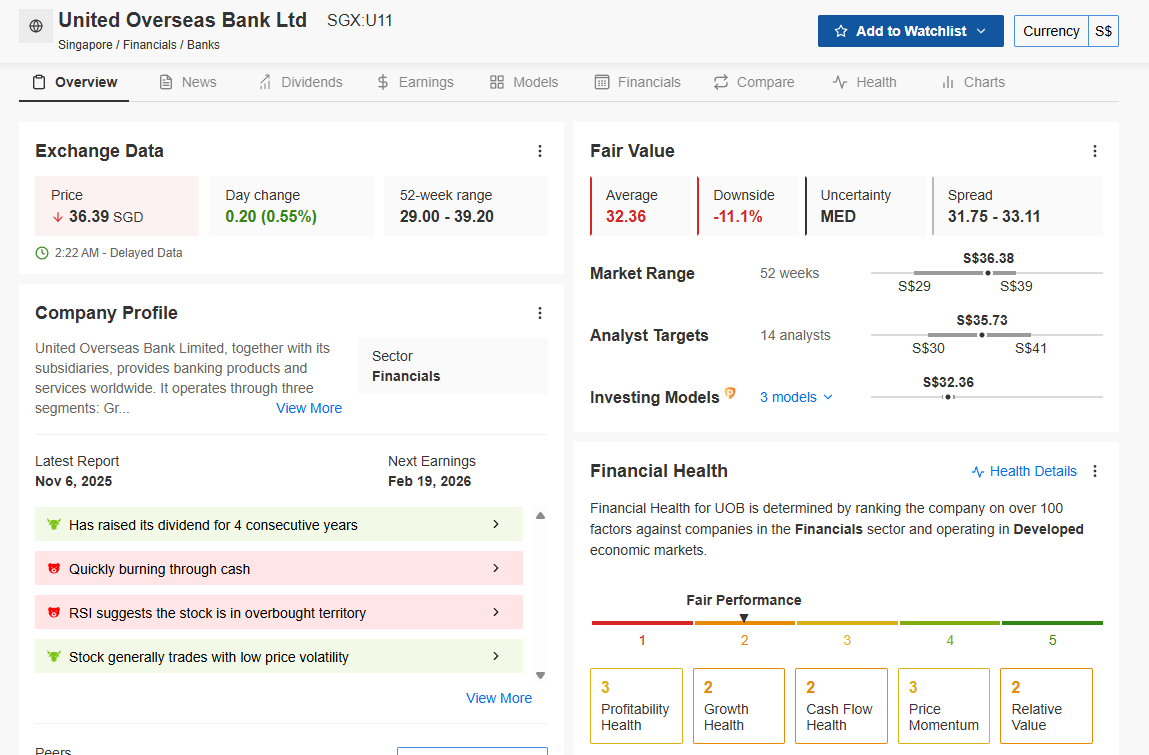

Financial Health Score: 2 / 5 (Fair Performance)

Source: InvestingPro data. Unlock these institutional tools for yourself: Use code INVESTINGIGUANA for an exclusive 55% discount to kickstart 2026.

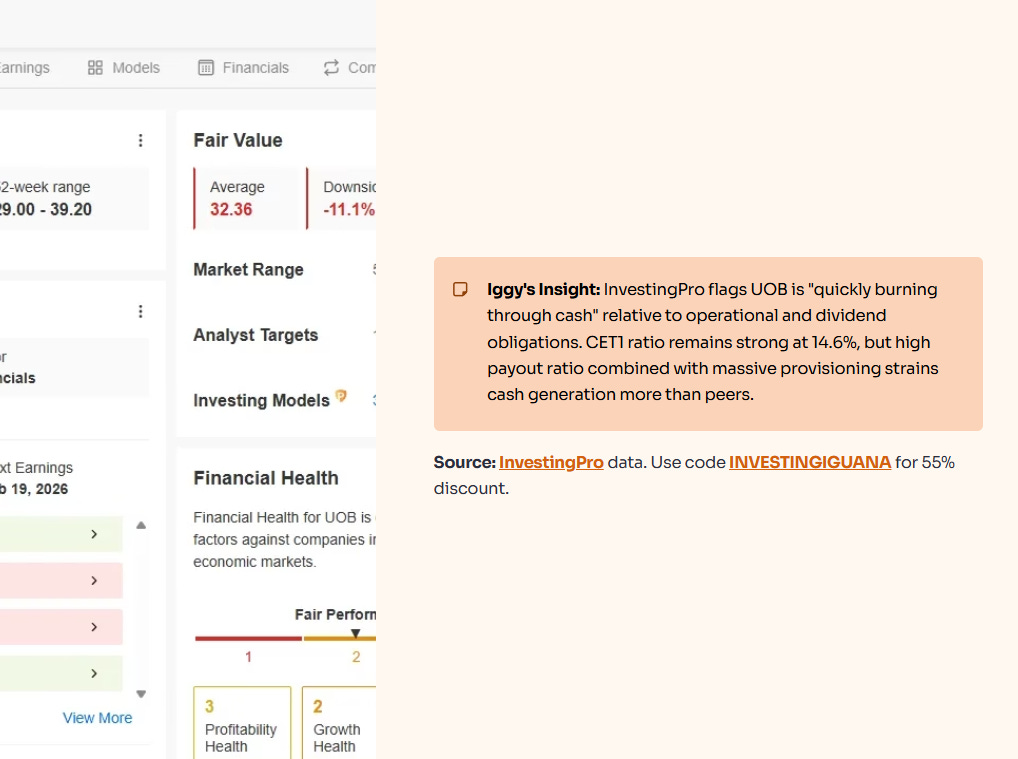

💡 Iggy’s Insight: InvestingPro currently flags that UOB is “quickly burning through cash” relative to its operational and dividend obligations. While UOB remains well-capitalised with a CET1 ratio of 14.6%, this warning signals that the high payout ratio combined with massive provisioning is straining cash generation more than its peers.

Source: InvestingPro data. Unlock these institutional tools for yourself: Use code INVESTINGIGUANA for an exclusive 55% discount to kickstart 2026.

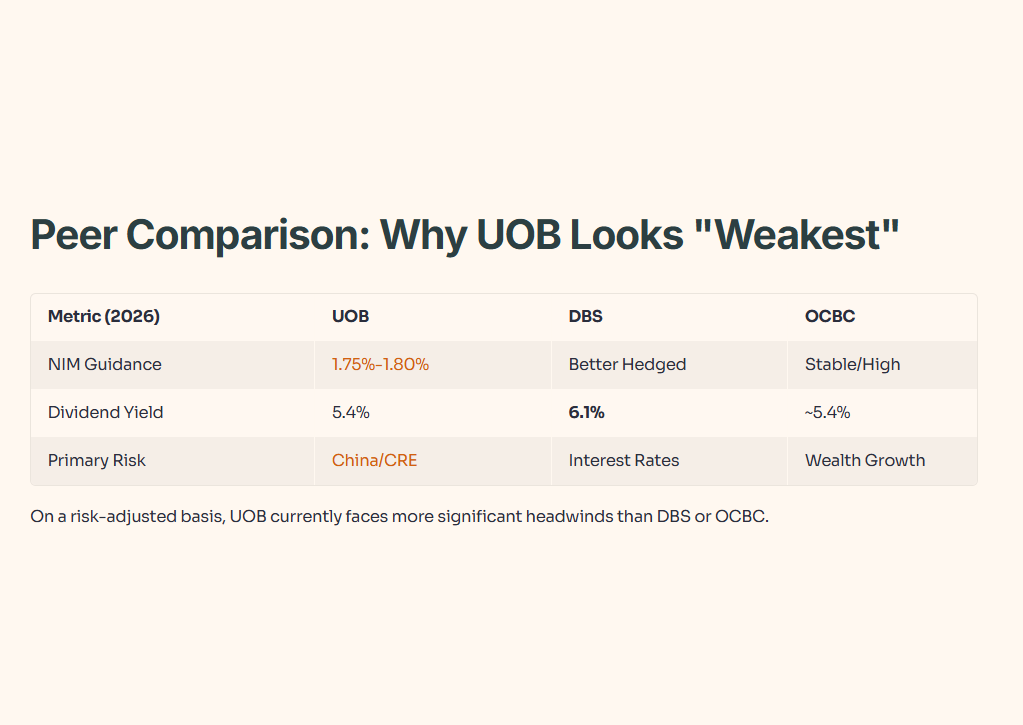

Peer Comparison: Why UOB Looks the “Weakest”

On a risk-adjusted basis, UOB currently faces more significant headwinds than DBS or OCBC.

The Verdict: The 2026 Action Plan