Is DFI a Yield Trap? The Truth Behind the Asset Sales & 70% Payout

Why dumping Cold Storage might be the smartest move DFI ever made—and what the new 15% growth target means for your passive income portfolio.

The Hook: Shrinking to Grow?

If you live in Singapore, you’ve noticed the shift. The Cold Storage at your local mall might have changed hands, and the Giant hypermarket that used to dominate the basement is facing an uncertain future. For the average observer, DFI Retail Group (SGX: D01) looks like a company in retreat. They sold their Singapore food business—icons like Cold Storage and Giant—to Macrovalue for S$125 million.

To the uneducated investor, selling revenue-generating assets looks like weakness. But if you care about your dividend yield and capital preservation, this might be the most bullish signal we’ve seen in years.

DFI just announced a massive strategic overhaul: a hike to a 70% dividend payout ratio and a target of 11-15% profit growth through 2028. The stakes are high. If they execute, this is a dividend aristocrat in the making. If they fail, it’s a classic value trap. Let’s look at the numbers the market is ignoring.

In This Article:

• The Hook: Shrinking to Grow?

• The Surgery: Cutting the Fat to Save the Patient

• The Dividend Plan: Is the 70% Payout Real?

• The “InvestingPro” Data Check: Health vs. Hype

• Part A: The Dividend “Red Flag” That Isn’t

• Part B: The Health Score Reality Check

• The Growth Plan: 15% CAGR or Pipe Dream?

• The Investor’s Playbook: How to Trade DFI

The Surgery: Cutting the Fat to Save the Patient

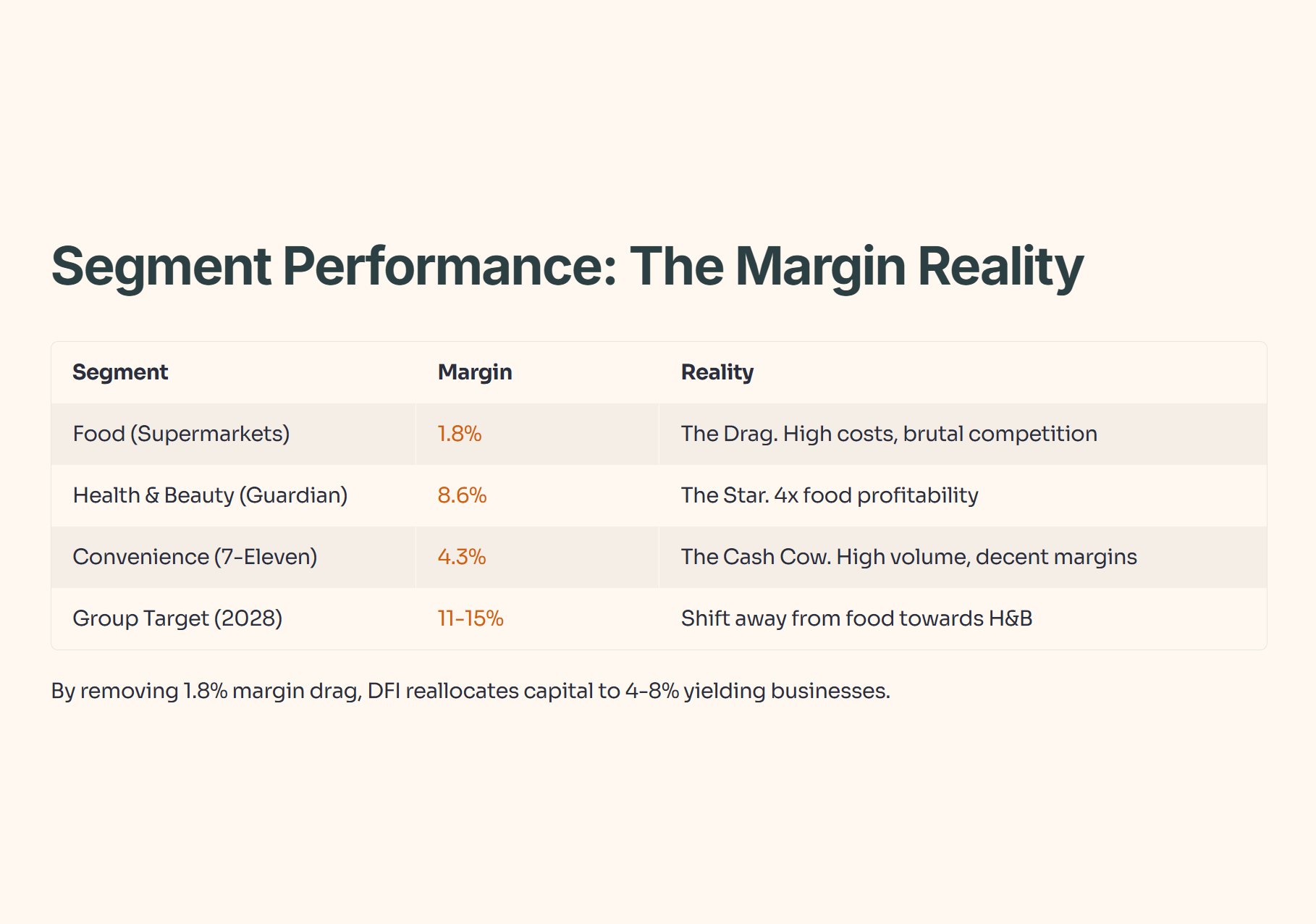

Why did DFI sell its Singapore food business? It wasn’t just about cash; it was about margin physics. In 2024, the food business was a drag on the entire group.

While underlying profit for the group jumped 30% to US$201 million, the food division was fighting for scraps with a razor-thin 1.8% operating margin. Contrast that with Health & Beauty (Guardian) and Convenience (7-Eleven).

DFI Segment Performance & Margin Reality (2024)

By selling the Singapore food operations, DFI isn’t losing money; they are stopping the bleeding. They are reallocating capital from a 1.8% margin business to businesses yielding 4-8%.

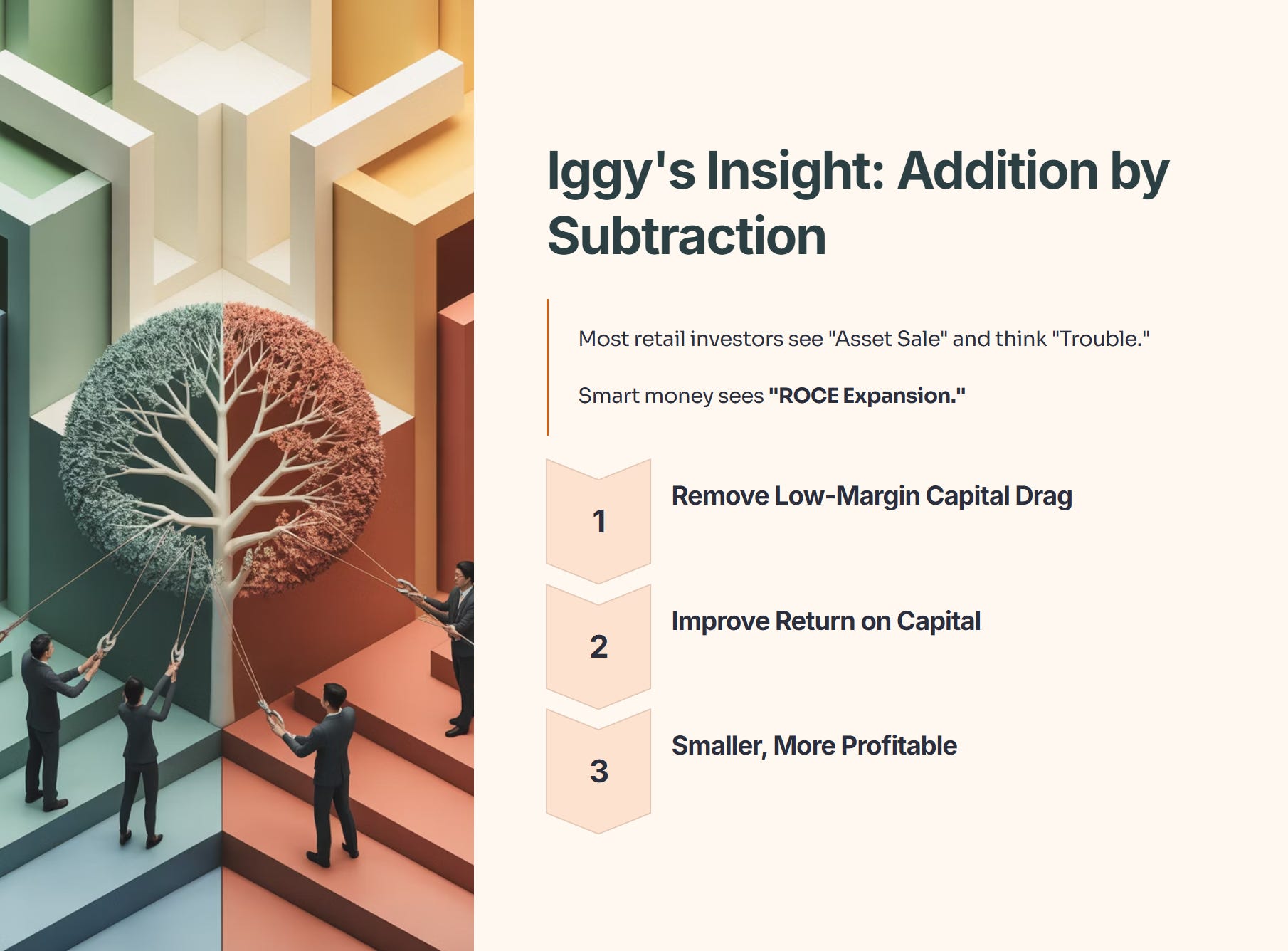

Iggy’s Insight:

Most retail investors see “Asset Sale” and think “Trouble.” Smart money sees “ROCE Expansion.” By removing the low-margin capital drag of Singapore supermarkets, DFI automatically improves its Return on Capital Employed. I’d rather own a smaller, highly profitable company than a massive, inefficient one. This is addition by subtraction.

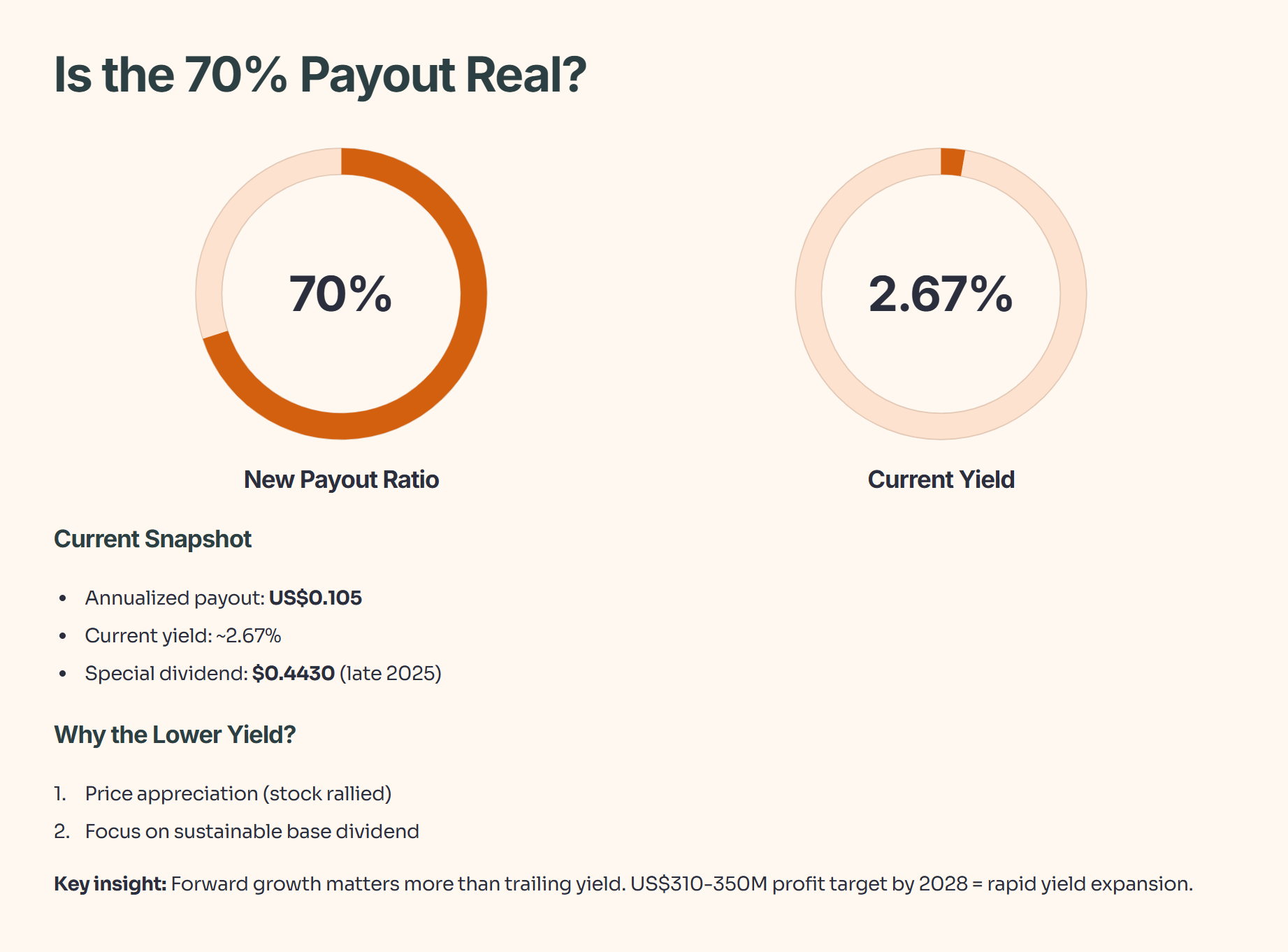

The Dividend Plan: Is the 70% Payout Real?

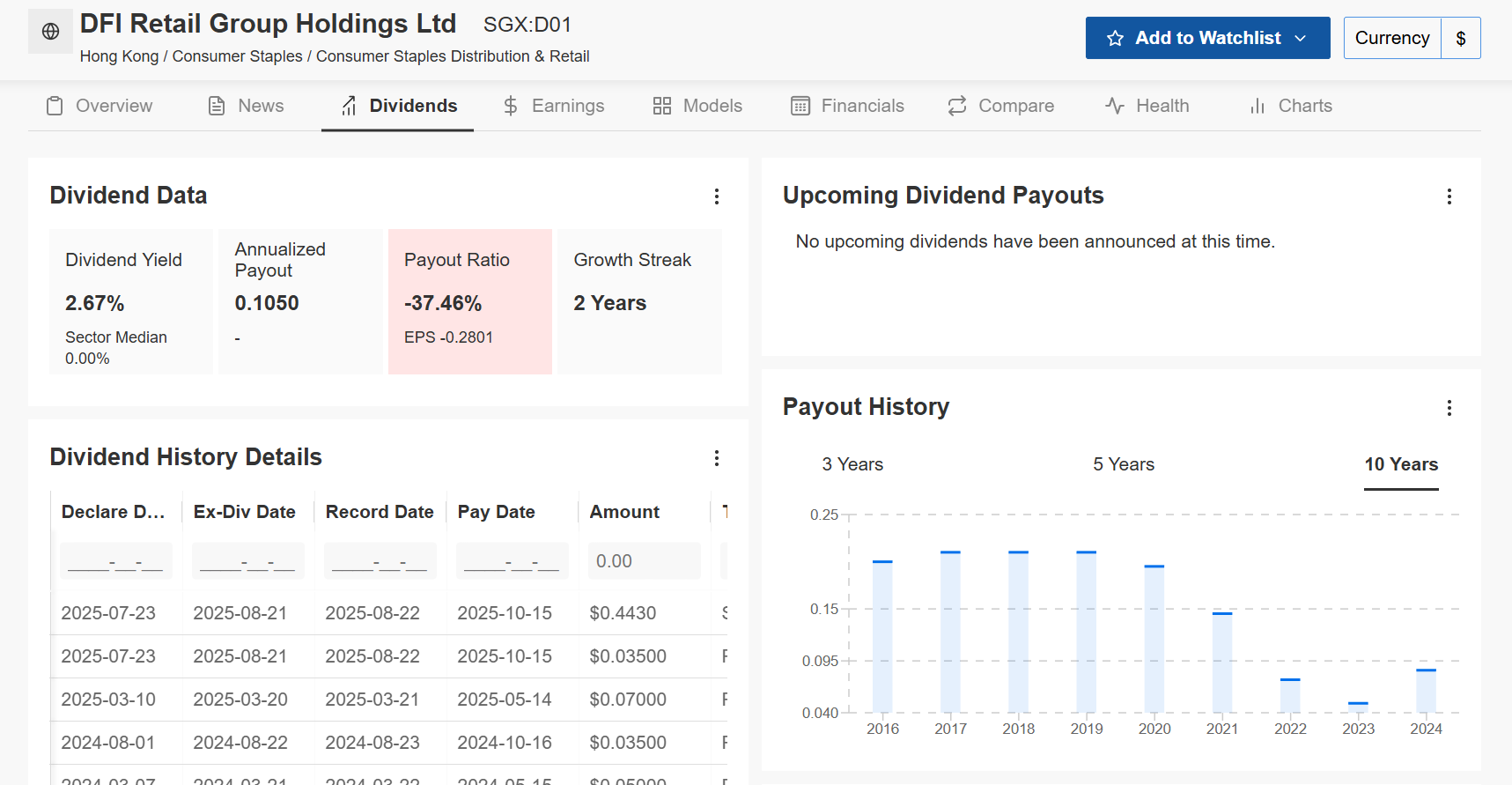

DFI has committed to increasing its dividend payout ratio from 60% to 70%. However, if you look at the raw data today, you might see a confusing picture. The current “Annualized Payout” sits at US$0.105, translating to a yield of roughly 2.67%.

Why the drop from the historical 3-4% yield? Two reasons:

Price Appreciation: The stock has rallied (the denominator got bigger).

Focus on Quality: We are looking at a sustainable base dividend, excluding the massive one-off “Special Dividends” (like the $0.4430 payout seen in late 2025 from asset sales).

The key for us isn’t the trailing yield—it’s the forward growth. If DFI hits its US$310-350 million profit target by 2028, that 2.67% yield on cost will grow rapidly.

The “InvestingPro” Data Check: Health vs. Hype

I don’t just guess at whether a turnaround is real. I check the institutional models to see if the fundamentals back the story. We have two critical data points here that tell the real story of DFI’s pivot.

Part A: The Dividend “Red Flag” That Isn’t

Source: InvestingPro by Investing.com (Data as of December 2025). Premium members can use code INVESTINGIGUANA for up to 50% off.

Iggy’s Insight: Don’t Let the “Negative” Fool You You’ll notice the Payout Ratio is -37.46% (Red Box). A novice investor sees this and panics, thinking the dividend is unfunded.

The Reality: The ratio is negative because reported earnings are negative due to non-cash write-downs from the Singapore food sale. Dividends are paid from Cash Flow, not accounting profits. The $0.105 payout is real, and the $0.443 special dividend in late 2025 proves management is willing to return cash to you.

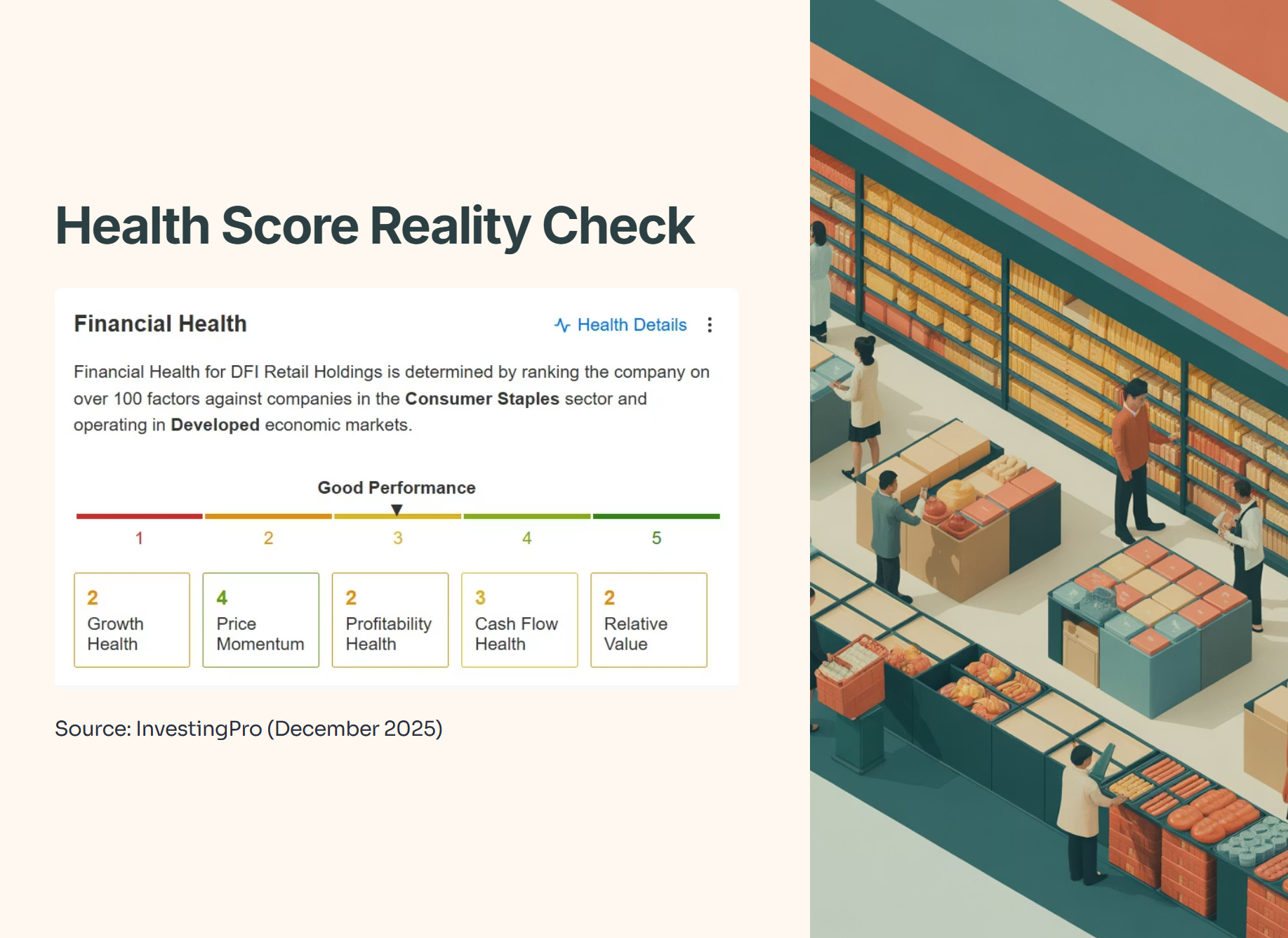

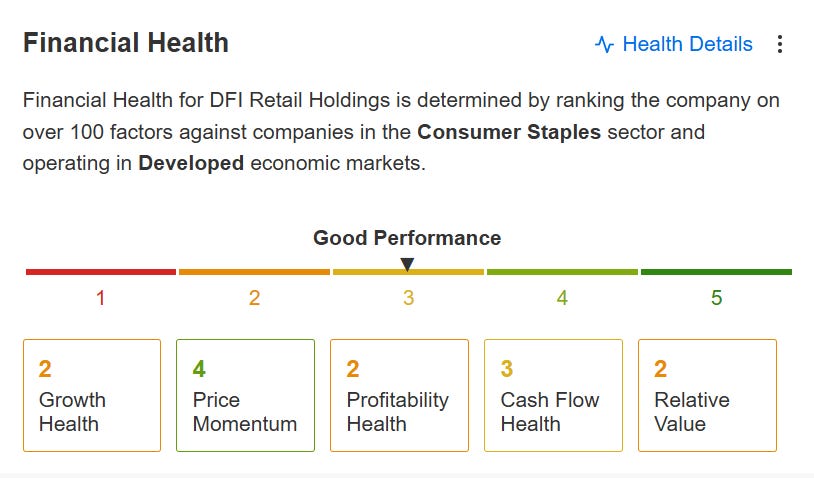

Part B: The Health Score Reality Check

Source: InvestingPro by Investing.com (Data as of December 2025). Premium members can use code INVESTINGIGUANA for up to 50% off.

The Analysis: This scorecard confirms my “Turnaround” thesis perfectly. If this were a stable blue-chip, you’d want to see 4s and 5s. But for a recovery play, this is exactly what we look for:

Price Momentum (4/5): The “Green” score confirms the market has woken up. The smart money is already accumulating, driving the price up. We are following the trend, not fighting it.

Profitability Health (2/5): This looks weak, but it’s backward-looking. It reflects the messy separation of the food business. We are buying for the future margin expansion, not the past mess.

Cash Flow Health (3/5): This is the safety net. A “3” is solid average. It means the company generates enough cash to sustain operations and the dividend, but it’s not a fortress yet. This validates our “Buy” rating but reinforces the need to keep position sizes moderate (4-5%).