Digital Core REIT Q3 2025: When a 40% Discount Meets Record-Low Data Centre Vacancy

Your REIT is trading at a steep discount. Meanwhile, AI demand is pushing data centre rents to all-time highs. What gives?

Digital Core REIT just dropped its Q3 2025 business and operational update, revealing numbers Singapore investors should not ignore. This is a data centre REIT holding prime properties in the world’s busiest markets – Northern Virginia, Frankfurt, Silicon Valley, and Osaka – yet the shares are nearly 40% below net asset value. That’s puzzling, given what’s happening on the ground: record-low vacancy rates, surging rental prices, and AI workloads needing more power than some countries.

I’m Iggy, your Singapore-based financial analyst and host of The Investing Iguana. I’ve spent years breaking down Singapore REITs and global real estate trends to help investors make sense of the numbers. Digital Core REIT is a name that consistently appears in value screeners: high yield, low price-to-book, but with real questions about execution and timing.

This deep dive takes you slide-by-slide through Digital Core REIT’s Q3 2025 report. I’ll unpack the key figures, explain market dynamics, and help you decide whether this discount is a buying opportunity or a value trap. By the end, you’ll know exactly where Digital Core REIT stands among Singapore data centre REITs – and if it deserves space in your CPF/SRS portfolio.

In This Article:

• Slide 1: Key Highlights

• Slide 2: Market and Portfolio Update—Northern Virginia

• Slide 3: Capitalizing on Favorable Fundamentals

• Slide 4: Discounted Valuation vs Peers

• Slide 5: Portfolio Overview

• Slide 6: Customer Profile

• Slide 7: Core Portfolio Performance

• Slide 8: Financial Overview

• Slide 9: Balance Sheet

• Slide 10: Debt Maturity & Interest Rate Sensitivity

• Regional Market Updates

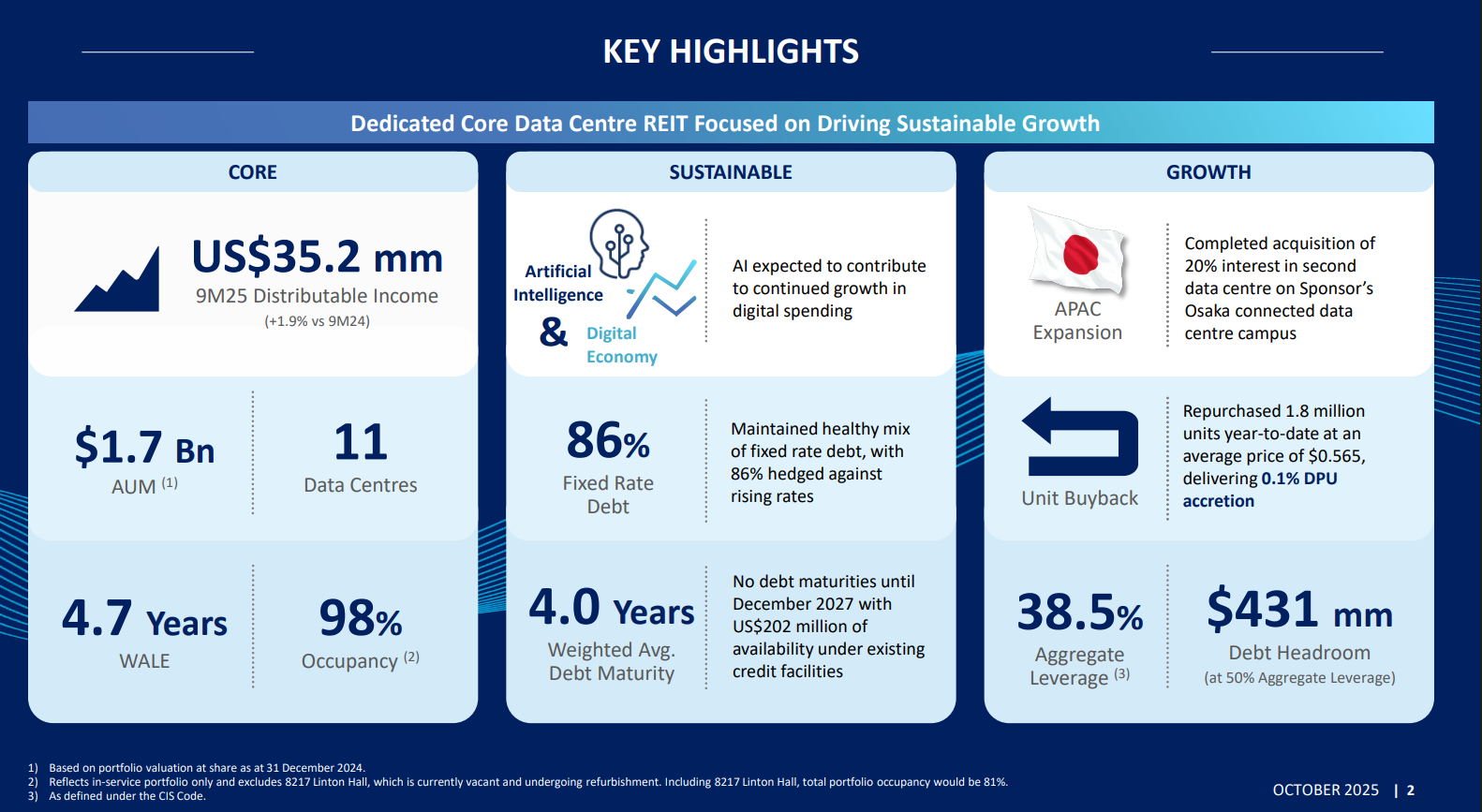

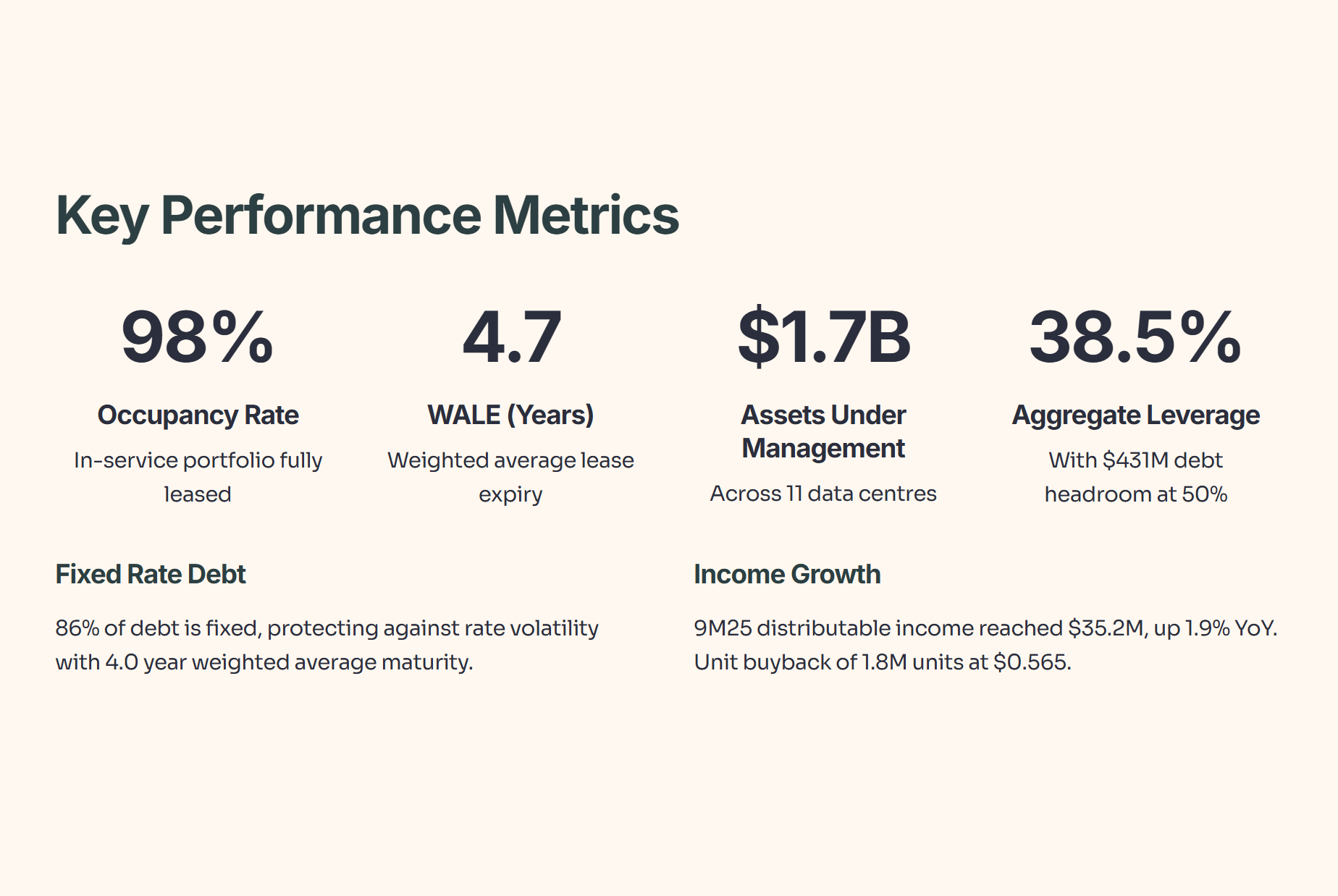

• Iggy’s Assessment: Buy, Hold, or Sell?Slide 1: Key Highlights

Digital Core REIT opened its Q3 2025 deck with a strong portfolio snapshot:

98% occupancy in its active properties

4.7 years weighted average lease expiry

11 data centres, USD 1.7 billion in assets under management

The REIT reported USD 35.2 million in distributable income for the first nine months of 2025, up 1.9% year-on-year. While not explosive, it’s a steady climb at a time when many REITs are still coping with higher interest costs.

On the balance sheet, leverage stands at 38.5%, with USD 431 million in debt headroom at the 50% cap. 86% of debt is fixed rate, shielding the REIT from further rate hikes. No maturities arrive until December 2027.

The REIT also expanded in the quarter, acquiring a stake in a new Osaka data centre – a smart play as Osaka emerges as Japan’s AI and cloud hub.

Lastly, management repurchased 1.8 million units at USD 0.565, signaling confidence in the share’s value.

Key Metrics Table:

High occupancy and long-term leases offer stability. The well-hedged debt and generous headroom mean management has flexibility for future growth.

Slide 2: Market and Portfolio Update—Northern Virginia

The Northern Virginia data centre is one of Digital Core REIT’s flagships. It sits on a 32-acre parcel, with enterprise-grade infrastructure for security, water feeds, and cooling.

Northern Virginia remains the world’s largest data centre market. Vacancy: almost zero. This environment gives landlords serious pricing power. The REIT’s facilities here represent 33% of annualized rent, all fully occupied.

AI workloads require much higher power – racks can draw up to 250 kW. Properties with sufficient water and cooling attract premium rents.

This regional portfolio includes Hastings Drive (fully fitted, 90% ownership, 100% occupied), Devin Shafron Drive (shell and core, also fully occupied), and Linton Hall Road, being refurbished for future leasing.

Northern Virginia Breakdown Table:

This market stands out for Singapore investors: ultra-low vacancy and top-tier tenants ensure stable, growing income – but also bind performance to US dynamics.

Slide 3: Capitalizing on Favorable Fundamentals

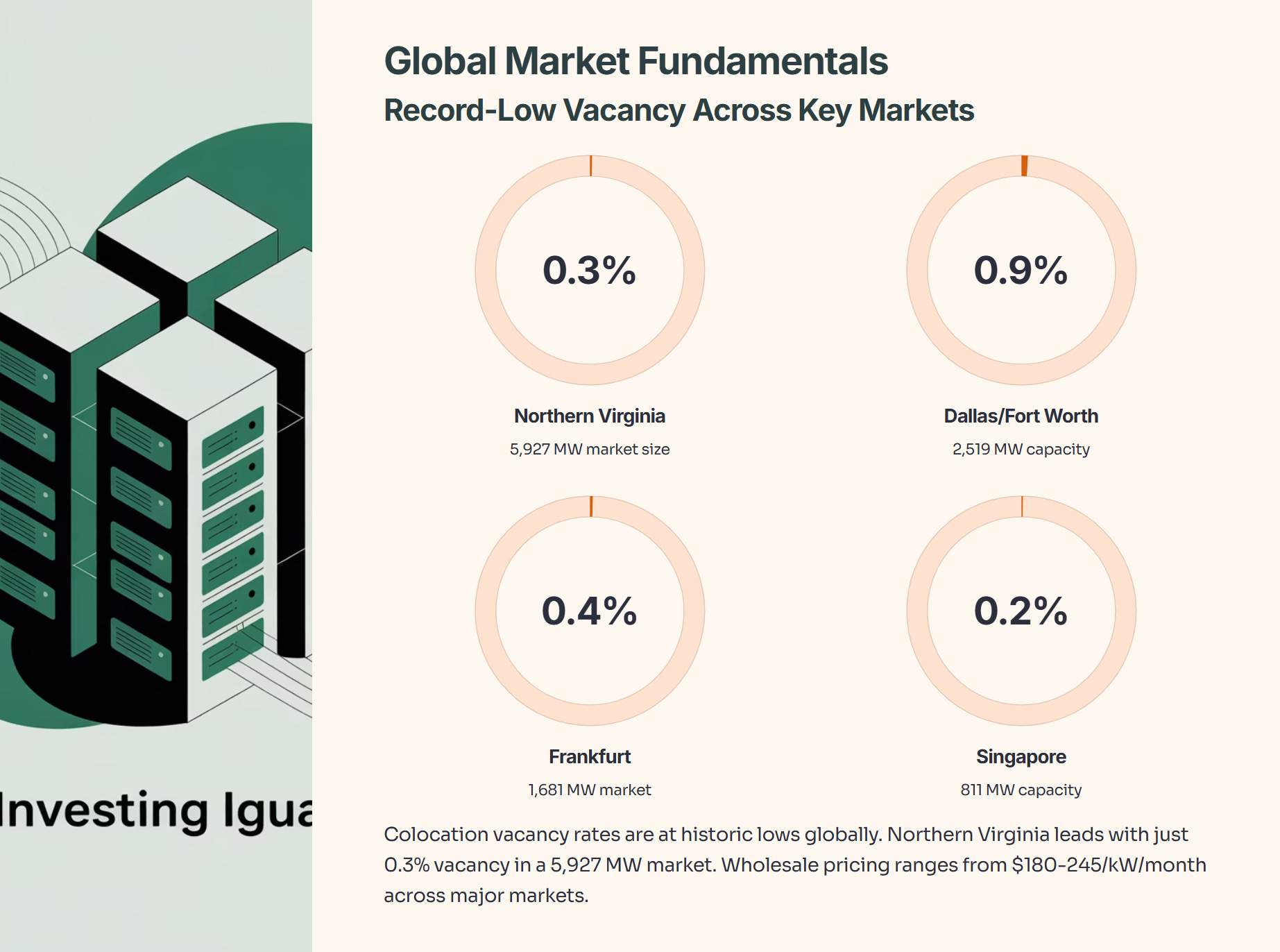

Market tailwinds are strong. Digital Core REIT operates in regions with record-low vacancy and rising rents. Land and capacity are scarce, setting up classic conditions for price appreciation.

Northern Virginia, Frankfurt, and Singapore lead the pack for low vacancy (ranging from 0.2% to 0.4%). Rents in these markets have surged, with Northern Virginia’s wholesale rates jumping from USD 130 to USD 180 per kW per month in one year.

Rising rents owe much to AI workloads, power constraints, and global regulatory hurdles. Building new data centres is getting harder, creating a moat around existing properties.

Comparable transactions in these markets support current valuations, so this is not just theoretical value; it’s backed by live deals.

Global Data Centre Snapshot Table:

Digital Core REIT’s exposure to high-demand hubs is rare. Whether the market rewards it or stays cautious will depend on execution.

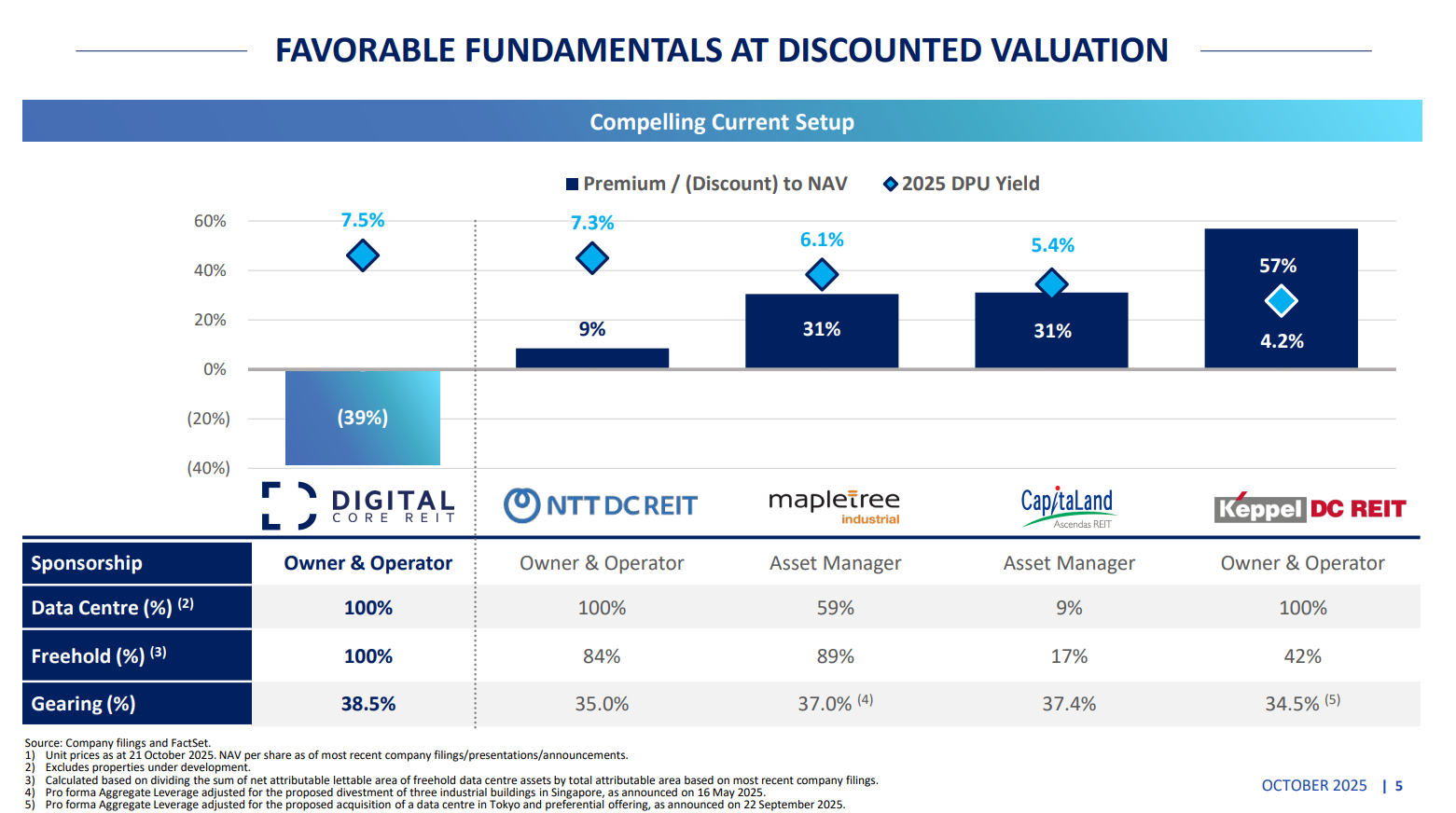

Slide 4: Discounted Valuation vs Peers

Digital Core REIT trades at a 39% discount to NAV, with a 7.5% yield. Contrast this with Keppel DC REIT (trades at a premium, 7.3% yield) and Ascendas or Mapletree Industrial (31% premium, lower yields).

Why the discount? It’s a smaller REIT (USD 1.7 billion AUM), less liquid, and has pure-play data centre exposure. Higher leverage (38.5% vs. 34–37% for peers) increases risk but also potential return.

DPU (distribution per unit) growth is modest at 1.9% this year; investors may need to see more before re-rating happens. Concerns about the sponsor relationship – possible conflicts around asset pricing – create caution.

Singapore Data Centre REITs Table:

This is a value investor’s setup: high yield, deep discount, and pure-play exposure.

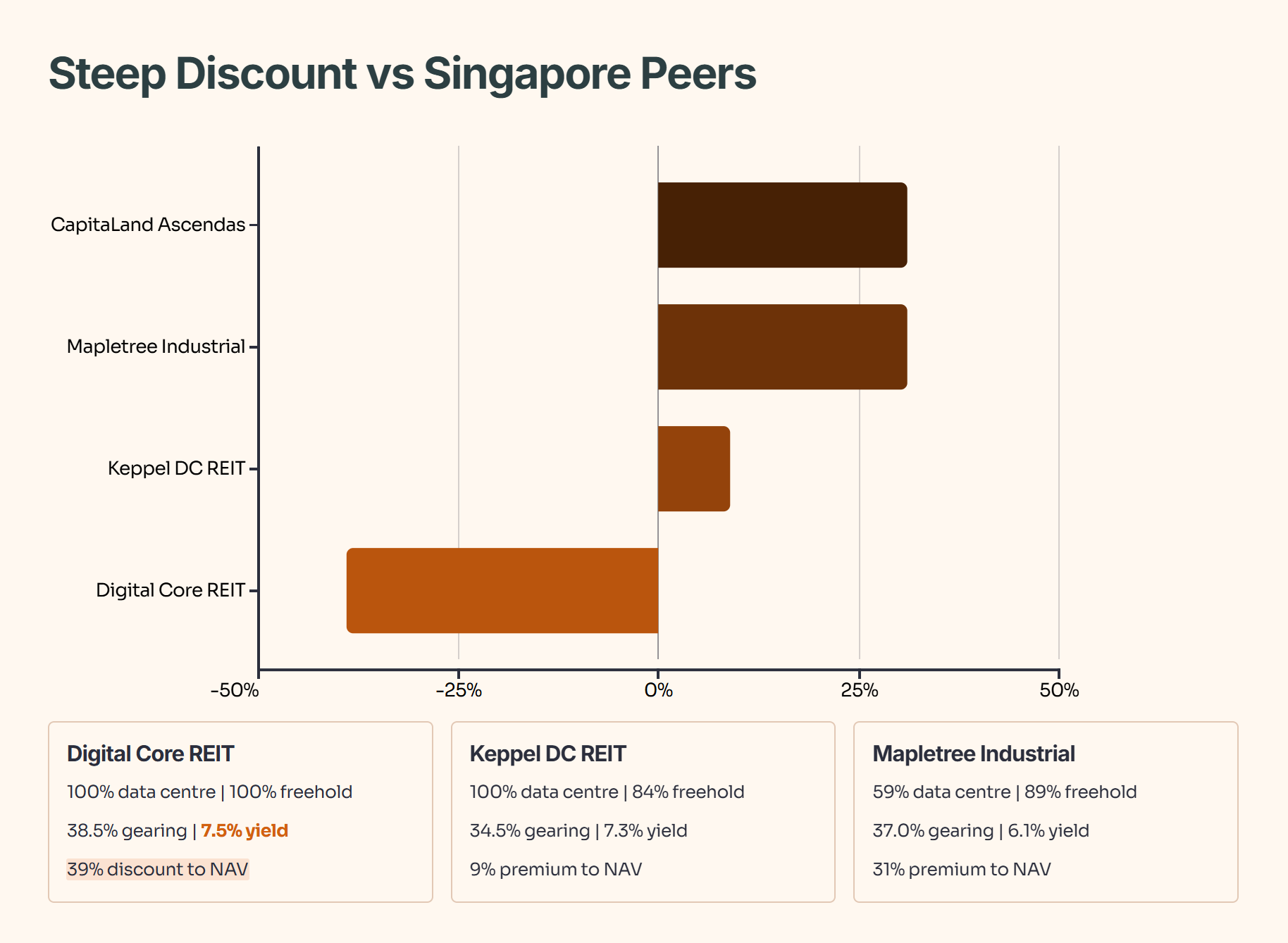

Slide 5: Portfolio Overview

Digital Core REIT’s portfolio includes 11 data centres across Northern Virginia, Silicon Valley, Toronto, Los Angeles, Frankfurt, and Osaka. All are 100% freehold – unlocking long-term value.

US markets dominate rent contribution (about half the portfolio), with Frankfurt (Europe) and Osaka (Asia) providing geographic diversity. Property breakdown: 84% fully fitted, 10% shell/core, 6% colocation. Triple net leases cover 63% of contracts, ensuring costs pass to tenants.

Lease expiries are well-laddered, with most rent locked in through 2031.

Portfolio Structure Table:

Lease structure and property mix give stability and income predictability.

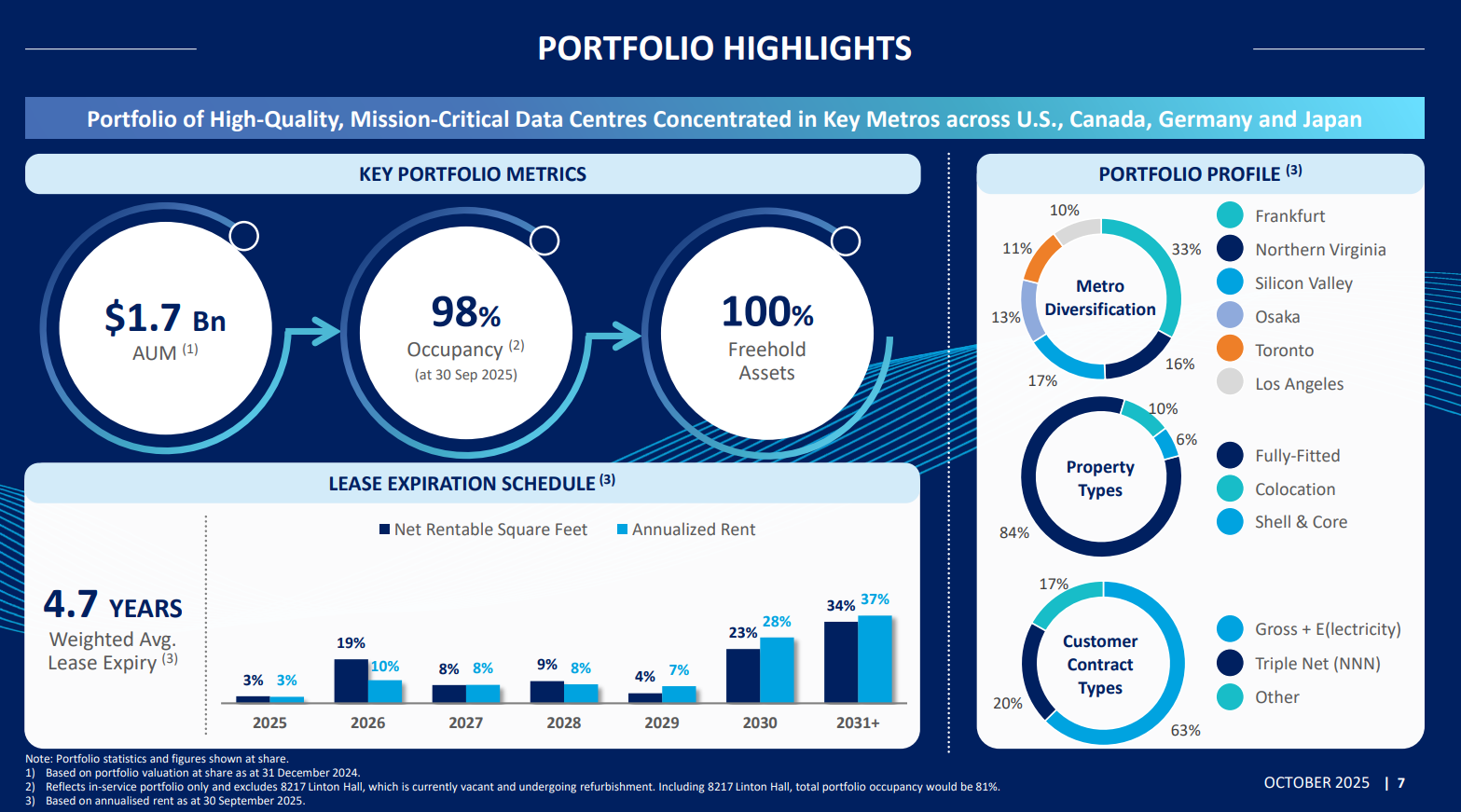

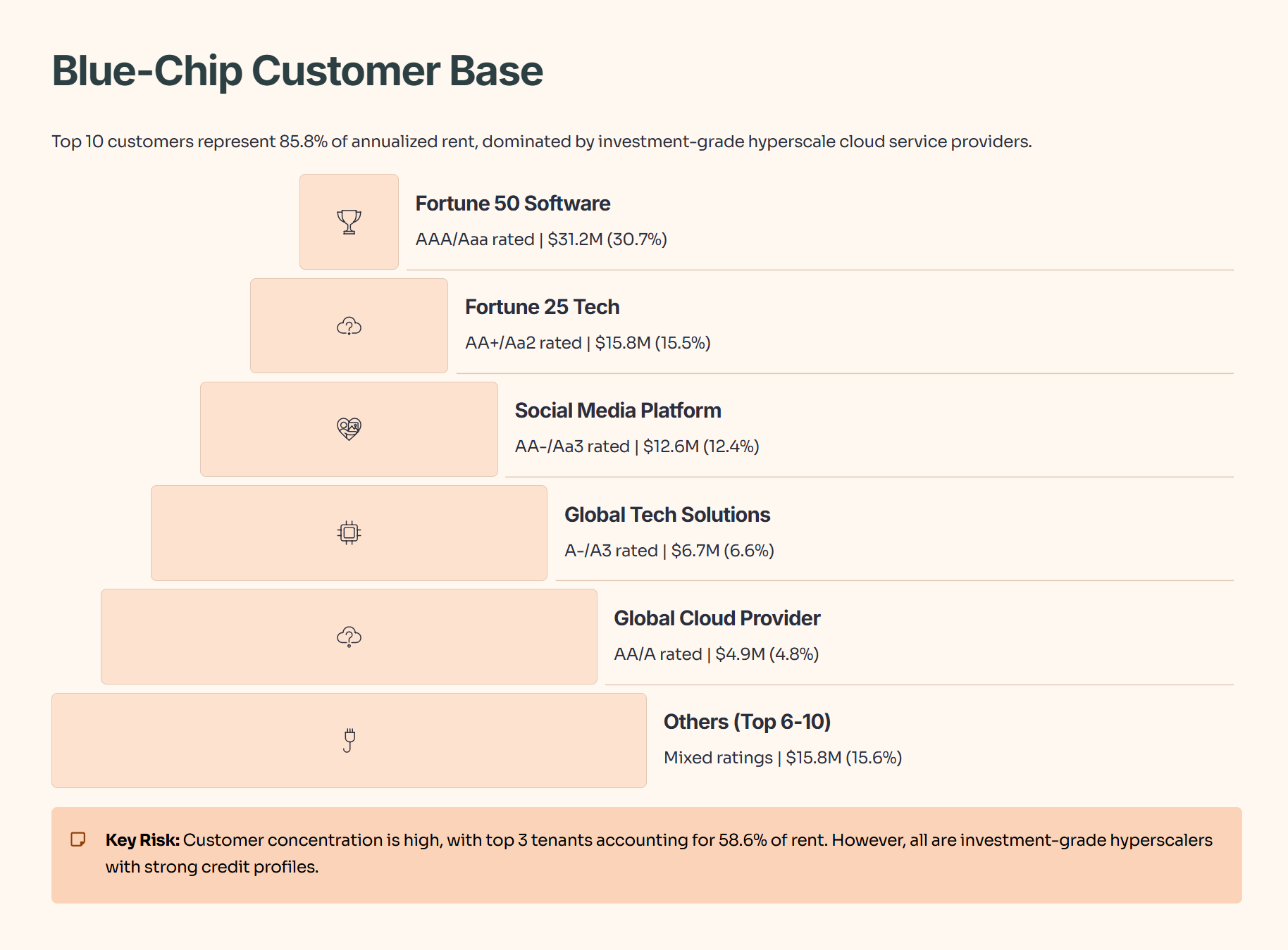

Slide 6: Customer Profile

Digital Core REIT serves over 120 customers; 79% of rent comes from investment-grade tenants. The top 10 clients provide nearly 86% of rent – dominated by Fortune 50 software and tech companies, plus leading social platforms.

Tenancy split: 61% hyperscale cloud providers, 33% colocation/IT, 6% social media/other. Triple net contracts with major tech firms lower risk of default.

Top 10 Customers Table:

Few tenants account for most income, but their credit strength and long leases lower the risk profile.

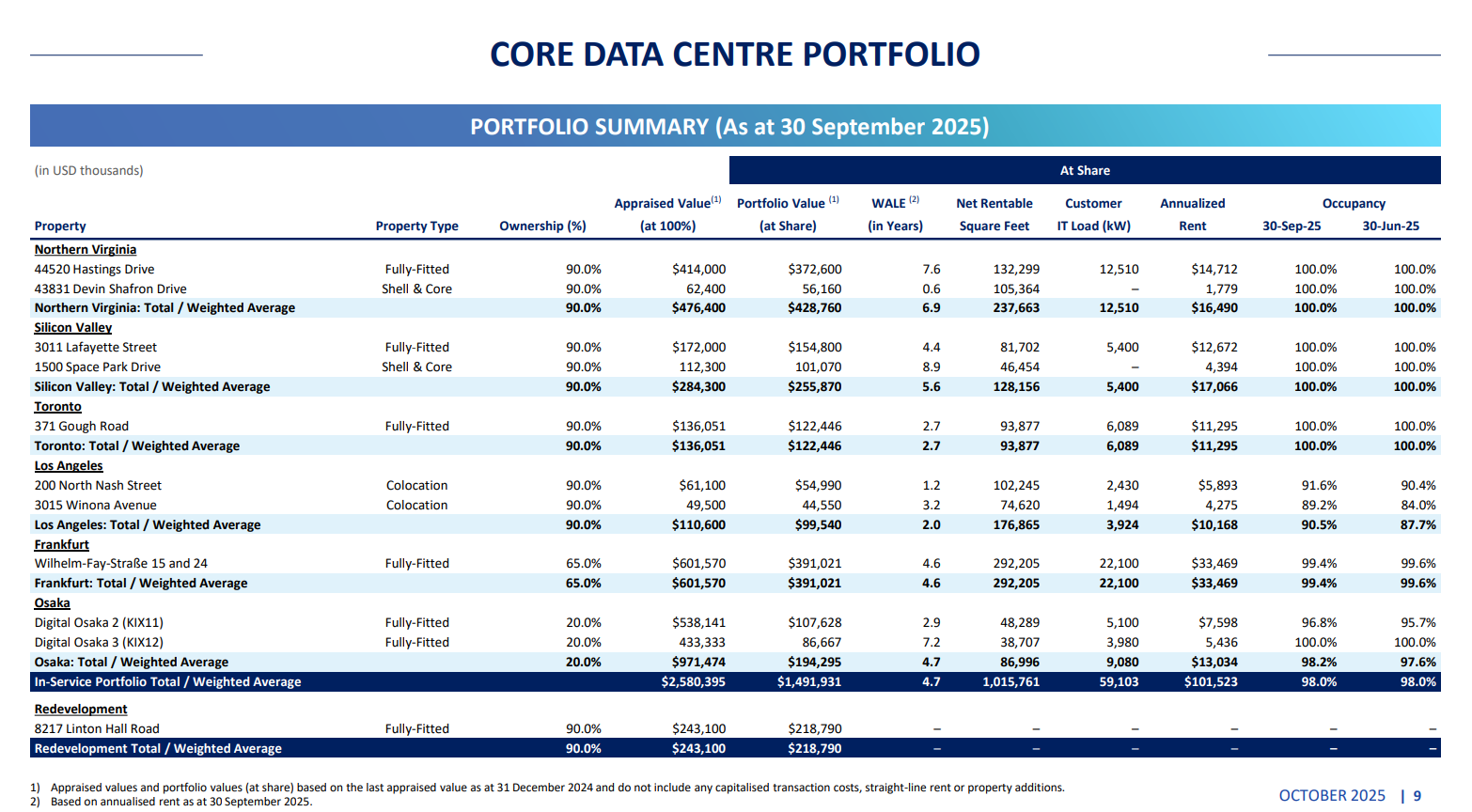

Slide 7: Core Portfolio Performance

Current assets: 10 operating properties, 1 redevelopment (Linton Hall). Portfolio value is USD 2.58 billion gross, USD 1.71 billion on the REIT’s share.

Northern Virginia and Frankfurt account for the highest rent contributions. Osaka and Silicon Valley offer expansion upside. Linton Hall, once leased at prevailing rates, could materially boost distributable income.

Portfolio Table:

98% occupancy, long WALE, 100% freehold delivers stable income and growth opportunity from refurbishments.

Slide 8: Financial Overview